May 21, 2026

The Processing Technology Gap Reshaping Critical Metals Supply Chains

For decades, the dominant assumption in critical minerals strategy was straightforward: find more deposits, build more mines, produce more metal. That logic held when ore grades were high, processing was predictable, and geopolitical supply chains were relatively stable. None of those conditions reliably apply today. The global metallurgical industry is confronting a structural mismatch between the feedstocks it has and the processing technologies it inherited, and that gap is increasingly where competitive advantage, investment capital, and national industrial strategy are converging.

Understanding why Boston Metal raises $75m for MOE tech matters requires understanding this broader context first. The company's latest financing round is not simply a funding milestone. It reflects a fundamental shift in how the metals industry is beginning to think about where supply chain resilience actually comes from.

When big ASX news breaks, our subscribers know first

Why Conventional Metallurgy Can No Longer Carry the Load

Traditional pyrometallurgical and hydrometallurgical processes were engineered during an era when rich, homogeneous ore bodies were abundant. Blast furnaces, smelters, and solvent extraction circuits perform well when feedstocks are consistent and high-grade. The problem is that the easy ore is largely gone, and what remains is increasingly complex, low-grade, or locked inside industrial waste streams that existing flowsheets cannot economically process.

The consequences of this mismatch are visible across multiple critical metals simultaneously:

- Niobium supply is concentrated to a degree that borders on a single-country dependency, with roughly 90% of global production originating from Brazil

- Tantalum carries conflict mineral exposure risks and geographic concentration that have repeatedly disrupted electronics supply chains

- Vanadium production is dominated by China, Russia, and South Africa, creating compounding geopolitical risk for Western industrial consumers

- Nickel has experienced extreme price volatility tied to Indonesian nickel supply risks and shifting demand profiles from the EV battery sector

Across all four metals, the underlying issue is the same: the combination of geographic concentration and processing technology limitations means that large volumes of potentially recoverable metal value remain stranded in materials that conventional methods cannot touch economically.

The critical metals sector is not simply facing a supply shortage. It is facing a processing technology gap. The ability to unlock metals from complex, low-grade, or secondary feedstocks is increasingly the defining competitive variable in supply chain strategy.

Molten Oxide Electrolysis: How the Technology Actually Works

Molten Oxide Electrolysis is an electrochemical metallurgical process in which metal oxides are dissolved into a molten oxide electrolyte bath and then reduced directly to liquid metal at the cathode using electrical current. There are no carbon-based reductants involved. When the electricity input comes from renewable sources, the process generates no direct CO2 emissions, which represents a fundamental departure from conventional smelting chemistry that has changed little in over a century.

The technical architecture of MOE creates capabilities that competing approaches cannot simultaneously replicate:

- Electrochemical selectivity: The process can target specific metal values within complex, multi-element oxide mixtures, a capability conventional smelting simply cannot achieve at comparable economics

- Feedstock flexibility: MOE operates across a wide range of metal oxide systems, including low-grade ores, metallurgical concentrates, and industrial waste streams such as tailings and slag

- Modular scalability: Electrolytic cell design supports incremental capacity expansion without requiring proportional jumps in capital expenditure, a meaningful advantage over large fixed-cost smelting infrastructure

- No intermediate reduction step: Unlike hydrogen-based direct reduction routes, which require hydrogen infrastructure and an intermediate processing stage, MOE converts metal oxides directly in the molten bath

Furthermore, critical minerals processing technology continues to evolve rapidly alongside MOE, and understanding the broader landscape of emerging approaches provides important context for evaluating where Boston Metal sits within a competitive field.

MOE's Two Commercial Application Tracks

Boston Metal has structured its commercial strategy around two parallel application pillars, each targeting a distinct but related market opportunity:

| Application | Target Output | Feedstock Type | Strategic Significance |

|---|---|---|---|

| Steel Decarbonisation | Zero-CO2 iron and steel | Iron ore | Addresses approximately 7–9% of global CO2 emissions from steelmaking |

| Critical Metals Recovery | Niobium, tantalum, vanadium, nickel | Low-grade ores, mining waste, metallurgical by-products | Unlocks stranded value; diversifies critical mineral supply |

This dual architecture matters from an investor perspective. Single-application deep-tech metallurgy ventures carry concentrated execution risk. A platform that can address both the decarbonisation of bulk metals production and the recovery of high-value critical metals from non-conventional feedstocks has a diversified commercial runway that most competing technologies lack entirely.

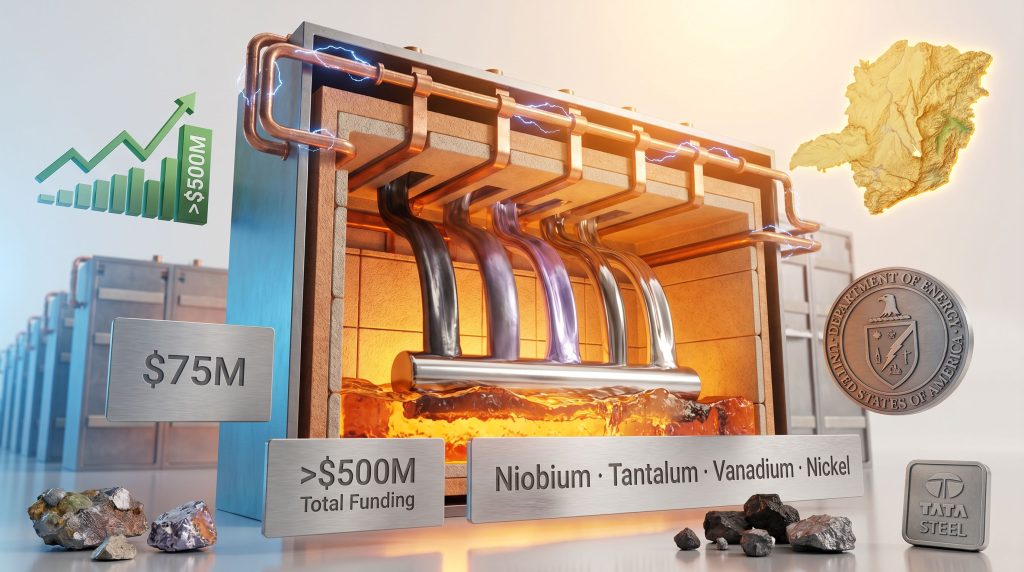

Breaking Down the $75 Million Round

Boston Metal raises $75m for MOE tech represents its latest financing milestone, bringing total cumulative funding to more than $500 million. The round includes Tata Steel as a new strategic contributor alongside existing institutional and strategic investors.

The Tata Steel participation deserves careful analysis rather than being treated as a routine line item. As one of the world's largest integrated steel producers, Tata Steel carries simultaneous exposure to both of MOE's commercial application tracks. The company has a direct strategic interest in decarbonising its own steelmaking operations, and it also faces supply chain risk from critical metal concentration in the same metals Boston Metal targets for MOE-based recovery.

Industrial anchor investors in deep-tech metallurgy rounds are analytically distinct from financial investors. Their participation typically signals that a technology has crossed from laboratory demonstration to credible commercial deployment readiness, evaluated against operational rather than purely financial criteria.

Cumulative Funding in Context

| Funding Stage | Capital Position | Strategic Significance |

|---|---|---|

| Pre-$75M rounds | Approximately $425M+ | Platform development, pilot-scale demonstration, early commercial deployments |

| Current round | Over $500M total | Commercial-scale deployment acceleration across US and international markets |

Crossing the $500 million cumulative threshold positions Boston Metal among the most heavily capitalised deep-tech metallurgy ventures globally. This is not merely a symbolic milestone. It reflects the capital intensity required to take a novel electrometallurgical platform through multiple rounds of institutional due diligence, engineering validation, pilot-scale demonstration, and into commercial production infrastructure.

Climate Investment technology director Rick Cutright has described this financing as a pivotal step, noting that Boston Metal has built a new metallurgical platform and demonstrated its ability to produce high-quality metals from complex feedstocks. The emphasis, as Cutright framed it, is now firmly on commercial production rather than further technological validation. Critical metals represent the right initial market because the demand urgency is immediate, the economics are attractive, and MOE can expand supply from materials that conventional processes systematically leave behind.

Where the Capital Goes: Active Facilities and Deployment Strategy

The $75 million will fund two parallel commercial tracks: additional commercial-scale MOE deployments targeting niobium, tantalum, vanadium, and nickel, and geographic expansion across US domestic manufacturing and international markets.

Boston Metal's active operational footprint currently includes:

- Minas Gerais, Brazil: An operational MOE critical metals facility where Boston Metal's global technical team works alongside local personnel. This facility represents real-world commercial production capability, not pilot-scale demonstration, and its location is strategically significant given Brazil's position as the dominant global niobium producer

- Weirton, West Virginia, USA: An advanced manufacturing plant selected by the US Department of Energy as a supported facility, connecting Boston Metal's commercial strategy to federal frameworks for domestic critical mineral processing and manufacturing onshoring

The Brazil facility placement is worth examining from a geological and supply chain perspective. Minas Gerais is home to some of the world's most significant niobium deposits, and the state has historically been the epicentre of global niobium production. Operating an MOE facility in this region gives Boston Metal proximity to both primary ore sources and the metallurgical expertise concentration that has developed around them over decades.

The Critical Metals Boston Metal Is Targeting and Why They Matter

The four metals at the centre of Boston Metal's commercial pipeline are not randomly selected. Each sits at the intersection of surging structural demand and constrained supply, creating the market conditions where a processing technology capable of unlocking non-conventional feedstocks carries genuine commercial advantage. Indeed, critical minerals and energy security have become inseparable strategic considerations for governments and investors alike.

| Metal | Primary End-Use Sectors | Supply Chain Risk Profile |

|---|---|---|

| Niobium | High-strength steel alloys, superconductors, EV battery anodes | ~90% of global supply concentrated in Brazil |

| Tantalum | Semiconductors, capacitors, aerospace components | Geographic concentration; conflict mineral exposure history |

| Vanadium | Vanadium redox flow batteries, steel strengthening agents | Supply dominated by China, Russia, South Africa |

| Nickel | EV battery cathodes, stainless steel, superalloys | Price volatility; Indonesian and Russian supply concentration |

A less commonly appreciated dynamic in this metals group is that demand is not growing uniformly or cyclically. Each metal is being pulled by structural, long-duration demand vectors simultaneously:

- Vanadium is increasingly central to grid-scale energy storage through vanadium redox flow battery systems, a technology whose deployment curve is directly tied to the global renewable energy buildout

- Tantalum demand is accelerating with AI infrastructure expansion, as tantalum capacitors are critical components in data centre hardware and advanced semiconductor packaging

- Niobium is gaining attention in next-generation battery research as a potential anode material that could offer faster charging and longer cycle life compared to conventional graphite-based anodes

- Nickel remains the highest-volume critical metal in EV battery cathode chemistry, with demand projections tied directly to the global passenger vehicle electrification timeline

The Low-Grade and Waste Feedstock Opportunity

Conventional metallurgy requires ore grades above minimum economic thresholds that exclude a large proportion of known global resources. These thresholds are not fixed by geology. They are fixed by processing economics. MOE's electrochemical selectivity shifts those thresholds downward, effectively expanding the addressable resource base without requiring new primary mining development at high-grade deposits.

Recovering metals from waste streams, including tailings, slag, and process residues from existing mining and smelting operations, offers a particularly compelling near-term commercial pathway. The capital requirements are lower than greenfield mine development, the feedstocks are already aggregated and partially characterised, and the recovery economics improve as the value of the target metals rises.

The next major ASX story will hit our subscribers first

How MOE Compares to Competing Technologies

| Technology Approach | CO2 Profile | Feedstock Flexibility | Commercial Maturity |

|---|---|---|---|

| Molten Oxide Electrolysis (MOE) | Zero direct emissions when renewable-powered | High: oxides, waste streams, low-grade materials | Commercial-scale deployment stage |

| Hydrometallurgy (solvent extraction) | Low to moderate | Moderate: requires soluble feedstocks | Mature commercial technology |

| Pyrometallurgy (conventional smelting) | High CO2 intensity | Low: grade-sensitive | Mature but facing decarbonisation pressure |

| Hydrogen Direct Reduction | Near-zero with green hydrogen | Low: primarily iron ore focused | Pilot to early commercial |

| Ionic liquid electrometallurgy | Low | Moderate | Pre-commercial research stage |

The competitive position MOE occupies is specific and difficult to replicate. It simultaneously delivers zero-emission potential and high feedstock flexibility, a combination that no other approach at equivalent commercial maturity currently achieves. Consequently, mining electrification and decarbonisation trends are increasingly pointing towards electrochemical platforms like MOE as the most viable long-term pathway for the industry. Boston Metal CEO Tadeu Carneiro has articulated this strategic framing directly, describing critical metals as the new strategic commodities and emphasising that what the world requires is not simply more metal production but smarter and more adaptable production methods.

Frequently Asked Questions: Boston Metal and MOE Technology

What is Molten Oxide Electrolysis?

MOE is an electrochemical metallurgical process that uses electricity to reduce metal oxides directly to liquid metal within a molten oxide electrolyte bath, without any carbon-based reductants. When powered by renewable electricity, the process produces no direct CO2 emissions and can process a broad range of feedstocks including low-grade ores and industrial waste materials.

How much has Boston Metal raised in total?

As of May 2026, Boston Metal has raised more than $500 million in total cumulative funding, including the most recent $75 million round. For further detail on the announcement, the latest funding round has been covered extensively across industry and investment media.

Which critical metals does MOE target commercially?

Boston Metal's commercial pipeline centres on niobium, tantalum, vanadium, and nickel, all of which share a profile of high structural demand growth and constrained conventional supply.

Why is Tata Steel participating in this round?

Tata Steel's involvement reflects strategic exposure to both MOE application tracks: decarbonising its own steelmaking operations and securing supply chain optionality for critical metals inputs across its manufacturing operations.

What makes MOE different from conventional smelting?

Conventional smelting uses carbon as a chemical reductant, generates significant CO2, and requires relatively high-grade, consistent feedstocks. MOE uses electricity as both energy source and reductant, operates without direct carbon inputs, and can process heterogeneous, low-grade, or waste-derived feedstocks that conventional processes cannot handle economically.

Five Strategic Implications for Industry Observers

- Processing technology is becoming a supply chain asset class. MOE's ability to unlock value from non-conventional feedstocks reframes supply chain resilience as a technology investment, not just a mining geography question

- Industrial anchor investors signal commercial readiness. Tata Steel's participation elevates Boston Metal's credibility beyond venture-stage positioning into territory evaluated against operational deployment criteria

- The $500 million funding threshold carries analytical weight. It reflects multiple rounds of institutional due diligence survival and the capital scale required for commercial metallurgical infrastructure

- Waste stream processing is an underappreciated near-term commercial pathway. Recovery from tailings, slag, and process residues offers lower capital requirements than greenfield development while targeting the same high-value metals

- Demand fundamentals across the four target metals are structural and long-duration. Electrification, AI infrastructure expansion, grid-scale energy storage, and advanced defence manufacturing are not cyclical demand drivers. They are decade-scale structural forces that support the multi-year commercialisation timelines inherent to deep-tech metallurgy investment

Disclaimer: This article is intended for informational purposes only and does not constitute financial or investment advice. Forward-looking statements regarding technology commercialisation, market demand, and company performance involve inherent uncertainties and assumptions. Readers should conduct independent research and consult qualified advisers before making any investment decisions.

Want To Stay Ahead Of The Next Major Critical Minerals Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries across niobium, vanadium, nickel, and beyond — turning complex mineral data into actionable investment insights the moment they're announced. Explore historic discoveries and their returns or start your 14-day free trial today to position yourself ahead of the broader market.