July 17, 2026

The Geopolitics of Diamonds: Why Africa's Producer Nations Are Reclaiming the Crown

For most of the twentieth century, the global diamond industry operated on a simple principle: a small number of Western-listed mining corporations controlled extraction, marketing, and pricing, while the nations sitting atop the world's richest diamond deposits collected royalties and minority dividends. That model is now fracturing in real time, and the Botswana De Beers stake sale is the clearest expression of how profoundly the rules of resource ownership are being rewritten.

This is not simply a corporate transaction. It is a test of whether African producer nations can convert geological endowment into genuine strategic control, and whether the financing architecture exists to support that ambition at scale.

When big ASX news breaks, our subscribers know first

Why Anglo American Is Exiting One of Mining's Most Iconic Brands

Anglo American's decision to put De Beers up for sale in May 2024 reflected a calculated reallocation of capital rather than any sudden loss of confidence. The company had identified copper and iron ore as its priority commodities heading into a decade shaped by electrification and infrastructure investment, and De Beers represented a concentration of risk in an asset class facing structural headwinds from two directions simultaneously.

The first pressure was cyclical but severe: natural diamond prices fell sharply in the period leading up to the divestiture announcement, driven by post-pandemic demand normalisation and inventory overhang in the midstream cutting and polishing sector. The second pressure was more fundamental. Lab-grown diamonds, manufactured through chemical vapour deposition or high-pressure high-temperature processes, had achieved price points low enough to compete directly with natural stones in the jewellery market, particularly among younger consumers less attached to the scarcity narrative that had underpinned De Beers' marketing for decades.

De Beers itself acknowledged the synthetic threat by launching its own lab-grown brand, Lightbox, at deliberately low retail price points. The strategic intent was to commoditise the synthetic segment and protect the premium positioning of natural diamonds. Whether that strategy has succeeded remains genuinely contested among industry analysts, and the ambiguity itself partly explains the valuation gap between what Anglo American believes the business is worth and what the market is willing to pay.

The Valuation Disconnect and What Does It Signal?

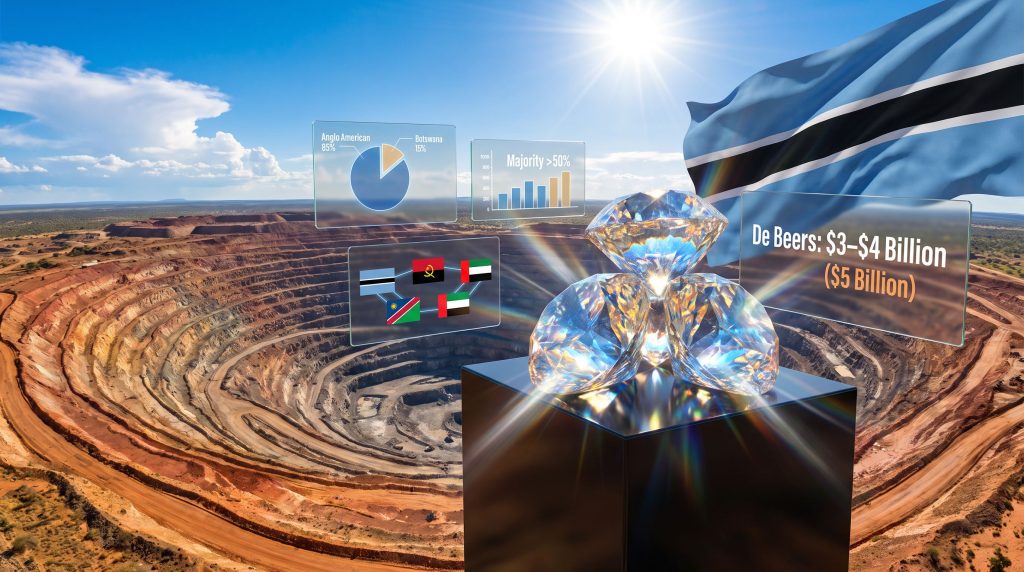

Anglo American's internal valuation of De Beers sits at approximately $5 billion, while independent analyst estimates cluster in the $3 to $4 billion range, implying a discount of between 20% and 40% to the seller's expectations.

| Valuation Perspective | Estimated Range |

|---|---|

| Anglo American (seller estimate) | ~$5 billion |

| Independent analyst consensus | $3 to $4 billion |

| Implied discount to seller's ask | 20 to 40% |

That gap reflects more than routine negotiating positions. It encodes deep uncertainty about the long-term trajectory of natural diamond demand, the geopolitical risk premium attached to multi-jurisdictional African operations, and the difficulty of applying standard discounted cash flow models to a business whose core pricing assumptions are in structural flux. For any prospective buyer, the valuation question is inseparable from a thesis about whether natural diamonds can sustain their premium over synthetics through branding and provenance marketing alone.

The Global Diamond Consortium: Who Is Behind Anglo's Preferred Bidder?

The sale process began with six bidding parties in 2025 before narrowing to two shortlisted consortia. Anglo American subsequently identified the Global Diamond Consortium as its preferred buyer, a selection that Botswana's Minister for State President, Defence and Security, Moeti Mohwasa, confirmed publicly before any formal announcement from Anglo American itself. That sequencing is telling: it demonstrates how deeply embedded Botswana's government is in the deal's political and commercial architecture.

Reported participants in the consortium include former De Beers chief executive Gareth Penny, who now chairs asset manager Ninety One, a Qatari sovereign investment fund, and Israeli businessman Nir Livnat. The consortium's proposal notably incorporates Angola and Namibia as structural partners rather than passive investors, a design choice with significant strategic logic. This reflects broader mining consolidation trends emerging across the sector, where multi-party ownership structures are increasingly replacing single-operator models.

Why Does the Consortium's Architecture Matter Beyond the Purchase Price?

Including diamond-producing sovereign governments within the ownership structure addresses one of the most persistent operational risks in African mining: political friction between foreign-controlled mining companies and the host nations that own the underlying resources. When Angola and Namibia hold equity rather than simply collecting royalties and taxes, their incentive structure shifts from adversarial to aligned.

Gareth Penny's involvement carries its own signal value. His tenure as De Beers chief executive gave him direct experience managing the Botswana government relationship, navigating the Diamond Trading Company's sightholder system, and operating through commodity downturns. For a business requiring a credible turnaround thesis, the presence of an experienced sector operator is not cosmetic: it is central to the investment case.

Botswana's Pre-Emptive Rights: Three Paths to a Different Future

At the legal heart of this transaction sits Botswana's pre-emptive rights mechanism. These contractual entitlements allow an existing minority shareholder to match or acquire a stake being sold to a third party before that sale is finalised. Botswana currently holds a 15% equity stake in De Beers, and its pre-emptive rights apply to Anglo American's 85% stake now being divested.

The government has three structurally distinct options available to it:

- Exercise rights independently, acquiring the stake without partnering with the preferred bidder, maximising sovereign control but requiring full financing capacity from Botswana alone.

- Co-invest alongside the Global Diamond Consortium, partnering with Anglo's chosen buyer to share the financial burden while securing a larger equity position than the current 15%.

- Align with a separately chosen third party, such as a Gulf sovereign wealth fund, to back a Botswana-led acquisition outside the consortium framework.

Botswana's stated ambition is to secure a majority or controlling stake above 50%, which would fundamentally transform its role from passive minority investor to active strategic owner with direct influence over De Beers' diamond pricing benchmarks, sightholder allocation decisions, and long-term marketing strategy.

Current and Targeted Ownership Structure

| Stakeholder | Current Stake | Target Position |

|---|---|---|

| Anglo American | 85% | Exiting via sale |

| Botswana Government | 15% | Majority or controlling (above 50%) |

| Angola (interest expressed) | 0% | Potentially 20 to 30% |

| Namibia (interest expressed) | 0% | To be determined |

Owning a controlling interest in De Beers would give Botswana something royalties and taxes cannot: decision-making authority over the DTC sightholder system, which determines which rough diamond traders gain access to De Beers' production at contracted prices. That system is a gatekeeper to the global rough diamond trade, and whoever controls it shapes the economics of the entire downstream pipeline from cutting centres in Antwerp, Mumbai, and Surat through to retail jewellery markets worldwide. As the global diamond producers landscape continues to evolve, such control carries profound strategic implications.

Gulf Capital as the Financing Mechanism: UAE and Oman Enter the Equation

Botswana's government under President Duma Boko has engaged the United Arab Emirates and an Omani sovereign wealth fund as potential financing partners to support its majority stake ambition. This is a strategically coherent choice for several reasons that go beyond the availability of capital.

Gulf sovereign wealth funds are structurally suited to long-duration, resource-backed asset acquisitions. Their investment horizons extend across decades rather than quarterly earnings cycles, their capital bases are insulated from the short-term redemption pressures facing institutional fund managers, and their commodity investment experience, built through generations of hydrocarbon asset management, translates meaningfully to hard-asset diamond ownership.

Comparing Botswana's Financing Pathways

| Financing Pathway | Strategic Upside | Key Risk |

|---|---|---|

| UAE sovereign partnership | Large capital base, long investment horizon | Potential governance dilution |

| Omani sovereign wealth fund | Established resource investment track record | Smaller balance sheet than Abu Dhabi peers |

| Angola and Namibia co-investment | Regional alignment, shared producer interests | Coordination complexity |

| Botswana standalone acquisition | Maximum sovereign control | Fiscal strain on government balance sheet |

Furthermore, there is a geopolitical dimension. By engaging Gulf capital rather than Western financial institutions or Chinese state investment vehicles, Botswana is seeking partners with fewer policy conditionality requirements while simultaneously diversifying its international financial relationships. That positioning reflects a broader pattern visible across African mining finance, where nations explore non-traditional capital partnerships as an alternative to arrangements that historically came with governance or policy prescriptions attached.

Angola's Strategic Calculus and the Prospect of a Pan-African Diamond Bloc

Angola's interest in acquiring a meaningful stake in De Beers, with reported targets in the 20 to 30% range, is driven by more than financial return. Angola operates significant diamond production through assets including the Catoca mine in Lunda Sul province, one of the world's largest kimberlite diamond mines by output volume. Gaining equity in De Beers would give Angola access to the marketing, branding, and distribution infrastructure that currently sits entirely outside its control.

The distinction between a strategic shaping stake and a purely financial investment is critical here. A financial investor in De Beers would be satisfied with dividend income and capital appreciation. Angola's interest, however, is in using its ownership position to integrate De Beers' market access mechanisms with its own production pipeline, potentially routing Angolan rough diamonds through De Beers' sightholder system to achieve better price realisation than it currently obtains through independent channels.

Analytical scenario: If Botswana secures a controlling stake while Angola holds approximately 25% and Namibia joins as a third producer-nation partner, the result would be an unprecedented Southern African diamond consortium controlling the world's most recognised diamond brand. The governance implications for global rough diamond supply management would be profound, representing a structural shift in who sets the terms of the diamond trade rather than simply who participates in it.

The OPEC analogy is instructive but imperfect. Producer-nation coordination in oil has demonstrated both the power and the fragility of multi-sovereign commercial alliances. Divergent national fiscal positions, competing political cycles, and the absence of a unified regulatory framework across Botswana, Angola, and Namibia all represent genuine friction points. Consequently, the directional logic of producer-nation coordination in diamonds is compelling precisely because De Beers' historical marketing architecture was built on managed supply, and that mechanism would be far more credible in the hands of the nations producing the diamonds than in the hands of a publicly listed mining major answerable to quarterly earnings pressure.

The next major ASX story will hit our subscribers first

The Structural Challenges That Persist Regardless of Ownership

Lab-Grown Diamonds: Disruption That Compounds Value Uncertainty

The synthetic diamond segment is not a temporary aberration. Chemical vapour deposition technology has reduced the cost of producing gem-quality lab-grown diamonds dramatically over the past decade, and production scale continues to expand, particularly in China and India. The price differential between natural and lab-grown diamonds has narrowed to the point where the premium for natural stones must be sustained entirely through differentiated branding and provenance storytelling rather than objective quality metrics: a well-cut lab-grown diamond is, by all gemological measures, identical to its natural equivalent.

This creates an unusual strategic challenge for any new De Beers owner. The business model depends on sustaining consumer belief in a value hierarchy that science does not support, which means the marketing infrastructure is not a complement to the operational assets but rather the primary source of value. Any governance transition that undermines the coherence or credibility of De Beers' brand communication could accelerate natural diamond price erosion in ways that would be difficult to reverse.

Operational Complexity Across Five Jurisdictions

| Operating Country | Nature of Operations |

|---|---|

| Botswana | Primary production hub, including Jwaneng and Orapa mines |

| Namibia | Marine and alluvial diamond recovery operations |

| Angola | Exploration and emerging production assets |

| South Africa | Historical production base |

| Canada | Northern operations |

Each jurisdiction carries its own regulatory approval requirements, and any ownership change of the scale contemplated here will require clearance from multiple sovereign governments simultaneously. The shifting mining geopolitics of resource-rich nations further complicate this picture. Canada's diamond sector has also experienced its own turbulence, with the Ekati mine in the Northwest Territories entering receivership following a Supreme Court of British Columbia ruling in July 2026, adding further complexity to the Canadian operational picture.

The Roadmap to Completion: Q4 2026 and the Conditions That Must Be Met

Botswana's government has indicated the transaction is expected to close by the fourth quarter of 2026, a timeline that is ambitious given the multi-party complexity of the deal. The critical path to completion involves sequential decisions that each carry their own uncertainty:

- Botswana finalises its pre-emptive rights decision, determining whether to partner, proceed alone, or bring in a Gulf sovereign co-investor.

- Financing structure is confirmed and capital commitments are locked in with UAE or Omani partners.

- Anglo American and the consortium execute a binding sale agreement.

- Multi-jurisdictional regulatory approvals are obtained across Botswana, Namibia, Angola, South Africa, and Canada.

- Botswana government cabinet or parliamentary approval is secured.

- Transaction closes and ownership transfers to the new consortium structure.

Any single step in this sequence carries the potential for delay, and the interdependencies between them mean that slippage in one area can cascade across the entire timeline.

Resource Sovereignty as a New Strategic Framework

The Botswana De Beers stake sale is best understood not as a single corporate transaction but as a live experiment in what resource sovereignty can look like when it moves beyond rhetoric into structured commercial execution. Botswana is not nationalising an asset or imposing punitive terms on a foreign operator. It is using contractual pre-emptive rights, engaging sophisticated financial advisors, and assembling Gulf sovereign capital partnerships to pursue a majority stake on commercial terms.

That distinction between resource nationalism and resource sovereignty matters enormously for how the investment community should interpret events. Nationalisation destroys value through uncertainty and deterrence. Commercially structured sovereign acquisition, if executed competently, can preserve operational continuity, institutional knowledge, and brand equity while redistributing the long-term value capture toward the nations whose geological endowments make the business possible in the first place.

In addition, the role of mining private equity in structuring such deals is becoming increasingly relevant as sovereign buyers seek experienced capital partners who understand both the operational and financial dimensions of large-scale resource asset transitions.

Whether Botswana can execute this ambition within the constraints of its government balance sheet, its Q4 2026 timeline, and the competing interests of Angola, Namibia, and Gulf sovereign partners remains genuinely uncertain. But the sophistication of the approach being taken signals that the era of passive mineral royalties as the ceiling of African producer-nation ambition is drawing to a close.

Readers seeking further context on De Beers' operational history, the evolving global diamond market, and Anglo American's broader corporate restructuring can find ongoing coverage at Mining.com, which tracks major mining sector transactions and commodity market developments across all major producing regions. For additional analysis on diamond market valuations and consumer trends, Rapaport provides specialist industry reporting on rough and polished diamond pricing.

Disclaimer: This article contains forward-looking analysis, scenario projections, and commentary on valuation ranges derived from publicly reported sources. Nothing in this article constitutes financial or investment advice. Readers should conduct their own due diligence before making any investment decisions related to companies or assets discussed herein. Valuations, timelines, and ownership outcomes described are subject to significant uncertainty and may differ materially from those ultimately achieved.

Want to Stay Ahead of the Next Major Resource Sovereignty Play?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries and turning complex data into actionable investment insights — so subscribers are positioned ahead of the broader market before price-moving news becomes common knowledge. Explore how major discoveries have historically delivered extraordinary returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to secure your market-leading edge.