July 18, 2026

The Century-Long Grip on African Diamonds Is Finally Loosening

For more than a hundred years, the global diamond trade operated through a system of centralised control that kept pricing power, marketing authority, and value capture firmly in the hands of multinational corporations headquartered far from the mines themselves. Africa supplied the stones. Others captured the margins. That model is now facing its most serious challenge yet, and the Botswana De Beers takeover debate sits at the very centre of it.

The question now confronting Botswana is deceptively simple on the surface: how much of De Beers should it own? Beneath that question, however, lies a far more complex calculation involving fiscal exposure, sovereign ambition, structural industry decline, and the long-term future of African resource ownership.

When big ASX news breaks, our subscribers know first

What the Numbers Reveal About Botswana's Diamond Dependency

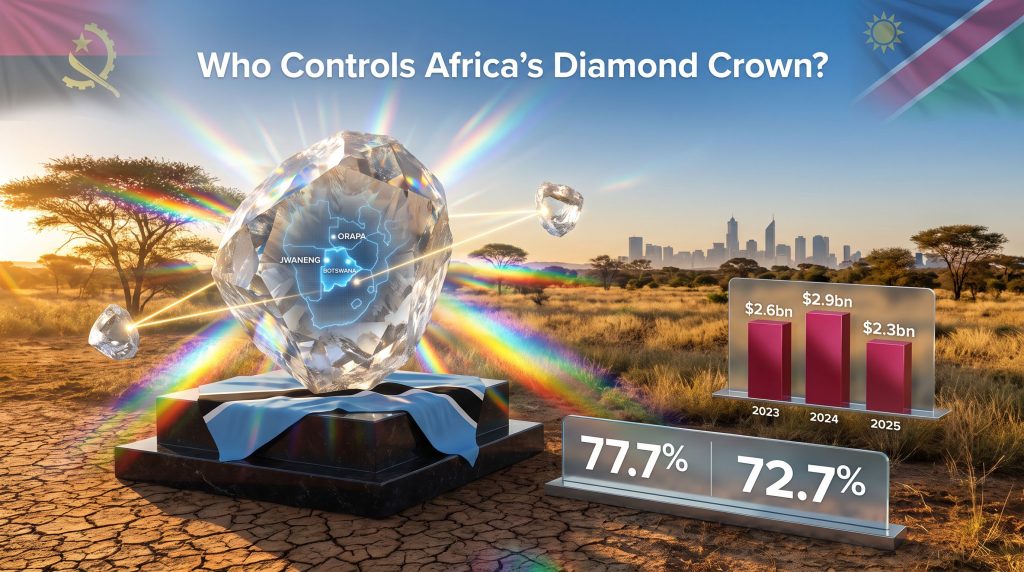

Before analysing the strategic options available to Gaborone, it is worth understanding precisely how exposed Botswana is to the diamond trade. According to the Bank of Botswana, diamonds represented 77.7% of the country's goods exports in Q2 2025, declining marginally to 72.7% in Q3 2025. The sector consistently delivers approximately three-quarters of Botswana's foreign-exchange earnings and funds roughly one-third of government revenue.

This dependency is the central paradox of the Botswana De Beers takeover debate. On one hand, Botswana's economic survival is intertwined with the diamond industry, making strategic influence over De Beers a matter of national interest. Furthermore, commodity price pressures have added another layer of urgency to getting the ownership structure right.

On the other hand, acquiring a larger stake in a business whose valuation has been decimated by structural headwinds would concentrate fiscal risk in precisely the asset Botswana can least afford to mismanage.

The deeper the diamond dependency, the higher the stakes of getting this ownership decision wrong. For Botswana, this is not a portfolio investment. It is an existential economic question.

Anglo American has recorded impairment charges against De Beers across three consecutive reporting periods, totalling more than $7.8 billion in combined writedowns:

| Year | Impairment Recorded | Carrying Value Impact |

|---|---|---|

| 2023 | $2.6 billion writedown | Significant initial erosion |

| 2024 | $2.9 billion writedown | Accelerating decline |

| 2025 | $2.3 billion writedown | Carrying value halved to ~$2.3 billion |

An independent valuation conducted in February 2025 placed De Beers at approximately $4.9 billion, a figure that already reflected the severity of the rough-diamond price collapse. Total De Beers revenue reached $3.5 billion in 2025, rising from $3.3 billion the previous year, with rough-diamond revenue climbing to $3.0 billion. Yet average realised prices continued to fall, underscoring the disconnect between volume and pricing power.

Who Is the Global Diamond Consortium and Why Does It Matter?

Anglo American selected the Global Diamond Consortium as its preferred acquirer for its 85% stake in De Beers following a competitive process that reportedly began with six participating groups before narrowing progressively. The consortium is reported to be led by Gareth Penny, who served as De Beers' chief executive from 2006 to 2010 and currently chairs South African asset manager Ninety One.

The significance of Penny's leadership extends beyond industry familiarity. His tenure at De Beers coincided with a period of significant operational transformation, including efforts to modernise the Sightholder system, the mechanism through which De Beers distributes rough diamonds to approved buyers. That institutional knowledge could prove valuable when navigating the turnaround challenge that any new ownership structure will inherit.

The field of competing bidders that was eventually narrowed included:

| Bidder / Group | Background | Outcome |

|---|---|---|

| Global Diamond Consortium (Gareth Penny) | Former De Beers CEO; Ninety One chairman | Preferred bidder |

| Nir Livnat Group | Israeli diamond industry businessman | Not selected |

| Qatari Investment Fund | Gulf sovereign capital | Not selected |

| Michael O'Keeffe Group | Former CEO, Burgundy Diamond Mines | Not selected |

| Anil Agarwal-linked Group | Indian mining magnate | Eliminated in earlier rounds |

Notably, the consortium's proposed structure includes potential participation by Angola and Namibia, both active diamond-producing nations that had previously declared independent interest in acquiring a controlling De Beers stake. Angola's initial competing bid prompted high-level diplomatic engagement with Botswana aimed at reducing inter-African rivalry. The consortium framework could consequently convert that rivalry into collaboration.

Botswana's Three Strategic Paths and the Risk Profile of Each

Botswana's Minister for State President, Defence and Security, Moeti Mohwasa, confirmed to lawmakers that the government retains full discretion to pursue any of three distinct ownership paths. A final decision is expected before the Q4 2026 transaction deadline, subject to government approval. In the context of the broader global mining landscape, this decision carries significant weight beyond Botswana's borders.

Path One: Exercise Pre-Emptive Rights Independently

Botswana holds a legal right of first refusal over Anglo American's 85% stake. This mechanism grants Gaborone the authority to match or restructure the proposed transaction without needing to compete against external bidders. President Duma Boko has publicly stated his administration's ambition to secure full sovereign control over De Beers.

Advantages: Maximum operational and strategic influence over mining, marketing, pricing, and global brand positioning. Full alignment between national economic interests and corporate direction.

Risks: Requires substantial sovereign capital or external financing. Full exposure to a business navigating one of the most structurally challenging environments in the modern diamond industry's history.

Path Two: Co-Invest Alongside the Global Diamond Consortium

Rather than exercising its rights alone, Botswana could join the consortium as a co-investor, increasing its ownership stake without absorbing the full financial burden of sole acquisition.

Advantages: Distributes financial risk across multiple partners. Combines sovereign strategic interest with private-sector operational expertise. A pan-African ownership model involving Botswana, Angola, and Namibia could meaningfully reframe De Beers as a producer-nation-led enterprise for the first time in its history.

Risks: Diluted decision-making authority. Potential misalignment between Botswana's long-term strategic priorities and the return-driven objectives of private capital partners.

Path Three: Retain the Existing 15% Stake

If Botswana declines to exercise its pre-emptive rights, the Global Diamond Consortium would proceed as the controlling owner, with Botswana retaining its minority position.

Advantages: Lowest immediate financial risk. Operational leverage is preserved through existing structures.

Risks: Reduced influence over De Beers' global strategic direction. Future ownership decisions made without Botswana in a controlling position.

The Debswana Advantage: Understanding Botswana's Hidden Leverage

A critical and often underappreciated dimension of the Botswana De Beers takeover calculation is that Botswana's power over De Beers extends far beyond its 15% equity position. The Debswana joint venture, a 50-50 partnership between the Botswana government and De Beers, operates the Jwaneng and Orapa mines, two of the highest-value diamond operations anywhere in the world.

These mines collectively supply approximately 70% of De Beers' annual rough diamond output. That figure is not merely impressive; it is structurally decisive. No prospective buyer of De Beers can operate the business viably without Botswana's active cooperation. This asymmetry gives Gaborone negotiating leverage that no equity percentage alone could replicate. Indeed, questions of resource sovereignty are increasingly central to how governments worldwide assess strategic asset ownership.

The Jwaneng and Orapa Mines: Why They Are Irreplaceable

The Jwaneng mine, situated in southern Botswana, is widely regarded as the world's richest diamond mine by value. Its ore grades, measured in carats per hundred tonnes, consistently rank among the highest of any producing operation globally. Orapa, one of the largest diamond mines by surface area, complements Jwaneng through volume output and long-established processing infrastructure.

Together, these assets are not easily replicated or substituted. Diamond mining is intensely location-specific; kimberlite pipes, the geological formations from which gem-quality diamonds are extracted, are finite in number and vary enormously in grade and value. Botswana's kimberlites sit at the premium end of that spectrum.

What the 2025 Sales Agreement Changed

In February 2025, Botswana and De Beers executed a new 10-year sales agreement (extendable by five years) and renewed Debswana's mining licences through 2054. The agreement progressively transfers a larger share of Debswana's production to the Okavango Diamond Company, the government-owned marketing entity.

This arrangement already represents a meaningful transfer of revenue and marketing control toward Botswana. A larger equity stake in De Beers itself would deepen that trajectory, adding brand authority and global distribution influence to an operational advantage Botswana already possesses.

The Structural Headwinds Facing Natural Diamonds

Any analysis of the Botswana De Beers takeover must grapple honestly with the industry forces reshaping natural diamond demand. The challenges are not cyclical fluctuations; they reflect durable shifts in consumer behaviour, technology, and global spending patterns.

- Price collapse: Natural rough-diamond prices have fallen by approximately 50% since 2022, compressing margins across the entire supply chain from mine to retailer.

- Lab-grown diamond competition: Laboratory-grown diamonds, produced through High Pressure High Temperature (HPHT) and Chemical Vapour Deposition (CVD) processes, now offer gem-quality stones at a fraction of the cost of mined equivalents. Consumer acceptance, particularly among younger demographics, has accelerated faster than most industry forecasters anticipated.

- China demand weakness: Slower luxury consumption in China, historically a critical growth engine for rough-diamond absorption, has removed a key demand pillar that supported pricing through the previous decade.

- Inventory overhang: Excess pipeline inventory accumulated across the midstream, particularly among Indian cutting and polishing centres in Surat, has suppressed price recovery even as production has been curtailed.

- Operational restructuring: De Beers has implemented more than $100 million in annual cost reductions since 2024. The recently announced two-year production suspension at Venetia mine in South Africa, which accounts for approximately 10% of De Beers' total output and 40% of South Africa's diamond production, reflects the severity of the adjustment being undertaken.

Lab-grown diamonds are not simply a cheaper alternative product. They represent a fundamental technological disruption to the scarcity proposition that has underpinned natural diamond pricing and desirability for over a century.

The next major ASX story will hit our subscribers first

Financing the Ambition: Where Botswana Is Looking for Capital

The scale of capital required for a meaningful De Beers acquisition exceeds what Botswana's sovereign balance sheet can comfortably absorb independently, particularly given the S&P credit rating pressures the country has faced in recent periods. To address this, Botswana has entered financing discussions with:

- Oman's sovereign wealth fund

- The United Arab Emirates

These conversations reflect both the magnitude of the acquisition cost and the growing appetite among Gulf sovereign capital pools for exposure to African resource assets. For Botswana, securing external co-financing would allow it to pursue a larger ownership stake without overextending its fiscal position. For Gulf partners, access to one of the world's most iconic mining brands offers long-term asset diversification. Trends in African mining finance suggest this kind of cross-regional capital partnership is becoming increasingly common across the continent.

Anglo American's Strategic Retreat and What It Signals

Anglo American announced its intention to divest De Beers in May 2024, framing the decision as part of a comprehensive portfolio restructuring undertaken in response to its rejection of a takeover approach from BHP. The strategic logic centres on concentrating capital and management focus on copper, premium iron ore, and crop nutrients, commodities Anglo views as structurally aligned with long-term demand growth.

The assets being shed, including diamonds, platinum group metals, nickel, and steelmaking coal, reflect a deliberate move away from commodity diversification toward concentrated sector leadership. This pattern is not unique to Anglo. Mining industry consolidation has created structural windows for African sovereign entities and regional capital to step into ownership positions historically dominated by multinational corporations.

Frequently Asked Questions: Botswana De Beers Takeover

What is Botswana's current ownership stake in De Beers?

Botswana holds a 15% equity stake in De Beers, with Anglo American controlling the remaining 85%. Botswana also holds substantial operational leverage through the Debswana joint venture and the Okavango Diamond Company.

Who is the preferred buyer for Anglo American's De Beers stake?

Anglo American has selected the Global Diamond Consortium as its preferred acquirer. The consortium is reported to be led by former De Beers CEO Gareth Penny and proposes including Angola and Namibia as participant nations. Reports indicate that Angola's early competing interest significantly shaped the contours of the final consortium structure.

What is De Beers currently valued at?

De Beers was independently assessed at approximately $4.9 billion in February 2025. Anglo American's carrying value has been reduced to approximately $2.3 billion following three consecutive years of impairments exceeding $7.8 billion in total.

When is the transaction expected to be finalised?

The sale is targeted for completion in the fourth quarter of 2026, subject to Botswana's government approval and resolution of its pre-emptive rights decision.

Why have natural diamond prices fallen so sharply?

Natural rough-diamond prices have declined by approximately 50% since 2022, driven by reduced luxury spending in China, excess inventory across the supply chain, and rapidly accelerating consumer adoption of laboratory-grown diamonds, which are produced through HPHT and CVD technologies and offer visually comparable quality at significantly lower price points.

The Precedent That Extends Well Beyond Diamonds

The Botswana De Beers takeover decision will not be judged solely on its financial merits. Its outcome will function as a reference point for how African producer nations engage with future divestiture processes across the continent's resource sector. A successful transition to majority African ownership, whether through Botswana acting alone, in partnership with Gulf sovereign capital, or through a pan-African consortium, would demonstrate that geological endowment can be converted into durable economic sovereignty.

Conversely, an acquisition that stretches Botswana's balance sheet into a structurally declining asset, without a credible operational and market recovery strategy, would reinforce caution among African governments considering similar resource nationalisation moves elsewhere.

Botswana's government has confirmed it is working with financial advisers to determine the optimal transaction structure. Minister Mohwasa has made clear that any successful buyer, regardless of structure, must demonstrate genuine operational expertise, long-term ownership stability, and a credible, well-capitalised plan to navigate the recovery of a business facing the most sustained demand contraction in its modern history.

The Q4 2026 deadline is approaching. The decision Botswana makes will shape not only who controls one of the world's most recognisable mining brands, but also how much of the value generated by African diamonds ultimately stays on African soil.

This article is intended for informational purposes only and does not constitute financial or investment advice. All valuations, forecasts, and transaction timelines referenced are based on publicly available information and are subject to change. Readers should conduct independent due diligence before making any investment decisions related to entities or sectors discussed.

Want to Track the Next Major Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time ASX alerts the moment significant mineral discoveries are announced, translating complex geological and commodity data into clear, actionable insights for investors at every level — explore historic discovery returns to understand the scale of opportunity, then begin your 14-day free trial to position yourself ahead of the broader market.