July 11, 2026

The Grid Gap at the Heart of Mexico's Energy Future

Every major energy transition in modern history has been preceded by a capital reallocation — a gradual but irreversible shift in where money flows before physical infrastructure changes. The current global energy transition and energy security challenge is no exception, and the numbers are now large enough to constitute a structural signal rather than a directional trend. Global energy investment is projected to reach US$3.42 trillion in 2026, with 58% of that capital directed toward electricity infrastructure — grids, renewables, storage, and electrification systems. Since 2022, electricity investment has consistently exceeded fossil fuel investment globally, and that margin continues to widen.

Against this backdrop, the Mexico energy strategy fossil fuels versus electrification debate is not simply a policy question. It is a capital allocation challenge with measurable consequences for industrial competitiveness, energy security, and the fiscal viability of the state itself.

When big ASX news breaks, our subscribers know first

Why Mexico's Energy Capital Is Concentrated in Hydrocarbons

The global capital reallocation toward electricity has been steep and sustained. Clean energy, grids, storage, and efficiency collectively attracted US$2.2 trillion in 2025 — roughly double the capital flowing into fossil fuels worldwide. The International Energy Agency has characterised this shift as the emergence of a new "Age of Electricity," driven by the electrification of transport, buildings, and industry, combined with surging demand from data centres and cooling systems. Global electricity demand grew an estimated 4.3% in 2024, accelerating sharply from 2.5% in 2023.

Mexico's investment posture sits in structural contrast to this global pattern. Nearly two-thirds of national energy capital remains concentrated in petroleum and PEMEX. Fossil fuel investment across Latin America fell 20% over the same period, declining to approximately US$90 billion — yet Mexico's domestic allocation continues to tilt heavily toward the hydrocarbon side of the ledger.

This divergence is not simply an ideological choice. It reflects genuine structural dependencies that are difficult to unwind rapidly:

- Liquid fuels dominate freight logistics and long-haul transport

- Gasoline and diesel demand in personal mobility remains high across the country

- A significant share of industrial activity continues to rely on hydrocarbon inputs

- PEMEX revenues underpin a substantial portion of federal public finances

- An extensive refining, storage, and distribution network requires continuous capital to maintain energy security

The more analytically precise question is not whether Mexico is "behind" the global trend — it is whether the country can simultaneously manage its hydrocarbon obligations while constructing the grid infrastructure that accelerating electrification demand will require.

What Mexico's Electricity Mix Actually Looks Like in 2025

Fossil Fuel Dominance in Power Generation

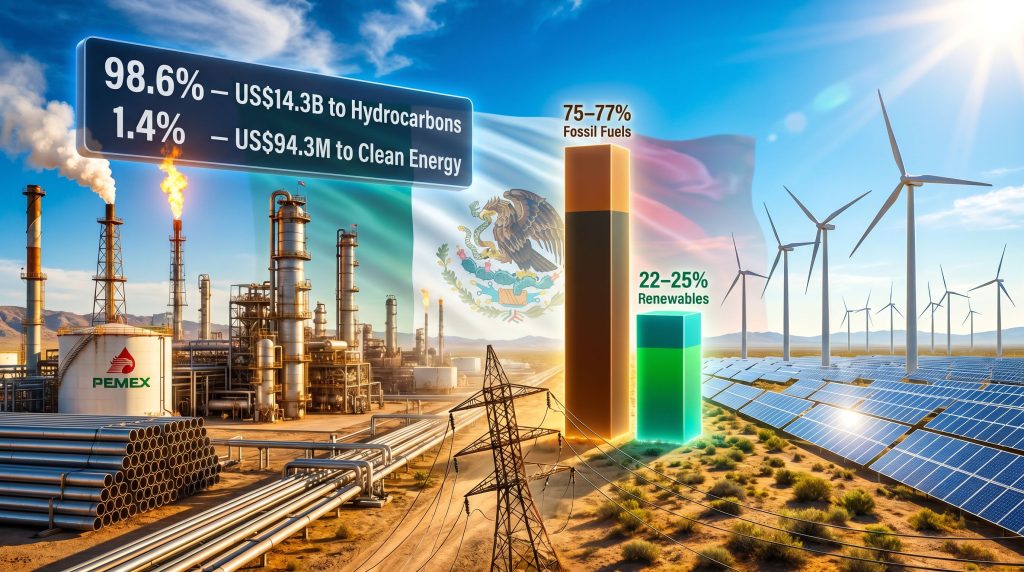

Understanding the scale of Mexico's energy transition challenge begins with an honest assessment of the current generation mix. As of 2023-2024, fossil fuels account for approximately 75%-77% of Mexico's total electricity generation. Natural gas is the dominant source, responsible for roughly 60%-62% of power output. Oil contributes approximately 9%-10% of generation, while coal accounts for 5%-8% and is gradually being phased down.

Renewables, nuclear, and efficient cogeneration combined represent only 22%-25% of the electricity mix. Wind and solar together contribute an estimated 10%-18% of generation — a share that remains well below the country's stated policy ambitions and far below the levels that would be expected from a nation with Mexico's solar irradiance and wind resource endowment. Indeed, renewables point towards Mexico's energy security as a viable long-term path, though significant deployment barriers remain.

The Capacity Gap Between Targets and Reality

| Metric | Current Level (2024) | 2030 Target | Gap |

|---|---|---|---|

| Clean energy share of generation | ~22.5% | 37.8%-45% | ~15-22 percentage points |

| Solar capacity (GW, 1.5°C compatible) | Significant shortfall | Requires ~58 GW additional | ~58 GW deficit |

| Wind capacity (GW, 1.5°C compatible) | Significant shortfall | Requires ~11 GW additional | ~11 GW deficit |

| Gas-fired generation reduction (if 45% target met) | Baseline | 20% reduction required | US$1.6B annual gas import savings |

Key Insight: Mexico's official clean energy target ranges from 36% to 45% by 2030 depending on scenario modelling. Meeting even the lower bound requires installing approximately 46 GW of new solar and wind capacity — roughly six times the deployment pace recorded in 2022.

What makes this gap particularly challenging is that it must be closed through a combination of public and private investment during a period when regulatory frameworks are simultaneously being restructured in ways that affect private sector participation.

How the Federal Budget Reveals Mexico's True Energy Priorities

Reading the Numbers Behind the Policy

Budget allocations are among the most reliable indicators of revealed government priorities — they reflect operational commitments rather than aspirational statements. The proposed 2026 Federal Expenditure Budget provides a clear quantitative picture of where Mexico's energy strategy actually sits:

- PEMEX receives US$28.2 billion in federal support

- SENER (the Ministry of Energy) sees its budget increase by 86.8%, reaching US$14.5 billion

- Of SENER's total allocation, 98.6% — equivalent to US$14.3 billion — is directed toward hydrocarbons

- Only 1.4% of SENER's budget, or US$94.3 million, is designated for clean energy development

The Structural Tension Between Ambition and Fiscal Architecture

The Sheinbaum administration has articulated a genuine renewable energy agenda. Its publicly committed targets include:

- Achieving 38% renewable electricity in the national mix by 2030

- Adding 32,000 MW of new generation capacity during the transition period

- Mobilising MX$739 billion in total energy investment

- Maintaining oil production at 1.8 million barrels per day as a fiscal bridge

The tension between these targets and the fiscal architecture that must fund them is measurable. When 98.6% of the energy ministry's budget flows to hydrocarbons and only 1.4% to clean energy, the public portion of the renewable investment programme depends heavily on either private capital mobilisation or future budget reallocation — neither of which is guaranteed by the current framework.

Furthermore, the broader clean energy transition globally demonstrates that delayed grid investment consistently produces compounding costs that outweigh short-term hydrocarbon revenue gains.

Callout: The 2030 energy strategy frames hydrocarbons and electrification as sequential rather than competing priorities. Whether this sequencing is operationally viable depends on grid infrastructure investment that the current budget does not yet adequately fund.

The 2025 Energy Reform and Its Effect on Renewable Investment

What Changed in March 2025

The March 2025 energy reform restructured Mexico's power sector in ways that have material consequences for the pace of the energy transition. The reform entrenched state-owned CFE's priority in both dispatch and investment:

- At least 54% of electricity dispatched to the national grid must originate from CFE plants

- Private producers — including renewable energy developers — are limited to a maximum 46% share of grid dispatch

- CFE's fossil gas, oil, nuclear, and hydroelectric plants are dispatched before cheaper renewable energy sources, regardless of cost efficiency or marginal economics

How Dispatch Rules Undermine the Business Case for Renewables

This dispatch priority structure is economically significant beyond its regulatory implications. It effectively subsidises higher-cost fossil generation at the expense of lower-cost renewables that are already connected and operational. The competitive dynamics established under the 2014 energy liberalisation — which had attracted substantial private renewable investment through competitive auctions — are partially reversed by this framework. According to analysis of Mexico's electricity reform, these policy reversals introduce significant long-term investment risk.

The historical regulatory trajectory illustrates a pattern of inconsistency that rational investors must price into their return assumptions:

| Legislative Milestone | Key Provision | Outcome |

|---|---|---|

| 2008 LAERFTE | Fossil fuel limits: 65% by 2024, 60% by 2035, 50% by 2050 | Targets missed; fossil fuels still >75% of generation |

| 2015 Amendment | Abolished mandatory fossil fuel limits | Removed accountability mechanism |

| 2014 Energy Reform | Liberalised power sector; enabled private renewable investment | Partially reversed by 2025 reform |

| 2025 Energy Reform | CFE dispatch priority; 54% state generation mandate | Slows renewable adoption; deters private capital |

Two-thirds of the US$30 billion in annual grid investment that the IEA's Stated Policies Scenario requires for Latin America must come from the private sector. Regulatory uncertainty directly constrains that flow. This is the critical linkage between the 2025 reform and Mexico's 2030 clean energy targets: the reform's dispatch rules make it structurally harder to attract the private capital that the public budget is not positioned to replace.

Mexico's Transmission and Distribution Crisis

The Grid Investment Gap Is Already Producing Failures

Globally, electrical grid investment grew from US$314 billion in 2015 to more than US$540 billion in 2026 — a 72% increase driven by the need to transport and manage increasingly complex, decentralised energy mixes. Battery storage capital deployment multiplied more than a hundredfold over the same decade. Global oil investment, by contrast, fell approximately 35% between 2015 and 2026.

Mexico has not matched this grid investment trajectory, and the consequences are now visible in operational failures. SENER Undersecretary Jorge Islas Samperio acknowledged at the ITA-LAC 2026 forum on July 8, 2026, that Mexico's recent power disruptions are not generation problems but transmission and distribution network failures. This distinction is operationally critical: it confirms that the investment imbalance between fuel-side capital and grid-side capital is already producing measurable service degradation, not merely future risk.

Power interruptions have affected at least 20 Mexican states during the 2026 summer demand season — a direct consequence of transmission constraints under elevated load conditions.

Three Demand Pressures Converging on a Constrained Grid

What makes Mexico's grid vulnerability particularly acute is the convergence of three structural demand drivers that are intensifying simultaneously:

- Nearshoring industrial expansion — manufacturing relocations from Asia are adding significant new industrial electricity loads, particularly in northern and central states where transmission constraints are most acute

- Data centre growth — digital infrastructure investment is accelerating power consumption across commercial and industrial categories, with energy-intensive AI computing infrastructure representing a new and rapidly growing load class

- Electric vehicle adoption — EV penetration remains early-stage but introduces distributed load patterns that require grid modernisation to manage effectively without creating localised stress points

Annual grid investment across Latin America must double to US$30 billion under the IEA's Stated Policies Scenario to support the region's electrification trajectory. Mexico's current investment posture falls short of this benchmark at precisely the moment demand pressures are accelerating.

The next major ASX story will hit our subscribers first

The Sequential Transition Model: Viable Strategy or Structural Risk?

How the Sheinbaum Framework Is Constructed

The current administration's energy approach explicitly positions fossil fuels and electrification as complementary phases rather than binary alternatives. Oil production targets are maintained at 1.8 million barrels per day through the transition period, with fuel import reduction pursued in parallel with renewable generation expansion. Hydrocarbons are framed as a fiscal bridge — generating the revenues that fund the public portion of the renewable transition rather than an asset class to be rapidly wound down.

This framing has genuine economic logic. PEMEX revenues continue to underpin a significant share of federal public finances. An abrupt withdrawal from hydrocarbon investment would create a fiscal gap that renewable revenues could not fill on any near-term timeline.

Where the Sequential Model Faces Its Stress Test

The sequential model carries an embedded assumption that deserves scrutiny: it assumes that PEMEX revenues can fund grid and renewable investment at the required pace while PEMEX itself is experiencing a structurally declining production trajectory. The fiscal bridge is narrowing at precisely the moment grid investment requirements are growing.

Scenario Framing: If PEMEX production declines faster than renewable capacity is installed, Mexico risks a fiscal-energy double bind — reduced hydrocarbon revenues coinciding with unmet electricity demand growth. The grid investment gap is the critical variable that determines whether the sequential transition model remains viable or produces a prolonged period of energy insecurity.

Three conditions must hold simultaneously for the sequential model to succeed:

- Grid investment must accelerate materially — transmission and distribution spending must scale toward the IEA's US$30 billion annual regional benchmark, with private capital mobilised through stable regulatory frameworks

- PEMEX fiscal contributions must remain sufficient to fund the public portion of renewable and grid investment through the transition window, despite declining production

- Renewable deployment must achieve approximately six times the 2022 pace to meet the 45% clean energy target, requiring policy certainty and dispatch rules that do not systematically disadvantage renewables

A Less Discussed Dynamic: Mexico's Resource Potential and the Private Capital Question

What Mexico's Solar and Wind Endowment Actually Represents

One analytically underweighted dimension of the Mexico energy strategy fossil fuels versus electrification debate is the scale of Mexico's untapped renewable resource potential. The country possesses some of the highest solar irradiance levels in the western hemisphere, concentrated in the northern states of Sonora, Chihuahua, and Baja California. Wind resources in the Isthmus of Tehuantepec are among the most competitive in Latin America on a cost-per-megawatt-hour basis.

This resource endowment means the constraint on Mexico's renewable deployment is not physical availability but a combination of regulatory uncertainty, grid connection bottlenecks, and dispatch rules that reduce the bankability of new projects. International renewable developers and infrastructure investors understand this dynamic well — Mexico's resource quality is not in question, but the investment framework that governs returns is.

The nearshoring industrial expansion, often framed purely as a demand challenge for the grid, also represents a potential catalyst for renewable energy solutions at scale. Energy-intensive manufacturers relocating from Asia frequently require renewable power purchase agreements as part of their sustainability commitments. This creates a commercial pull for renewable development that operates somewhat independently of the regulatory dispatch framework — large industrial offtakers can negotiate bilateral contracts that provide the revenue certainty project financing requires.

Whether this commercial dynamic can generate renewable investment at a pace sufficient to compensate for the dispatch disadvantage created by the 2025 reform is one of the more consequential open questions in Mexico's energy sector. Moreover, the shifting geopolitical landscape in mining adds further complexity, as critical minerals demand for battery storage and grid components intensifies globally and Mexico's positioning within that supply chain remains underdeveloped.

Frequently Asked Questions: Mexico Energy Strategy

What percentage of Mexico's electricity comes from fossil fuels?

As of 2023-2024, fossil fuels generate approximately 75%-77% of Mexico's electricity, with natural gas alone accounting for 60%-62% of total power output. Renewables, nuclear, and cogeneration collectively represent only 22%-25% of the generation mix.

What is Mexico's renewable energy target for 2030?

The Sheinbaum administration has set a target of 45% clean electricity generation by 2030, though official planning scenarios range from 36% to 45%. The government's operational benchmark is 37.8% clean energy by 2030, up from approximately 22.5% in 2024.

How much does Mexico spend on fossil fuels versus clean energy in its federal budget?

In the proposed 2026 Federal Expenditure Budget, SENER allocates 98.6% of its US$14.5 billion budget to hydrocarbons — equivalent to US$14.3 billion — while only 1.4% (US$94.3 million) is directed toward clean energy. PEMEX receives an additional US$28.2 billion in federal support.

Why is Mexico's electrical grid struggling with outages?

Mexico's power disruptions are primarily transmission and distribution failures, not generation shortfalls. Underinvestment in grid infrastructure, combined with rising demand from industrial nearshoring and summer peak loads, has produced outages across at least 20 states during the 2026 summer season.

How does the 2025 energy reform affect renewable investment in Mexico?

The March 2025 reform mandates that CFE supplies at least 54% of grid electricity, with CFE's fossil-fuel plants dispatched before cheaper renewable sources. This dispatch priority structure undermines renewable competitiveness and creates regulatory uncertainty that deters the private investment required to fund Mexico's 2030 renewable targets.

What is Mexico's oil production target under the current energy strategy?

The current Mexico energy strategy fossil fuels versus electrification framework maintains oil production at 1.8 million barrels per day while simultaneously pursuing renewable expansion, treating hydrocarbons as a fiscal and energy security bridge through the transition period.

This article contains forward-looking analysis based on publicly available investment data, IEA projections, and official Mexican government budget documents. Energy transition timelines and investment forecasts involve significant uncertainty. Readers should not interpret any portion of this analysis as financial or investment advice.

Want to Track the Critical Minerals Powering Mexico's Energy Transition?

As Mexico's grid infrastructure gap widens and global demand for battery storage, solar, and transmission components accelerates, the race to secure the critical minerals underpinning this transition is intensifying — and Discovery Alert's proprietary Discovery IQ model delivers real-time ASX alerts the moment significant mineral discoveries are announced, turning complex data into actionable opportunities. Explore historic discoveries and their returns to see what early positioning can mean, then begin your 14-day free trial at Discovery Alert to stay ahead of the market.