July 11, 2026

The Structural Fork in the Road: Understanding Cameroon's Hydrocarbon Inflection Point

Across the Gulf of Guinea, a quiet but consequential transformation is reshaping how hydrocarbon-producing nations think about their energy futures. The era of easy crude extraction from legacy fields is giving way to a more complex landscape defined by maturing reservoirs, infrastructure dependency, and the growing strategic weight of natural gas. Cameroon sits at the centre of this transition, and the numbers embedded in its own government planning documents tell a story that goes well beyond a single year's production forecast.

The Cameroon oil and gas activity drop and rebound narrative is not simply about one vessel leaving port. It reflects decades of compounding geological reality, fiscal structure, and the difficult arithmetic of upstream development timelines converging at the same moment.

When big ASX news breaks, our subscribers know first

What the Production Numbers Actually Reveal

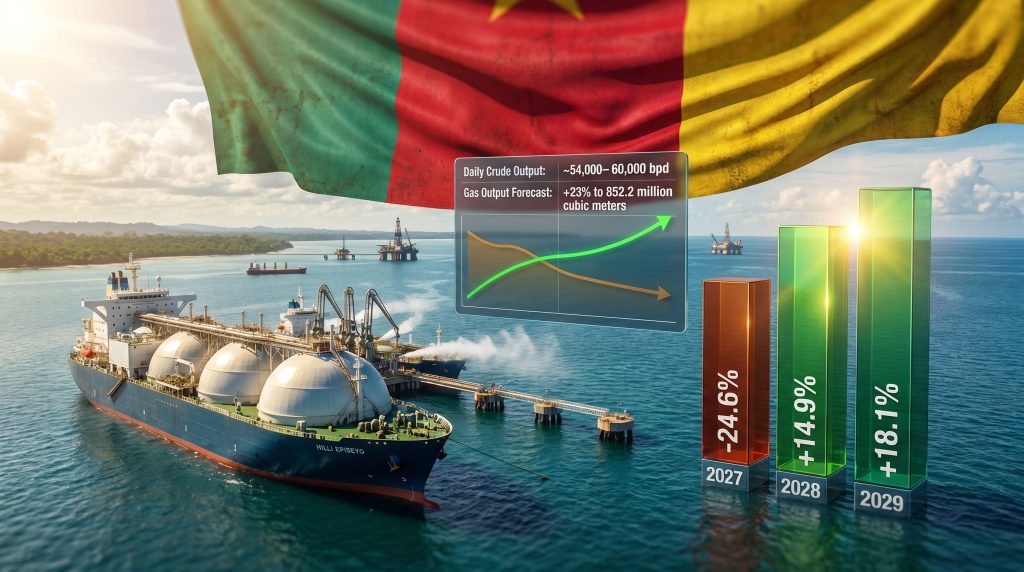

Cameroon's crude oil output has been in structural retreat for more than two decades. At its peak in the early 2000s, the country produced in the vicinity of 100,000 barrels per day (bpd). By 2024–2025, that figure had eroded to an estimated range of 54,000 to 60,000 bpd, representing a decline of roughly 40 to 46% from peak output levels.

This is not a cyclical correction triggered by oil price weakness. It is the predictable consequence of mature field depletion in the Rio del Rey Basin, where the majority of Cameroon's producing assets are concentrated. Furthermore, a critically important data point underscores just how deep this structural problem runs: Cameroon recorded a 0% oil Reserve Replacement Ratio in 2021–2022, meaning that for those years, no new reserves were being added to replace what was being extracted.

A reserve replacement ratio below 100% is a warning sign for any producer; zero represents an acute long-term production threat. For broader context on production decline and maturity assessment in the Rio del Rey Basin, academic research covering the 2012–2022 period offers a detailed picture of how this depletion has unfolded over time.

| Metric | Peak Period | 2024–2025 Estimate | Change |

|---|---|---|---|

| Daily Crude Output | ~100,000 bpd (2000s) | ~54,000–60,000 bpd | ~40–46% decline |

| Oil and Gas Revenue Forecast | Baseline | -13% in 2025 | Structural erosion |

| Projected Sector Activity | 2026 baseline | -24.6% in 2027 | Sharp contraction |

Production-sharing contract structures, which govern most of Cameroon's upstream arrangements, amplify fiscal sensitivity during output declines. As gross production falls, the government's share of lifting volumes shrinks, compressing hydrocarbon revenues at a rate that can move faster than headline output declines suggest. This dynamic has required successive adjustments to the Ministry of Finance's medium-term budget programming. Monitoring crude oil price trends remains essential for understanding how external market forces further compound these fiscal pressures.

The LNG Vessel That Changed Everything, and Its Departure

To understand why 2027 is shaping up as a particularly difficult year, the Hilli Episeyo floating liquefied natural gas (FLNG) vessel must occupy a central place in the analysis.

When the vessel arrived off the coast of Kribi in 2018, it fundamentally repositioned Cameroon's hydrocarbon identity. Before the Hilli Episeyo, Cameroon was a crude oil exporter with modest domestic gas use. After it, the country became an LNG exporter, with gas output surging by a remarkable 272% in the wake of the vessel's startup. Annual LNG production capacity grew from 1.2 million tonnes per annum (mtpa) at launch to 1.4 mtpa by 2022, following an expansion of the facility.

The partnership structure behind the venture involved Norwegian operator Golar LNG, the state-owned National Hydrocarbons Corporation (SNH), and French upstream producer Perenco, which together developed the Sanaga South and Ebome gas fields to feed the vessel. This multi-party arrangement was a template for how smaller gas-producing nations across the Gulf of Guinea could monetise offshore gas resources without the capital expenditure associated with permanent onshore liquefaction infrastructure. The LNG supply outlook for 2025 and beyond provides additional context on how global LNG dynamics are shifting simultaneously.

The 24.6% projected contraction in oil and gas activity for 2027 is not primarily a crude oil story. It is an LNG infrastructure story. The departure of the country's sole floating LNG facility removes a critical export pathway that took nearly a decade to establish, creating a structural gap that no existing asset can immediately fill.

The Hilli Episeyo's scheduled departure from Cameroonian waters in July 2026, after eight years of operation, closes that export window entirely. No replacement FLNG or onshore liquefaction facility is positioned to absorb the volumes that the vessel processed. Consequently, the result is a near-total suspension of LNG export capacity heading into 2027, which the government's own Medium-Term Economic and Budgetary Programming Document (DPEB 2027–2029) has acknowledged as the primary driver of the projected 24.6% contraction in sector activity.

Natural Gas Growth as an Interim Counterweight

Despite the looming infrastructure gap, gas production itself was projected to grow by 23% to approximately 852.2 million cubic metres in 2025. This growth was driven by development activity in the Douala-Kribi-Campo (DKC) basin, which has emerged as the strategic counterweight to the declining Rio del Rey crude base.

The distinction between infrastructure-led production growth and exploration-led reserve expansion is critical here. Cameroon's near-term gas output increases reflect development of resources that are already characterised and partially developed, not new discoveries entering the pipeline. The challenge is that without the processing and export infrastructure to monetise those volumes internationally, gas production growth becomes a partially stranded resource in the medium term.

| Basin | Primary Resource | Current Status | Strategic Role |

|---|---|---|---|

| Rio del Rey | Crude Oil | Mature, declining | Legacy production base |

| Douala-Kribi-Campo (DKC) | Natural Gas | Active development | Future growth anchor |

The geological characteristics of the DKC basin make it more amenable to gas monetisation than conventional crude extraction. The basin's offshore geology favours gas-condensate accumulations rather than the heavier crude reserves that defined the Rio del Rey Basin's productive history. This distinction shapes what type of infrastructure investment is needed and which international operators are likely to find the acreage attractive.

The 2025 Licensing Round: Signals of Investor Appetite

In August 2025, SNH launched an international call for expressions of interest covering nine exploration and production blocks across the Rio del Rey and Douala/Kribi-Campo basins. The submission deadline was set for March 30, 2026, with block awards announced on April 24, 2026. The SNH's block awards represent a meaningful step forward as the upstream investment cycle begins to gain renewed momentum.

Five of the nine blocks attracted operators willing to enter production-sharing contract negotiations:

| Block Name | Basin | Awarded Operator | Contract Type |

|---|---|---|---|

| Bolongo Exploration | Rio del Rey | Octavia Energy Corporation Limited | PSC Negotiation |

| Etinde Exploration | Douala/Kribi-Campo | Murphy West Africa Ltd. | PSC Negotiation |

| Tilapia | Douala/Kribi-Campo | Murphy West Africa Ltd. | PSC Negotiation |

| Elombo | Douala/Kribi-Campo | Murphy West Africa Ltd. | PSC Negotiation |

| Ntem | Douala/Kribi-Campo | Murphy West Africa Ltd. | PSC Negotiation |

Several structural observations emerge from this award pattern:

- Murphy West Africa's concentration in the DKC basin across four contiguous or proximate blocks signals a deliberate gas-focused strategy, potentially oriented toward building the scale needed to justify future monetisation infrastructure investment.

- Octavia Energy's entry into the Rio del Rey Basin represents a contrarian bet on residual crude potential in an acreage position that major operators have largely moved away from, suggesting the company sees value in production optimisation or near-field exploration that larger players may have overlooked.

- Four blocks going unawarded is a meaningful signal. It reflects either fiscal terms that did not satisfy operator return thresholds, geological risk perceptions that deterred interest, or both. In frontier basin contexts across Sub-Saharan Africa, partial uptake in licensing rounds is common, but the ratio of awarded to offered blocks provides a real-time read on investor appetite.

Can the 2028–2029 Rebound Be Taken at Face Value?

The government's programming document projects a 14.9% rebound in oil and gas activity in 2028, followed by 18.1% growth in 2029. These are not trivial numbers, and they carry political as well as economic weight given Cameroon's hydrocarbon revenue dependency. However, the dependency chain between block award and first production is long and contains multiple independent failure points:

- PSC negotiation completion requires agreement on fiscal terms, local content obligations, and environmental frameworks.

- Investment commitment requires operator financing, which is sensitive to global crude price levels and capital allocation priorities within international portfolios.

- Development work involves seismic acquisition, appraisal drilling, and infrastructure planning, each carrying its own timeline.

- First production is the final step, and in Sub-Saharan African upstream contexts, announced timelines routinely extend by 12 to 36 months beyond initial projections.

Three scenarios bracket the plausible range of outcomes:

Scenario A (Base Case): Newly awarded blocks complete PSC negotiations by late 2026, investment commitments are secured through 2027, and development work proceeds on schedule, enabling first production contributions by 2028. Activity rebounds 14.9% in 2028 and 18.1% in 2029.

Scenario B (Delayed Recovery): Contract negotiations extend into 2027 due to fiscal terms disagreements or financing gaps. Development timelines slip by 12 to 18 months, pushing meaningful production contributions to 2029 or beyond. The 2028 rebound is muted or absent.

Scenario C (Structural Stagnation): Block development stalls due to global oil price volatility, operator financing constraints, or regulatory friction. The 2027 contraction deepens without an offsetting production ramp, and the sector enters a prolonged low-output phase.

The honest assessment is that Scenario A requires everything in the development chain to perform on schedule. In a region where that has historically been the exception rather than the rule, both investors and fiscal planners should assign meaningful probability to Scenario B. Indeed, oil price trends in 2025 have added further uncertainty to operator investment decisions across the region.

The next major ASX story will hit our subscribers first

Cameroon's Transition in Regional Context

Cameroon's trajectory is not unique within the Gulf of Guinea. Gabon, Equatorial Guinea, and Côte d'Ivoire have each navigated versions of the same structural challenge: mature crude fields in natural decline, increasing gas resource identification, and the search for monetisation pathways that do not require the capital intensity of traditional LNG megaprojects.

The floating LNG model pioneered commercially in Cameroon through the Hilli Episeyo has become arguably the most important enabling technology for smaller gas producers in the region. The vessel's relatively modest scale and deployable nature allowed Cameroon to access LNG export markets without the multibillion-dollar commitment of a permanent onshore facility. The irony is that the same flexibility that made FLNG attractive as an entry mechanism also means the infrastructure departs when the commercial arrangement concludes, leaving a monetisation gap that fixed infrastructure would not create.

State hydrocarbons companies across the region are under increasing pressure to balance declining legacy asset revenues with the capital requirements of new development, while simultaneously managing local content obligations and fiscal contributions to national budgets. SNH's active pursuit of the 2025 licensing round reflects this tension directly.

Fiscal Pressure and the Economic Spillover of the 2027 Contraction

Hydrocarbon revenues have historically represented a significant share of Cameroon's government receipts. A 24.6% contraction in sector activity translates directly into fiscal pressure across the 2027 budget cycle, compressing the resources available for infrastructure investment, social expenditure, and debt service. Understanding the commodity price impact on revenue-dependent economies provides a useful framework for contextualising these pressures.

The knock-on effects extend beyond government accounts. Upstream activity contraction in the Kribi area will affect:

- Oilfield services providers and their local employment bases

- Logistics operators and port activity at the deep-water port of Kribi

- Local supply chains that developed around FLNG operations over the past eight years

- Downstream gas consumers dependent on associated gas volumes

Against this backdrop, the confirmation of $227 million in UK-backed financing for the Ebolowo-Akom II-Kribi road project signals that international capital continues to view the Kribi corridor as a long-term strategic asset, even as near-term hydrocarbon activity contracts. Infrastructure investment of this scale takes a multi-decade perspective on economic activity in a region, which provides some counterweight to the cyclical pessimism that a single year's sector contraction might otherwise generate.

Non-oil revenue diversification remains the structural answer to hydrocarbon revenue volatility, but building alternative tax bases and export streams takes time measured in years, not budget cycles.

Frequently Asked Questions: Cameroon Oil and Gas Activity Drop and Rebound

Why is Cameroon's oil and gas activity expected to fall 24.6% in 2027?

The projected decline reflects two converging pressures: the continued natural depletion of mature crude oil fields concentrated in the Rio del Rey Basin, and the departure of the Hilli Episeyo floating LNG vessel from Cameroonian waters in mid-2026. The vessel's exit eliminates the country's only operational LNG export facility, removing a gas monetisation pathway that contributed significantly to sector activity since 2018.

When is Cameroon's oil and gas sector expected to recover?

According to the government's DPEB 2027–2029 document, a recovery of 14.9% is projected for 2028, followed by 18.1% growth in 2029. These projections are contingent on newly awarded upstream blocks progressing from contract negotiation through to first production within that timeframe, which remains an ambitious but not impossible target.

Which companies were awarded blocks in Cameroon's 2025 licensing round?

Five blocks were awarded for production-sharing contract negotiations. Octavia Energy Corporation Limited secured the Bolongo block in the Rio del Rey Basin, while Murphy West Africa Ltd. was selected for four blocks in the Douala/Kribi-Campo Basin: Etinde Exploration, Tilapia, Elombo, and Ntem.

What was the Hilli Episeyo and why does its departure matter?

The Hilli Episeyo was a floating liquefied natural gas vessel operated off the coast of Kribi from 2018. Its arrival triggered a 272% surge in Cameroonian gas output and enabled the country to become an LNG exporter for the first time. Its departure in July 2026 after eight years of operation removes the country's sole LNG processing and export capability, directly contributing to the projected 2027 sector contraction.

Is Cameroon's crude oil production in permanent decline?

Output has fallen from approximately 100,000 bpd in the early 2000s to an estimated 54,000 to 60,000 bpd in 2024–2025. The 0% reserve replacement ratio recorded in 2021–2022 indicates that without significant new discoveries or enhanced recovery programmes in mature fields, this trajectory is structural rather than temporary. Furthermore, a broader industry analysis of resource-producing nations confirms that this pattern of mature field decline is a recurring challenge across multiple commodity sectors.

What is Cameroon's gas production outlook?

Gas production was forecast to grow 23% to approximately 852.2 million cubic metres in 2025, driven by DKC basin development. The longer-term outlook depends on new infrastructure investment to monetise volumes that the Hilli Episeyo previously processed, making the DKC basin development activity of Murphy West Africa a pivotal variable to watch.

Key Takeaways

- The 2027 contraction is a foreseeable structural event, not an unexpected shock, driven by the simultaneous effects of mature field depletion and infrastructure departure.

- The 2025 licensing round produced credible but partial results, with five of nine blocks attracting operators, signalling moderate investor appetite rather than broad enthusiasm.

- Murphy West Africa's DKC basin concentration is the most strategically significant outcome of the licensing round, with implications for Cameroon's long-term gas monetisation options.

- Recovery projections for 2028–2029 are directionally plausible but carry execution risk at every stage of the upstream development pipeline.

- Fiscal planning through 2027 must assume lower hydrocarbon revenues, requiring parallel effort to build non-oil revenue capacity and manage expenditure within tighter constraints.

- The broader regional pattern confirms that the Cameroon oil and gas activity drop and rebound cycle is consistent with trajectories observed across the Gulf of Guinea.

Disclaimer: This article contains forward-looking statements, projections, and scenario analysis based on publicly available government planning documents and industry data. These projections involve inherent uncertainty and should not be construed as investment advice. Actual outcomes may differ materially from those projected. Readers seeking additional context on Cameroon's energy sector and broader African economic developments can explore related coverage from Ecofin Agency, which provides ongoing reporting on hydrocarbon activity across Central and West Africa.

Want to Stay Ahead of Significant Mineral Discoveries Before the Broader Market Reacts?

While Cameroon's hydrocarbon sector navigates structural contraction and infrastructure gaps, the broader commodities landscape continues to generate high-impact discovery opportunities — and Discovery Alert's proprietary Discovery IQ model instantly identifies significant ASX mineral discoveries, turning complex data across more than 30 commodities into clear, actionable insights. Explore historic examples of major discoveries and their market returns, then begin your 14-day free trial to position yourself ahead of the market.