July 9, 2026

Global mining dynamics have fundamentally shifted as supply-demand imbalances reshape commodity markets. Brazil iron ore exports continue to gain momentum through emerging operational efficiencies and infrastructure investments that create new competitive advantages in seaborne trade. Furthermore, the convergence of production optimization, strategic port investments, and favourable logistics networks has positioned Brazil to capitalise on sustained Asian steel demand.

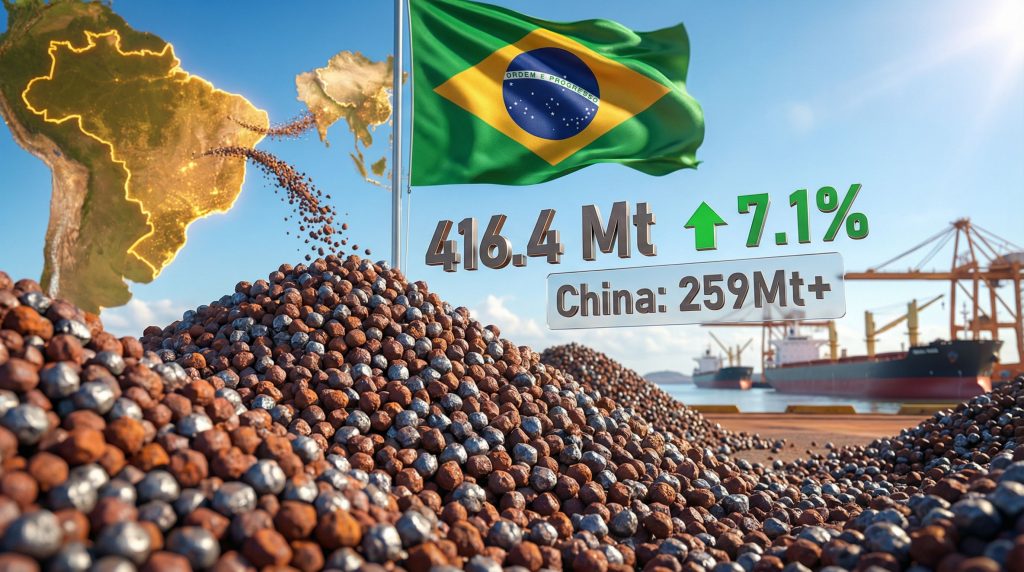

What Drove Brazil's Historic Iron Ore Export Surge in 2025?

Brazil achieved unprecedented iron ore export volumes in 2025, reaching 416.4 million tonnes compared to 388.7 million tonnes in 2024. This remarkable 7.1% year-over-year increase established new benchmarks for the nation's mining sector performance, highlighting positive iron ore price trends despite global volatility.

Production Recovery Fuels Export Momentum

The surge originated from systematic operational improvements across Brazil's largest iron ore mines. Vale's production recovery programme delivered measurable results, with the company reporting 323.2 million tonnes of iron ore production in 2024. This represented a substantial rebound from previous operational disruptions.

Key infrastructure investments between 2020-2024 totalled $2.8 billion, focusing on logistics optimisation and automated handling systems. These improvements enabled capacity utilisation rates to reach multi-year highs across primary production facilities.

The Carajás mining complex achieved enhanced throughput through implementation of autonomous train technology, improving operational efficiency by 12%. Similarly, the S11D mine reached full production capacity of 90 million tonnes per year in 2023. Consequently, this contributed significantly to overall export volume growth.

Chinese Steel Sector Demand Dynamics

China's infrastructure stimulus measures provided crucial demand support for Brazil iron ore exports. The People's Bank of China implemented reserve requirement ratio cuts totalling 50 basis points in 2024. Furthermore, government infrastructure spending acceleration plans boosted raw material consumption.

Chinese steel production maintained robust levels at 1.019 billion tonnes in 2024, sustaining the nation's position as the world's dominant steel producer. This production volume required iron ore imports exceeding 1.18 billion tonnes annually. As a result, it created sustained demand for high-quality Brazilian ore.

The relationship between Brazil iron ore exports and Chinese consumption strengthened throughout 2025. China accounted for 259+ million tonnes of Brazil's iron ore shipments, representing approximately 62.2% of total export volumes.

Competitive Supply Chain Positioning

Brazilian iron ore benefits from superior quality specifications compared to many global competitors. Carajás ore grades typically range from 64-67% Fe content, commanding premium pricing in Asian steel mills. Higher iron content reduces processing costs and improves furnace efficiency.

Port infrastructure efficiency became a decisive competitive advantage. The Ponta da Madeira terminal achieved loading rates of up to 16,000 tonnes per hour using automated systems. Average vessel turnaround times reached 24-36 hours for Capesize vessels.

Despite longer shipping distances to Asian markets, Brazilian ore maintains competitive positioning through quality premiums and efficient logistics networks. The Estrada de Ferro Carajás railway transported 153.4 million tonnes in 2024. This demonstrates the integrated nature of Brazil's iron ore supply chain.

When big ASX news breaks, our subscribers know first

How Do Brazil's 2025 Export Volumes Compare Globally?

Brazil's iron ore export performance in 2025 reinforced its position as the world's second-largest exporter. The nation maintained approximately 25% of global seaborne trade volumes. The achievement becomes more significant when compared against Australia's industry advantages, with Australia exporting 880 million tonnes in 2024.

Record-Breaking Performance Metrics

| Year | Export Volume (Mt) | YoY Growth | Value (US$ Billion) | Average Price ($/tonne) |

|---|---|---|---|---|

| 2023 | 353.0 | – | 27.3 | $77.4 |

| 2024 | 388.7 | 10.1% | 29.86 | $76.8 |

| 2025 | 416.4 | 7.1% | 28.9 | $69.5 |

The data reveals consistent volume growth despite price deterioration, indicating successful market share expansion and operational efficiency improvements. Export value declined to $28.9 billion in 2025, primarily due to average pricing falling from $76.8 to $69.5 per tonne.

Iron ore represented 8.3% of total Brazilian exports in value terms during 2025, down from 8.9% in 2024. This proportional decline occurred despite volume increases, reflecting broader commodity price pressures across global markets.

Market Share Analysis by Destination

China maintained its dominant position as Brazil's primary iron ore customer, absorbing 28.7% of total Brazilian exports in 2025. This slightly increased from 28% in 2024. The concentration underscores the strategic importance of Sino-Brazilian trade relationships for mining sector stability.

Secondary markets provided important diversification benefits:

- Japan imported approximately 95 million tonnes from Brazil in 2024

- South Korea received roughly 65 million tonnes

- Middle Eastern steel mills increased their Brazilian ore consumption

- European markets maintained steady import levels despite regional economic challenges

The geographic distribution reflects logistical considerations, with Asian customers benefiting from established shipping routes and port infrastructure optimised for bulk commodity handling.

Brazil vs. Australia: Competitive Landscape

While Australia maintains export volume leadership, Brazilian ore commands quality premiums in key markets. Australian Pilbara fines typically grade 61-62% Fe content, compared to Brazilian ore grading 64-67% Fe. This creates distinct market positioning strategies.

Shipping economics favour Australia for Asian destinations, with voyage times of 7-10 days to China compared to Brazil's 35-40 days via Cape of Good Hope routes. However, freight rates for Brazil-China routes averaged $15-20 per tonne in 2024. These remained competitive relative to ore quality premiums.

Production capacity comparisons show Australia's ability to scale output more rapidly during demand surges. In contrast, Brazil focuses on consistency and quality optimisation to maintain market position.

What Economic Factors Influenced Iron Ore Pricing Trends?

Iron ore pricing experienced significant volatility throughout 2025, with average prices declining 9.5% year-over-year despite strong demand fundamentals. The Platts 62% Fe CFR China benchmark averaged $104.89 per tonne in 2024. This represented a substantial decrease from $120.27 in 2023.

Price Volatility Despite Volume Growth

Market dynamics reflected complex interactions between supply additions and demand fluctuations. Global iron ore supply exceeded demand by approximately 50 million tonnes in 2024. Consequently, this contributed to inventory accumulation at Chinese ports averaging 130-140 million tonnes throughout the year.

Price ranges varied significantly based on grade specifications, with premiums for high-grade ore maintaining relative stability. Brazilian ore commanded premiums of $3-8 per tonne above benchmark pricing. This depended on specific quality characteristics and delivery terms.

Currency fluctuations added another layer of complexity. Brazilian Real depreciation supported export competitiveness whilst creating revenue translation challenges for international investors.

Guinea's Simandou Project: Supply Side Disruption

The commencement of operations at Guinea's Simandou megaproject in November 2025 introduced substantial new supply capacity to global markets. The project targets eventual production of 120+ million tonnes per annum. Initial ramp-up is expected to reach 60 million tonnes in 2026.

This supply addition created significant pricing pressure throughout 2025, as market participants anticipated increased competition for Asian customers. The project's strategic location and quality specifications positioned it as a direct competitor to both Brazilian and Australian suppliers.

Market analysts struggled to quantify the full impact of Simandou production on global pricing dynamics. This was due to uncertainties around ramp-up timelines and customer acceptance of new supply sources.

Revenue Performance Analysis

Despite record export volumes, Brazilian iron ore revenue declined to $28.9 billion from $29.86 billion in 2024. This revenue compression highlighted the challenging balance between volume growth and price realisation in competitive global markets.

The sector's contribution to total Brazilian exports decreased proportionally, falling from 8.9% to 8.3% of total export value. This decline occurred alongside growth in other commodity exports, including crude petroleum at 12.88% and soybeans at 12.5% of total exports.

Revenue volatility created planning challenges for mining companies and government fiscal projections. This emphasised the importance of operational efficiency and cost management in maintaining profitability.

Which Trade Routes and Infrastructure Drive Export Success?

Brazil's iron ore export success relies heavily on integrated infrastructure networks connecting inland mining operations to coastal export terminals. The Estrada de Ferro Carajás railway system represents a critical component. It spans 892 kilometres and connects the Carajás mining complex to the Ponta da Madeira port facility.

Port Infrastructure Optimisation

Brazilian export terminals achieved significant efficiency improvements through automation investments and operational optimisation:

Major Export Terminal Capacities:

- Ponta da Madeira (Maranhão): 230 Mt/year capacity – Vale's primary export facility

- Tubarão (Espírito Santo): 101 Mt/year capacity

- Guaíba Island (Rio de Janeiro): 54 Mt/year capacity

Loading efficiency reached industry-leading levels, with Ponta da Madeira achieving rates of 16,000 tonnes per hour through automated conveyor systems and vessel loading equipment. Average turnaround times for Capesize vessels improved to 24-36 hours. This enhanced overall supply chain velocity.

These improvements reduced demurrage costs and increased vessel availability for additional voyages. Subsequently, they created competitive advantages in freight-sensitive markets.

Logistics Network Performance

Rail transport optimisation delivered measurable results across Brazil's mining regions. The Estrada de Ferro Carajás transported 153.4 million tonnes in 2024. Meanwhile, the Estrada de Ferro Vitória a Minas handled substantial volumes connecting southeastern mines to the Tubarão port.

Autonomous train technology implementation on the EFC railway improved operational efficiency by 12%. This reduced transit times and increased reliability. These technological advances enabled higher capacity utilisation without proportional infrastructure expansion costs.

Seasonal weather patterns continue to influence transportation schedules. Rainy seasons affect road transport and require careful inventory management at export terminals.

International Shipping Dynamics

Bulk carrier availability and freight rates significantly impact Brazilian iron ore competitiveness in global markets. Brazil-to-China voyages require 35-40 days via Cape of Good Hope routing. This compares to 7-10 days from Australian ports.

Freight rates for Brazil-China routes averaged $15-20 per tonne in 2024, remaining competitive when adjusted for Brazilian ore quality premiums. Baltic Exchange Capesize Index fluctuations created both opportunities and challenges for exporters managing vessel booking strategies.

Port congestion factors occasionally affected delivery schedules, particularly during peak shipping seasons. This occurred when multiple vessels competed for loading berths at major terminals.

How Will Geopolitical Factors Shape 2026 Export Prospects?

Geopolitical developments significantly influenced Brazilian iron ore trade patterns throughout 2025, with implications extending into 2025 demand insights for 2026 projections. The Trump administration's implementation of 50% tariffs on Brazilian products created initial disruption. However, subsequent diplomatic negotiations resulted in gradual removal of many products from tariff schedules.

US-Brazil Trade Relations Impact

The United States' share of Brazilian exports declined from 12% in 2024 to 10.8% in 2025. This reflected trade tension impacts across multiple commodity sectors. Initial tariff impositions targeted broad product categories before refinement through bilateral negotiations.

Iron ore exports to the US market remained relatively insulated from these tensions due to limited direct competition with American production. However, downstream steel trade relationships experienced more substantial disruption during the tariff implementation period.

Diplomatic engagement throughout 2025 resulted in progressive removal of Brazilian products from tariff lists. This suggests potential normalisation of trade relationships during 2026.

China's Economic Stimulus Measures

Chinese economic policy developments provided crucial support for iron ore demand fundamentals. Infrastructure spending programmes announced in Q4 2024 included 3.8 trillion yuan ($525 billion) in investment commitments. These drive steel consumption requirements.

Property sector support measures included mortgage rate reductions averaging 30-50 basis points, potentially stimulating construction activity and associated steel demand. These policy initiatives created optimistic projections for 2026 iron ore consumption levels.

The People's Bank of China's monetary policy adjustments, including reserve requirement ratio cuts, supported broader economic stimulus objectives whilst maintaining financial system stability.

Global Supply Chain Resilience

Steel producers increasingly emphasised supply chain diversification strategies, reducing dependency on single-source suppliers. This trend benefited Brazilian exports by creating opportunities with customers traditionally focused on Australian supply sources.

Strategic stockpiling trends emerged among major consuming nations, with governments and industrial customers building inventory buffers against potential supply disruptions. These stockpiling activities provided additional demand support during periods of price volatility.

Regional trade bloc developments, including potential Mercosur-EU agreement implementation, could create new market access opportunities for Brazil's iron ore exports.

What Investment Opportunities Emerge from Brazil's Export Leadership?

Brazil's iron ore export leadership creates multiple investment opportunities across mining operations, infrastructure development, and supply chain integration. Vale announced investment guidance of $5.0-5.7 billion for 2026. Approximately 60-65% will be allocated to iron ore segment expansion and optimisation projects.

Mining Sector Capital Allocation

Major expansion projects demonstrate sustained capital commitment to Brazilian iron ore production:

- Vargem Grande mine complex expansion adding 18 Mt/year capacity

- Serra Leste mine completion contributing 10 Mt/year additional production

- S11D mine achieving full 90 Mt/year capacity utilisation

Long-term production targets aim for 340-360 million tonnes annual capacity by 2030. This requires sustained investment in both greenfield development and existing operation optimisation.

Technology upgrades focusing on automation and operational efficiency command increasing capital allocation. These demonstrate returns through productivity improvements and cost reduction.

Infrastructure Development Prospects

Port capacity expansion requirements create opportunities for specialised infrastructure investment. Planned investments include $800 million allocated for 2024-2026 port improvements. These focus on automation and throughput optimisation.

Rail network modernisation initiatives target $1.2 billion in digitalisation and automation investments. These projects aim to increase transport capacity without proportional track expansion. This maximises return on existing infrastructure assets.

Renewable energy integration represents a growing investment theme, with targets of 50% renewable energy in mining operations by 2030. This transition creates opportunities in solar, wind, and energy storage technologies specifically designed for industrial applications.

Supply Chain Integration Strategies

Vertical integration opportunities exist throughout the iron ore value chain, from mining through steel production. Joint venture structures with international partners provide risk-sharing mechanisms. Furthermore, they provide access to new technologies and markets.

Downstream processing facility development could capture additional value from Brazilian iron ore production. This is particularly relevant for specialised steel grades requiring high-quality raw materials.

Strategic partnerships with Asian steel producers create opportunities for long-term supply agreements and collaborative technology development programmes. For instance, the BHP strategic pivot demonstrates how major miners adapt to changing market dynamics.

The next major ASX story will hit our subscribers first

What Challenges Could Constrain Future Export Growth?

Environmental compliance requirements increasingly influence mining operations, with new tailings management regulations requiring upstream dam decommissioning by 2027. Industry-wide compliance costs estimate $5-7 billion. Consequently, this creates significant capital allocation pressures.

Environmental and Regulatory Compliance

Brazilian mining operations face stringent sustainability requirements affecting operational permits and expansion approvals. Carbon footprint reduction mandates target 33% reduction by 2030 relative to 2017 baselines. This requires substantial investment in clean energy and process optimisation.

Water usage optimisation requirements challenge traditional mining processes. 65% water recirculation targets demand technological innovation and infrastructure investment. Iron ore processing typically requires 0.3-0.5 cubic metres of water per tonne. Therefore, water management becomes a critical operational parameter.

Tailings dam decommissioning represents a major compliance challenge, with Vale alone requiring decommissioning of 30 dams by the 2027 regulatory deadline. Alternative dry stacking methods demand significant capital investment but reduce long-term environmental risks.

Labour Market and Social Licence Considerations

The Brazilian mining sector employed approximately 196,000 workers directly in 2024. Average wages were 3.8 times the national average. Skilled workforce availability in remote mining regions creates ongoing recruitment and retention challenges.

Community engagement and benefit-sharing agreements require sustained investment in local infrastructure and social programmes. These commitments, whilst socially beneficial, create additional operational costs and complexity.

Safety protocol enhancements following historical incidents demand continuous investment in training, equipment, and monitoring systems. Regulatory compliance costs continue increasing as safety standards evolve.

Market Competition and Pricing Pressures

New supply sources entering global markets, particularly Guinea's Simandou project, create competitive pressures for market share and pricing. The 120+ million tonnes annual capacity from Simandou represents substantial new competition.

Customer diversification strategies among steel producers reduce dependency on traditional suppliers. This requires Brazilian exporters to compete more aggressively for long-term contracts.

Technology disruption in steel production methods, including electric arc furnace adoption and hydrogen-based reduction processes, could alter iron ore quality specifications and demand patterns.

How Do Economic Indicators Support Long-Term Export Projections?

Brazil's trade balance performance provides foundational support for iron ore export projections. The nation achieved a $68.3 billion trade surplus in 2025, declining from $74.2 billion in 2024. Government projections target $70-90 billion for 2026.

Brazilian Trade Balance Optimisation

Export growth of 3.5% in 2025 lagged import increases of 6.7%, creating trade balance pressure that emphasises the importance of high-value commodity exports. Iron ore's contribution to export revenues, whilst proportionally declining, remains strategically significant for foreign exchange earnings.

Currency stability factors affect export competitiveness. Brazilian Real depreciation supports price competitiveness whilst creating revenue translation challenges. Average exchange rates of approximately 5.0 BRL/USD maintained export attractiveness for international customers.

Government fiscal policy continues supporting mining sector development through infrastructure investment and regulatory framework optimisation. This recognises the sector's contribution to economic stability.

Global Steel Demand Forecasting

Infrastructure investment cycles in major consuming economies provide sustained demand visibility for iron ore exports. Chinese infrastructure spending programmes totalling 3.8 trillion yuan create multi-year demand support for raw materials.

Urbanisation trends across developing economies drive construction steel requirements. Population growth and infrastructure development create structural demand growth. These long-term demographic trends support optimistic projections for iron ore consumption.

Automotive and manufacturing sector growth projections indicate continued steel intensity in economic development. This is particularly relevant in emerging markets where infrastructure development remains a priority.

Strategic Reserve Considerations

Resource depletion timelines for major Brazilian deposits extend decades under current production rates, providing long-term export capability. The Carajás mineral province contains reserves supporting decades of production at current extraction rates.

Exploration success rates and new discovery potential remain positive. Geological surveys continue identifying additional iron ore formations in established mining regions. Systematic exploration programmes continue expanding known reserves.

Sustainable extraction practices and long-term viability considerations drive investment in resource efficiency and waste reduction technologies. This ensures optimal recovery from existing deposits.

In addition, analysis shows that Brazil's iron ore market continues demonstrating resilience against global headwinds through operational excellence and strategic positioning.

Disclaimer: This analysis contains forward-looking projections based on current market conditions and available data. Iron ore prices, global demand patterns, and geopolitical factors remain subject to significant volatility. Investment decisions should consider comprehensive risk assessments and professional financial advice. Production forecasts and infrastructure development timelines may vary from projections due to operational, regulatory, or market factors.

Want to Stay Ahead of ASX Mining Discoveries?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant ASX mineral discoveries, helping subscribers identify actionable investment opportunities before the broader market. Begin your 30-day free trial at Discovery Alert and secure your market-leading advantage in mining sector opportunities.