June 12, 2026

Understanding Botswana's Diamond Inventory Crisis: A National Economic Challenge

Resource-dependent economies face periodic cycles of abundance and scarcity, but few situations demonstrate the complexities of commodity market dynamics as starkly as the current diamond inventory crisis unfolding across Southern Africa. When global market forces converge with technological disruption and trade policy shifts, the resulting economic pressures can overwhelm even the most established mining operations and create cascading effects throughout entire national economies. The current Botswana diamond stockpile situation exemplifies these challenges, as the nation grapples with unprecedented inventory levels while navigating broader market disruption.

The mechanics of inventory accumulation in extractive industries reveal fundamental tensions between production economics and market absorption capacity. Unlike manufactured goods where production can be easily adjusted to match demand, mining permitting basics involve massive fixed costs, long-term infrastructure commitments, and geological constraints that limit operational flexibility. This structural reality becomes particularly acute when market conditions deteriorate rapidly, leaving producers with limited options beyond production suspension or inventory buildup.

When big ASX news breaks, our subscribers know first

The Scale of Stockpile Accumulation in Southern Africa's Mining Economy

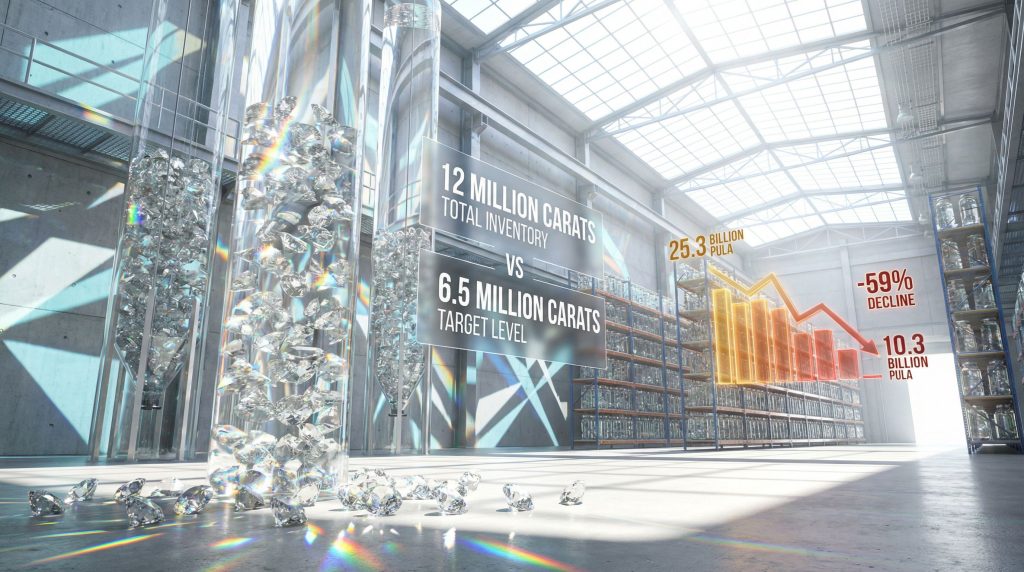

Botswana's current Botswana diamond stockpile reached 12 million carats by the end of December 2025, according to the country's Finance Ministry Budget Strategy Paper. This accumulation represents nearly double the government's allowable inventory target of 6.5 million carats, creating an excess of approximately 5.5 million carats that must be absorbed by global markets before meaningful production increases can resume.

To contextualise this volume, Botswana produced 18 million carats in 2024, ranking as the world's second-largest diamond producer after Russia according to Kimberley Process Certification Scheme data. The current stockpile therefore represents approximately 8 months of production at historical output levels, while the target inventory level represents roughly 4.3 months of production capacity.

The physical and financial implications of managing such large inventories extend far beyond simple storage considerations. Diamond stockpiles require sophisticated security measures, specialised storage facilities, and significant insurance coverage. More critically, the working capital tied up in unsold inventory creates opportunity costs and financing pressures that compound the economic challenges facing mining operations.

How Excess Inventory Reflects Global Diamond Market Disruption

The inventory accumulation directly reflects structural changes occurring across global diamond markets. Lab-grown diamond competition has created unprecedented pricing pressure on natural stones, while weakening global demand in key luxury goods markets has reduced absorption capacity for new production. These forces operate simultaneously to compress pricing and extend the time required to clear existing inventory.

Debswana, the joint venture between Botswana and De Beers that accounts for 90% of the country's diamond sales, was forced to implement temporary production suspensions at several mining operations during 2024 and 2025. This operational response demonstrates the limited tools available to mining companies when faced with unsustainable market conditions: either continue production and accumulate unmarketable inventory, or suspend operations and preserve cash flow while accepting the fixed costs of maintaining idle capacity.

The pricing environment has created a scenario where mineral revenues declined to 10.3 billion pula ($729.24 million) in 2025/26, compared to a historical annual average of 25.3 billion pula. This represents a 59% revenue decline despite maintained production infrastructure and capabilities, illustrating how market conditions can rapidly transform profitable operations into cash flow challenges.

What Economic Forces Created Botswana's 12 Million Carat Surplus?

Multiple converging factors have combined to create the current inventory crisis, with each force amplifying the others to produce an exceptionally challenging market environment for natural diamond producers.

Lab-Grown Diamond Competition Reshaping Natural Gem Markets

The emergence of laboratory-created diamonds as a commercially viable alternative has fundamentally altered the competitive landscape for natural stones. Lab-grown diamonds offer identical physical and chemical properties to natural diamonds at substantially lower production costs, creating a commodity-like price floor that challenges the premium pricing traditionally associated with natural gems.

This technological disruption operates through several mechanisms:

• Direct price competition: Lab-grown stones of equivalent quality retail at significant discounts to natural diamonds

• Consumer acceptance: Growing market acceptance of synthetic alternatives, particularly among younger consumers

• Production scalability: Lab-grown diamond production can be rapidly scaled up or down based on demand conditions

• Marketing challenges: Natural diamond producers must justify premium pricing through origin stories and rarity claims

The impact extends beyond simple price competition. Lab-grown diamonds have created market segmentation where natural diamonds must compete primarily on emotional and aspirational value rather than functional characteristics. This shift requires natural diamond producers to invest heavily in marketing and brand differentiation while accepting compressed profit margins.

Global Demand Weakness Across Key Consumer Markets

Simultaneous demand weakness across major consuming markets has compounded the competitive pressures from lab-grown alternatives. Luxury goods consumption patterns have shifted significantly, with multiple factors contributing to reduced diamond demand.

Economic uncertainty in key markets has led consumers to defer discretionary luxury purchases, while changing demographic preferences have reduced the traditional association between diamonds and major life events. Additionally, younger consumers increasingly prioritise experience-based spending over material goods, further reducing demand for traditional diamond jewellery.

The cumulative effect of these demand-side pressures has been to reduce the market's ability to absorb current production levels, even before accounting for competitive pressure from lab-grown alternatives.

Production Economics vs. Storage Costs in Mining Operations

Mining operations face complex economic calculations when market conditions deteriorate. The decision to continue production versus suspending operations involves multiple cost considerations:

Fixed costs continue regardless of production levels:

• Mine infrastructure maintenance

• Security and safety systems

• Regulatory compliance requirements

• Core workforce retention

Variable costs can be controlled through production adjustments:

• Energy consumption for extraction and processing

• Transportation and logistics

• Additional workforce requirements

• Equipment maintenance directly related to production levels

Inventory costs increase with stockpile accumulation:

• Physical storage facility requirements

• Security and insurance costs

• Working capital financing costs

• Quality preservation measures

The optimisation problem becomes particularly complex when storage capacity constraints are reached, as occurred when the Botswana diamond stockpile exceeded its 6.5 million carat target level. Beyond this threshold, continued production becomes operationally impossible without market sales, regardless of the economic merits of maintaining output.

How Does Botswana's Diamond Stockpile Compare to Global Mining Standards?

Understanding Botswana's inventory situation requires examining how mining operations typically manage inventory levels relative to production capacity and market conditions.

| Metric | Current Level | Target Level | Variance |

|---|---|---|---|

| Total Inventory | 12 million carats | 6.5 million carats | +85% excess |

| Production Capacity | 18 million carats/year | Variable | Suspended operations |

| Revenue Impact | 10.3 billion pula | 25.3 billion pula (historical) | -59% decline |

| Inventory-to-Production Ratio | 0.67 (8 months) | 0.36 (4.3 months) | +86% above target |

Inventory Management Strategies in Resource-Dependent Economies

The 6.5 million carat allowable inventory level established by Botswana's government reflects several operational and financial considerations unique to diamond mining operations. This target represents approximately 4.3 months of production at maximum capacity, which aligns with typical mining industry practices for managing working capital and operational risk.

Mining operations generally maintain inventory levels that balance several competing objectives:

• Market absorption capacity: Inventory levels should not exceed the market's ability to absorb production over reasonable timeframes

• Operational flexibility: Sufficient inventory to maintain sales during temporary production disruptions

• Working capital optimisation: Minimising capital tied up in unsold inventory while maintaining adequate safety stocks

• Storage infrastructure limits: Physical constraints on storage capacity and associated security requirements

The fact that Botswana's inventory has reached 85% above target levels indicates that market absorption has fallen well below the anticipated levels used to establish the original target. This suggests either that the target was based on more favourable market conditions, or that current market disruption exceeds historical precedents used to establish inventory management protocols.

International Mining Stockpile Benchmarks and Best Practices

While comprehensive comparative data across major diamond producing nations remains limited, general principles from industry evolution insights suggest that inventory-to-production ratios above 0.5 (6 months) typically indicate market absorption problems requiring operational adjustments.

Botswana's current ratio of 0.67 places it in territory where production constraints become necessary to prevent further inventory accumulation. The target ratio of 0.36 appears consistent with industry norms for maintaining operational flexibility without excessive working capital requirements.

The decision to suspend production at certain Debswana operations represents a standard response when inventory levels exceed operational parameters. This approach preserves cash flow and prevents further inventory accumulation while maintaining the option to resume production when market conditions improve.

What Are the Macroeconomic Implications of Diamond Inventory Buildup?

The inventory crisis extends far beyond mining sector impacts to create cascading effects throughout Botswana's broader economy, given the country's substantial dependence on diamond revenues.

GDP Contraction Patterns in Commodity-Dependent Nations

Botswana's economy was projected to contract by approximately 1% in 2025, following a 3% contraction in 2024. This represents a cumulative economic decline of roughly 4% over two years, largely attributable to diamond sector weakness.

The contraction mechanism operates through multiple channels:

Direct effects:

• Reduced mining sector employment and wages

• Lower business investment in mining operations

• Decreased demand for mining-related services and supplies

Indirect effects:

• Reduced government spending due to lower tax revenues

• Decreased consumer spending as mining sector wages decline

• Reduced business confidence affecting investment decisions across sectors

Multiplier effects:

• Service sector contraction as economic activity declines

• Construction and real estate impacts from reduced economic growth

• Financial sector effects as loan demand decreases and credit quality concerns emerge

Foreign Exchange Reserve Pressures from Reduced Export Volumes

Diamonds typically contribute three-quarters of Botswana's foreign exchange receipts, making the sector's weakness a critical constraint on the country's external economic position. The 59% decline in mineral revenues translates directly into reduced foreign exchange earnings, creating multiple pressures:

• Import capacity constraints: Reduced ability to finance essential imports

• Currency stability risks: Potential downward pressure on exchange rates

• External debt servicing: Increased difficulty meeting foreign currency debt obligations

• Investment financing: Reduced capacity to attract foreign investment requiring currency stability

Fiscal Revenue Shortfalls and Government Budget Constraints

With diamonds contributing approximately one-third of national revenues, the revenue collapse creates immediate fiscal sustainability challenges. Government responses typically involve some combination of:

Revenue enhancement measures:

• Increased taxation on non-mining sectors

• Improved tax collection efficiency

• Asset sales or privatisation programmes

Expenditure reduction measures:

• Reduced government spending on discretionary programmes

• Deferred infrastructure investment projects

• Public sector employment adjustments

Financing measures:

• Increased government borrowing

• Utilisation of sovereign wealth fund resources

• International financial assistance

According to the Finance Ministry, limited scope for increased output will constrain the economy, unless the non-mining sector performs strongly. This acknowledgment recognises that fiscal sustainability depends either on mining sector recovery or successful economic diversification.

The next major ASX story will hit our subscribers first

How Do Trade Tariffs Amplify Botswana's Diamond Storage Challenge?

Trade policy changes have created additional headwinds for Botswana's diamond exports, complicating efforts to reduce inventory levels through increased sales to traditional markets.

US Market Access Costs and 15% Tariff Impact Analysis

Botswana's diamond exports to the United States now face a 15% tariff, directly increasing the final consumer price and reducing demand elasticity. This tariff operates as a direct tax on consumers, with the burden shared between importers and final purchasers depending on market conditions. Furthermore, detailed tariff impact analysis reveals how such trade barriers create cascading effects throughout global supply chains.

The economic impact of the tariff operates through several mechanisms:

• Price elasticity effects: Higher consumer prices reduce quantity demanded

• Competitive displacement: Imports from non-tariff countries gain market share

• Distribution channel impacts: Importers may shift sourcing to avoid tariff costs

• Profit margin compression: Exporters may absorb portions of tariff costs to maintain market position

For a luxury good like diamonds, demand tends to be relatively price elastic, meaning that tariff-induced price increases can produce disproportionate reductions in quantity demanded. This amplifies the challenge of reducing Botswana's inventory levels through US market sales.

Indian Market Dynamics and Additional Duty Risks

India represents another critical market for Botswana's diamond exports, both as a processing centre and as a consumer market. The Finance Ministry warned that higher tariffs imposed on major diamond consuming markets such as India could prolong lower gem prices and squeeze profit margins.

India's role in global diamond markets extends beyond consumption to include substantial processing and re-export activities. Tariffs on rough diamond imports to India would therefore affect:

• Processing economics: Higher input costs for Indian diamond processors

• Re-export competitiveness: Reduced ability to compete in processed diamond markets

• Supply chain efficiency: Disruption of established trading relationships

• Market concentration: Potential shifts in processing activity to other locations

Export Diversification Strategies for Landlocked Mining Economies

Botswana's landlocked geography creates additional challenges for export diversification, as all shipments must transit through neighbouring countries to reach ports. This geographic constraint limits the country's ability to rapidly shift export destinations in response to changing tariff and market conditions.

Successful export diversification for landlocked mining economies typically requires:

• Transportation infrastructure development: Improved rail and road connections to multiple ports

• Trade agreement negotiations: Preferential access arrangements with multiple partners

• Market development investments: Marketing and relationship-building in new markets

• Quality certification systems: Meeting varying standards requirements across different markets

Can Botswana's Non-Mining Sectors Offset Diamond Revenue Losses?

The Finance Ministry's acknowledgment that economic recovery depends on strong non-mining sector performance highlights the critical importance of economic diversification for Botswana's fiscal and economic sustainability.

Economic Diversification Opportunities in Southern Africa

Botswana possesses several natural advantages that could support diversification efforts, particularly when considering the broader global mining landscape and regional competitive positioning:

Geographic advantages:

• Strategic location in Southern Africa

• Political stability relative to regional averages

• Established transportation infrastructure

Natural resources beyond diamonds:

• Agricultural potential in certain regions

• Tourism attractions including wildlife and natural areas

• Solar energy potential for renewable energy exports

Human capital foundation:

• Relatively high education levels

• English language proficiency

• Mining sector technical expertise transferable to other industries

Tourism, Agriculture, and Service Sector Growth Potential

Tourism represents one of the most immediately viable diversification opportunities, given Botswana's established reputation for wildlife conservation and safari tourism. The sector offers potential for:

• Foreign exchange generation: International tourists provide direct foreign currency earnings

• Employment creation: Tourism is relatively labour-intensive

• Regional development: Tourism can drive development in rural areas

• Value-added services: Hospitality, transportation, and cultural services

Agricultural development faces greater challenges due to climate and soil constraints, but specialised opportunities exist in:

• Beef exports: Established cattle industry with export potential

• Specialty crops: High-value agricultural products suited to local conditions

• Agro-processing: Value-added processing of agricultural outputs

Service sector development could focus on:

• Financial services: Regional banking and insurance hub

• Transportation and logistics: Transit services for landlocked regional countries

• Business process outsourcing: Leveraging English proficiency and education levels

Infrastructure Investment Requirements for Economic Transition

Successful diversification requires substantial infrastructure investments that may be constrained by the current fiscal situation. Key requirements include:

Transportation infrastructure:

• Airport capacity expansion for tourism

• Road and rail improvements for agricultural exports

• Port access improvements through regional cooperation

Communications infrastructure:

• Broadband internet for service sector development

• Mobile network coverage for rural tourism areas

Energy infrastructure:

• Reliable electricity supply for industrial development

• Renewable energy capacity for cost competitiveness

Water infrastructure:

• Irrigation systems for agricultural development

• Water supply reliability for tourism and industrial uses

What Production Strategies Will Clear Botswana's Diamond Excess?

Resolving the inventory crisis requires careful coordination between production management, market development, and demand recovery initiatives.

Inventory Drawdown Timelines and Market Absorption Capacity

The Finance Ministry indicated that production is expected to remain broadly unchanged until inventory levels are drawn down closer to minimum allowable levels. This approach prioritises inventory reduction over production maximisation, reflecting recognition that market absorption capacity currently limits sales more than production capacity.

The drawdown timeline depends on several factors:

Market absorption rate:

• Global diamond demand recovery

• Competitive positioning relative to lab-grown alternatives

• Success in developing new markets or applications

Inventory composition:

• Quality distribution of stockpiled diamonds

• Size and grade characteristics affecting marketability

• Processing requirements before sale

Pricing strategies:

• Willingness to accept lower prices to accelerate sales

• Selective marketing of higher-value stones

• Bulk sales to industrial applications

With 5.5 million carats of excess inventory requiring market absorption, and assuming normal market conditions eventually return, the drawdown period could extend 12-18 months or longer depending on demand recovery rates.

Mine Reopening Economics and Operational Flexibility

The temporary suspension of certain mining operations provides Debswana with operational flexibility to manage production levels based on market conditions. Reopening decisions will likely consider:

Market condition indicators:

• Sustained price recovery in natural diamond markets

• Reduced competitive pressure from lab-grown alternatives

• Inventory levels approaching target ranges

Operational readiness factors:

• Mine maintenance and safety requirements

• Workforce availability and training needs

• Equipment condition and upgrade requirements

Financial considerations:

• Cash flow projections from resumed operations

• Working capital requirements for increased production

• Capital investment needs for operational restart

Strategic Partnerships and Joint Venture Optimisation

The Debswana joint venture structure between Botswana and De Beers provides both advantages and constraints in managing the current crisis. Advantages include:

• Shared risk and resources: Both partners contribute to operational decisions and funding

• Market expertise: De Beers brings global marketing and distribution capabilities

• Operational efficiency: Established management systems and technical expertise

Potential optimisation opportunities might include:

• Marketing coordination: Enhanced cooperation in promoting natural diamond demand

• Market development: Joint investment in developing new consumer markets

• Processing capabilities: Value-added processing to improve profit margins

• Technology development: Research into cost reduction or quality enhancement technologies

How Does Botswana's Situation Reflect Broader Mining Industry Trends?

Botswana's diamond inventory crisis illustrates several broader challenges facing the global mining industry as technological disruption and market dynamics reshape commodity markets.

Commodity Cycle Management in Resource Extraction

Traditional commodity cycle management assumes that supply and demand imbalances eventually resolve through price adjustments that encourage consumption and discourage production. However, Botswana's situation demonstrates how technological disruption can create structural rather than cyclical challenges:

Traditional cycle characteristics:

• Price declines reduce production incentives

• Reduced supply eventually supports price recovery

• Higher prices encourage consumption and new production

Disrupted cycle dynamics:

• Technological alternatives provide price ceilings

• Structural demand shifts may be permanent rather than cyclical

• Production constraints may not generate sufficient price support

This suggests that mining operations may need to develop new approaches to managing commodity cycles when technological substitutes are available.

Technology Disruption Across Traditional Mining Sectors

The lab-grown diamond phenomenon represents a broader pattern of technological disruption affecting multiple mining sectors:

• Synthetic materials: Laboratory alternatives to natural materials

• Recycling technologies: Improved recovery of metals from electronic waste

• Substitution materials: Alternative materials providing equivalent functionality

• Efficiency improvements: Technologies reducing material requirements in end applications

Mining companies increasingly must consider not only geological and market factors, but also technological disruption risks when making long-term investment decisions.

Sovereign Wealth Fund Strategies for Commodity Nations

Countries heavily dependent on commodity revenues face particular challenges in managing economic volatility. However, understanding the broader context of how US economy and tariffs affect global trade patterns becomes crucial for policy makers. Botswana's experience highlights the importance of:

Counter-cyclical fiscal policies:

• Building reserves during high-revenue periods

• Maintaining spending capacity during revenue declines

• Avoiding procyclical fiscal adjustments that amplify economic cycles

Economic diversification investments:

• Using commodity revenues to build alternative economic sectors

• Infrastructure investments that support non-commodity growth

• Education and human capital development

Risk management strategies:

• Hedging or insurance against commodity price volatility

• Flexible production capacity to respond to market conditions

• International cooperation to manage market disruption

What Long-Term Economic Reforms Could Stabilise Botswana's Mining Revenues?

Addressing the structural challenges revealed by the diamond inventory crisis requires comprehensive reforms that enhance the resilience and competitiveness of Botswana's mining sector while accelerating economic diversification.

Value-Added Processing and Downstream Integration

Moving beyond raw diamond exports toward processed products could improve profit margins and reduce vulnerability to commodity price volatility:

Processing facility development:

• Diamond cutting and polishing operations

• Jewellery manufacturing capabilities

• Industrial diamond processing for specialised applications

Technical capability building:

• Training programmes for skilled diamond processing workers

• Technology transfer partnerships with established processing centres

• Quality certification systems for processed products

Market development:

• Branding initiatives for Botswana-processed diamonds

• Direct marketing to consumer markets

• Development of industrial diamond applications

Regional Trade Agreement Opportunities

Botswana's landlocked position and regional integration potential could be leveraged to reduce trade costs and expand market access:

African Continental Free Trade Area (AfCFTA) opportunities:

• Tariff-free access to African markets

• Reduced trade barriers for processed products

• Regional supply chain integration

Bilateral trade agreements:

• Preferential access arrangements with major consuming countries

• Investment protection agreements to attract processing investment

• Technical cooperation agreements for technology transfer

Sustainable Mining Practices and ESG Compliance Benefits

Environmental, social, and governance (ESG) considerations increasingly influence consumer preferences and investment decisions. Botswana could differentiate its diamonds through:

Environmental sustainability:

• Renewable energy use in mining operations

• Water conservation and environmental restoration

• Carbon footprint reduction initiatives

Social responsibility:

• Community development programmes

• Local employment and procurement preferences

• Revenue sharing with affected communities

Governance transparency:

• Public reporting of mining revenues and government receipts

• Anti-corruption measures in mining operations

• Stakeholder engagement processes

These initiatives could support premium pricing for Botswana diamonds relative to alternatives that lack similar certification.

Key Takeaways: Navigating Diamond Market Volatility in 2026

Botswana's diamond stockpile crisis provides important lessons for resource-dependent economies facing technological disruption and market volatility.

Risk Management Strategies for Resource-Dependent Economies

Diversification imperative: The 59% revenue decline despite maintained production capacity demonstrates the vulnerability of commodity-dependent economies to market disruption. Successful risk management requires:

• Economic sector diversification: Development of non-mining revenue sources

• Market diversification: Reduced dependence on single export markets

• Product diversification: Value-added processing and product differentiation

• Financial diversification: Sovereign wealth funds and counter-cyclical fiscal policies

Operational flexibility: The ability to suspend production when market conditions deteriorate provides crucial flexibility for mining operations. This requires:

• Scalable operations: Mine designs that can adjust production levels efficiently

• Inventory management: Storage and financing capabilities for temporary stockpiling

• Workforce flexibility: Employment arrangements that accommodate production variations

Market intelligence: Early identification of technological disruption and market shifts enables proactive responses rather than reactive adjustments.

Market Recovery Indicators and Timeline Projections

Recovery from Botswana's diamond stockpile situation will likely require multiple favourable developments:

Short-term indicators (6-12 months):

• Stabilisation of lab-grown diamond market share growth

• Improved luxury goods consumption in key markets

• Progress in inventory drawdown toward 6.5 million carat target levels

Medium-term indicators (1-3 years):

• Successful differentiation of natural diamonds from lab-grown alternatives

• Diversification of export markets to reduce tariff impact

• Development of non-mining economic sectors

Long-term indicators (3-5 years):

• Sustainable competitive positioning for natural diamonds

• Economic diversification reducing diamond revenue dependence below current one-third of national revenues

• Enhanced processing capabilities creating higher value-added exports

According to recent analysis from Mining MX, "Botswana's diamond glut constrains recovery prospects as weak global prices and lab-grown competition continue to pressure the natural diamond market." Meanwhile, a report by The Independent noted that "Botswana's diamond stockpile crisis reveals the structural challenges facing traditional mining economies in an era of technological disruption."

"The projections and analysis presented in this article are based on publicly available information and current market conditions. Commodity markets are inherently volatile and subject to unpredictable changes in technology, regulation, and consumer preferences. Readers should conduct independent research and consult qualified advisors before making investment or policy decisions based on this analysis."

The resolution of Botswana's diamond stockpile crisis will serve as an important case study for how resource-dependent economies can adapt to technological disruption while maintaining fiscal sustainability and economic growth. Success will require coordinated efforts across production management, market development, economic diversification, and international trade policy to navigate the complex challenges facing traditional commodity exporters in an era of rapid technological change.

Looking to Capitalise on Emerging Mining Investment Opportunities?

Whilst major producers like Botswana face inventory challenges in traditional commodities, these market disruptions often create exceptional opportunities in smaller mining companies making significant discoveries. Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Begin your 30-day free trial today and discover how historic mineral discoveries have generated substantial market returns for early investors.