July 9, 2026

When Supply Chains Become Battlegrounds: Russia's Diesel Crisis Explained

Global energy markets have always carried embedded geopolitical risk, but the conventional assumption was that major hydrocarbon producers possessed sufficient infrastructure redundancy to absorb localised disruptions. That assumption is being stress-tested in real time. The convergence of sustained military targeting, domestic supply collapse, and record-breaking European fuel margins in mid-2026 represents a case study in how modern warfare can weaponise energy infrastructure vulnerabilities in ways that ripple across continents.

Understanding why Russia bans diesel exports after Ukrainian drone strikes requires looking beyond the policy announcement itself and examining the structural fragility it exposes. Furthermore, the geopolitical risk landscape surrounding energy infrastructure has grown considerably more complex in recent years.

When big ASX news breaks, our subscribers know first

The Engineering Reality Behind Refinery Vulnerability

Oil refineries are not easily hardened targets. Unlike military installations, they are sprawling, chemically complex facilities where a single precision strike on distillation columns, heat exchangers, or catalytic cracking units can cascade into weeks or months of lost production capacity. Russia's refining sector, much of which was built during the Soviet era and partially modernised over the past two decades, was not designed with drone warfare in mind.

Ukrainian strike campaigns have progressively targeted these facilities, and the cumulative damage has been substantial. Estimates suggest that roughly 25% of Russia's total refining capacity has been disrupted or impaired, equating to approximately 1.75 million barrels per day of lost throughput. To contextualise that figure: it exceeds the entire daily crude oil output of several OPEC member nations.

The damage is not evenly distributed. Refinery complexes in southern and central Russia that handle the bulk of diesel production have been disproportionately affected, creating bottlenecks that cannot simply be rerouted through undamaged facilities.

From Refinery Damage to Filling Station Queues

The supply chain breakdown follows a predictable sequence, but its speed and geographic spread have been striking. Reduced refinery throughput compresses wholesale diesel availability, which in turn strains regional distribution networks, ultimately manifesting as empty forecourts and extended queues at filling stations.

Nearly all of Russia's 83 administrative regions are now reporting some degree of fuel supply disruption. In areas including New Moscow, authorities have introduced purchase limits of 100 litres per transaction as a demand-side rationing measure. Russian Deputy Prime Minister Alexander Novak publicly acknowledged at a televised government meeting that fuel conditions were creating significant public concern, describing the situation at filling stations as complex.

What makes this acknowledgment notable is its context. Russian officials have historically been cautious about attributing domestic economic difficulties to the conflict. The formal recognition that Ukrainian drone strikes on oil refineries are the primary driver of domestic fuel shortages marks a meaningful shift in official communications.

The Export Ban: Scope, Mechanics, and What It Signals

On July 9, 2026, Russia introduced a comprehensive ban on diesel exports applicable to all producers, with an announced end date of July 31, 2026. The government framed it as a temporary stabilisation measure to redirect existing production volumes toward the domestic market.

This was not an isolated policy decision. It sits within a broader framework of export restrictions:

- A complete ban on gasoline exports was already active until September 30, 2026

- A partial ban on gasoline trading remained in place until October 31, 2026

- A programme to begin importing fuel during July was simultaneously announced

The fuel import announcement deserves particular attention. Russia is one of the world's largest hydrocarbon producers. The decision to import fuel is not a logistical adjustment; it is an admission that export redirection alone cannot bridge the supply gap that refinery damage has created. It signals that Russian planners have concluded that domestic repair timelines extend well beyond what short-term export restrictions can compensate for.

Export bans are the fastest available policy instrument when refining capacity is compromised, requiring no new capital expenditure and delivering rapid volume redirection. However, their structural costs accumulate quickly: disrupted long-term supply contracts, reoriented buyer relationships, and permanent trade flow shifts that may not reverse even after the ban is lifted.

The Data That Preceded the Ban

Critically, Russia's export ban formalised a collapse that was already well underway before the official announcement. The following data illustrates the scale of deterioration:

| Metric | Figure | Context |

|---|---|---|

| Russian diesel exports (June 2026) | ~1.8 million metric tons | Down 39% from May 2026 |

| Year-on-year export decline (June) | -46% | vs. 3.35 million metric tons in June 2025 |

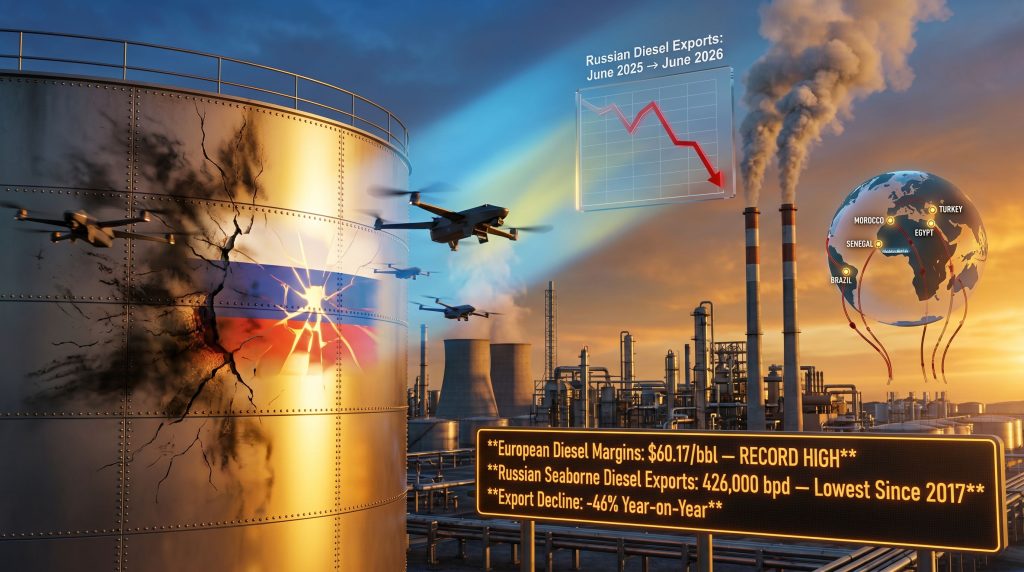

| Seaborne diesel shipments (June avg.) | ~426,000 bpd | Lowest level recorded since 2017 |

| Average export rate (June 2026) | ~480,000 bpd | Down approximately 53% year-on-year |

| Estimated refining capacity disrupted | ~1.75 million bpd | Approximately 25% of total Russian capacity |

Seaborne diesel volumes falling to their lowest point since 2017 before any formal prohibition was enacted means the ban is as much a political signal of domestic prioritisation as it is a practical supply management mechanism. Markets had already begun pricing in reduced Russian supply; the official announcement simply removed residual uncertainty about the direction of policy.

Global Price Shock: Why European Markets Reacted Instantly

Russia held the position of world's second-largest diesel exporter prior to the escalation of Ukrainian infrastructure targeting. That scale of market presence means disruptions to Russian export volumes carry systemic weight in global fuel pricing, particularly in markets that had maintained procurement relationships with Russian suppliers either directly or through intermediary refiners.

The market response was immediate: benchmark European diesel margins surged to a record $60.17 per barrel following the export ban announcement. That figure is not merely a pricing statistic; it reflects the market's collective assessment that available supply from alternative sources cannot quickly or fully replace withdrawn Russian volumes. Consequently, crude oil price volatility has intensified across global benchmarks as traders reassess medium-term supply assumptions.

Who Is Most Exposed to the Supply Reorientation?

In June 2026, the primary buyers of Russian seaborne diesel were distributed as follows:

- Turkey and Brazil collectively absorbed at least 50% of available seaborne cargoes, making them the most immediately exposed to supply reorientation challenges

- Morocco, Egypt, and Senegal had emerged as significant secondary importers during the same period

- These nations, particularly those in Africa, had pivoted toward Russian diesel partly as a cost management strategy given the discounted pricing that geopolitical isolation had created

The challenge these buyers now face is not simply sourcing alternative volumes; it is doing so in a market where global diesel inventories were already described by analysts as dangerously low heading into the disruption. Nations with lower purchasing power face a structural disadvantage when competing against European buyers at elevated margin levels.

The next major ASX story will hit our subscribers first

The Repair Dilemma: Why This Crisis Differs From 2023

Russia implemented a temporary diesel export ban during September and October of 2023, providing a historical reference point. That episode lasted approximately two months before domestic conditions stabilised and export flows resumed. Global markets recovered relatively quickly once Russian volumes returned to the market.

The 2026 situation is structurally different in one critical respect: the source of the supply disruption is ongoing and externally controlled.

| Factor | 2023 Ban | 2026 Ban |

|---|---|---|

| Primary cause | Seasonal demand pressures, logistics constraints | Active military targeting of refining infrastructure |

| Duration control | Within Russia's unilateral management | Dependent on conflict trajectory |

| Repair feasibility | Standard maintenance timelines | Hampered by active retargeting risk |

| Import supplementation | Not announced | Formally announced for July 2026 |

| Structural refinery damage | Minimal | Estimated at 25% of total capacity |

Russia's energy infrastructure operators cannot conduct sustained repair operations at facilities that remain active military targets. Ukraine's campaign has demonstrated the capability to repeatedly strike the same installations, creating an operational environment where repair investment carries significant destruction risk. This is why Russian planners appear to have accepted that restoration will be a medium-to-long-term process rather than a rapid intervention. Moreover, the broader trade war impact on oil prices has added another layer of complexity to already strained global energy supply chains.

The Geopolitical Irony: Who Fills the Gap?

One of the less-discussed dimensions of this supply disruption involves the indirect role of third-country refiners. Several nations purchased Russian crude at significant discounts following Western sanctions regimes, processed that crude domestically, and exported refined products including diesel into global markets. With Russian diesel exports collapsing, these same refined product exporters are now positioned to partially fill the supply gap that Russian refinery damage has created.

This dynamic illustrates a recurring feature of commodity market disruptions: supply gaps rarely remain unfilled for extended periods, but the entities that fill them, and the price at which they do so, can permanently restructure trade relationships and buyer dependencies. In addition, OPEC's influence on oil markets will play a pivotal role in determining how quickly alternative supply sources can be mobilised.

The speed at which European diesel margins reached record levels reveals a structural vulnerability that energy security analysts have flagged repeatedly: concentrated supplier dependency creates systemic exposure that cannot be hedged away through financial instruments alone. Physical supply alternatives take time to develop, and that time gap is precisely where price spikes occur.

Policy Options Remaining for Russian Energy Planners

With refinery repair timelines extended by ongoing strike risk, Russian energy policy is operating within a constrained toolkit:

| Policy Tool | Current Status | Core Limitation |

|---|---|---|

| Diesel export ban | Active until July 31, 2026 | Temporary measure; does not address supply root cause |

| Gasoline export ban | Active until September 30, 2026 | Reduces foreign exchange revenues |

| Fuel import programme | Announced for July 2026 | Logistically complex and cost-intensive |

| Regional purchase limits | Implemented (e.g., 100L cap) | Demand-side management only |

| Refinery repair operations | Ongoing | Constrained by active military targeting |

The combination of export restrictions, fuel rationing, and import supplementation represents a reactive policy posture. None of these tools resolve the fundamental supply deficit; they manage its domestic consequences while the underlying infrastructure damage persists. Furthermore, the broader oil price movements driven by these developments are reshaping energy procurement strategies across multiple regions simultaneously.

Russia bans diesel exports after Ukrainian drone strikes as a short-term stabilisation measure, but the refinery damage reported by gCaptain underscores that this policy response addresses symptoms rather than the structural cause.

Frequently Asked Questions: Russia's Diesel Export Ban

Why Did Russia Ban Diesel Exports in July 2026?

Russia enacted the ban to redirect domestically produced diesel toward its internal market after Ukrainian drone strikes on refining facilities caused widespread supply disruptions, resulting in fuel shortages and extended queues at filling stations across nearly all of the country's administrative regions.

How Long Will Russia's Diesel Export Ban Last?

The ban was announced with a scheduled end date of July 31, 2026. Given that the underlying cause involves ongoing military targeting of energy infrastructure rather than a correctable domestic logistics issue, extension remains a possibility if supply conditions fail to stabilise.

Which Countries Are Most Affected by Russia's Diesel Export Ban?

Turkey and Brazil, which together absorbed at least half of Russian diesel seaborne exports in June 2026, face the most immediate supply reorientation challenge. Morocco, Egypt, and Senegal are also materially exposed as secondary importers.

What Happened to European Diesel Prices After the Ban?

Benchmark European diesel margins rose to a record $60.17 per barrel following the ban announcement, reflecting market assessment of the supply tightening impact on already-constrained global inventories.

How Much Had Russian Diesel Exports Already Declined Before the Ban?

Seaborne diesel exports had already fallen to approximately 426,000 barrels per day in June 2026, the lowest level since 2017, representing a 46% year-on-year decline and a 39% month-on-month collapse from May 2026.

Is Russia Importing Fuel to Compensate for Domestic Shortages?

Yes. The Russian government announced plans to begin importing fuel during July 2026 as a supplementary measure, acknowledging that export redirection alone is insufficient to close the domestic supply gap created by refinery damage.

Disclaimer: This article contains forward-looking analysis, market projections, and interpretive commentary based on publicly available data current at the time of writing. Energy market conditions can change rapidly, and no component of this article should be construed as financial or investment advice. Readers are encouraged to consult independent sources including Reuters and Economic Times Energy World for supplementary reference and updated reporting.

Want to Stay Ahead of Commodity Supply Shocks and Their Market Impact?

When geopolitical events reshape energy and resource markets at speed, Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, helping investors identify actionable opportunities before the broader market reacts — explore historic discoveries and their returns to understand the magnitude of what early positioning can mean, and begin your 14-day free trial today to secure a genuine market-leading advantage.