May 15, 2026

Botswana's Stockpile Crisis Reaches Critical Threshold

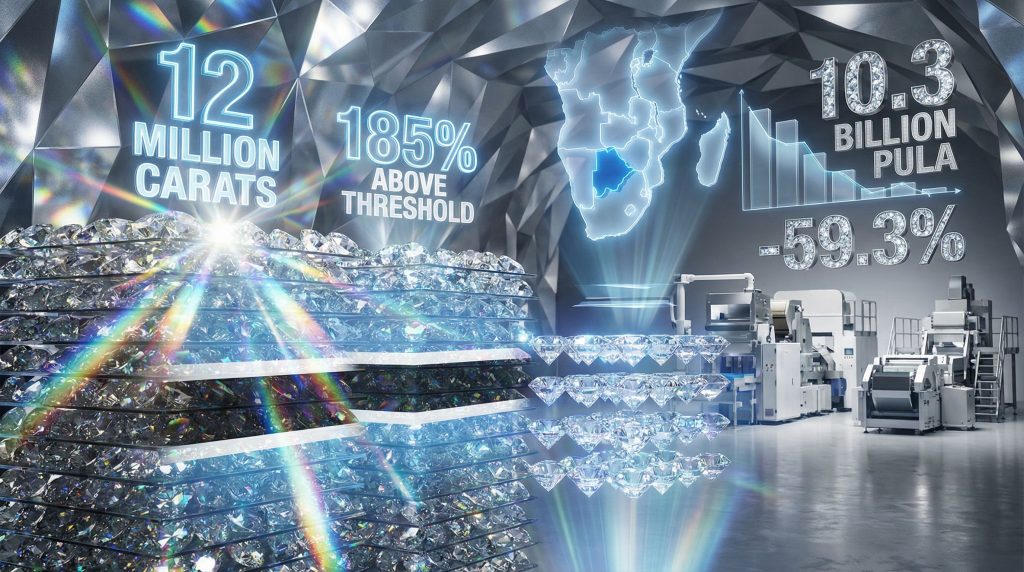

The Botswana diamond glut has reached unprecedented levels, with national inventories swelling to 12 million carats by December 2025. This accumulation represents 185% of the government's maximum allowable threshold of 6.5 million carats, creating the most severe inventory crisis in the nation's mining history. The excess stockpile of 5.5 million carats effectively represents more than three months of historical production capacity held in storage, generating substantial carrying costs and strategic constraints.

The accumulation occurred with remarkable velocity during 2024-2025, reflecting rapid deterioration in global demand conditions that exceeded production adjustment capabilities. Despite operational modifications at Debswana facilities, inventory continued building as market weakness outpaced supply reduction efforts.

Strategic Production Management Framework

Botswana's response involves systematic production restraint rather than accelerated operations, representing sophisticated recognition that supply-side expansion would further depress pricing without generating proportional revenue benefits. The Ministry of Finance indicates that production will remain broadly unchanged until inventory levels approach minimum allowable thresholds, creating operational capacity for future expansion when market conditions stabilise.

This inventory management approach requires secure storage infrastructure for 12 million carats, specialised security arrangements, and substantial working capital allocation that creates ongoing operational expenses. The government operates within structured inventory policies establishing maximum and minimum allowable stockpile levels, though minimum thresholds remain undisclosed in public documentation.

Revenue Impact Quantification

| Financial Metric | Current Projection | Historical Average | Variance |

|---|---|---|---|

| Mineral Revenues | 10.3 billion pula | 25.3 billion pula | -59.3% |

| Government Revenue Exposure | 33% diamond-dependent | Stable historical | Concentrated risk |

| Foreign Exchange Earnings | 75% diamond-related | Traditional levels | Systemic dependency |

The 59.3% revenue decline from 25.3 billion pula historical averages to 10.3 billion pula projections creates budget pressures comparable to major fiscal crises in resource-dependent economies. This 15 billion pula shortfall forces government spending reductions or external financing requirements that compound economic contraction effects throughout domestic markets. Botswana is currently experiencing a significant diamond oversupply crisis, affecting the entire economic landscape.

When big ASX news breaks, our subscribers know first

Laboratory Diamond Technology Disrupts Market Structure

Synthetic diamond production has achieved 20-30% market share penetration within compressed timeframes of approximately five to seven years, representing unprecedented disruption velocity in commodity markets. This technological advancement delivers physically equivalent products at 40-60% price discounts relative to natural diamonds, fundamentally altering competitive dynamics across the industry.

Laboratory-created stones share identical crystal structures, hardness ratings, and optical characteristics with natural diamonds, eliminating traditional quality differentiation arguments. Gemological laboratories distinguish synthetic from natural stones through sophisticated analysis of growth patterns and inclusions, but these distinctions do not affect physical functionality or aesthetic properties.

Manufacturing Technology Evolution

Two primary production methodologies dominate synthetic diamond manufacturing. High-Pressure High-Temperature (HPHT) processes simulate natural formation conditions through extreme pressure and temperature applications, whilst Chemical Vapor Deposition (CVD) methods deposit diamond material layer-by-layer through controlled chemical reactions.

CVD methodologies increasingly dominate industrial-scale production due to superior economics and quality consistency. Manufacturing costs have declined 15-25% annually during 2020-2024, supporting continued market share expansion while maintaining competitive pricing advantages over natural alternatives. This trend follows broader patterns of mining industry evolution towards technologically advanced production methods.

Consumer Preference Transformation

Demographic analysis reveals that younger consumer cohorts demonstrate significantly higher openness to laboratory-created alternatives, suggesting structural market shifts as demographic composition evolves. Millennials and Generation Z consumers increasingly prioritise sustainability attributes and value propositions over traditional rarity arguments supporting natural diamond premiums.

Market Reality: Wedding engagement ring markets have experienced measurable lab-grown penetration of 15-25%, representing significant structural change even in traditionally conservative market segments with high emotional significance.

Economic Dependency Creates Systemic Vulnerabilities

Botswana's diamond-dependent economic architecture reveals critical structural weaknesses during commodity downturns. The combination of 33% government revenue dependency and 75% foreign exchange earnings concentration in diamond-related activities creates dual fiscal and balance-of-payments vulnerabilities without natural offsetting mechanisms.

This dependency profile exceeds concentration levels in most developed economies and matches resource-dependent developing nations facing similar commodity shock risks. When diamond sector revenues decline, both government fiscal capacity and import financing capability contract simultaneously, creating compounding economic pressures.

Employment and Supply Chain Effects

Direct diamond mining employment reaches approximately 10,000-12,000 workers across Debswana and related operations. Indirect employment through transportation, security, retail, and service sectors extends total impact to 40,000-50,000 jobs when supply chain and consumer spending multiplier effects are included.

Mining sector employment disruptions cascade through retail and hospitality sectors serving mining communities, transportation companies handling mineral logistics, financial services supporting mining operations, and manufacturing sectors dependent on mining sector demand.

GDP Contraction Dynamics

Mining sector output historically contributed 20-25% of Botswana's GDP during normal production periods, with diamond-specific contributions representing 15-20% of total economic output. The sector's contraction directly reduced GDP growth rates by 2-3 percentage points, explaining the observed 3% GDP contraction in 2024 and projected 1% contraction in 2025.

Strategic Production Optimisation Under Inventory Constraints

Current production management prioritises inventory normalisation over output maximisation, reflecting understanding that market oversupply requires supply-side discipline rather than production acceleration. Debswana, generating 90% of national diamond sales, implements controlled production schedules responding to policy guidance regarding acceptable inventory thresholds.

The temporary production halts at certain Debswana operations during 2024-2025 represent operational responses to accumulating inventory levels exceeding policy constraints rather than technical difficulties or labour disputes. These strategic adjustments demonstrate sophisticated market management designed to support pricing discipline during weak demand conditions. Furthermore, such approaches align with broader industry consolidation trends across global mining operations.

Inventory Composition Analysis

The 12 million carat stockpile composition by quality grades affects pricing potential and liquidation timelines. Higher-quality stones typically liquidate more readily in weak markets whilst lower-quality inventory may require extended holding periods or discounted pricing to achieve market clearance. Government transparency regarding stockpile quality distribution would improve market confidence in recovery projections.

Minimum Threshold Strategies

While maximum inventory thresholds of 6.5 million carats are publicly disclosed, minimum allowable levels remain implicit in government policy documentation. Clarification of minimum targets would improve precision in recovery timeline projections and provide market participants better visibility into production resumption triggers.

International Trade Pressures Compound Domestic Challenges

Potential US tariffs of 15% on Botswana exports create additional headwinds for diamond market recovery, particularly when combined with possible Indian import duties. This trade policy risk carries particular significance given that 90% of mined diamonds undergo processing in India, meaning supply chain disruptions could amplify existing pricing pressures. Such tariffs impacting markets create complex secondary effects beyond direct trade costs.

The interaction between trade policy and market fundamentals creates multiple risk scenarios:

Trade Risk Assessment Matrix

| Risk Factor | Impact Level | Timeline | Mitigation Options |

|---|---|---|---|

| US Tariff Implementation | High | Immediate | Alternative market access |

| Indian Processing Duties | Medium | 6-12 months | Processing hub diversification |

| Global Demand Weakness | High | Ongoing | Product differentiation |

| Currency Fluctuations | Medium | Continuous | Hedging strategies |

Moreover, Botswana warns diamond oversupply to hit growth as global market conditions continue deteriorating. Consequently, these trade tensions compound an already challenging environment for the nation's diamond sector.

Economic Diversification Strategies for Risk Mitigation

Reducing structural dependence on diamond revenues requires developing alternative mineral production and downstream processing capabilities. Base-metal expansion opportunities include copper, nickel, and cobalt development that leverage existing mining infrastructure and expertise whilst accessing different commodity markets. Such diversified mining investments provide portfolio benefits during commodity-specific downturns.

Alternative Revenue Development

Diversification initiatives focus on copper mining expansion in established geological formations, battery mineral extraction including lithium and cobalt deposits, value-added processing infrastructure for regional mineral beneficiation, and technology integration implementing advanced mining techniques.

These alternatives aim to reduce diamond sector revenue concentration below current 33% levels whilst maintaining mining sector employment and expertise. Regional positioning as a Southern African mineral processing hub could generate service revenues independent of commodity price volatility.

The next major ASX story will hit our subscribers first

Market Recovery Timeline Analysis Under Multiple Scenarios

Recovery prospects depend on converging factors including global economic conditions, consumer sentiment restoration, and competitive positioning relative to synthetic alternatives. Government assessments acknowledge the possibility of non-recovery to historical revenue levels, indicating recognition of structural rather than cyclical market transformation.

Scenario Probability Assessment

Optimistic Recovery (2-3 years) involves global luxury demand rebounding substantially, lab-grown market share stabilising below 30%, international trade tensions resolving favourably, and inventory normalisation completing successfully.

Base Case Scenario (3-5 years) features gradual consumer demand recovery, synthetic competition stabilising at 25-35% share, partial revenue restoration to 60-70% historical levels, and an extended inventory management period.

Structural Transformation (5+ years) encompasses permanent market share loss to synthetics, declining diamond sector economic contribution, alternative revenue sources becoming essential, and economic model requiring fundamental restructuring. Additionally, potential US tariff effects could accelerate structural changes across global commodity markets.

Investment Strategy Implications for Diamond Sector Exposure

The convergence of inventory accumulation, technological disruption, and changing consumer preferences creates complex investment considerations across diamond-dependent assets. Traditional valuation models based on historical demand patterns may inadequately capture structural market evolution toward synthetic alternatives.

Portfolio Risk Assessment Framework

Investors evaluating diamond sector exposure should distinguish between cyclical market corrections with eventual demand recovery, structural market evolution requiring permanent valuation adjustments, technology disruption effects on traditional producer competitiveness, and geographic concentration risks in diamond-dependent economies.

Strategic Positioning Considerations

Traditional Diamond Producers face defensive positioning requirements with potential consolidation opportunities as weaker operators exit markets under pricing pressure. Technology-Enabled Companies such as synthetic diamond manufacturers and processing technology providers benefit from structural market shifts toward laboratory-created alternatives.

Diversified Mining Operations demonstrate superior risk-adjusted positioning during market transitions through reduced diamond concentration and alternative commodity exposure.

What Are the Geological Factors Affecting Recovery Prospects?

Botswana's diamond reserves maintain world-class geological characteristics with established kimberlite pipe deposits at Jwaneng and Orapa mines representing some of the world's most productive diamond sources. These geological advantages provide cost-competitive production capabilities that support market positioning even during challenging pricing environments.

The diamond grade quality from Botswana operations typically exceeds global averages, generating premium pricing potential relative to lower-quality global production. However, synthetic diamond quality improvements have reduced natural diamond quality premiums, limiting the competitive advantage from superior geological resources.

Reserve Life and Resource Optimisation

Established reserves support multi-decade production timelines, providing operational flexibility during extended market downturns. This reserve depth enables strategic production management without resource depletion concerns, supporting inventory optimisation strategies currently being implemented by government policy.

The Botswana diamond glut represents more than a temporary market correction; it signals fundamental structural changes in global diamond markets. For investors and policymakers, understanding these dynamics becomes crucial for navigating the sector's transformation whilst managing associated economic risks and opportunities.

Disclaimer: This analysis contains forward-looking projections regarding diamond market recovery, commodity prices, and economic conditions that involve inherent uncertainties. Actual outcomes may differ materially from scenarios presented due to unpredictable market dynamics, technological developments, or policy changes affecting global diamond markets.

Are You Tracking the Next Major Commodity Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, helping investors identify actionable opportunities whilst markets like Botswana's diamonds face structural challenges. With immediate notifications covering over 30 commodities simplified into clear, gold-equivalent metrics, subscribers gain crucial market advantages during volatile commodity cycles. Begin your 30-day free trial today to position yourself ahead of major market movements and explore why historic discoveries can generate substantial returns even when traditional markets face unprecedented disruption.