June 30, 2026

The Invisible Architecture of Supply Chain Sovereignty

The modern global economy runs on a category of materials that most consumers never think about. Rare earth elements inside electric vehicle motors, niobium reinforcing aerospace-grade steel alloys, graphite packed into battery anodes, and nickel enabling the electrochemical reactions that power smartphones and grid storage systems. These minerals sit at the intersection of clean energy, advanced manufacturing, and national defense. Yet for decades, the geopolitical architecture governing their supply remained largely invisible to policymakers outside of specialist circles.

That invisibility is now over. The accelerating critical minerals demand driven by electric vehicle adoption, grid-scale energy storage, and next-generation defense systems has forced Western governments to confront an uncomfortable structural reality: the processing and refining of many critical minerals is overwhelmingly concentrated in a single nation. This concentration creates fragility that bilateral partnerships, most notably the deepening framework between Brazil and the United States, are explicitly designed to address.

Understanding the mechanics of Brazil and United States critical minerals cooperation requires looking beyond the diplomatic headlines and into the geological, economic, and geopolitical forces shaping it.

When big ASX news breaks, our subscribers know first

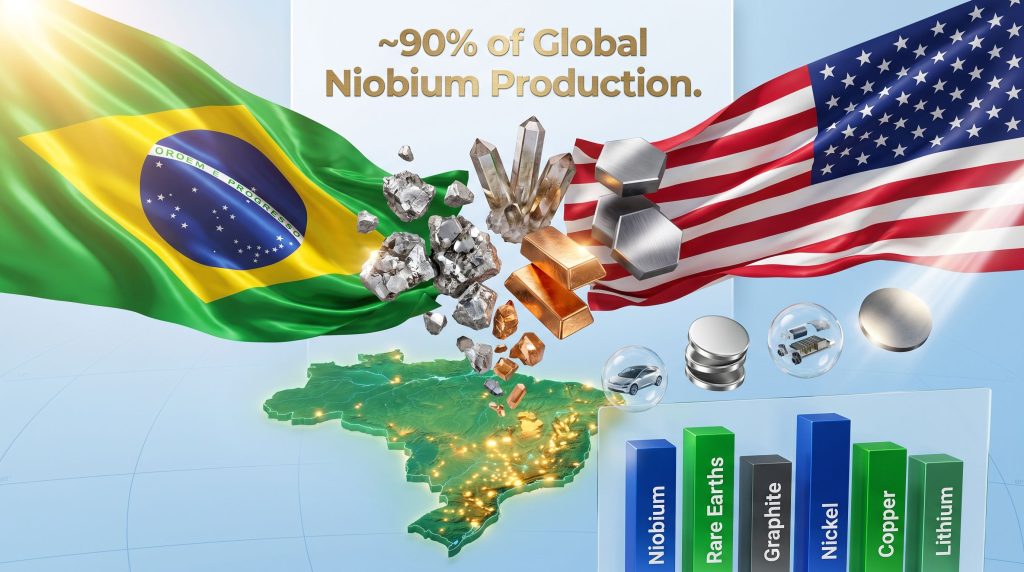

Brazil's Mineral Endowment: Far More Than Raw Material

Brazil's geological profile is genuinely extraordinary. It is not simply a country with mineral reserves. It is, in several key categories, the dominant global producer in ways that have no close parallel.

Brazil's Critical Mineral Reserves: A Resource Superpower in Context

| Mineral | Brazil's Global Standing | Primary Strategic Use |

|---|---|---|

| Niobium | ~90% of global production | High-strength steel alloys, aerospace |

| Rare Earth Elements | Significant reserves, largely underutilised | EV motors, defense electronics |

| Graphite | Large natural deposits | EV battery anodes |

| Nickel | Major laterite deposits | Battery cathodes, stainless steel |

| Copper | Emerging production base | Electrification infrastructure |

| Lithium | Growing exploration pipeline | EV batteries, grid storage |

Niobium deserves particular attention because its strategic profile is widely misunderstood. While lithium and cobalt dominate public discussion about battery supply chains, niobium's near-monopoly status in Brazil is arguably more structurally significant. Approximately 90% of global niobium production comes from a single country, and within Brazil, a substantial share flows through just a handful of mining operations. This concentration means any disruption — whether from regulatory change, infrastructure failure, or geopolitical realignment — has immediate global consequences for aerospace manufacturing and high-strength steel production.

The less well-known dimension of niobium's strategic importance lies in its applications within advanced steel alloys. Small additions of niobium, typically less than 0.1% by weight, can increase steel strength by up to 30%, reducing the material required for structures ranging from pipelines to vehicle chassis. This outsized performance-per-unit characteristic makes niobium strategically valuable in ways that tonnage figures alone do not capture.

Why Geological Wealth Alone Does Not Create Supply Chain Value

There is a critical distinction that is frequently overlooked in policy discussions: the difference between having minerals in the ground and having the industrial infrastructure to convert those minerals into processed, specification-grade materials that manufacturers can actually use.

Brazil's rare earth supply chains illustrate this gap clearly. The country holds substantial rare earth deposits, yet remains a minor player in the global rare earth market because the extraction, separation, and processing infrastructure required to convert ore into magnet-grade neodymium, praseodymium, and dysprosium oxides has not been built at scale. Processing rare earths involves complex hydrometallurgical techniques including solvent extraction, ion exchange, and controlled precipitation chemistry. Each stage requires significant capital investment, technical expertise, and regulatory approval.

The economic multiplier argument is compelling: a tonne of rare earth ore exported generates dramatically less economic value than a tonne of separated rare earth oxide, and a fraction of the value created by finished rare earth magnets. Furthermore, building processing capacity inside Brazil rather than simply shipping ore to offshore refiners is increasingly a condition of domestic political support for foreign investment in the sector.

The Institutional Framework Behind U.S.-Brazil Critical Minerals Cooperation

From Diplomatic Dialogue to Investment Pipeline

The U.S.-Brazil Critical Minerals Working Group represents the operational layer of a broader strategic relationship. Rather than functioning as a traditional trade negotiation body, it is designed as a technical coordination mechanism that aligns regulatory frameworks, investment facilitation processes, and supply chain certification standards across both governments.

This distinction matters for investors. Technical cooperation bodies tend to produce more durable outcomes than politically exposed trade agreements because they operate at the working level, building institutional relationships and regulatory alignment that persist across electoral cycles. The working group format also creates a direct channel between private sector project developers and government decision-makers on both sides, accelerating the resolution of permitting, financing, and offtake questions that would otherwise require years of bilateral negotiation.

For further context on this institutional development, the U.S. Embassy in Brazil has published detailed information on the forum discussions underpinning the partnership.

The Minerals Security Partnership Context

The Minerals Security Partnership, or MSP, is a multilateral initiative involving the United States, European Union, United Kingdom, Canada, Australia, Japan, South Korea, and other allied nations. Its core function is coordinating investment and policy support to develop mineral supply chains outside of Chinese-controlled processing infrastructure.

Brazil's positioning within this framework is particularly significant because it represents the largest and most geologically diverse potential partner in the Western Hemisphere, combining democratic governance with a mineral portfolio that spans virtually every category of strategic importance to the clean energy transition.

U.S. development finance institutions, including the Development Finance Corporation, have already deployed capital into Brazilian mineral ventures spanning rare earth and nickel projects. This is not theoretical future engagement. Active financing relationships exist and are expanding as the strategic rationale for Brazil and United States critical minerals cooperation strengthens.

The China Variable: De-Risking Without Decoupling

Mapping the Dependency Problem

China's position in the critical minerals value chain extends well beyond what reserve statistics suggest. While China does hold significant domestic reserves of several strategic minerals, its decisive competitive advantage lies further downstream: in the processing, refining, and manufacturing stages where raw ore is converted into the specification-grade materials that feed advanced industrial supply chains.

Consider the numbers that define the dependency problem:

- China processes approximately 60% of the world's lithium and 85% of rare earth elements at the refining stage

- China accounts for roughly 70% of global battery anode graphite production

- Chinese entities control significant cobalt processing infrastructure in the Democratic Republic of Congo

- China dominates the production of rare earth permanent magnets, which are essential for EV motors and wind turbines

These figures reveal that the strategic vulnerability is not primarily about where minerals are mined. It is about where they are transformed into usable industrial inputs. A U.S. manufacturer sourcing Australian lithium ore still faces Chinese dependency if that ore travels to Chinese refineries before reaching battery cell factories. Understanding China's rare earth strategy is, consequently, essential context for evaluating the urgency of the Brazil partnership.

Brazil's Strategic Positioning Between Two Giants

Brazil faces a genuinely complex balancing act. China is Brazil's largest trading partner, absorbing substantial volumes of Brazilian agricultural commodities and raw materials including iron ore. Pivoting sharply toward the United States on mineral supply chains carries economic and diplomatic costs that Brazilian policymakers cannot ignore.

The more nuanced reading of Brazil's position is that it is pursuing strategic leverage rather than strategic alignment. As Western demand for Brazilian minerals intensifies, Brazil's negotiating position strengthens on all fronts. The country can credibly insist on in-country processing requirements, favorable financing terms, and technology transfer arrangements as conditions of expanded cooperation, knowing that the United States has limited alternatives within the hemisphere.

Investment Opportunities and the Processing Infrastructure Thesis

Where the Financial Opportunity Actually Lies

For investors tracking Brazil and United States critical minerals cooperation, the most significant financial opportunity is not in primary mine development. Exploration and extraction, while capital intensive, represent the least differentiated segment of the value chain. The structural opportunity lies in processing and refining infrastructure, where value addition is highest and where Western supply chains are most exposed.

A scenario analysis of what a fully integrated Brazil-U.S. mineral supply chain could look like by 2035 illustrates the progression:

- Stage 1: Accelerated exploration and resource definition across niobium, rare earth element, and nickel deposits, supported by geological survey data sharing and exploration financing

- Stage 2: Construction of processing facilities on Brazilian soil, backed by blended finance structures combining DFC capital, Export-Import Bank instruments, and private equity

- Stage 3: Certified minerals entering U.S. manufacturing supply chains under preferential trade terms, with verifiable chain-of-custody traceability

- Stage 4: Brazilian-refined battery materials feeding North American EV production lines and defense manufacturing programs

The blended finance model deserves particular attention. Public development capital, such as DFC deployment, effectively de-risks the first tranche of investment in processing facilities, enabling private capital to enter at scale at later project stages when technical and regulatory uncertainties have been resolved. This sequencing is well understood in development finance circles but is frequently underestimated by equity market participants assessing Brazilian mineral plays.

In addition, the U.S. critical minerals push under domestic policy frameworks is creating further incentives for accelerating this investment pipeline.

Key Barriers That Cannot Be Dismissed

| Cooperation Model | Strengths | Weaknesses |

|---|---|---|

| Raw material export agreements | Fast to implement, low complexity | Minimal value-add for Brazil, volatile pricing |

| Joint processing investment | High value retention, strategic depth | Capital intensive, long development timelines |

| Technology transfer arrangements | Builds long-term capacity | Requires sustained political commitment |

| Blended finance structures | Reduces risk, accelerates deployment | Complex governance, coordination challenges |

Brazil's environmental licensing framework is among the most complex in the world. Indigenous land rights obligations under Brazilian constitutional law create consultation requirements that can extend project timelines by years, particularly for mineral deposits located in or near protected territories. The Amazon region, which contains significant mineral prospectivity in areas such as the Carajas mineral province, is also subject to intense environmental scrutiny at both domestic and international levels.

Infrastructure gaps compound this challenge. Many of Brazil's most prospective mineral deposits are located in remote areas of the Amazon basin or the Cerrado, requiring investment in roads, power supply, and logistics networks before mining or processing operations become commercially viable. These infrastructure requirements are not trivial and represent a hidden capital cost that project financial models must account for carefully.

Comparing Brazil Against Other U.S. Mineral Partners

Friend-Shoring in Practice

| Partner | Geological Strength | Processing Capacity | Governance | Proximity to U.S. |

|---|---|---|---|---|

| Australia | Strong, diverse | Advanced | Very High | Distant |

| Canada | Moderate, diverse | Strong | Very High | Adjacent |

| DRC | Exceptional (cobalt, copper) | Limited | Elevated Risk | Distant |

| Brazil | Exceptional, highly diverse | Underdeveloped | High | Hemispheric |

Australia brings deep institutional alignment through Five Eyes intelligence and defense relationships, along with more developed mineral processing infrastructure. However, its geographic distance from U.S. manufacturing centers adds logistical complexity and cost. Canada offers the closest geographic partnership but has a narrower tropical mineral profile, lacking Brazil's niobium dominance and rare earth scale.

Brazil's combination of geological diversity spanning niobium, rare earths, nickel, graphite, copper, and lithium, paired with democratic stability and Western Hemisphere geography, makes it the most strategically valuable underdeveloped mineral partner available to the United States at this point in the energy transition.

The next major ASX story will hit our subscribers first

Nickel, Graphite, and Copper: The Battery Supply Chain Anchors

Brazil's nickel deposits are predominantly laterite-type, formed through tropical weathering of ultramafic rocks over geological timescales. Laterite nickel processing has historically been more technically challenging than processing sulphide nickel ores, which yield more easily separable concentrate. However, emerging high-pressure acid leach, or HPAL, technology has substantially improved the economics of laterite processing, and battery-grade mixed hydroxide precipitate can now be efficiently produced from Brazilian laterite feedstock.

Graphite's role in lithium-ion batteries is frequently underappreciated in mainstream coverage. Every lithium-ion cell requires a graphite anode, and the anode typically accounts for a larger mass of critical mineral content than the cathode in most commercial battery chemistries. Brazil's natural graphite deposits, particularly in the states of Minas Gerais and Bahia, represent a meaningful alternative to Chinese-sourced anode material, though beneficiation and purification to battery-grade specification — typically 99.95% or higher purity — requires investment in downstream processing.

Copper demand projections deserve attention in the context of electrification broadly. Estimates suggest global copper demand could increase by 50% or more by 2040 driven by grid expansion, EV charging infrastructure, and renewable energy installations. Brazil's copper production base, while currently modest relative to Chile or Peru, is expanding and will likely attract significant exploration capital as the supply gap thesis strengthens. The broader energy security role of these minerals further underpins the long-term strategic rationale for investment in Brazilian processing capacity.

The Road Ahead: Milestones That Will Define Partnership Maturity

Measuring the real progress of Brazil and United States critical minerals cooperation requires tracking concrete outcomes rather than diplomatic statements. The indicators that matter most include:

- Formalisation of investment protection frameworks with clear arbitration mechanisms acceptable to U.S. institutional investors

- Progress on in-country rare earth processing capacity, specifically the establishment of separation facilities capable of producing battery-grade and magnet-grade rare earth oxides

- Volume and diversity of U.S. private capital deployed into Brazilian processing ventures, not just exploration plays

- Development of supply chain traceability systems that can meet the verification requirements of U.S. manufacturers operating under domestic content rules

- The expansion of bilateral cooperation to encompass Chile, Argentina, and Peru under a Western Hemisphere minerals architecture modelled on the Brazil framework

For those seeking independent analysis of how this partnership might evolve, the Columbia University Energy Policy Centre has published a detailed assessment of Brazil's potential role in diversifying U.S. critical mineral supply.

The long-term strategic question is not simply whether Brazil and the United States can build a stronger bilateral mineral relationship. It is whether the Western Hemisphere can construct a self-reinforcing critical minerals ecosystem capable of genuinely competing with Chinese supply chain dominance across the full value chain from ore in the ground to specification-grade materials at factory gate.

The geological foundation for that ecosystem exists in extraordinary abundance. The institutional architecture is being actively constructed. Whether the capital, the political will, and the processing infrastructure follow at the speed required by the energy transition timeline remains the central uncertainty that investors, policymakers, and strategic planners are working to resolve.

This article is intended for informational purposes only and does not constitute financial or investment advice. Projections, scenarios, and forward-looking statements involve inherent uncertainty and should not be relied upon as predictions of future outcomes.

Want to Capitalise on the Next Major Critical Minerals Discovery Before the Broader Market?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant ASX mineral discoveries — spanning nickel, rare earths, graphite, copper, and beyond — are announced, transforming complex data into clear, actionable investment insights for both short-term traders and long-term investors. Explore historic examples of major mineral discoveries and their extraordinary returns, then begin your 14-day free trial today to ensure you're positioned ahead of the market when the next transformative discovery is announced.