July 18, 2026

When Geopolitics Meets Distressed Debt: Understanding the Sherritt Crisis

Most mining company failures follow a familiar script: commodity prices collapse, margins compress, and debt becomes unserviceable. The crisis unfolding at Sherritt International Corp. follows an entirely different trajectory. Here, the underlying mineral assets retain genuine strategic value, operations were viable until external forces intervened, and the financial emergency is not the product of poor capital allocation but of geopolitical shock. Understanding that distinction is not merely academic. It fundamentally changes how creditors, investors, and potential acquirers should evaluate the competing rescue frameworks now being placed before the company's board.

The Sherritt rival rescue plan debate is, at its core, a contest over who controls the recovery of a distressed but strategically relevant mining operation at a time when nickel and cobalt have become central to battery supply chain security. The stakes extend well beyond one company's balance sheet.

When big ASX news breaks, our subscribers know first

The Moa Joint Venture: Asset Quality Beneath the Financial Noise

Before dissecting the competing recapitalisation proposals, it is worth establishing precisely what is being fought over. The Moa nickel-cobalt joint venture, situated in the Holguín province of eastern Cuba, is not a marginal or depleted asset. It is one of the world's laterite nickel operations with a multi-decade production history, producing both nickel and cobalt through a hydrometallurgical refining process that includes a finishing facility in Fort Saskatchewan, Alberta.

Laterite nickel deposits, unlike sulphide deposits, sit closer to the earth's surface and are mined through open-pit methods. The Moa deposit is a limonite-saprolite type laterite, which is processed using high-pressure acid leaching (HPAL) technology to extract nickel and cobalt in a mixed sulphide intermediate form. This processing pathway is technically demanding and capital-intensive, which is precisely why Moa's existing infrastructure represents a significant barrier to replication.

Cobalt recovered from Moa carries particular relevance in the current market environment. Cobalt is a critical input in lithium-ion battery cathode chemistries, particularly NMC (nickel-manganese-cobalt) formulations used widely in electric vehicles. Furthermore, while cobalt-free battery chemistries are advancing, NMC variants continue to dominate in high-energy-density applications. The Moa joint venture thus sits at the intersection of legacy mining infrastructure and forward-looking cobalt supply chain demand.

What Makes Moa Geologically Distinctive

Laterite deposits in Cuba, including Moa, are notable for their relatively high cobalt content compared to many other global laterite operations. Cuban laterites formed through prolonged tropical weathering of ultramafic rocks, concentrating nickel and cobalt in the upper limonite horizon. This geological origin means the ore is amenable to the acid-leach processing pathway that Sherritt has operated for decades.

The key takeaway for investors evaluating the rescue scenarios: the underlying resource is not in question. What is being negotiated is the financial and corporate structure that will determine who benefits from restarting production. Consequently, the nickel market importance of assets like Moa cannot be overstated in the current energy transition environment.

How Sanctions Cascaded Into a Going Concern Warning

Cuba's energy crisis, the proximate cause of Moa's production suspension in February 2026, did not arise in isolation. The tightening of U.S. sanctions under the Trump mining policy environment restricted the island's ability to import sufficient oil to meet industrial and civilian power needs. The resulting electricity shortfalls made sustained mining and processing operations at Moa economically and practically unviable.

This sequence matters for risk assessment. Sherritt's operational challenges stem from an external policy decision, not from reserve depletion, cost blowouts, or technical failures at the asset level. When sanctions change, or when Cuba finds alternative energy supply pathways, the Moa operation could potentially resume relatively quickly compared to a mine that has suffered physical damage or exhausted its ore body.

The going concern warning Sherritt issued in June 2026 reflects the financial consequences of suspended production, not a permanent impairment of the underlying asset. The company publicly acknowledged it would lack sufficient cash to repay debt obligations if lenders declared a default and demanded early repayment. That acceleration risk mechanism is the single most urgent variable in the recapitalisation timeline.

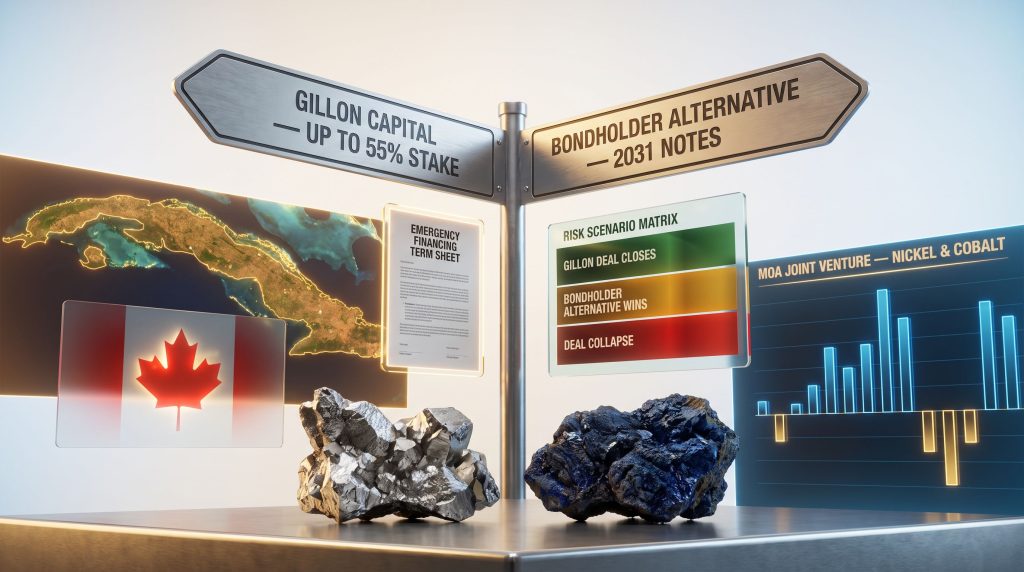

Two Rescue Paths, One Distressed Company

The Sherritt rival rescue plan debate crystallises around two structurally distinct proposals. Each carries a different risk profile, regulatory exposure, and implied ownership outcome.

The Gillon Capital Proposal in Detail

Gillon Capital LLC is a Texas-based family office associated with Ray Washburne, a businessman who served as a senior adviser in the first Trump administration. The firm entered exclusive preliminary negotiations with Sherritt to acquire warrants exercisable for up to 55% of the company's equity, priced at a discount to Sherritt's May 15, 2026 share price. The warrant exercise window extends over a nine-month period following deal closing.

Several structural features of this arrangement deserve scrutiny:

- The non-binding nature of the current agreement means Sherritt has explicitly stated there is no assurance the transaction will complete on any specific timeline.

- Warrant-based structures defer actual capital inflow until exercise, meaning the company does not immediately receive the full equity injection.

- The nine-month exercise window creates an extended period of ownership uncertainty.

- The proposer's political connections raise the question of whether regulatory navigation is an explicit or implicit part of the value proposition.

On the regulatory dimension, any transaction touching Sherritt's Cuban assets must navigate the U.S. Office of Foreign Assets Control framework. The U.S. State Department and Treasury have confirmed they do not object to negotiations proceeding but have reserved the right to require final approval before any deal closes. This conditional pathway introduces material completion risk regardless of how well negotiations proceed at the corporate level. According to Sherritt's own shareholder communications, the board remains committed to evaluating all viable paths to recapitalisation.

The Bondholder Alternative: Creditor Leverage as Deal Architecture

Holders of Sherritt's 2031 notes have formally identified a competing recapitalisation framework backed by investors described only as credible strategic and financial participants. The bondholder group's public statement made several strategically significant moves simultaneously:

- It asserted that the Gillon Capital proposal should not be treated as the default or sole viable path.

- It signalled that the pace of engagement has not matched the severity of the company's financial circumstances.

- It submitted an emergency financing term sheet to address near-term liquidity needs.

- It effectively positioned itself as both a creditor constituency and a potential recapitalisation partner.

In distressed debt restructurings, the submission of a competing term sheet by an organised noteholder group is rarely a passive or defensive act. It is typically a coordinated effort to force a dual-track process, improve deal economics for creditors, or displace an incumbent bidder whose terms are viewed as unfavourable to the existing capital structure.

The decision to withhold the identities of the alternative investors adds a layer of complexity for Sherritt's board. Evaluating a competing proposal with incomplete counterparty disclosure creates genuine fiduciary challenges, particularly under the scrutiny of TSX governance requirements for change-of-control transactions. Industry observers noting that Sherritt has dropped its previous plan to dissolve Cuban assets will recognise this as a significant strategic pivot that makes the bondholder alternative all the more consequential.

Side-by-Side Comparison of Competing Proposals

| Dimension | Gillon Capital Proposal | Bondholder Alternative |

|---|---|---|

| Proposing Party | Texas-based family office | Organised 2031 noteholder group + undisclosed investors |

| Deal Stage | Exclusive negotiations underway | Submitted; engagement pace criticised |

| Equity Structure | Warrants for up to 55% stake | Recapitalisation framework; terms undisclosed |

| Liquidity Provision | Not publicly confirmed | Emergency financing term sheet submitted |

| Regulatory Exposure | Requires U.S. State Dept. and Treasury final approval | Standard creditor and regulatory process |

| Political Dimension | High; proposer linked to former Trump adviser | Lower; primarily financial and strategic |

| Timeline Certainty | Nine-month post-closing warrant window | Unspecified; urgency emphasised |

The Strategic Premium Embedded in Critical Minerals

One factor that distinguishes the Sherritt situation from a conventional distressed mining scenario is the strategic classification of its core commodities. Nickel and cobalt are formally identified as critical minerals in Canada, the United States, and the European Union, reflecting dependency concerns in battery supply chains, defence applications, and energy transition infrastructure. In addition, critical minerals security has become a central theme for policymakers across Western economies in recent years.

For any investor group seeking to acquire influence over Moa, the asset represents more than its discounted cash flow value under current suspended conditions. It represents optionality on a producing operation in a world where Western-aligned cobalt supply outside the Democratic Republic of Congo remains scarce. The DRC accounts for approximately 70% of global cobalt production, according to the U.S. Geological Survey, making alternative sources in politically navigable jurisdictions disproportionately valuable to supply chain planners.

This strategic premium may partially explain why multiple credible investor groups are competing for influence over the Sherritt outcome despite the apparent complexity and regulatory uncertainty of the situation. Furthermore, battery metals investment trends suggest that institutional appetite for assets with genuine long-term supply chain relevance remains robust even in distressed circumstances.

Risk Scenarios: Mapping the Possible Outcomes

| Scenario | Trigger | Likely Outcome |

|---|---|---|

| Gillon Deal Closes | Exclusive negotiations succeed; regulatory approvals granted | Sherritt retains Cuban assets; equity diluted to 45%; operational restart possible |

| Bondholder Alternative Wins | Board accepts competing proposal | Recapitalisation on creditor-friendly terms; potentially lower political risk |

| Dual-Track Process | Board evaluates both proposals simultaneously | Competitive tension improves deal terms; timeline risk increases |

| Deal Collapse | Neither proposal advances; lenders accelerate debt | Insolvency proceedings or court-supervised restructuring |

| Regulatory Block | U.S. authorities decline final approval | Any agreed deal voided; company returns to Cuban asset dissolution strategy |

The next major ASX story will hit our subscribers first

What the Debt Structure Reveals About Timing Pressure

The 2031 notes at the centre of the bondholder group's organisation carry a maturity date that nominally provides runway. However, the going concern disclosure reframes the relevant time horizon entirely. The operative risk is not the 2031 maturity date but the acceleration clause that allows lenders to demand immediate repayment upon a default declaration.

In practice, distressed mining companies operating under going concern warnings face a narrow window before lender patience expires. The emergency financing term sheet submitted by the bondholder group addresses precisely this gap, providing a potential bridge between the current liquidity shortfall and the completion of any longer-term recapitalisation. Whether Sherritt's board accepts that term sheet will serve as an early and telling signal of which direction the company's leadership is leaning.

Decision Points That Will Define the Outcome

Several near-term milestones carry outsized significance for all stakeholders:

- Board response to the competing proposal: Whether the board agrees to evaluate the bondholder alternative alongside the Gillon exclusive arrangement will determine the process architecture.

- Emergency financing acceptance or rejection: Sherritt's response to the bondholder term sheet is arguably the most immediate signal of board intent.

- Disclosure of alternative investors: If the identities of the bondholder-backed investors become public, the market will be able to assess credibility and strategic fit more concretely.

- U.S. regulatory guidance: Any formal statement from the State Department or Treasury on approval conditions will materially affect deal viability and timing.

- TSX change-of-control approval process: The exchange's governance requirements will set the outer boundary on deal execution timelines regardless of which proposal advances.

The Sherritt rival rescue plan is a rare convergence of geopolitical dislocation, distressed debt dynamics, and critical mineral asset value. The outcome will be shaped not only by financial terms but by the ability of any counterparty to navigate a uniquely complex regulatory environment where political capital and financial capital carry roughly equal weight.

Frequently Asked Questions

What is the Sherritt rival rescue plan?

An organised group of Sherritt's 2031 bondholders has formally presented an alternative recapitalisation proposal to compete with an existing offer from Gillon Capital LLC. The bondholder-backed plan involves undisclosed strategic and financial investors and includes an emergency financing term sheet to address near-term liquidity needs.

Who is Gillon Capital LLC?

Gillon Capital LLC is a Texas-based family office associated with Ray Washburne, who served as a senior adviser in the Trump administration. The firm entered a non-binding preliminary agreement to acquire warrants exercisable for up to 55% of Sherritt, priced at a discount to the company's May 15, 2026 share price, with a nine-month exercise window following deal closing.

Why did Sherritt halt production at its Cuban mine?

Sherritt suspended operations at its Moa nickel and cobalt joint venture in eastern Cuba in February 2026 after U.S. sanctions tightened Cuba's ability to import sufficient oil, triggering an island-wide energy crisis that rendered continued mining operations unviable.

What does the going concern warning mean for investors?

The going concern warning indicates Sherritt may not have sufficient cash to repay debt obligations if lenders declare a default and demand early repayment. It does not mean the underlying mining asset is impaired or depleted, but it does signal acute liquidity fragility that requires resolution through recapitalisation, asset sale, or emergency financing.

What regulatory approvals are required for any rescue deal?

Any transaction must receive final approval from U.S. regulatory authorities including the State Department and Treasury given Cuba sanctions exposure, Toronto Stock Exchange approval for any change of control, and satisfaction of all definitive documentation requirements before warrants can be exercised or equity transferred.

What happens if neither rescue plan succeeds?

If no recapitalisation is completed and lenders accelerate debt repayment, Sherritt would face an acute liquidity crisis likely resulting in insolvency proceedings, court-supervised restructuring, or forced asset sales, potentially including the liquidation of its Cuban joint venture interests.

Want to Stay Ahead of Significant Mineral Discoveries Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including critical minerals like nickel and cobalt that sit at the heart of today's battery supply chain — instantly translating complex data into actionable insights for investors at every experience level. Explore historic discoveries and their remarkable returns, then begin your 14-day free trial to position yourself ahead of the market.