June 11, 2026

The Atlantic Shift: How a Structural Energy Crisis Is Redrawing India's Crude Map

When geopolitical shocks ripple through global energy markets, the effects rarely arrive cleanly. They accumulate — through freight rate spikes, insurance surcharges, delayed cargo nominations, and refinery throughput anxiety — until procurement teams and energy ministries are forced to act structurally rather than tactically. That is precisely the dynamic now reshaping India's crude import architecture in 2026, as Brazil crude supplies to India surge at a pace few analysts anticipated even twelve months ago.

Understanding this shift requires looking beyond the headline volume numbers. The real story lies in the convergence of technical compatibility, upstream investment leverage, geopolitical alignment, and the quiet reconfiguration of one of the world's most consequential bilateral energy relationships.

When big ASX news breaks, our subscribers know first

How Gulf Shipping Disruptions Created India's Crude Sourcing Emergency

India's refining sector is among the most throughput-intensive in the world, processing more than 5 million barrels per day across a network of public and private facilities. That scale creates an operational vulnerability that is easy to underestimate: any sustained disruption to a dominant supply corridor does not merely raise costs — it threatens the crude slate continuity that underpins refinery run rates and, ultimately, domestic fuel availability.

The Iran conflict that intensified in early 2026 introduced exactly that kind of disruption. Furthermore, oil price movements across global benchmarks added another layer of complexity for Indian procurement teams navigating an already strained market. Gulf-origin shipments — historically the backbone of India's import basket — became subject to a compounding set of logistical headaches:

- War-risk insurance premiums on tankers transiting the Strait of Hormuz and adjacent waters escalated sharply, adding meaningful costs to each cargo

- Vessel rerouting added voyage days, straining just-in-time crude delivery schedules for refineries operating on lean inventory buffers

- Uncertainty around Iranian crude availability introduced planning risk for Indian refiners that had historically relied on discounted Iranian grades when sanctions permitted

The cumulative effect forced Indian state-owned refiners and private players alike to accelerate a diversification agenda that had previously moved at a deliberate, measured pace. What had been a contingency consideration rapidly became an operational necessity.

What Makes Brazilian Crude Technically Ideal for Indian Refineries

Not all crude diversification is equal. The technical fit between a crude grade and a refinery's configuration determines whether diversification delivers genuine processing economics or merely shifts one set of problems for another.

Brazil's primary export grades — Tupi and Buzios, both produced from the prolific pre-salt Santos Basin — possess a combination of characteristics that align well with India's complex refinery configurations. Indeed, the crude market dynamics currently playing out globally have made these technical advantages all the more commercially attractive for Indian buyers.

Understanding Medium-Sweet Crude: Why Sulfur Content Matters

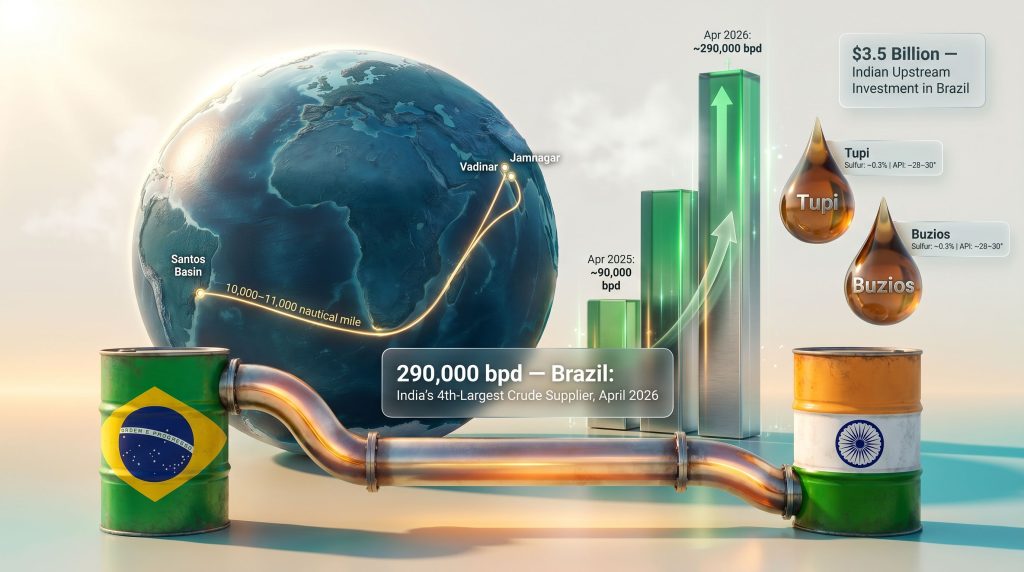

The term medium-sweet refers to crude oil with relatively low sulfur content — typically below 0.5% by weight — combined with moderate API gravity. Tupi and Buzios both carry sulfur levels around 0.3%, compared to Arab Light at approximately 1.8% and Iranian Heavy at roughly 1.7%.

This distinction carries direct financial implications. Lower-sulfur crude reduces the operational load on a refinery's hydrodesulfurization (HDS) units — the processing equipment that strips sulfur from fuel streams. For Indian refineries complying with Bharat Stage VI (BS-VI) fuel standards, which mandate ultra-low sulfur content in diesel and petrol, processing a lower-sulfur feedstock reduces both energy consumption and catalyst costs in the desulfurization process.

Yield Profile: Why Diesel and Jet Fuel Matter to India

Beyond sulfur, the yield structure of Brazilian pre-salt crude is particularly attractive. Both Tupi and Buzios produce a disproportionately high share of middle distillates — the refinery cuts that generate diesel and aviation turbine fuel (ATF). India's consumption growth in both categories has consistently outpaced gasoline demand growth, making middle-distillate-rich crude grades structurally valuable for domestic market alignment.

| Crude Grade | Origin | Sulfur Content | API Gravity | Primary Refined Output |

|---|---|---|---|---|

| Tupi | Brazil (Pre-Salt) | ~0.3% | 28–30° API | Diesel, Jet Fuel |

| Buzios | Brazil (Pre-Salt) | ~0.3% | 28–30° API | Diesel, Jet Fuel |

| Arab Light | Saudi Arabia | ~1.8% | ~33° API | Gasoline, Diesel |

| Iranian Heavy | Iran | ~1.7% | ~31° API | Fuel Oil, Diesel |

Refinery Configuration: Reliance and the Private Sector Advantage

Private refiner Reliance Industries has emerged as the most aggressive buyer of Brazilian crude in India's import mix, accounting for nearly 50% of visible import volumes during January through April 2026. This is not coincidental. Reliance's twin-refinery complex at Jamnagar in Gujarat — collectively one of the largest refining installations on the planet — is configured with extensive secondary processing units that can exploit the yield advantages of medium-sweet Atlantic Basin grades.

State refiners are following a more structured path. BPCL's February 2026 supply agreement with Petrobras — covering 12 million barrels over India's FY27 financial year — represents the first formal long-term procurement contract between an Indian PSU and Brazil's national oil company for this scale of crude volume. The deal establishes a contractual demand floor that insulates BPCL from spot market pricing volatility while giving Petrobras volume certainty for production planning.

The Volume Surge: Quantifying How Fast Brazil Crude Supplies to India Are Growing

The pace of the trade acceleration has been striking even by the standards of a market accustomed to rapid rebalancing. In March 2026, Brazilian crude arrivals at Indian ports averaged approximately 137,000 barrels per day. By April 2026, that figure had effectively doubled, reaching 275,000 to 290,000 bpd — elevating Brazil to the position of India's fourth-largest crude supplier.

The year-on-year comparison is even more instructive. April 2026 volumes were roughly 200,000 bpd higher than the same month in 2025, representing a near-tripling of flows within twelve months. According to Trading Economics data on India's crude imports from Brazil, Brazil's crude exports to India in April 2025 were in the vicinity of 90,000 bpd — a baseline that makes the current trajectory unmistakable.

Brazil supplied approximately 290,000 barrels per day of crude oil to India in April 2026, making it India's fourth-largest crude supplier — up from roughly 90,000 bpd in April 2025.

Forward-looking tanker tracking data indicated that additional Brazilian cargoes were already en route to Indian ports for May 2026 delivery, suggesting the volume surge is not a one-month aberration but a sustained directional shift.

Trade Value Context: From $1 Billion to a Rapidly Expanding Baseline

India's crude imports from Brazil were valued at approximately US$1.01 billion in 2024. Given that volumes have effectively tripled on a year-on-year basis since then, the bilateral crude trade value is on a trajectory to substantially exceed that figure — potentially reaching $3 billion or more on an annualised basis if April 2026 run-rates are sustained. This has meaningful implications for the bilateral trade balance between the two countries and for India's overall energy import expenditure mix.

The Investment Architecture Behind the Trade Relationship

What distinguishes the Brazil-India crude relationship from a purely transactional commodity trade is the depth of upstream investment that underpins it. Indian PSUs ONGC Videsh Ltd (OVL) and BPRL (Bharat Petro Resources Ltd) have collectively committed $3.5 billion to Brazil's upstream oil sector, making Brazil India's largest upstream investment destination in the Americas and its third-largest globally.

This equity presence creates a structural dynamic that goes beyond spot market procurement. Equity crude — crude produced from blocks in which an Indian entity holds a working interest — can be lifted by the investing company at cost-plus pricing, avoiding the spot market premium entirely. This provides a more predictable and often lower-cost supply channel than pure contract or spot purchases.

The BM-SEAL-4 Proposal: Deepwater Equity at Scale

India is actively evaluating a proposal for OVL to acquire an equity interest of up to $1.17 billion in Brazil's offshore BM-SEAL-4 block. This deepwater asset sits within the broader Santos Basin pre-salt play — a geological province that holds some of the largest discovered deepwater oil reserves in the Western Hemisphere.

The strategic logic of equity investment versus long-term supply contracts can be framed as follows:

- Equity crude provides cost-linked supply that moves with production costs rather than market prices, offering protection during demand-driven price spikes

- Long-term contracts (such as the BPCL-Petrobras deal) provide volume certainty but expose the buyer to market-linked pricing mechanisms

- Spot purchases offer flexibility but introduce both price and availability risk — precisely the vulnerability that the Gulf disruption exposed

A combined approach — equity stakes supplemented by long-term contracts and opportunistic spot purchases — represents the most resilient procurement architecture, and India appears to be pursuing exactly this layered model.

Brazil's Downstream Reciprocity Proposal

A less-publicised but strategically significant dimension of the relationship involves Brazil's proposal for Indian capital deployment into its downstream refining infrastructure. As reported by Strat News Global, Brazil has offered to accelerate crude supply volumes in exchange for Indian investment in refinery expansion and access to India's downstream operational expertise.

This reciprocal model mirrors the architecture of India's most strategically embedded energy relationships globally. In exchange for offtake guarantees and capital, India's PSUs gain preferential supply access, project equity, and the ability to export Indian engineering and operational capabilities — a model that has been refined through India's engagement with Russian, UAE, and African upstream assets.

The Brazil-India energy relationship is evolving beyond a buyer-seller arrangement into a vertically integrated bilateral energy partnership encompassing upstream equity, crude trade, and downstream co-investment.

Shifting Buyer Composition: What the Private Sector Surge Signals

The change in who is buying Brazilian crude in India is as analytically significant as the change in how much is being bought.

| Period | Dominant Brazilian Crude Buyer in India | Estimated Share |

|---|---|---|

| Full Year 2025 | State-owned refiners (BPCL, IOC, HPCL) | Majority |

| January-April 2026 | Reliance Industries (Private) | ~50% of visible volumes |

Reliance's dominance in recent months reflects several converging factors. Its Jamnagar complex operates with greater crude slate flexibility than most state refiners, allowing it to capture the yield advantages of Brazilian grades more efficiently. Its commercial procurement team also operates with less bureaucratic lead time than PSU procurement processes, enabling faster response to spot market opportunities as Gulf supply uncertainty intensified.

The competitive dynamic between state and private refiners for Petrobras supply relationships will be worth monitoring. If OVL's BM-SEAL-4 equity investment closes, it would create a preferential supply channel for PSU refiners — potentially rebalancing the buyer mix back toward state refiners over time.

The next major ASX story will hit our subscribers first

BRICS, Bilateral Diplomacy, and the Broader Strategic Context

Energy trade rarely operates in isolation from geopolitical relationships, and the Brazil-India crude axis is no exception. Both nations are BRICS members, and the geopolitical trade shifts reshaping supply corridors globally have in many ways accelerated this bilateral energy alignment. The bloc provides a diplomatic coordination framework that has demonstrably accelerated bilateral energy negotiations. Brazil's foreign ministry maintains regular engagement with its Indian counterpart specifically around the enhancement of oil export volumes as part of a broader strategic agenda.

That broader agenda encompasses:

- Defence procurement cooperation between the two countries

- Digital public infrastructure technology transfer, where India's DPI stack has attracted Brazilian interest

- Critical minerals supply chains, where the growing critical minerals demand driven by the global energy transition positions Brazil's substantial reserves of niobium, rare earth elements, and lithium as a potential long-term supply source for India

- Energy transition cooperation, including biofuels — Brazil is the world's second-largest ethanol producer and a potential partner for India's blending programme

Crude oil functions as the anchor commodity in this multi-dimensional relationship, but the strategic architecture extends well beyond it.

Key Risks and Constraints That Could Limit Trade Expansion

The Freight Cost Equation

The most structurally persistent challenge for Brazil crude supplies to India is simple geography. The voyage from Brazilian loading terminals — primarily in the Santos Basin and Campos Basin off the Southeast Brazilian coast — to India's west coast refineries at Vadinar, Mundra, and Kochi covers approximately 10,000 to 11,000 nautical miles. This compares to roughly 2,500 to 3,500 nautical miles for Gulf crude.

The economics are manageable at scale using Very Large Crude Carriers (VLCCs) — vessels capable of carrying 2 million barrels per voyage — because the per-barrel freight cost on a VLCC is meaningfully lower than on smaller tanker classes. However, the Gulf crude freight advantage does not disappear entirely, and it creates a ceiling on the price discount that Brazilian crude must offer to remain competitive on a landed cost basis.

Petrobras Production Trajectory and Operational Risks

Brazil's export capacity is ultimately constrained by Petrobras's production growth trajectory. The company has outlined production targets extending through 2030 that project continued growth from its pre-salt portfolio, but this plan is subject to:

- Capital expenditure cycles and financing conditions

- Weather and operational risks associated with deepwater production in the Santos Basin

- Regulatory and fiscal framework stability in Brazil

- The pace of FPSOs (Floating Production, Storage and Offloading vessels) being commissioned on new pre-salt fields

Indian Port and Refinery Infrastructure

Not all of India's crude receiving infrastructure is equally equipped to handle a significant increase in VLCC traffic from Brazil. Berth draft limitations, single-point mooring capacity, and crude receiving terminal throughput rates at key west coast ports will require capital investment if Brazilian crude volumes are to scale toward the upper end of projected scenarios.

Scenario Analysis: Where Brazil Crude Supplies to India Could Go by 2030

| Scenario | Key Assumption | Projected Brazil Supply to India (bpd) by 2030 |

|---|---|---|

| Base Case | Gulf disruptions ease; Brazil maintains current supply growth | 300,000-350,000 bpd |

| Accelerated Integration | OVL equity investment closes; refining partnership formalised | 450,000-500,000 bpd |

| Constrained Growth | Freight cost pressures and Petrobras capex delays limit expansion | 200,000-250,000 bpd |

Note: These scenarios represent analytical projections based on current trends and stated strategic intentions. They are not guarantees of future trade outcomes and should not be treated as investment advice. Energy trade volumes are subject to geopolitical, operational, and macroeconomic variables that cannot be predicted with certainty.

The accelerated integration scenario — where OVL successfully closes the BM-SEAL-4 equity stake and a downstream refining partnership is formalised — could realistically position Brazil as India's second-largest non-Gulf crude supplier by 2028, fundamentally reshaping the Atlantic-to-Asia energy trade corridor. Consequently, the trade war impact on oil markets and ongoing geopolitical instability will continue to act as tailwinds for this structural realignment, with downstream implications for tanker markets, refining margins across Asia, and the competitive positioning of other Atlantic Basin producers targeting Indian demand.

Frequently Asked Questions: Brazil Crude Supplies to India

Why is India increasing crude imports from Brazil in 2026?

India is actively diversifying its crude sourcing away from Gulf suppliers following shipping disruptions caused by the Iran conflict. Brazil's medium-sweet crude grades are technically well-suited to Indian refineries, and bilateral investment ties have accelerated long-term supply agreements.

How much crude does Brazil supply to India?

In April 2026, Brazil supplied approximately 275,000 to 290,000 barrels per day to India, making it India's fourth-largest crude supplier. This represents roughly double the volume shipped in March 2026 and approximately 200,000 bpd more than a year earlier.

What crude grades does Brazil export to India?

Brazil primarily exports Tupi and Buzios crude from its pre-salt Santos Basin fields. Both are classified as medium-sweet grades with low sulfur content of around 0.3% and high diesel and jet fuel yields, making them particularly attractive for India's complex refinery configurations.

What is the BPCL-Petrobras deal?

In February 2026, India's state refiner BPCL signed a one-year supply agreement with Brazil's national oil company Petrobras for the purchase of 12 million barrels of crude oil during India's FY27 financial year.

Is India investing in Brazil's oil sector?

Indian PSUs OVL and BPRL have collectively invested $3.5 billion in Brazil's upstream oil sector, making Brazil India's largest upstream investment destination in the Americas. India is also evaluating a further investment of up to $1.17 billion by OVL in the offshore BM-SEAL-4 block, and Brazil has proposed Indian investment in its downstream refining sector.

How does BRICS factor into the Brazil-India energy relationship?

Both nations are BRICS members, and the bloc provides a diplomatic coordination framework that supports bilateral energy negotiations, investment structuring, and broader strategic cooperation across defence, digital infrastructure, and critical minerals sectors.

Want to Track the Next Major Resource Discovery Before the Market Does?

As Brazil's crude surge reshapes global energy corridors and investor attention turns to the commodities underpinning this structural shift, Discovery Alert's proprietary Discovery IQ model delivers real-time ASX mineral discovery alerts — instantly translating complex resource data into actionable opportunities for both traders and long-term investors. Explore how historic mineral discoveries have generated extraordinary returns and begin your 14-day free trial today to position yourself ahead of the market.