July 24, 2026

Brazil emerges within this context as a potentially transformative force in rare earth markets, leveraging substantial geological advantages and strategic partnerships to challenge existing supply chain structures. The country's approach extends beyond traditional resource extraction, encompassing comprehensive value chain development and international collaboration frameworks designed to reduce global mineral supply vulnerabilities. As the critical minerals energy transition accelerates globally, Brazil's brazilian rare earth strategy positions the nation as a key player in reshaping international supply chains.

Brazil's Geological Advantages and Reserve Position

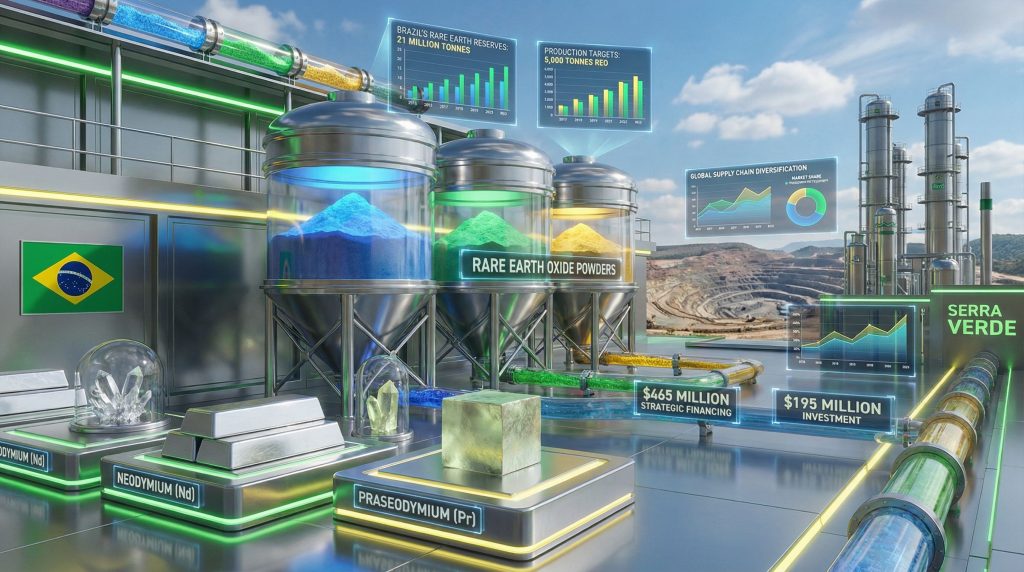

Brazil's rare earth potential stems from exceptional geological characteristics that differentiate its deposits from conventional hard rock operations. According to the US Geological Survey (USGS), Brazil holds approximately 21 million tonnes of rare earth reserves, positioning it as the world's second-largest reserve holder behind China. This positioning is particularly significant when considering the broader global mining landscape and competitive dynamics.

These deposits offer unique operational benefits through their clay-hosted mineralization, enabling extraction methods that significantly reduce environmental impact compared to traditional mining approaches. Brazilian companies emphasise that their soft, clay-hosted deposits eliminate the need for conventional drilling, blasting, or tailings dam construction, presenting a more sustainable mining practices profile.

The geological composition of Brazilian deposits contains high concentrations of strategically important heavy rare earth elements, including:

- Neodymium and praseodymium: Essential components for permanent magnet production in wind turbines and electric vehicle motors

- Terbium and dysprosium: Critical for high-performance magnetic applications requiring temperature stability

- Yttrium and europium: Vital for electronics manufacturing and renewable energy system components

This mineral composition aligns directly with Western technology sector demands, particularly as industries transition toward electrification and renewable energy systems requiring these specific rare earth elements.

When big ASX news breaks, our subscribers know first

Current Production Infrastructure and Development Pipeline

Brazil's rare earth development centres on creating integrated processing capabilities rather than focusing solely on raw material extraction. The country's flagship operation, the Serra Verde facility in Minaçu, Goiás, represents Brazil's first comprehensive rare earth mining and processing operation, targeting annual production of 5,000 tonnes of rare earth oxides.

This facility demonstrates Brazil's technical capability to advance beyond primary extraction toward value-added processing, a strategic distinction that positions the country as a potential integrated supplier rather than merely a raw material source. Furthermore, these developments align with broader industry evolution trends reshaping global resource sectors.

Brazil's Rare Earth Development Landscape

| State | Active Projects | Development Phase | Key Characteristics |

|---|---|---|---|

| Goiás | 3 projects | Production/Advanced development | Integrated processing focus |

| Bahia | 8 projects | Exploration/Development stages | Diverse deposit types |

| Minas Gerais | 7 projects | Early-stage exploration | Traditional mining region |

| São Paulo | 5 projects | Research and assessment | Technology development |

| Other regions | 4 projects | Preliminary evaluation | Regional expansion |

The development pipeline reflects a distributed approach to rare earth extraction across multiple states, reducing operational concentration risk while leveraging regional geological advantages and existing mining infrastructure.

Financial Architecture Supporting Strategic Development

Brazil's rare earth strategy relies on a combination of international partnerships and domestic financial mechanisms designed to accelerate sector development. The most significant international commitment comes from the U.S. International Development Finance Corporation, which has allocated $465 million specifically for Brazilian rare earth projects.

This financing represents strategic Western interest in diversifying rare earth supply chains away from Chinese dominance, reflecting broader geopolitical efforts to establish alternative mineral supply sources. The U.S. commitment signals long-term strategic partnership rather than short-term investment, indicating sustained support for Brazilian rare earth development. Additionally, these developments must consider the broader context of US-China trade impacts on global resource markets.

Brazil has complemented international financing with domestic allocation of $195 million specifically designated for critical mineral development initiatives, focusing on:

- Infrastructure development supporting mining operations

- Technology transfer programmes facilitating advanced processing capabilities

- Environmental compliance systems ensuring sustainable operations

- Workforce development initiatives building specialised technical expertise

Financing Structure Challenges

Brazilian rare earth companies face unique financial constraints that differentiate their capital access from traditional mining operations. Domestic lending restrictions limit access to Brazilian capital markets, while collateral limitations prevent companies from using mining rights as security for financing arrangements.

Key Financing Constraints Analysis

| Challenge Category | Market Impact | Strategic Response |

|---|---|---|

| Capital access limitations | Restricted domestic funding | International partnership development |

| Collateral restrictions | Limited security options | Alternative financing structures |

| Extended development cycles | Prolonged payback periods | Government-backed guarantee programmes |

| Commodity price volatility | Revenue uncertainty | Long-term offtake agreements |

These constraints necessitate innovative financing approaches, driving Brazilian companies toward international partnerships and alternative investment structures that can accommodate the unique characteristics of rare earth development projects.

Addressing Global Supply Chain Vulnerabilities

China currently controls over 85% of global rare earth refining capacity, creating strategic vulnerabilities for technology-dependent economies worldwide. This concentration presents significant supply security risks, particularly as rare earth elements become increasingly critical for clean energy technologies and advanced manufacturing applications.

Brazil's emergence as an alternative supplier directly addresses these concentration risks through several strategic advantages:

- Geographic diversification: Reducing dependence on single-region supply sources

- Political stability: Offering reliable partnership frameworks with democratic governance structures

- Established mining expertise: Leveraging decades of large-scale mining experience and infrastructure

- Environmental standards alignment: Meeting Western market expectations for sustainable extraction practices

Western Alliance Integration Strategy

Brazil's rare earth development aligns strategically with critical mineral security initiatives across Western nations, creating complementary policy frameworks that support integrated supply chain development. According to recent research from Science Direct, this alignment includes coordination with:

- U.S. Critical Materials Strategy focusing on domestic supply chain resilience

- European Union Critical Raw Materials Act establishing alternative supplier partnerships

- Canadian Critical Minerals Strategy emphasising North American supply security

- Australian Critical Minerals Strategy creating Pacific region cooperation frameworks

This multi-national coordination creates market opportunities for Brazilian rare earth producers while supporting Western strategic mineral security objectives.

Technical and Infrastructure Development Requirements

Brazil currently lacks sophisticated separation and purification technologies necessary for high-purity rare earth production, representing the primary technical barrier to achieving integrated supply chain capabilities. Addressing this gap requires comprehensive technology transfer initiatives and strategic partnerships with established processors.

Processing Technology Development Needs

The transition from raw material extraction to value-added processing demands significant technological advancement across multiple areas:

- Separation technology: Advanced techniques for isolating individual rare earth elements from mixed concentrates

- Purification processes: Methods for achieving commercial-grade purity levels required by end-users

- Quality control systems: Testing and verification capabilities ensuring consistent product specifications

- Environmental management: Technologies minimising processing waste and environmental impact

Infrastructure Investment Requirements

| Infrastructure Category | Current Capacity | Investment Needed | Development Timeline |

|---|---|---|---|

| Processing facilities | Limited operational capacity | $2-3 billion | 5-7 years |

| Transportation networks | Regional coverage adequate | $500 million | 3-5 years |

| Port facility expansion | Capacity constraints | $300 million | 2-4 years |

| Power infrastructure | Regional limitations | $800 million | 4-6 years |

These infrastructure requirements represent substantial capital commitments but are essential for establishing Brazil as a competitive rare earth supplier capable of serving international markets at scale.

Regulatory Framework and Environmental Considerations

Brazil's environmental regulations require comprehensive impact assessments and mitigation strategies for rare earth projects, potentially extending development timelines while ensuring sustainable operational practices. This regulatory approach aligns with international environmental standards, supporting market access to environmentally conscious Western buyers.

The permitting process optimisation represents a critical policy challenge requiring coordination between federal and state authorities. Streamlining regulatory approvals while maintaining environmental protection standards demands sophisticated regulatory framework development that balances development speed with environmental safeguards.

Environmental Advantage of Clay-Hosted Deposits

Brazilian companies emphasise the environmental advantages of their clay-hosted rare earth deposits, which enable extraction without conventional mining impacts. These deposits require minimal surface disturbance and eliminate traditional tailings storage requirements, reducing environmental footprint compared to hard rock rare earth operations.

This environmental profile provides competitive advantages in markets increasingly focused on sustainable sourcing practices, particularly as Western companies implement supply chain sustainability requirements. As highlighted by Mining Technology, this approach attracts international investors seeking responsible mining partnerships.

The next major ASX story will hit our subscribers first

Strategic Success Metrics and Timeline Projections

Brazil's rare earth strategy encompasses ambitious production targets spanning multiple development phases, each designed to incrementally establish the country as a major global supplier. The brazilian rare earth strategy framework sets clear benchmarks for measuring progress across multiple dimensions.

Short-term Development Objectives (2025-2027)

- Achieve 10,000+ tonnes annual rare earth oxide production capacity

- Establish three operational processing facilities with integrated capabilities

- Secure long-term offtake agreements with Western technology companies and governments

- Complete critical infrastructure development supporting key mining regions

Medium-term Market Penetration Goals (2027-2030)

- Capture 5-8% of global rare earth supply through scaled production operations

- Develop domestic magnet manufacturing capabilities reducing dependence on Chinese processing

- Establish Brazil as the preferred Western alternative supplier for strategic applications

- Create vertically integrated supply chains spanning extraction through finished component production

Long-term Vision Implementation (2030+)

- Achieve top-three global rare earth supplier status through continued capacity expansion

- Accomplish full value chain integration from mining operations to advanced technology components

- Establish Brazil as a regional critical mineral technology development hub

- Lead global sustainable rare earth production practices through technological innovation

Market Dynamics and Geopolitical Implications

Brazil's rare earth strategy implementation could fundamentally transform global market dynamics through increased supply diversity and reduced single-source dependencies. This transformation extends beyond simple supply addition, potentially restructuring pricing mechanisms and supply chain relationships across the entire rare earth sector.

Price Stabilisation Potential

Increased supply diversity from Brazilian production could reduce the extreme price volatility that has historically characterised rare earth markets. This stabilisation would benefit downstream manufacturers through more predictable input costs, potentially accelerating adoption of rare earth-dependent technologies across multiple industries.

Competition for Brazilian rare earth resources may accelerate technology transfer between established processors and Brazilian companies, advancing global processing capabilities while creating new centres of technical expertise outside traditional rare earth producing regions.

Strategic Balance Transformation

Brazil's emergence as a major rare earth supplier represents more than resource development, constituting a comprehensive approach to reshaping global critical mineral supply chains. This transformation could reduce strategic dependencies while creating new partnership frameworks between resource-rich developing nations and technology-dependent developed economies.

The success of Brazil's brazilian rare earth strategy may establish a model for other nations seeking to develop critical mineral sectors, potentially leading to further supply chain diversification and reduced concentration risks across multiple strategic minerals beyond rare earths. Consequently, this approach demonstrates how resource endowment can be leveraged strategically rather than simply exploited for immediate economic gain.

"Brazil's rare earth development strategy demonstrates how resource-rich nations can leverage geological advantages to establish strategic partnerships while building domestic technological capabilities, potentially reshaping global critical mineral supply chains through comprehensive value chain integration rather than simple raw material extraction."

However, the ultimate success of the brazilian rare earth strategy depends on coordinated execution across multiple stakeholder groups, sustained political commitment, and continued international partnership development throughout the extended development timeline required for establishing world-class rare earth production capabilities.

Market Analysis Disclaimer: This analysis is based on publicly available information and industry reports. Rare earth market conditions, production timelines, and investment requirements are subject to change based on technological developments, regulatory changes, and market conditions. Readers should conduct independent research and consult with qualified professionals before making investment or business decisions related to rare earth markets or Brazilian mining operations.

Could Brazilian Rare Earth Developments Signal New Investment Opportunities?

As Brazil positions itself to challenge China's dominance in critical mineral supply chains, savvy investors are recognising the potential for significant returns when major rare earth discoveries emerge on markets worldwide. Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable trading opportunities before the broader market responds. Begin your 14-day free trial today and gain the market-leading advantage needed to capitalise on the next transformative mineral discovery.