June 17, 2026

The Capital Architecture Behind BP Selling Stakes in Kaskida and Tiber Projects

Ultra-deepwater oil development operates under a financial logic that is fundamentally different from conventional upstream investment. The further offshore a project sits, the higher the water column above the reservoir, and the more technically complex the extraction architecture, the greater the front-loaded capital commitment required before a single barrel reaches the surface. For even the largest integrated energy companies, this creates a structural tension between ambition and balance sheet discipline. It is within this context that BP selling stakes in Kaskida and Tiber projects becomes not just a corporate transaction, but a window into how the global deepwater industry is evolving its approach to risk allocation.

When big ASX news breaks, our subscribers know first

Understanding the Scale of What BP Is Offering

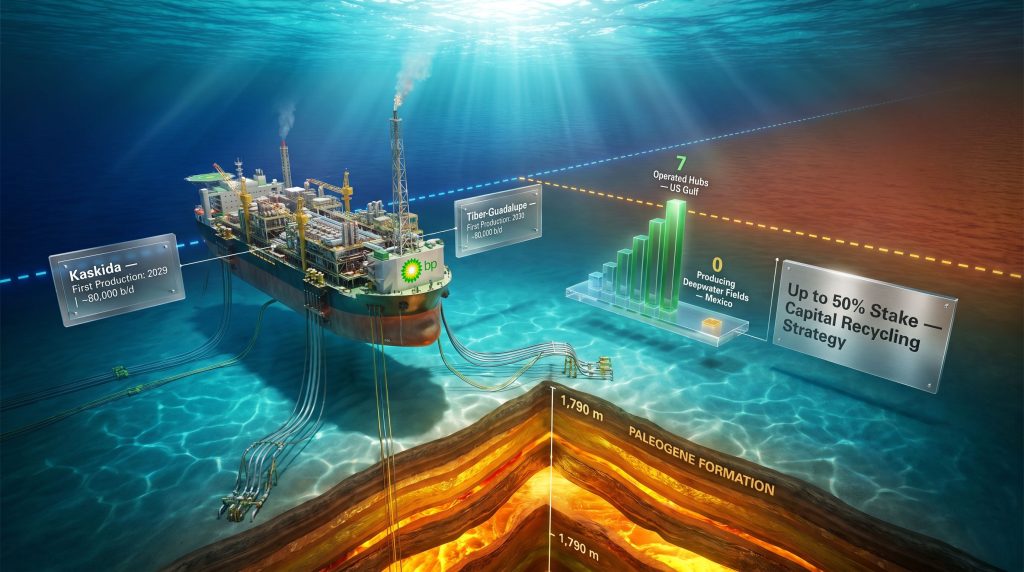

The two projects at the centre of this process represent some of the most capital-intensive upstream developments currently active in the United States. Kaskida, located in the Keathley Canyon block of the US Gulf of Mexico at a water depth of approximately 1,790 metres, was originally discovered in 2006 and carries estimated oil-in-place of approximately 3 billion barrels. That scale of resource took nearly two decades to reach a development decision, underscoring just how technically demanding the Paleogene formation can be to unlock.

BP formally approved Kaskida in 2024, designating it as its sixth operated production hub in the Gulf region. The first development phase involves a floating production platform connected to subsea wells, with first production targeted for 2029 and peak output projected at approximately 80,000 barrels per day. Tiber-Guadalupe, approved in 2025 as a fully BP-owned asset at the time of sanction, is positioned to become the company's seventh operated hub in the Gulf, with first production targeted for 2030 and a comparable peak output figure.

Kaskida and Tiber: Key Project Metrics

| Project | Discovery / Approval | Water Depth | Estimated Resource | First Production Target | Peak Output |

|---|---|---|---|---|---|

| Kaskida | Discovered 2006 / Approved 2024 | ~1,790m | ~3 billion barrels oil-in-place | 2029 | ~80,000 b/d |

| Tiber-Guadalupe | Approved 2025 | Ultra-deepwater | Not publicly disclosed | 2030 | ~80,000 b/d |

Reports from Reuters indicate BP has considered divesting up to 50% of each project, though no final stake size has been confirmed and the company has declined to comment publicly on the sale process. Given the resource scale and strategic positioning of both assets, the transactions are widely expected to be valued in the billions of dollars collectively.

The Strategic Logic Under Meg O'Neill's Leadership

The timing of this process is inseparable from the leadership transition at BP. Meg O'Neill assumed the chief executive role in April 2026, becoming the company's first externally appointed CEO in over a century. Her strategic mandate centres on upstream capital discipline, portfolio rationalisation, and restoring investor confidence following years in which BP's share price materially underperformed its supermajor peers.

The decision to market minority interests in Kaskida and Tiber while retaining operatorship on both is a textbook application of the farm-out model: the operating company preserves technical control and execution authority while bringing in financial partners to co-fund development capital expenditure in exchange for a production interest. This structure has been deployed extensively across global deepwater basins and is the same framework underpinning most of Mexico's international deepwater partnerships.

Retaining operatorship while distributing financial exposure is not a sign of retreat from an asset. It is a proven mechanism through which supermajors accelerate development timelines without overextending their balance sheets at any single project.

This process also sits within BP's broader strategic reversal on renewables. Following sustained investor pressure over returns and strategic direction, BP has materially reduced its emphasis on low-carbon investment and recommitted to upstream oil and gas growth. The Gulf of Mexico is a centrepiece of this repositioning, with BP targeting US production of approximately 1 million barrels of oil equivalent per day by 2030. Consequently, selling minority stakes in its two most significant development-stage Gulf projects is a financing optimisation within a reaffirmed growth strategy, not a directional retreat.

Furthermore, understanding the broader market context is essential here. The current crude oil prices environment plays a meaningful role in shaping how potential partners assess the attractiveness of committing capital to long-dated deepwater projects.

The Paleogene Formation: Geology at the Heart of the Story

Both Kaskida and Tiber sit within the Paleogene formation, a deepwater geological sequence running beneath the Gulf of Mexico that has emerged as one of the most significant hydrocarbon-bearing plays in the Western Hemisphere. Characterised by high-pressure, high-temperature reservoirs at significant water depths, the formation demands advanced drilling and completion technology, but rewards that complexity with substantial recoverable volumes and favourable crude quality.

What makes the Paleogene particularly significant from a geopolitical and investment perspective is its cross-border continuity. The same rock sequences extend across the US-Mexico maritime boundary into the Perdido Fold Belt on the Mexican side. Exploratory drilling on the Mexican side of that boundary has confirmed comparable hydrocarbon volumes and crude quality to the US discoveries, meaning the geological case for Mexican deepwater development is not speculative — it is geologically validated.

This cross-border continuity creates a direct analytical link between BP selling stakes in Kaskida and Tiber and the investment outlook for Mexico's deepwater frontier. The same formation, the same pressure regimes, the same reservoir characteristics. The difference lies entirely in the financing environment, regulatory framework, and operator capability on each side of the maritime line.

Mexico's Deepwater Reality: A Single Project Against Seven Hubs

The contrast between the US and Mexican sides of the Gulf is striking, and it is largely a function of structural financing constraints rather than geological shortcomings.

US Gulf vs Mexican Gulf: Deepwater Development Comparison

| Dimension | US Gulf (BP) | Mexican Gulf (PEMEX / Partners) |

|---|---|---|

| Active deepwater hubs | 7 operated by BP alone | 0 producing deepwater fields |

| First deepwater production | Multi-hub, multi-decade history | Trion project targeting 2028 |

| Peak production achieved | Exceeded 2 million b/d (pre-2020) | Zero barrels from deepwater to date |

| Capital model | Farm-out / risk-sharing with majors | Mixed contracts; PEMEX budget constrained |

| Geological basis | Paleogene / Perdido Fold Belt | Same formation, cross-border continuity |

Mexico's only credible deepwater project with a defined path to production is Trion, discovered by PEMEX in 2012 and developed in partnership with Woodside Energy following regulatory approval by Mexico's CNH. Trion is targeting first production in 2028, with peak output projected at approximately 110,000 b/d of oil and 101 MMcf/d of gas. Sixteen years after discovery, it remains a single-project program on the Mexican side of a basin where BP alone operates seven hubs.

Until 2016, PEMEX was the sole company permitted to pursue deepwater exploration on the Mexican side of the Gulf. The structural consequences of that exclusivity, compounded by PEMEX's severe domestic budget constraints and declining production from legacy shallow-water fields, created a deepwater development deficit that one partnership project cannot meaningfully close. In addition, the trade war impact on oil prices adds another layer of uncertainty for international partners evaluating exposure to projects with decade-long development timelines.

What BP's Approach Reveals About PEMEX's Challenge

The most instructive aspect of BP selling stakes in Kaskida and Tiber for Mexico's energy sector is not the transaction itself, but what it implies about capital requirements at this scale of development.

BP is a supermajor with a strong balance sheet, an established Gulf of Mexico infrastructure network, decades of deepwater operational experience, and a multi-hub production base that generates the cash flows to fund new development cycles. Even with all of those advantages, it is still actively seeking partners to co-fund two projects it has already sanctioned. The financial burden of ultra-deepwater development at the Paleogene scale is simply too large to carry unilaterally, even for a company of BP's size.

For PEMEX, which is navigating severe domestic budget cuts, declining legacy production, and a debt burden that constrains its investment capacity, the financing challenge is compounded by an order of magnitude. Mexico's deepwater program is not just competing with BP's Gulf hubs for international partner interest; it is competing against projects that are already sanctioned, already operated by experienced international majors, and already further along development curves.

The farm-out model that BP is now employing for Kaskida and Tiber is precisely the architecture that Mexico's CNH promoted through its licensing rounds. The structural mechanism is the same. The difference is the operator capacity and the balance sheet standing behind it.

BP's own project pages confirm the company's existing Mexican deepwater exposure. BP holds blocks 1 and 3 in the Southeast Saline Basin in partnership with Equinor and TotalEnergies, and a shallow water position in block 34 in the same basin. However, none of these positions have moved beyond exploration and appraisal phases, and no production timeline has been announced for any of them. Even BP, with its operational track record and capital resources, has not accelerated its Mexican deepwater positions toward development.

The next major ASX story will hit our subscribers first

Key Structural Differences in Deepwater Financing Models

Understanding why the farm-out model works in the US Gulf but faces headwinds in Mexico requires unpacking the specific conditions that make capital partners willing to commit:

-

Regulatory predictability: International capital partners require confidence that the fiscal and regulatory framework will not shift materially between project sanction and first production, a multi-year window.

-

Operator credibility: Financial partners co-investing in a farm-out are buying exposure to the operator's technical capability as much as the geology. BP's Gulf operating track record is among the deepest in the industry.

-

Infrastructure proximity: Existing pipeline, processing, and logistics infrastructure reduces tie-in costs and accelerates production timelines, a significant advantage on the US side of the Gulf.

-

Balance sheet backstop: Even minority partners need confidence that the operator can carry projects through cost overruns or oil price downturns without being forced to defer or cancel development phases.

PEMEX faces structural challenges on most of these dimensions simultaneously, which is why replicating the risk-distribution architecture that BP is deploying for Kaskida and Tiber is significantly more difficult on the Mexican side of the Paleogene. For instance, a broader crude oil price analysis for 2025 highlights how geopolitical and trade dynamics further complicate long-term capital commitments in frontier deepwater environments.

Frequently Asked Questions: BP Selling Stakes in Kaskida and Tiber

What is BP selling in the Kaskida and Tiber projects?

BP has initiated a process to market minority stakes in both the Kaskida and Tiber ultra-deepwater projects in the US Gulf of Mexico. Reports indicate BP has considered selling up to 50% of each project, though no final stake sizes or transaction values have been publicly confirmed.

How much are the Kaskida and Tiber stakes worth?

The transactions are expected to be valued in the billions of dollars given the scale of the projects, their estimated resource volumes, and their strategic positioning within BP's Gulf portfolio. No official valuation has been disclosed.

Will BP retain operational control after the stake sale?

Yes. BP is expected to retain operatorship of both projects, meaning it will continue to manage technical execution and development decisions. The stake sale is structured to bring in capital partners, not to transfer operational control.

When will Kaskida and Tiber start producing oil?

- Kaskida: First production targeted for 2029

- Tiber: First production targeted for 2030

- Both projects are projected to reach peak output of approximately 80,000 barrels per day each

What is the Paleogene formation and why does it matter?

The Paleogene formation is a deepwater geological sequence beneath the Gulf of Mexico characterised by high-pressure, high-temperature reservoirs at ultra-deep water depths. It extends across the US-Mexico maritime boundary into the Perdido Fold Belt, making it geologically relevant to both US and Mexican deepwater development programs. Both Kaskida and Tiber sit within this formation.

Key Takeaways: BP Selling Stakes in Kaskida and Tiber Projects

- BP is marketing minority stakes of up to 50% in each of Kaskida and Tiber as part of a capital-recycling and risk-sharing strategy under new CEO Meg O'Neill

- Kaskida targets first oil in 2029; Tiber targets first oil in 2030, with each projecting peak output of approximately 80,000 b/d

- The Paleogene formation underpinning both projects extends into Mexican waters, creating a direct geological link between BP's divestiture process and Mexico's deepwater investment outlook

- Mexico's deepwater program remains anchored by a single project, Trion, targeting first production in 2028, compared to BP's seven operated hubs across the maritime boundary

- The farm-out model BP is employing mirrors the framework Mexico's CNH has promoted through its licensing rounds; however, PEMEX's fiscal constraints make replication significantly more difficult

- Even for a supermajor with BP's operational depth and financial capacity, ultra-deepwater development at Paleogene scale requires capital partners — a reality that carries important implications for any state-owned operator attempting to build a deepwater program without equivalent resources. The broader oil price rally and shifting geopolitical currents only reinforce why OPEC's influence on oil markets remains a critical variable for deepwater investment decisions globally

Disclaimer: This article contains forward-looking statements and production forecasts sourced from publicly available reporting. All timelines, output projections, and transaction details are subject to change. Nothing in this article constitutes financial or investment advice.

Want to Stay Ahead of Significant Commodity and Resource Discoveries in Real Time?

Discovery Alert's proprietary Discovery IQ model instantly identifies high-potential ASX mineral announcements across more than 30 commodities, delivering actionable insights to subscribers before the broader market reacts — explore historic discovery returns on Discovery Alert's dedicated discoveries page and begin a 14-day free trial to secure a genuine market-leading edge.