June 24, 2026

When Government Fiscal Policy Becomes a Balance Sheet Tool

The global mining industry has long operated on a simple financial logic: raise equity, secure commodity-linked debt, and hope that metal prices cooperate long enough to justify the capital deployed. That model is under structural strain. Rising interest rates, ESG-driven investor scrutiny, and the sheer scale of capital required to build next-generation critical mineral projects have exposed the limitations of traditional mine finance. Something had to give.

What is emerging in its place is a more sophisticated architecture, one where government-mandated fiscal incentives are not treated as a welcome afterthought but as foundational components of a project's capital stack. Canada's investment tax credit framework, designed specifically to accelerate domestic critical mineral development, is now being operationalised at a scale that could fundamentally reshape how large mining projects are financed across the G7.

The Canada Nickel US$600M tax credit facility, structured around the Crawford Nickel Sulphide Project in Ontario, is the clearest expression of this shift yet.

When big ASX news breaks, our subscribers know first

Understanding the Mechanics of Tax Credit Bridge Financing

Before examining Crawford specifically, it is worth understanding precisely how investment tax credit (ITC) monetisation functions as a project finance instrument, because the mechanics are counterintuitive to those accustomed to traditional mining finance.

Unlike a grant, which transfers capital to a project developer upfront, an ITC is a fiscal entitlement that materialises only after qualifying capital expenditure has been incurred. This creates a structural timing gap: the developer must spend first and receive the credit later, often well into or after the construction phase.

A tax credit bridge facility resolves this mismatch. The developer borrows against the anticipated ITC entitlement during construction, using the future credit as effective security for the debt. Once the credits are formally recognised and monetised post-commissioning, the facility is repaid. The result is that future government fiscal support is converted into present-day construction capital.

A tax credit facility does not create new government spending; it accelerates the economic benefit of an existing fiscal commitment, compressing the timeline between policy intent and real-world capital deployment at the project level.

This distinction matters enormously for project economics. The difference between receiving US$600 million at commissioning versus receiving it during construction could represent hundreds of millions of dollars in avoided equity dilution and reduced financing costs. Furthermore, Canada Nickel has secured an exclusive mandate for this facility, underscoring the seriousness of the arrangement.

Crawford's Resource Base and Why Scale Unlocks Credit Eligibility

The Crawford Nickel Sulphide Project sits within the Timmins Nickel District of Ontario, a region with a well-established mining infrastructure base and a regulatory environment that is among the most understood in North America. Crawford's resource base stands at 10.13 million tonnes of measured and indicated nickel, placing it among the largest nickel sulphide deposits on the continent.

The sulphide classification is technically important and often underappreciated by generalist investors. Nickel sulphide deposits differ fundamentally from the laterite and mixed hydroxide precipitate (MHP) pathways that dominate Indonesian production:

- Sulphide ores are amenable to conventional flotation processing, which is far less energy-intensive than high-pressure acid leach (HPAL) used for laterite nickel

- Sulphide concentrates typically carry higher grades of payable nickel and produce fewer problematic by-products

- The carbon intensity of sulphide processing is substantially lower, a distinction that is becoming commercially decisive under emerging regulatory frameworks

- Sulphide deposits also tend to produce cobalt and platinum group elements as co-products, improving overall project economics and revenue diversification

This geological foundation is what makes Crawford's ESG credentials credible rather than aspirational. The low-carbon production profile is not engineered onto an inherently dirty process; it is an organic outcome of the deposit's mineralogy, amplified by the carbon capture infrastructure being built around it.

The Three Carbon Pathways That Unlock US$600M in Tax Credits

Canada Nickel's access to the Canada Nickel US$600M tax credit facility is contingent on Crawford's verified carbon sequestration capabilities. The project has identified three distinct pathways for permanent carbon mineralisation, and it is this multi-pathway approach that distinguishes Crawford from other projects seeking CCUS tax credit eligibility.

The most technically differentiated of these is IPT Carbonation Technology, a proprietary mineralisation process that converts injected carbon dioxide into stable carbonate rock within approximately six months. Unlike conventional carbon capture approaches that store CO₂ in geological formations under pressure, IPT Carbonation permanently locks carbon into solid mineral form, effectively eliminating the long-term leakage risk that complicates the verification of other CCUS methodologies.

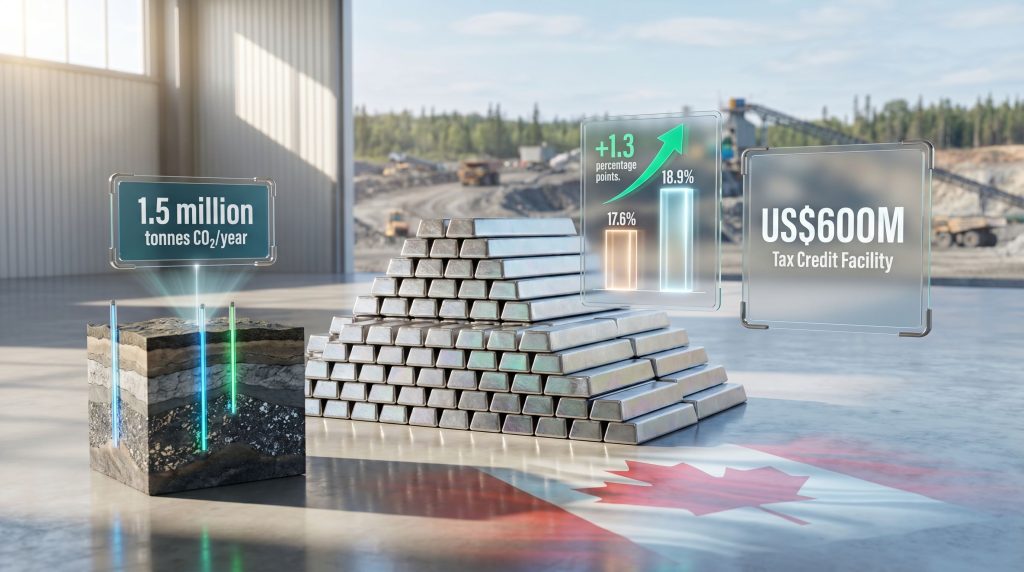

At Crawford's projected operating scale, the combined carbon sequestration capacity across all three pathways is estimated at up to 1.5 million tonnes of CO₂ per year. This figure does not merely offset the project's operational emissions; it positions Crawford as a potentially net-negative carbon nickel producer, a distinction that has direct commercial implications in offtake negotiations with battery manufacturers operating under Scope 3 emissions mandates.

Tax Credit Entitlement Breakdown

| Tax Credit Category | Estimated Value | Coverage Basis |

|---|---|---|

| CCUS Investment Tax Credit | ~US$300 million | 50% of eligible CCUS capital expenditures |

| Clean Technology Manufacturing Credit | ~US$300 million | Qualifying processing and refining expenditures |

| Total Combined Entitlement | US$600 million | Across both federal credit categories |

Canada's CCUS Investment Tax Credit applies at a rate of 50% of eligible capital expenditure for qualifying projects commissioned before 2030. The Clean Technology Manufacturing Credit targets the downstream processing stages, incentivising domestic value-add over raw ore export. Together, these instruments form the legislative foundation of the US$600M facility.

SB1 Markets and the Nordic Capital Dimension

The appointment of SB1 Markets AS as exclusive debt arranger carries significance beyond the transaction itself. SB1 Markets is a Nordic investment bank with operations anchored in Norway and Sweden, with deep expertise in structured debt for natural resource projects, an expertise shaped by decades of financing North Sea energy infrastructure under complex government fiscal frameworks.

The entry of Nordic capital into Canadian critical mineral development reflects a broader trend: international institutional investors with long experience in resource-sector structured finance are beginning to view Canadian critical mineral projects as a compelling risk-adjusted opportunity, particularly where government fiscal architecture reduces first-loss exposure.

The facility arrangement is targeted for completion by end of 2026, ahead of a Final Investment Decision planned for 2027, with construction commencement anticipated in late 2026 or early 2027 and first nickel production targeted for late 2028.

Structural Impact on Project Equity Requirements

The most immediate financial consequence of the facility is its effect on equity capital requirements. According to Canada Nickel's project economics, the US$600M bridge facility is designed to cover more than half of the equity capital required to construct Crawford. In practical terms:

- The equity raise required from the market is substantially reduced

- Dilution risk for existing shareholders is compressed

- The project's attractiveness to debt providers improves as the equity buffer becomes more credible

- Lenders can underwrite with greater confidence knowing a significant portion of the capital structure is backed by anticipated government fiscal entitlements rather than commodity price assumptions

When a project's capital structure incorporates a verified government fiscal entitlement at this scale, it fundamentally changes the risk calculus for every other financing participant in the stack.

IRR Scenarios: With and Without Tax Credit Inclusion

| Scenario | After-Tax IRR |

|---|---|

| Base Case (excluding ITC monetisation) | 17.6% |

| Enhanced Case (including full ITC inclusion) | 18.9% |

| IRR improvement from facility | +1.3 percentage points |

While 1.3 percentage points may appear modest in isolation, the compounding effect on net present value at Crawford's capital scale is material. For institutional investors evaluating the project on a risk-adjusted return basis, the ITC structure removes a category of uncertainty entirely, which is often worth more than the raw IRR improvement suggests. A completed definitive feasibility study underpins these return projections, providing lenders with a rigorous technical foundation.

The 2030 Commissioning Deadline and Its Strategic Implications

One of the most consequential and least discussed features of Canada's CCUS Investment Tax Credit is its built-in sunset clause. To qualify, projects must be commissioned before 2030. This legislative deadline creates a structural urgency that is already reshaping development timelines across the Canadian critical minerals sector.

For Crawford specifically, the timeline is tight but executable. A construction decision by end of 2026, FID in 2027, and first production in late 2028 would place commissioning comfortably within the eligibility window. However, the margin for delay is narrow, and this constraint will likely concentrate capital and regulatory attention on the small number of Canadian critical mineral projects that are genuinely close to production-ready status.

For the broader sector, the 2030 deadline functions as a competitive filter. Projects that cannot demonstrate construction-readiness within the next 12 to 24 months may find themselves locked out of the most generous ITC framework Canada has ever deployed for mining. Consequently, this dynamic is likely to accelerate mining sector consolidation and financing activity across the sector through 2026 and 2027.

The next major ASX story will hit our subscribers first

Western Battery Supply Chain Demand and Crawford's Positioning

The commercial case for Crawford extends well beyond its domestic financing structure. Indonesia currently accounts for approximately half of global nickel production, with the vast majority of that output processed through HPAL technology into intermediate products such as MHP and nickel matte. This processing pathway, while cost-competitive, carries a significantly higher carbon footprint than sulphide-based production and raises tailings management concerns that are increasingly scrutinised by ESG-focused capital allocators.

Western battery manufacturers and electric vehicle producers face a compounding regulatory challenge. In this context, critical minerals and energy security have become inseparable concerns for policymakers and investors alike:

- The EU Battery Regulation requires battery producers to disclose and progressively reduce the carbon footprint of battery-grade materials, with maximum lifecycle thresholds expected to tighten through the 2030s

- The US Inflation Reduction Act domestic content requirements incentivise the use of critical minerals sourced from free-trade agreement partners, of which Canada is the most strategically proximate

- Institutional investors across Europe and North America are applying Scope 3 emissions screening to supply chain inputs, creating indirect pressure on battery manufacturers to source from lower-carbon origins

Crawford's combination of sulphide mineralogy, verified carbon sequestration, Canadian jurisdiction, and scale positions it as one of a very small number of projects globally capable of meeting all three of these converging requirements simultaneously. The growing critical minerals demand from the energy transition only strengthens this positioning.

If Crawford achieves first production in late 2028 as targeted, it would enter the market during a period when IRA-compliant and EU Battery Regulation-compliant nickel from non-Indonesian sources is expected to be in acute short supply. The timing alignment between project delivery and regulatory-driven demand represents a structural commercial advantage that is independent of spot nickel price movements.

Key Risks and Execution Milestones

Critical Path to Financial Close

| Milestone | Target Timeline | Risk Assessment |

|---|---|---|

| Tax credit facility arrangement | End of 2026 | Medium |

| Final Investment Decision | 2027 | Medium-High |

| Construction commencement | Late 2026 / Early 2027 | Medium |

| First nickel production | Late 2028 | Medium |

| Full ITC monetisation | Post-commissioning | Low-Medium |

Principal Risk Dimensions

Policy continuity risk is the most systemic. The 2030 commissioning deadline is legislated but not immutable; changes to federal fiscal policy could alter credit rates or eligibility criteria. Developers relying on ITC monetisation at scale should monitor federal budget cycles closely through 2027.

Carbon verification risk is technically nuanced. The full US$600M entitlement is contingent on verified carbon capture performance across Crawford's three sequestration pathways. If actual CO₂ sequestration metrics fall short of projections, the monetisable credit quantum is reduced, which would require compensating adjustments elsewhere in the capital structure.

Debt market conditions represent an exogenous risk. SB1 Markets must arrange the facility in a lending environment that remains receptive to resource-sector structured credit. Rising credit spreads or a generalised retreat from natural resource exposure by Nordic institutional capital could affect facility economics and timeline.

Commodity price sensitivity remains relevant even within a policy-backed capital structure. A sustained downturn in nickel prices does not affect ITC entitlement directly, but it does affect lender appetite for the broader project debt package and could influence the terms on which the facility is ultimately arranged.

Comparative Policy Landscape: Where Canada Stands Globally

| Jurisdiction | Primary Incentive Mechanism | CCUS Credit Rate | Export Credit Support |

|---|---|---|---|

| Canada | ITC + Clean Tech Manufacturing Credit | 50% of eligible capex | Available |

| United States | Inflation Reduction Act credits | 30-50% (project-dependent) | Available (EXIM Bank) |

| Australia | Critical Minerals Production Tax Incentive | 10% of processing costs | Available |

| Indonesia | Tax holidays | Variable, no CCUS-specific credit | Limited |

Canada's 50% CCUS credit rate is among the most generous of any G7 jurisdiction for qualifying mining projects. Combined with the Clean Technology Manufacturing Credit and export credit agency support mechanisms, the layered fiscal architecture available in Canada creates a financing environment that is structurally difficult for competing jurisdictions to replicate in the near term.

A Template for the Sector, or a Unique Advantage?

The structural innovation at Crawford, converting anticipated ITC entitlements into deployable construction capital through a formally mandated debt facility, is not inherently project-specific. Any Canadian mining developer with qualifying CCUS or Clean Technology Manufacturing expenditures could theoretically pursue a similar approach within the existing legislative framework.

However, several features of Crawford make it an unusually strong candidate for this model:

- The sheer scale of the resource base generates a credit entitlement large enough to justify the complexity and cost of arranging a dedicated facility

- The three-pathway carbon sequestration approach provides verification redundancy that single-pathway projects cannot offer

- The Timmins jurisdiction carries regulatory familiarity and permitting precedent that reduces timeline risk for lenders

- The project's proximity to existing Ontario infrastructure reduces capital expenditure on ancillary logistics

In addition, direct extraction technologies are reshaping how the broader critical minerals sector approaches processing efficiency, offering further context for why innovative technical approaches like IPT Carbonation attract institutional interest.

Whether the Crawford model is replicated across the Canadian sector will depend significantly on whether SB1 Markets successfully arranges the facility on acceptable terms ahead of FID in 2027. A successful close would serve as a proof-of-concept that is likely to attract imitators across the critical minerals development pipeline. Analysts following Canada Nickel's long-term positioning note that the company's strategy is deliberately calibrated to capture this first-mover structural advantage.

Frequently Asked Questions

What exactly is the Canada Nickel US$600M tax credit facility?

It is a structured debt arrangement, exclusively mandated through SB1 Markets AS, that allows Canada Nickel to borrow against anticipated Canadian government investment tax credits during the construction phase of the Crawford project. The two credit categories involved are the CCUS Investment Tax Credit and the Clean Technology Manufacturing Credit, with the facility repaid once those credits are formally monetised post-commissioning.

How does IPT Carbonation Technology differ from conventional carbon capture?

Conventional geological carbon storage maintains CO₂ in a pressurised fluid or gas state within underground formations, carrying a long-term risk of leakage. IPT Carbonation converts CO₂ into solid carbonate minerals within approximately six months of injection, permanently locking carbon into rock form. This eliminates leakage risk and provides a more verifiable basis for carbon credit certification.

Why does the sulphide classification matter for Crawford's commercial positioning?

Nickel sulphide deposits produce concentrates that can be processed through conventional pyrometallurgical and hydrometallurgical routes at significantly lower carbon intensity than HPAL processing of laterite nickel. As Western battery manufacturers face tightening Scope 3 emissions requirements, the carbon intensity differential between sulphide and laterite nickel sources is becoming a commercially material factor in offtake pricing and supplier selection.

What happens if the 2030 commissioning deadline is missed?

Projects commissioned after 2030 would not qualify under the current CCUS ITC legislative framework. This could eliminate up to US$300 million of the anticipated credit entitlement, fundamentally altering Crawford's capital structure and IRR profile. The 2030 deadline is the single most consequential external constraint on Crawford's project timeline.

Disclaimer: This article is intended for informational purposes only and does not constitute financial or investment advice. Forward-looking statements regarding project timelines, tax credit entitlements, and production targets involve assumptions and uncertainties. Readers should conduct independent due diligence before making any investment decisions.

Want to Know Which ASX Mineral Discoveries Could Deliver Outsized Returns?

Discovery Alert's proprietary Discovery IQ model instantly identifies significant ASX mineral discoveries and translates complex data into actionable investment insights — the same kind of structural opportunity that major finds have historically delivered to early movers. Explore Discovery Alert's dedicated discoveries page to see historic examples of exceptional outcomes, and start your 14-day free trial to position yourself ahead of the broader market.