July 13, 2026

The Hidden Architecture Behind the Brazil Mining Premium

Geological endowment alone has never been sufficient to attract sustained institutional capital into a mining jurisdiction. History is littered with richly mineralised countries that spent decades in the shadow of a perceived risk discount, their resource wealth accessible only to the most opportunistic or patient investors. What actually transforms market perception is a convergence of factors operating simultaneously: infrastructure maturity, regulatory predictability, demonstrated project execution at scale, and the arrival of global capital as a validation signal. Brazil has, over the past several years, been moving through exactly this kind of structural transition. Understanding what is driving the Brazil mining premium, and more importantly, what it means in practical terms for investors conducting due diligence, requires looking well beneath the surface of commodity price cycles.

The concept of the Brazil mining premium has emerged as a shorthand for this repositioning, but it carries a dual meaning that most commentary glosses over. On one side sits a genuine valuation premium, driven by Brazil's exceptional critical minerals demand and the intensifying geopolitical competition for supply chain diversification. On the other sits a cost premium, shaped by evolving royalty structures and new tax instruments that are compressing margins for operators. Both are real. Both must be modelled.

When big ASX news breaks, our subscribers know first

How Brazil's Critical Mineral Position Creates a Structural Valuation Uplift

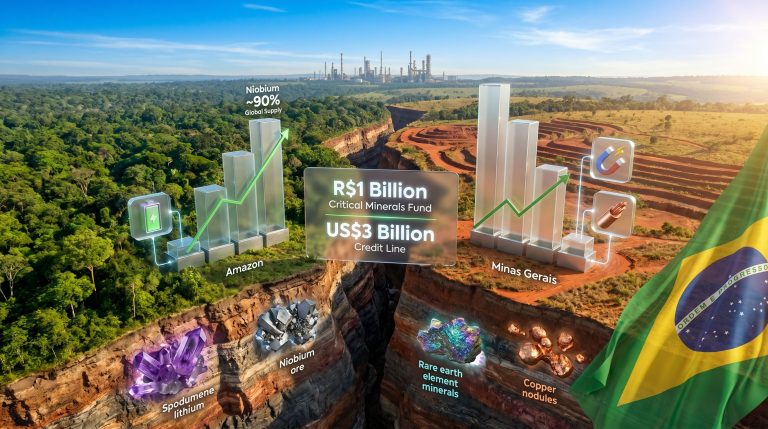

Brazil's geological inventory is, by any objective measure, extraordinary in its breadth and concentration. The country holds approximately 90% of the world's identified niobium reserves, a level of single-country dominance that is almost without parallel in the critical minerals universe. Niobium, used primarily to strengthen steel and increasingly explored for battery applications, has no near-term substitute and no geographically diversified supply alternative. That scarcity dynamic alone commands a structural premium.

Beyond niobium, Brazil ranks:

- 2nd globally in rare earth and graphite reserves

- 3rd globally in nickel

- 6th globally in lithium

The energy transition has amplified the investment significance of this inventory considerably. Projected critical mineral investment across Brazil has been revised upward by approximately 15.2%, with US$21.3 billion earmarked specifically for strategic mineral development across the 2026 to 2030 window. The geopolitical dimension has become equally concrete: the US government's US$565 million financing arrangement with rare earths producer Serra Verde, structured explicitly to exclude Chinese capital participation, represents a real-world expression of how Brazil's mineral assets are being valued in the context of supply chain security competition. Furthermore, rare earth supply chains are increasingly central to how governments and institutions are assessing this positioning.

| Premium Dimension | Key Metric | Investor Implication |

|---|---|---|

| Niobium reserve dominance | ~90% of world reserves | Strategic scarcity premium |

| Critical mineral investment uplift | +15.2% projected increase | Higher valuation multiples for explorers |

| US geopolitical financing | US$565M (Serra Verde deal) | Supply security demand driving capital |

| CFEM royalty (current) | 1%–3.5% of gross revenue | Baseline operating cost factor |

| Proposed royalty hike | +2% points (up to 4% total) | ~8.1% cost increase for producers |

| 2026 excise tax | 1% on iron ore extraction | New environmental cost layer |

| Government royalty intake growth | +55% vs. 2018 baseline | Fiscal pressure on margins |

The Cost Side of the Equation: Royalties, Taxes, and Fiscal Evolution

The valuation premium story is real, but it operates alongside a rising cost structure that sophisticated investors cannot ignore. Brazil's current CFEM royalty framework charges operators between 1% and 3.5% of gross revenue depending on the mineral being extracted. This baseline is broadly competitive internationally, but the trajectory is upward.

Proposed royalty increases of up to 2 additional percentage points would push effective rates toward 4% or higher for certain mineral classes. More significantly, a proposed shift in the calculation basis from net revenue to gross revenue would represent a material change in the effective burden even before the rate increase is applied. Modelling by operators suggests these combined changes could add approximately 8.1% to extraction costs for major producers.

Layered on top of this is a 2026 excise tax reform introducing a new 1% consumption tax on environmentally categorised activities, with iron ore extraction explicitly captured within scope. Taken together, these fiscal changes are projected to increase the government's royalty intake by 55% or more relative to 2018 baseline projections of US$0.9 to 1.3 billion. For investors, the practical implication is clear: project economics cited at current royalty rates require stress-testing against a rising fiscal baseline. Consequently, understanding mining permitting frameworks in comparable jurisdictions provides a useful benchmark when modelling these cost trajectories.

Investor Note: The Brazil mining premium is not a single fixed market rate. It describes two concurrent dynamics that move in opposite directions: a valuation uplift from critical mineral demand and geopolitical positioning, and a cost headwind from evolving royalty and tax structures. Accurate investment analysis requires both to be modelled simultaneously.

Capital Market Behaviour as a Jurisdictional Confidence Signal

Perhaps the most compelling evidence of Brazil's repositioning comes not from policy frameworks or geological surveys, but from where the world's largest mining companies have chosen to deploy capital. Vale, Rio Tinto, BHP, and Anglo American's premium portfolio all maintain significant Brazilian operations, and Kinross Gold operates what is recognised as Brazil's largest gold mine. At the mid-tier level, G Mining Ventures achieved a C$13 billion market valuation after fast-tracking development of its Tocantinzinho gold mine in the Tapajós district, an outcome that participants in the sector have cited as a benchmark proof-of-concept for what execution in the region can deliver.

Project financing conditions in the Tapajós have also evolved. Developers operating in the district have reported receiving multiple competing financing offers, drawing institutional participation from centres including London, Melbourne, and New York. A decade ago, that breadth of institutional attention would have been unusual for a Brazilian junior or mid-tier developer. The broadening of the investor base to include retail capital across North America, Europe, and Asia further reinforces the signal.

How Brazil Stacks Up Against Competing Jurisdictions

The comparative picture is instructive and, in certain dimensions, surprisingly favourable for Brazil:

| Jurisdiction Factor | Brazil | Peru | Canada | Australia | Selected Africa |

|---|---|---|---|---|---|

| Drill permit timeline | Weeks to months | 2–3 years (reported) | Months | Months | Variable |

| Federal regulatory stability | High | Moderate | High | High | Variable |

| State/provincial capacity | Uneven (Pará vs. Minas Gerais) | Variable | Strong | Strong | Often limited |

| Geological mapping coverage | ~30% high-resolution | Moderate | High | High | Low to moderate |

| Critical mineral endowment | Exceptional (niobium, REE, lithium) | Copper and silver dominant | Diverse | Diverse | Cobalt and copper dominant |

| Major miner presence | Vale, Rio Tinto, BHP, Anglo, Kinross | Multiple | Multiple | Multiple | Growing |

| Royalty/tax trajectory | Rising (proposed CFEM hikes) | Elevated | Stable | Stable | Variable |

| Financing market depth | Growing (London, NY, Melbourne) | Moderate | Deep | Deep | Shallow to moderate |

Drill permitting in Brazil typically takes weeks to months. The equivalent process in Peru has been reported to require two to three years, a structural differential that meaningfully accelerates capital deployment timelines and reduces holding costs for exploration-stage investors. That said, certain African jurisdictions may still offer more competitive financing terms in specific commodity classes, a nuance that merits acknowledgment rather than dismissal.

How Brazil's Regulatory Architecture Functions in Practice

Federal Consistency, State-Level Bottlenecks

The most counterintuitive insight for foreign investors entering Brazil is that the federal regulatory framework is genuinely stable and well-understood. It has changed little over extended periods of political volatility, which is itself a meaningful characteristic compared to several competing mining jurisdictions. Brazil's mining sector encompasses more than 7,000 registered companies, which gives the legal architecture real-world testing at scale.

The friction point is not the rules but the administrative capacity to implement them. Newer, high-growth mining states such as Pará face processing bottlenecks across four key regulatory bodies:

- ANM (Agência Nacional de Mineração): the national mining licensing authority

- FUNAI: the federal indigenous affairs agency with oversight over land use near indigenous territories

- ITERPA: Pará's state land registry

- SEMAS: Pará's state environmental secretariat

These agencies are collectively under-resourced relative to the volume of applications flowing through the Tapajós and surrounding districts. By contrast, more established mining states such as Minas Gerais, São Paulo, Mato Grosso, and Goiás have had decades longer to build administrative capacity and process applications more efficiently.

The Temporary Licensing Mechanism

The operational response to capacity gaps in newer mining states has been the widespread use of temporary operational permits, known locally as guia licenses. These instruments allow mines to commence production while full permitting continues to progress through the system on a parallel track. In practice, this mechanism has enabled several Pará operations to reach operating status on compressed timelines without waiting for final permit resolution.

The risk consideration is important: the gap between operational status and full permit resolution represents a contingent liability. Investors conducting due diligence should explicitly identify whether a project holds full permits or is operating under a temporary guia license, and assess the probability and timeline for full resolution.

Why State-Level Relationships Outweigh Federal Connections

Practical permitting authority in Brazil sits with state capitals rather than with federal agencies in Brasília. For Pará, that means Belém. Companies that attempt to resolve state-level permitting delays by escalating through federal channels or seeking foreign embassy intervention have consistently found limited effectiveness. The practical lesson is that early, sustained engagement with state regulators and local communities, initiated well before formal applications are filed, is the primary differentiator between smooth and stalled project timelines.

This dynamic creates a transferable advantage for established operators. Companies like Serabi Gold and Cabral Gold, which have built regulatory relationships over years of operation in the Tapajós, have effectively created a knowledge and relationship infrastructure that newer entrants to the district have been able to access through consultants and partnerships.

Infrastructure's Role in Reshaping Mining Economics

The extension of a paved federal highway from the soybean-producing heartland of Mato Grosso northward to a tributary of the Amazon Tapajós River illustrates, in concrete terms, how physical connectivity can transform regional mining economics. The road now carries approximately 5,000 trucks per day of traffic, connecting mine sites that were previously isolated and enabling shared processing infrastructure that would have been economically impractical without the transport link.

For Serabi Gold, the highway physically connected its two mine sites, Palito and Coringa, enabling them to share a single processing plant. This consolidation eliminated the need for a duplicate tailings facility at Coringa and substantially simplified its permitting requirements, since a separate tailings approval was no longer required. The nearby regional town of Nova Progresso grew to an estimated 30,000 to 40,000 residents as economic activity followed the infrastructure.

Community relations dynamics in the Tapajós illustrate a broader principle with cross-jurisdictional applicability. Local municipal opposition to Serabi's infrastructure decisions softened once the economic multiplier effects of operational activity became visible to residents and local government. Indigenous community relationships, initially characterised as difficult, improved substantially through sustained engagement over time. The counterpoint, drawn from operational experience in other mining regions globally, is instructive: projects that lose community support early face recovery timelines measured in years, not months, and some never recover meaningful social licence at all.

The next major ASX story will hit our subscribers first

Brazil's Geological Upside: The Mapping Gap as an Exploration Indicator

Only approximately 30% of Brazilian territory has been surveyed to high-resolution geological standards, despite the country's continental scale. Canada and Australia, the two most frequently cited peer jurisdictions for geological quality and institutional depth, have substantially higher systematic mapping coverage. However, the exploration upside in Brazil's unmapped territory corresponds to a structurally higher discovery rate potential per dollar of exploration expenditure compared to these more mature markets.

Brazil's lower mapping coverage is not a deficiency in any pejorative sense. It is a structural indicator of remaining discovery potential. The implication is that Brazil's exploration discovery rate relative to exploration expenditure may be structurally higher than peer jurisdictions for an extended period, simply because more of the country's geology has yet to be systematically interrogated.

The Tapajós: Historical Scale and Hard-Rock Potential

The Tapajós district carries the distinction of hosting what historians of the mining industry regard as the largest alluvial gold rush ever documented. During the 1980s, an estimated 20 to 30 million ounces of placer gold were recovered from the region's river systems by artisanal and small-scale miners operating in enormous numbers. The geological inference from that scale of alluvial production is significant: the vast majority of that gold originated from hard-rock source structures that have yet to be systematically located, drilled, or defined.

Cabral Gold's Cuiú Cuiú project, operating within this district, illustrates the exploration conversion potential. Historical drilling programs at the project accumulated approximately 30,000 metres, with subsequent operators adding a further 20,000 metres on top. The result was a doubling of the resource base since acquisition. A recent highlight intercept of 9.5 metres at 87.4 grams per tonne gold underscores the grade potential available in the district's hard-rock systems. With commercial production targeted for the third quarter of 2026 and six drill rigs active simultaneously, the Tapajós is demonstrating that district-scale gold production at meaningful grades is achievable.

Beyond Gold: Brazil's Diversifying Critical Mineral Districts

The gold narrative tends to dominate coverage of the Tapajós, but Brazil's mineral diversification story extends considerably further. According to Brazil's broader mineral profile, the country's resource base spans an exceptional range of commodities across its vast territory:

- Minas Gerais Lithium Valley: an emerging hard-rock lithium production district attracting growing investment interest as battery supply chain competition intensifies

- Pará's broader base: the state hosts the world's largest iron ore mine, major copper and bauxite operations, and generates the second-highest mining revenue of any Brazilian state after Minas Gerais

- Rare earths districts: receiving accelerating geopolitical attention as both US and European supply chain programmes seek non-Chinese sourcing

- Palladium and platinum: ValOre Metals is advancing a palladium-platinum project across a 51,000-hectare district, targeting a preliminary economic assessment by year-end while pursuing gold-focused acquisitions to build an integrated precious metals platform

Brazil's critical minerals bill, passed by the Chamber of Deputies in 2026, signals a legislative intention to formalise the country's position as a strategic supplier, though investors should note that legislative frameworks are distinct from project-specific regulatory approvals or support.

A Practical Due Diligence Framework for Brazil-Focused Mining Investments

The Brazil mining premium is a compelling narrative, but it requires disciplined project-level analysis rather than jurisdiction-level assumptions. The following framework captures the key variables investors should assess:

1. Regulatory Status and State Capacity

- Identify which state the project operates in and research that state's permitting track record and agency resourcing

- Distinguish explicitly between projects holding full environmental and mining permits versus those operating under temporary guia licenses

- Assess the operator's depth of established relationships with state-level agencies and local communities

2. Operational Cost Structure

- Model current CFEM royalty rates (1% to 3.5% of gross revenue) into project economics

- Incorporate the new 2026 excise tax layer into base-case financial models

- Stress-test project returns against proposed royalty increases of up to 2 additional percentage points and a potential shift from net to gross revenue as the calculation basis

3. Workforce and Supply Chain Risk

- Assess regional labour availability: surface and open-pit operations generally have stronger local workforce depth than underground mining, which requires more specialised skills

- Serabi Gold's experience of training underground workers from scratch and integrating approximately 100 Peruvian personnel illustrates the lead time required for specialised workforce development

- Equipment procurement lead times for imported machinery, much of it manufactured in China, can extend to seven months, requiring significantly longer planning horizons than operators in more developed mining regions typically encounter

4. Geological and Resource Validation

- Treat verbally cited project economics as preliminary indicators requiring formal disclosure verification before they can be used in investment models

- Assess the proportion of the district that has been systematically explored relative to the total land package held

- Evaluate how much of the historical drilling data has been independently validated and how much new drilling has been added by the current operator; furthermore, reviewing project feasibility studies from comparable operations provides a useful benchmark for assessing the rigour of resource estimation methodologies

Investor Caution: Jurisdictional risk in Brazil is increasingly viewed as manageable relative to many frontier and emerging mining regions. However, state-specific permitting timelines, local labour market depth, equipment import constraints, and the distinction between temporary and full permits remain material variables requiring project-level due diligence rather than blanket jurisdictional assumptions.

Frequently Asked Questions: Brazil Mining Premium

What exactly is the Brazil mining premium and does it have an official definition?

There is no single officially defined Brazil mining premium as a fixed market rate. The term describes two concurrent dynamics: a valuation premium reflecting Brazil's critical mineral endowment and energy-transition positioning, and a cost premium arising from evolving royalty and tax structures. Both must be understood to form an accurate investment view.

Which minerals are driving Brazil's valuation premium?

Niobium (approximately 90% of global reserves), rare earths, graphite, nickel, and lithium are the primary drivers. The energy transition has elevated demand for all of these, and geopolitical competition between the US and China has further amplified their strategic importance.

Why do state-level relationships matter more than federal connections in Brazil?

Practical permitting authority sits with state-level agencies rather than federal bodies. In Pará, decisions flow through Belém rather than Brasília. Federal escalation has proven largely ineffective at accelerating state-level processes, making early engagement with state regulators and local communities the most reliable path to permitting outcomes.

What is the Tapajós and why is it significant for gold investors?

The Tapajós is a mineral district in Pará state associated with the largest documented alluvial gold rush in recorded history, with an estimated 20 to 30 million ounces of placer gold recovered during the 1980s. Most of that gold is believed to have originated from hard-rock sources that remain largely unexplored, making the district a priority target for systematic exploration investment.

How does Brazil's permitting speed compare to Peru?

Drill permitting in Brazil typically takes weeks to months. In Peru, the same process has been reported to take two to three years. This differential represents a structural competitive advantage for Brazil in attracting exploration capital that requires faster deployment timelines.

How large is Brazil's mining sector as an economic contributor?

Brazilian mining directly and indirectly employs an estimated 2.2 to 2.3 million people and generated approximately US$60 billion in revenue in 2025, with mineral products accounting for roughly 55% of Brazilian exports by value, underscoring the sector's systemic importance to the national economy.

Key Takeaways: Reframing the Brazil Mining Investment Thesis

-

The Brazil mining premium is a dual-natured concept, simultaneously a valuation uplift driven by critical mineral scarcity and geopolitical demand, and a cost headwind from rising royalties and new tax instruments

-

Capital market validation from major miners including Rio Tinto, BHP, Anglo American, Vale, and Kinross, alongside G Mining Ventures' C$13 billion Tapajós valuation, signals a structural shift in how institutional capital perceives Brazilian jurisdictional risk

-

Approximately 70% of Brazil's territory remains unmapped to high-resolution geological standards, representing an exploration upside that is difficult to find in more mature mining jurisdictions

-

Operational success in Brazil depends less on federal policy connectivity and more on state-level relationship depth, early and sustained community engagement, and realistic planning for equipment lead times and workforce development

-

Cabral Gold's expected Q3 2026 first production, Serabi Gold's production ramp toward 50,000 to 60,000 ounces annually, and ValOre Metals' year-end PEA target collectively represent near-term catalysts that will test whether the Brazil mining premium thesis translates into delivered financial performance

-

The recent passage of Brazil's critical minerals bill and the US$565 million Serra Verde financing deal represent external signals that the country's strategic mineral assets are entering a new phase of international contestation, though project-level outcomes will continue to be determined by state-level administrative realities rather than national legislative signals alone

Investors seeking additional operational and jurisdictional perspectives on Brazil's evolving mining landscape can explore panel discussions and analyst commentary through Crux Investor's Analyst's Notes series at cruxinvestor.com.

Want to Identify the Next Major ASX Mineral Discovery Before the Market Moves?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly translating complex mineral data into actionable investment insights, whether you're tracking critical minerals, gold, or emerging commodity plays. Start your 14-day free trial today and explore how historic discoveries have generated exceptional returns for investors who positioned themselves early.