July 28, 2026

Understanding the Strategic Value of Botswana's Critical Minerals Landscape

The global energy transition has transformed critical minerals from industrial commodities into strategic national assets. As governments worldwide scramble to secure supply chains for technologies that will define the next century, a rare earth discovery in Botswana's northwest region signals a potential shift in the geopolitical balance of power surrounding rare earth elements.

The minerals sector stands at a crossroads where geology meets geopolitics, and where the distribution of underground resources increasingly determines above-ground influence. This intersection has never been more pronounced than in the current era of technological transformation, where the components of electric vehicles, wind turbines, and advanced electronics depend on elements that exist in only a handful of locations worldwide.

When big ASX news breaks, our subscribers know first

Why Rare Earth Elements Drive Modern Geopolitical Competition

Rare earth elements form the backbone of modern technological society, despite their name suggesting scarcity when they are actually relatively abundant in the Earth's crust. The challenge lies not in their availability but in their concentration and the complex processes required to extract and refine them into usable forms.

These 17 elements, including neodymium, dysprosium, and terbium, enable the miniaturisation and efficiency gains that make contemporary electronics possible. Electric vehicle motors rely on permanent magnets crafted from rare earth elements, while wind turbines require these materials for generators that can operate reliably for decades.

Defence applications extend from missile guidance systems to radar components, creating a direct link between mineral access and national security capabilities. Consequently, governments worldwide are reassessing their critical minerals strategy to reduce dependencies on single-source suppliers.

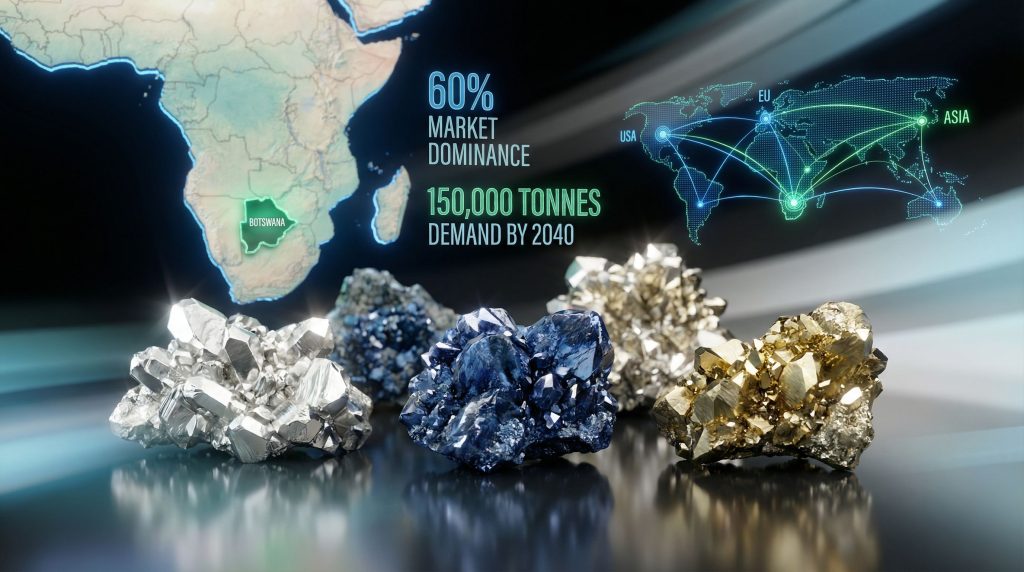

Current global production patterns reveal significant concentration risks. China maintains processing dominance through entities such as China Northern Rare Earth Group, a position that Western governments increasingly view as a strategic vulnerability.

This concentration emerged through decades of industrial development, environmental risk acceptance, and integrated supply chain construction that competitors now struggle to replicate. Furthermore, global trade tensions have heightened awareness of the risks associated with supply chain concentration.

The strategic importance becomes clearer when considering supply disruption scenarios. Manufacturing delays in electric vehicle production, wind turbine deployment bottlenecks, and defence electronics supply chain vulnerabilities all stem from this geographical concentration of processing capabilities.

Botswana's Emerging Position in African Critical Minerals Geography

Botswana enters this strategic landscape with distinct advantages shaped by decades of mineral sector development and institutional capacity building. The country's reputation as one of Africa's most mining-friendly jurisdictions stems from established infrastructure, clear regulatory frameworks, and a demonstrated track record of successful partnerships.

| African Rare Earth Projects | Development Stage | Estimated Timeline | Key Minerals |

|---|---|---|---|

| Gchwihaba, Botswana | Exploration/Feasibility | 2026-2028 | All 15 REE + polymetallics |

| Rainbow, South Africa | Production | Operating | Light REE concentrate |

| Longonjo, Angola | Construction | 2027-2029 | Heavy REE focus |

| Wigu Hill, Tanzania | Exploration | 2027-2030 | Niobium-REE complex |

The broader African context reveals increasing competition for exploration rights and long-term supply agreements. Countries including Namibia, Tanzania, and the Democratic Republic of Congo have attracted attention from both Western and Chinese firms seeking to secure future mineral supplies.

However, Botswana's regulatory stability and infrastructure development provide competitive advantages in this regional landscape. The government's strategic pivot toward base metals, coal, and critical minerals exploration represents a deliberate effort to reduce economic dependence on diamond revenues.

According to the Botswana Chamber of Mines, this diversification strategy aims to attract foreign investment while leveraging existing mining sector expertise and infrastructure. Moreover, this approach aligns with broader energy transition security objectives pursued by international partners.

How Does the Gchwihaba Discovery Compare to Global Rare Earth Deposits?

The technical specifications of Botswana's rare earth discovery in the northwest region near Shakawe reveal characteristics that could influence both development timelines and commercial viability. Understanding these geological factors provides insight into the project's potential role within global supply chains.

Technical Specifications of the Polymetallic System

Geological surveys conducted at the Gchwihaba Metals project identified mineralisation through systematic exploration combining geophysical methods with diamond core drilling confirmation. Ground magnetic and gravity surveys initially detected anomalies designated as targets C26 and C27, which subsequent drilling confirmed as hosting skarn-type mineralisation.

The mineral system extends from 20 to 50 metres below surface, a relatively shallow depth that could reduce extraction costs compared to deeper deposits requiring more intensive mining infrastructure. This accessibility factor becomes particularly relevant when evaluating capital requirements and operational complexity against competing projects globally.

Complete Mineral Portfolio Discovery:

- All 15 rare earth elements from the U.S. Geological Survey's 2025 Critical Minerals List

- Five additional strategic metals: copper, cobalt, nickel, vanadium, and silver

- Skarn-type mineralisation confirmed through diamond core drilling

Skarn deposits form through contact metamorphism between intrusive igneous rocks and carbonate-rich sedimentary formations. This geological setting often produces concentrated mineral zones with distinct spatial patterns that can facilitate selective mining and processing approaches. The polymetallic nature of the discovery adds complexity but also potential revenue diversification through multiple commodity streams.

Production Potential Scenarios Under Different Development Timelines

Development scenario modelling reveals the relationship between capital investment, regulatory approval timelines, and market entry strategies. Each pathway presents distinct risk-return profiles that influence investor decision-making and government policy responses.

| Development Scenario | Timeline | Capital Requirements | Production Capacity | Market Impact |

|---|---|---|---|---|

| Conservative | 5-7 years | $800M-1.2B | Moderate scale | Limited disruption |

| Moderate | 3-5 years | $1.2B-1.8B | Commercial scale | Regional influence |

| Accelerated | 2-3 years | $1.8B-2.5B | Large scale | Global significance |

The accelerated development scenario assumes streamlined regulatory processes, immediate access to development capital, and coordinated infrastructure investment. However, this pathway also carries elevated execution risks and potential environmental or community engagement challenges that could delay progress.

Processing methodology selection significantly influences both development costs and market positioning. Skarn deposits often respond well to conventional mineral processing techniques, but the polymetallic nature requires careful metallurgical design to optimise recovery rates.

What Strategic Advantages Does This Discovery Offer Western Supply Chains?

The geopolitical implications of Botswana's rare earth discovery extend beyond mineral economics to encompass supply chain security considerations that influence national policy decisions across Western nations. Understanding these strategic dimensions reveals why governments view mineral diversification as essential to technological sovereignty.

Diversification Away from Chinese Processing Dominance

Western dependency on Chinese rare earth processing infrastructure creates vulnerabilities that policymakers increasingly recognise as unacceptable strategic risks. Current supply chain analysis reveals that disruption scenarios could cascade through multiple industrial sectors simultaneously, affecting everything from consumer electronics to national defence capabilities.

The concentration of processing capacity in China emerged through systematic industrial development over several decades, combining environmental risk acceptance with integrated supply chain construction. Replicating this infrastructure elsewhere requires substantial capital investment, technical expertise transfer, and coordinated policy support.

Hypothetical Supply Disruption Impact Analysis:

- Electric vehicle production delays affecting climate transition timelines

- Wind turbine manufacturing bottlenecks limiting renewable energy deployment

- Defence electronics supply shortages compromising military readiness

- Consumer electronics price increases reducing technology adoption rates

- Industrial automation delays affecting manufacturing competitiveness

Botswana's political stability provides a crucial differentiator compared to other potential supply sources. The country's democratic institutions, rule of law frameworks, and established mining sector governance create predictable operating environments that reduce investment risks.

Integration with Existing North American and European Supply Networks

Transportation logistics analysis reveals both opportunities and challenges for integrating Botswana's mineral production with Western processing facilities. Geographic positioning requires careful consideration of shipping routes, port infrastructure capacity, and regional processing capabilities.

| Supply Route | Distance | Transit Time | Infrastructure Requirements | Estimated Costs |

|---|---|---|---|---|

| Botswana-Europe | 8,500 km | 21-28 days | Port expansion needed | $85-120/tonne |

| Botswana-North America | 15,200 km | 35-42 days | Existing infrastructure | $140-180/tonne |

| China-Europe (current) | 18,000 km | 28-35 days | Established networks | $95-130/tonne |

| China-North America | 11,500 km | 21-28 days | Established networks | $110-145/tonne |

The development of regional processing hubs represents a potentially transformative approach to addressing transportation cost challenges while building industrial capacity within southern Africa. Furthermore, this strategy could reduce dependency on long-distance shipping whilst creating employment opportunities.

Processing facility location analysis suggests that establishing intermediate processing capabilities in Botswana or neighbouring countries could optimise the balance between transportation costs and processing efficiency. However, such development requires coordinated investment in power generation, water infrastructure, and skilled workforce development.

How Will This Discovery Impact Botswana's Economic Diversification Strategy?

Botswana's economic transformation efforts reflect broader challenges facing resource-dependent nations seeking to reduce vulnerability to commodity price volatility whilst building sustainable development foundations. The rare earth discovery in Botswana provides opportunities to apply lessons learned from successful economic diversification models implemented elsewhere.

Beyond Diamonds: Building a Multi-Commodity Mining Economy

The country's historical relationship with diamond mining through De Beers Group established institutional frameworks and technical capabilities that provide foundations for expanding into other mineral sectors. However, transitioning from single-commodity dependence to diversified mineral production requires different operational approaches and mining investment strategies.

Economic diversification analysis from resource-rich nations demonstrates both successful and unsuccessful transition models. Norway's evolution from oil-dependent economy to renewable energy leader illustrates how resource revenues can fund transition investments whilst building alternative economic foundations.

Key Economic Transition Requirements:

- Revenue stabilisation through multiple commodity streams reducing price volatility exposure

- Foreign exchange earnings diversification supporting currency stability

- Employment diversification creating opportunities across different skill levels

- Technology transfer and capacity building developing local expertise

- Sovereign wealth fund development preserving mineral revenues for future generations

Government policy frameworks indicate prioritisation of exploration for base metals, coal, and critical minerals as components of broader economic diversification efforts. This strategic approach recognises both the opportunities and risks associated with natural resource development in an increasingly complex global economy.

Foreign Investment Attraction and Technology Transfer Opportunities

Mining sector foreign direct investment patterns reveal increasing competition among nations to attract exploration and development capital. Botswana's regulatory framework and institutional capacity provide competitive advantages, but successful investment attraction requires coordinated policy development and infrastructure investment.

Government Policy Incentives for Critical Mineral Development:

- Competitive tax structures designed to attract international mining companies

- Streamlined regulatory processes reducing development timeline uncertainties

- Infrastructure development commitments supporting mining sector expansion

- Skills development programmes building local workforce capabilities

- Environmental protection frameworks balancing development with conservation

Partnership models with Western mining companies and technology providers offer pathways for accessing both capital and technical expertise necessary for complex rare earth processing operations. These relationships can facilitate technology transfer whilst ensuring compliance with international environmental and social governance standards.

International development finance institutions increasingly recognise critical minerals as strategic priorities worthy of concessional financing and technical assistance. In addition, this policy environment creates opportunities for blended finance approaches that combine commercial investment with development funding.

The next major ASX story will hit our subscribers first

What Are the Potential Challenges and Risk Factors?

Comprehensive risk assessment reveals multiple categories of challenges that could influence development outcomes and investment returns. Understanding these risk factors enables stakeholders to develop appropriate mitigation strategies and contingency planning approaches.

Technical and Financial Development Hurdles

Capital requirements for rare earth extraction and processing represent substantial financial commitments that require careful structuring and risk management. Industry analysis suggests that integrated rare earth projects typically require $800 million to $2.5 billion in development capital, depending on scale and processing complexity.

Environmental impact assessment requirements involve comprehensive studies of water usage, tailings management, air quality impacts, and biodiversity protection measures. These assessments typically require 18-36 months to complete and can identify design modifications that influence both costs and development timelines.

| Risk Category | Probability | Impact Level | Mitigation Strategies |

|---|---|---|---|

| Technical/Geological | Medium | High | Extensive drilling, metallurgical testing |

| Financial/Market | Medium | High | Diversified funding, long-term contracts |

| Regulatory/Environmental | Low | Medium | Early engagement, compliance frameworks |

| Geopolitical/Trade | Low | High | Political risk insurance, diversified markets |

Community engagement protocols require sustained consultation with local populations, traditional authorities, and civil society organisations throughout project development phases. Experience from other African mining projects demonstrates that inadequate community engagement can result in significant delays and increased costs.

Geopolitical Response Scenarios from Competing Powers

Strategic competition for critical mineral resources creates complex diplomatic and economic dynamics that influence project development beyond purely commercial considerations. Understanding potential geopolitical responses enables stakeholders to prepare for various scenarios whilst maintaining operational flexibility.

Hypothetical Chinese Counter-Investment Strategies:

- Competing infrastructure development offers through Belt and Road Initiative funding

- Direct investment proposals with accelerated development timelines

- Technology transfer agreements providing processing expertise

- Long-term supply agreements offering premium pricing for exclusive access

- Regional partnership development creating alternative supply chain networks

Historical precedents in African critical mineral sectors demonstrate how geopolitical competition can both accelerate development through increased investment and complicate project execution through competing stakeholder pressures. Successful navigation requires diplomatic skills alongside technical and commercial expertise.

Western government support mechanisms include development finance programmes, technical assistance, and political risk insurance designed to encourage private sector investment in strategic mineral projects. These instruments can reduce project risks whilst ensuring alignment with broader policy objectives.

What Does This Mean for Global Rare Earth Market Dynamics?

Market impact analysis requires consideration of both supply-side changes and demand-side growth projections to understand how Botswana's discovery could influence global pricing and trade patterns. The International Energy Agency projects that demand for key critical minerals could more than double by 2030 under current energy transition policies.

Supply-Demand Rebalancing Implications

Global rare earth demand growth stems primarily from energy transition technologies and advanced manufacturing applications. Electric vehicle deployment alone could require 150,000 tonnes of rare earth elements annually by 2040, representing substantial increases from current consumption levels.

Market Impact Timeline:

-

2026-2028: Exploration and Feasibility Phases

- Limited market impact during technical studies

- Investment sentiment improvement for African mining

- Preliminary supply agreement negotiations

-

2029-2031: Construction and Early Production

- Gradual market share capture beginning

- Price volatility reduction through supply diversification

- Supply chain relationship development

-

2032-2035: Full Production Integration

- Meaningful contribution to global supply security

- Established processing and logistics networks

- Long-term price stabilisation effects

Market dynamics analysis suggests that new supply sources typically require 3-5 years to achieve full market integration after commercial production begins. This timeline reflects the conservative nature of industrial supply chains and the extensive qualification processes required for critical applications.

Price Stability and Strategic Reserve Considerations

Rare earth price volatility historically stems from supply concentration and the limited substitutability of these elements in critical applications. Price fluctuations can range from 50-200% over 12-18 month periods, creating significant challenges for both producers and consumers in long-term planning.

Strategic reserve policies implemented by Western governments aim to buffer against supply disruptions whilst providing market stability during transition periods. The United States maintains strategic stockpiles of critical minerals, whilst the European Union has proposed similar reserve systems.

| Global Region | Production Costs ($/kg REO) | Processing Capacity | Market Position |

|---|---|---|---|

| China | $8-15 | Dominant | Integrated supply chains |

| Australia | $12-22 | Limited | Mining focus |

| United States | $15-28 | Rebuilding | Strategic development |

| Africa (projected) | $10-18 | Developing | Emerging supplier |

Investment implications for rare earth-dependent industries include supply chain diversification strategies, long-term contract negotiations, and potential backward integration into mineral production. Companies heavily dependent on rare earth inputs increasingly evaluate vertical integration options to reduce supply security risks.

How Does This Fit Into Africa's Broader Critical Minerals Strategy?

Continental resource development strategies reflect growing recognition among African governments that natural resource endowments represent opportunities for industrial development rather than merely export revenue generation. This perspective shift influences policy frameworks and international partnership approaches across the continent.

Continental Resource Sovereignty Movement

The African Union's critical minerals development framework emphasises value addition requirements and local processing mandates designed to capture more economic benefits from natural resource endowments. This approach builds upon lessons learned from decades of raw material export dependence that generated limited industrial development.

Zimbabwe's recent decision to ban raw material exports exemplifies this value-addition approach, though implementation challenges demonstrate the complexity of transitioning from export-oriented to processing-focused mineral strategies. Such policies require substantial infrastructure investment and technical capacity development to succeed.

Case Study Analysis: Zimbabwe's Raw Materials Export Ban

- Mandatory local processing requirements for all mineral exports

- Foreign exchange retention policies encouraging value addition

- Infrastructure development requirements for processing facilities

- Employment creation mandates for mining operations

- Technology transfer requirements for international partnerships

Botswana's approach appears more gradual, balancing value addition objectives with practical development constraints and investor risk management. This methodology recognises that successful industrial development requires coordinated investment in infrastructure, skills development, and market access simultaneously.

Regional Infrastructure Development Requirements

Transportation corridor development represents a critical enabler for African critical minerals development, as many deposits exist in areas with limited infrastructure connectivity. Regional coordination through the Southern African Development Community (SADC) could optimise infrastructure investment whilst creating economies of scale.

Power generation requirements for mineral processing operations often exceed local grid capacity, necessitating coordinated energy infrastructure development. Botswana's coal resources and solar potential provide foundations for developing adequate power supply, but substantial investment and planning coordination are required.

Southern African Development Community (SADC) Integration Opportunities:

- Cross-border transportation infrastructure connecting mineral projects to ports

- Regional power grid development supporting energy-intensive processing

- Coordinated technical education programmes building specialised workforce capabilities

- Joint procurement initiatives reducing equipment and technology costs

- Standardised regulatory frameworks facilitating cross-border investment

Processing facility development could benefit from regional hub approaches that serve multiple countries whilst achieving economies of scale necessary for cost-competitive operations. Such coordination requires diplomatic cooperation alongside commercial collaboration among governments and private sector entities.

Frequently Asked Questions About Botswana's Rare Earth Discovery

When Will Commercial Production Begin?

Typical development timelines for rare earth projects span 5-7 years from initial discovery to commercial production, though this timeframe can vary significantly based on geological complexity, regulatory requirements, and financing availability. Botswana's current exploration phase indicates that commercial production would not begin before 2031 under optimistic scenarios.

Regulatory approval processes involve environmental impact assessments, community consultation procedures, and mining permit applications that typically require 24-36 months to complete. Botswana's established regulatory frameworks may accelerate these processes compared to jurisdictions with less developed mining governance systems.

Financing and partnership development phases often extend beyond technical studies, as rare earth projects require specialised processing expertise and substantial capital commitments. Successful projects typically secure both development funding and long-term supply agreements before beginning construction phases.

How Will This Affect Global Rare Earth Prices?

Market share implications depend heavily on production scale and timing relative to demand growth projections. If Botswana's production reaches significant scale by the mid-2030s, it could contribute to price stabilisation through supply diversification, though individual element prices will vary.

Price stabilisation effects typically emerge gradually as new supply sources achieve consistent production levels and develop established customer relationships. Historical analysis suggests that meaningful price impacts require new suppliers to capture at least 10-15% market share in specific rare earth elements.

Investment implications for rare earth-dependent industries include reduced supply security risks and potentially more stable long-term pricing, though transition periods may involve continued volatility as markets adjust to changing supply patterns.

What Role Will International Partners Play?

Western government development finance opportunities include institutions such as the U.S. Development Finance Corporation and European development banks that prioritise critical mineral projects supporting supply chain diversification objectives. These financing sources can provide both capital and political risk mitigation.

Technology transfer and processing expertise requirements suggest that partnerships with established mining companies will be essential for successful project development. Companies with rare earth processing experience possess specialised knowledge that is difficult to develop independently within short timeframes.

Strategic partnership models may involve joint venture structures, long-term supply agreements, or technical service arrangements that balance risk sharing with returns distribution among multiple stakeholders.

Investment and Strategic Implications for Stakeholders

Opportunities for Mining Sector Investors

Investment opportunity analysis reveals multiple entry points for different investor types, ranging from early-stage exploration funding to infrastructure development and processing facility construction. Each opportunity category presents distinct risk-return profiles suitable for different investment strategies.

| Investment Category | Capital Requirements | Risk Level | Return Timeline | Key Success Factors |

|---|---|---|---|---|

| Direct Equity Participation | $50M-200M | High | 7-12 years | Geological success, permits |

| Infrastructure Development | $200M-500M | Medium | 5-8 years | Government support, demand |

| Processing Facilities | $300M-800M | Medium-High | 6-10 years | Technology access, markets |

| Strategic Offtake Agreements | Variable | Low-Medium | 3-5 years | Production certainty, pricing |

Comparison with other African critical mineral investments suggests that Botswana offers superior regulatory stability and infrastructure foundations, though geological uncertainty remains until extensive drilling programmes confirm resource scale and quality parameters.

Early-stage investment opportunities may provide exposure to resource upside potential, whilst later-stage infrastructure and processing investments offer more predictable returns with lower geological risks but higher capital requirements.

Strategic Planning for Rare Earth-Dependent Industries

Supply chain risk mitigation strategies should incorporate potential Botswana production into long-term sourcing plans whilst maintaining realistic timelines for commercial availability. Companies heavily dependent on rare earth inputs may benefit from early engagement with project developers to secure future supply access.

Long-term offtake agreement considerations include pricing mechanisms, volume commitments, quality specifications, and delivery logistics that balance supply security with commercial flexibility. These agreements often require 3-5 year negotiation and development periods before production begins.

Hypothetical Integrated Supply Chain Development Model:

- Mining operations in Botswana producing rare earth concentrates

- Regional processing facilities creating separated rare earth elements

- Manufacturing partnerships developing finished components

- End-user integration supporting electric vehicle and renewable energy sectors

- Recycling infrastructure capturing value from end-of-life products

Regional hub development potential extends beyond individual projects to encompass broader industrial development that could transform southern Africa into a significant participant in global technology supply chains. This vision requires coordinated investment across multiple sectors and sustained political commitment to industrial development objectives.

The rare earth discovery in Botswana represents more than a geological find; it embodies the intersection of natural resource endowment, technological demand, and geopolitical strategy that will shape global economic relationships throughout the energy transition era. Success in developing this resource will require coordination among geological science, financial engineering, diplomatic relationships, and industrial development that reflects the complexity of modern mineral supply chains.

Disclaimer: This analysis contains forward-looking statements and projections based on current information and assumptions. Actual outcomes may vary significantly due to geological, technical, regulatory, market, and geopolitical factors beyond current knowledge. Readers should conduct independent due diligence and consult qualified professionals before making investment or strategic decisions based on this information.

Ready to Capitalise on the Next Major Critical Minerals Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Explore Discovery Alert's dedicated discoveries page to understand why major mineral discoveries can lead to substantial market returns, then begin your 14-day free trial today to position yourself ahead of the market.