June 11, 2026

The Perfect Storm Facing Australian Investors in 2025

Few investment environments in modern Australian history have combined as many simultaneous headwinds as the one taking shape right now. Rising borrowing costs, structurally elevated energy prices, fiscal expansion, and a sweeping overhaul of capital gains tax treatment are converging into conditions that fundamentally alter the calculus for retail and institutional investors alike.

Layer on top of that a rapidly shifting political landscape, state-level uranium policy in flux, and a global energy security shock that the head of the International Energy Agency has described as larger than both 1970s oil crises combined, and the picture becomes genuinely complex to navigate.

Understanding how Australia's capital gains tax changes and uranium mining ban policies intersect with these macro forces is now essential for anyone with exposure to ASX-listed resource companies, property, or long-term equity portfolios. Furthermore, the broader Australia critical minerals outlook plays a crucial role in contextualising why these policy decisions carry such significant long-term weight.

When big ASX news breaks, our subscribers know first

Australia's Interest Rate Divergence and Its Investor Psychology Impact

While much of the developed world has pivoted toward monetary easing, Australia remains locked in a tightening cycle. This divergence is not merely a technicality. It compounds the cost of capital across every asset class, suppresses discretionary investment capacity among retail participants, and creates a headwind that sits entirely outside the control of individual investors or companies.

The psychological effect on public market participation is already measurable. With the June 30 financial year-end approaching, tax-loss selling has become more elevated than in previous cycles. Investors are openly questioning the logic of holding equity positions when the government's proposed changes could double their effective tax burden on any gains realised.

The combination of higher rates, elevated energy costs, and an increasing tax burden on investment returns represents one of the most challenging environments for Australian investors in over two decades. That is not hyperbole — it is an arithmetic reality that fund managers, retail investors, and company boards are all being forced to reckon with simultaneously.

What Are Australia's Proposed Capital Gains Tax Changes?

From the 50% Discount to Inflation Indexation

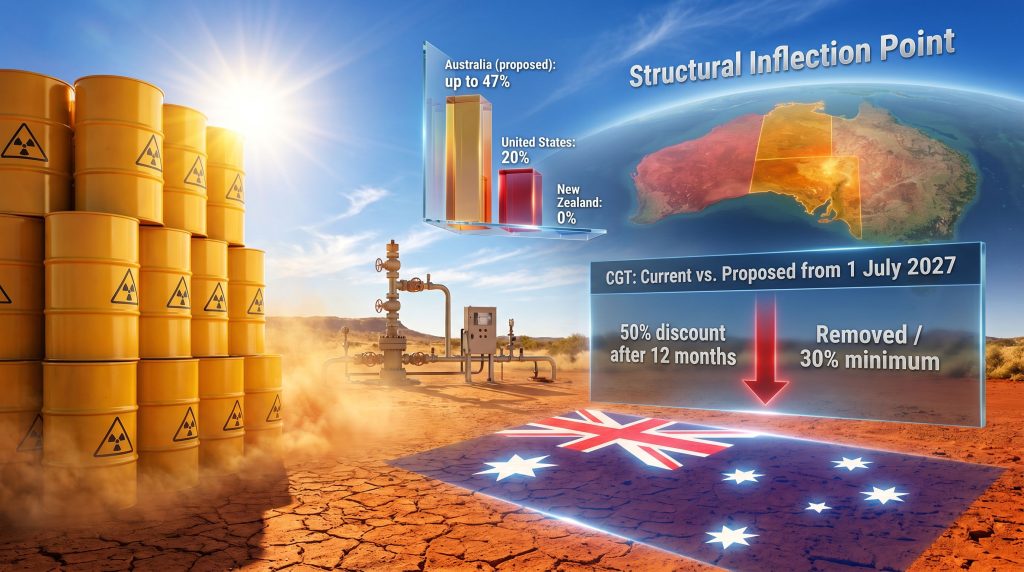

The centrepiece of the proposed tax reform is the removal of the 50% capital gains tax discount that has applied to assets held for more than 12 months. Under the existing framework, an investor on the top marginal rate of 47% effectively paid approximately 23.5% in CGT after the discount, which represented a reasonable risk-adjusted return incentive for long-term investors willing to commit capital over multi-year timeframes.

The proposed replacement mechanism is inflation indexation of the cost base, meaning investors would only be taxed on the real gain above inflation rather than the nominal gain. In theory this sounds equitable. In practice, for most historical holding periods and inflation scenarios, the 50% discount delivered substantially greater relief than indexation would. In low-inflation environments, the difference is particularly stark.

According to government tax analysis, the reforms represent one of the most significant structural changes to Australia's investment tax landscape in decades.

| Feature | Current System | Proposed System (from 1 July 2027) |

|---|---|---|

| Long-term CGT discount | 50% after 12 months | Removed |

| Cost base treatment | Fixed purchase price | Indexed to inflation |

| Minimum effective tax rate | None specified | 30% minimum floor |

| Entities affected | Individuals, trusts, partnerships | Individuals, trusts, partnerships |

| Asset classes covered | Property, shares, business assets | Property, shares, ETFs, crypto, managed funds, business assets |

The proposed 30% minimum effective tax rate applies regardless of holding period, structuring approach, or entity type, setting an absolute floor on the tax treatment of investment gains. Trusts and family investment vehicles that historically distributed gains to lower-income beneficiaries to reduce the effective rate face structural limitations under this new regime.

The Real-World Maths for Long-Term Investors

Consider a hypothetical investor who purchased $100,000 in ASX-listed shares in 2015 and sells in 2027 for $220,000. Under the current 50% discount, their taxable gain at the top marginal rate would be calculated on $60,000, producing a tax liability of approximately $28,200.

Under the proposed indexation model with a 30% minimum floor, the outcome depends heavily on the inflation adjustment applied. However, in a moderate inflation environment, the tax liability increases materially. For investors in the top marginal bracket, the effective rate nearly doubles.

This is not a subtle shift. It is a structural repricing of the after-tax return available from long-term equity investment in Australia.

Business Sales, Startups, and the Silent Partner Problem

The proposed changes extend beyond listed equities to cover business asset sales, meaning founders and entrepreneurs face a CGT rate of up to 47% on exit proceeds above the inflation-adjusted cost base. The technology startup community has mounted a highly visible public campaign around this point.

Social media content has illustrated the concept of the government effectively becoming a near-equal silent partner in any successful venture — contributing nothing to the sweat equity and capital risk while claiming nearly half the upside. The minerals exploration sector is lobbying for carve-outs similar to those likely to be granted to technology startups.

The sector argues that the risk profile of exploration investment, where capital is committed years or decades before any potential realisation event, makes the removal of the 50% discount particularly punitive. Whether those carve-outs will be granted remains uncertain. Consequently, junior explorers funding has emerged as a central concern for smaller ASX-listed resource companies facing these structural headwinds.

How Does Australia Compare Internationally?

The proposed changes place Australia at the high end of capital gains tax burden among comparable developed nations, with meaningful implications for capital allocation decisions at both the individual and institutional level.

| Country | Effective Long-Term CGT Rate | Key Structure |

|---|---|---|

| Australia (proposed) | Up to 47% (30% minimum floor) | Indexation replaces 50% discount |

| United States | ~20% (federal, long-term) | Preferential rate for assets held over 12 months |

| United Kingdom | 24% (property), 18% (other) | Tiered by asset class |

| New Zealand | 0% | No general capital gains tax |

| Canada | ~26.7% | 50% inclusion rate model |

| Denmark | ~42% | High-tax comparable |

New Zealand's finance ministry has been notably direct in positioning the country as a destination for Australian investors, entrepreneurs, and technology founders seeking a lower-tax environment. The risk of capital flight among high-net-worth individuals is a concern that critics argue has been underweighted in the government's budget modelling.

The Political Economy Behind the Reforms

Demographic Targeting and the Voting Bloc Strategy

Australia's baby boomer cohort has declined as a share of the electoral base. Younger voters and recent immigrants now represent a growing and increasingly decisive voting bloc. The Labor government's dual reform agenda targeting both CGT and negative gearing on established residential properties is explicitly designed to reduce asset prices and improve housing affordability for first-time buyers.

Negative gearing restrictions will apply to new residential property investments from 1 July 2027, with existing arrangements grandfathered. This provision protects established investors while removing the same wealth-building pathway for those entering the market after the cut-off date. The political optics of senior government figures having historically benefited from negative gearing while legislating its removal for future investors has generated sustained public backlash.

One Nation's Electoral Surge and Its Policy Implications

One Nation is now polling as the most popular party in Australia on a primary vote basis — a development that would have seemed implausible a decade ago. Critically, its growth is drawing not only from traditional conservative voters moving further right, but also from disaffected Labor supporters frustrated with high-tax, ideologically-driven economic policies.

This fragmented preference environment makes modelling two-party preferred outcomes extremely difficult. The preferential vote flows are no longer predictable, which introduces genuine policy uncertainty for long-horizon sectors like uranium mining where regulatory settings are determined by electoral outcomes.

One Nation explicitly supports lifting uranium mining bans and enabling domestic nuclear energy. If the party's electoral momentum continues through upcoming state elections and by-elections, these positions could shift from fringe advocacy to mainstream policy consideration faster than most market participants currently anticipate.

Australia's Uranium Mining Ban: A State-by-State Reality Check

Where Uranium Can and Cannot Be Mined

| Jurisdiction | Status | Key Details |

|---|---|---|

| South Australia | Permitted | Active ISR operations including Honeymoon and Four Mile |

| Northern Territory | Permitted | Added uranium to its own critical minerals list |

| Western Australia | Banned (since 2017) | Government exploration grants issued; ban under political pressure |

| New South Wales | Exploration only | Upper house bill passed to remove ban; lower house outcome uncertain |

| Queensland | Exploration only | Ban remains; electoral dynamics shifting |

The Northern Territory's Critical Minerals Move

The NT's decision to formally add uranium to its own critical minerals list directly contradicts the federal government's ongoing refusal to include uranium in the national critical minerals framework. This jurisdictional divergence reflects a broader tension between state-level economic development priorities and federal energy ideology.

The federal government's silence on uranium is at least partly strategic, as policymakers are anxious to prevent the uranium mining debate from becoming conflated with the politically sensitive question of domestic nuclear power generation. The United States recently added uranium to its national critical minerals list, reinforcing a global trend toward formal strategic recognition of the mineral's importance. Australia's federal position is consequently becoming increasingly isolated by comparison.

The New South Wales Upper House Breakthrough

For the first time in 39 years, a bill to remove both the uranium mining ban and the nuclear energy ban passed the NSW upper house. The bill must now pass the lower house, where the current political composition makes full passage in its existing form unlikely. Strategic options include separating the uranium mining component from the nuclear energy component to improve the probability of passage.

With a NSW state election approaching, the bill's trajectory through the lower house will be shaped by shifting electoral mathematics. The Broken Hill region provides a compelling economic case study: the area already has a uranium-competent workforce that commutes across the state border into South Australia to work at existing ISR operations. The geological mineralisation does not respect state boundaries, and the economic infrastructure for NSW uranium mining essentially already exists.

Western Australia: A Soft Signal Through Exploration Grants

Perhaps the most structurally interesting development is that the Western Australian government, which maintains a formal ban on uranium mining, has simultaneously issued government grants for uranium exploration within the state. The operational logic of funding the discovery of a resource that cannot currently be extracted represents either a policy contradiction or a soft signal that the ban is being reconsidered at a policy level.

Recent polling indicates approximately 57% of respondents support lifting the WA uranium mining ban, a level of public support that is politically significant in a state where resource sector employment and the broader mining economy are central to household income and government revenue. For a more detailed breakdown of the current regulatory landscape, the WA uranium mining status provides important additional context for investors monitoring this space.

The next major ASX story will hit our subscribers first

The Global Uranium Demand Picture

The IEA's Energy Security Warning

The head of the International Energy Agency recently characterised the current energy market disruption as larger than both 1970s oil shocks combined — an extraordinary statement from a historically cautious institution. The 1970s shocks triggered a wave of nuclear investment across the developed world. The IEA has indicated a similar investment cycle is likely to emerge within the next 12 to 24 months, driven by energy security concerns, rising electricity demand from AI data centres, and nuclear restart programmes across Europe and Asia.

For Australia's uranium sector, this global dynamic represents a structural demand tailwind. However, the translation of that global opportunity into local capital formation depends heavily on whether domestic policy barriers are reduced in a timeframe that aligns with the international investment cycle.

Australia's Fuel Security Vulnerability

Australia imports the majority of its liquid fuel requirements and operates only two fuel refining facilities nationally. Disruptions to Strait of Hormuz shipping routes created acute diesel supply shortages across the Australian mining sector, with some Western Australian operations forced to curtail or suspend activities entirely.

During the peak of the disruption, some mining companies received only approximately one-third of their requested diesel allocations despite their willingness to pay elevated prices. A national fuel task force with state representation was activated in response. This episode has accelerated policy discussions around energy self-sufficiency, with nuclear energy increasingly cited as a structural long-term solution rather than a fringe position.

International Capital Interest in Australian Uranium

Global interest in Australian uranium assets is drawing from multiple directions:

-

France: Previously sourced approximately 15% of uranium supply from Niger for its 58-reactor fleet before supply disruptions. French nuclear fuel companies, including Orano, had previously fully exited Australia but have recommenced operations and are actively seeking expanded involvement, particularly in Western Australia where French companies were responsible for most of the state's uranium discoveries during the 1970s.

-

Japan: Restarting existing reactors while simultaneously planning new builds, Japan is actively seeking to lock in uranium supply for the 2030s from trusted jurisdictions. Japanese investors have a strong historical relationship with Australian uranium investment and are aware they are competing against a narrowing window of opportunity.

-

Korea: Emerging as a potential capital source with strategic interest in securing long-term supply from politically stable, rule-of-law jurisdictions.

-

Canada: Cameco holds significant Western Australian uranium assets and continues to commit exploration capital, signalling institutional confidence in the long-term policy trajectory.

It is worth noting that Chinese investment in Australian uranium assets would attract significant national security scrutiny under existing foreign investment frameworks. This creates a structural competitive advantage for Japanese, Korean, French, and Canadian capital in accessing Australian projects.

ISR Technology: The Environmental and Commercial Case

Why In-Situ Recovery Changes the Development Economics

In-situ recovery (ISR) is widely recognised as the lowest-capital-expenditure and most environmentally sensitive method of uranium extraction commercially available. Rather than physically removing rock through open-cut or underground methods, ISR dissolves uranium mineralisation in place using a lixiviant solution, then pumps the uranium-bearing solution to a surface processing facility.

The in-situ leaching benefits are substantial and increasingly well understood by both regulators and investors. The practical advantages include:

- Dramatically smaller surface disturbance footprint compared to conventional mining

- Lower capital expenditure thresholds, improving project economics at lower uranium prices

- More straightforward environmental approval pathway in politically sensitive jurisdictions

- Well-established technical learning curve with global reference operations

Uzbekistan is recognised as the birthplace of commercial ISR uranium mining and remains the global reference point for technical best practice. Australian developers are actively benchmarking against both domestic ISR operations in South Australia and international precedents to optimise process flow design and reduce development risk.

Energy Price Dynamics: What the Regulator's Data Actually Shows

Reading the Retail Price Cap Data Correctly

Australia's energy regulator has announced retail energy price cap reductions for the coming year. The government has attributed this to successful renewable energy rollout. However, a more granular analysis of the data tells a more complex story.

The largest price reductions are concentrated in Queensland, driven primarily by expanded coal availability following the Queensland state government's commitment to maintaining coal-fired generation capacity through to approximately 2050. The smallest price reductions are recorded in South Australia, which has the highest penetration of renewable generation and grid-scale storage in the country.

This data creates a politically contested environment where both pro-coal and pro-renewable advocates can selectively cite supporting statistics with equal technical accuracy. The headline narrative that renewables deployment reduces consumer energy costs is not consistently supported by the comparative state-level data.

Green Hydrogen: The Billion-Dollar Programme That Did Not Deliver

The federal budget included a $1 billion reduction in funding for the Hydrogen Headstart programme, which was designed to subsidise large-scale green hydrogen projects. Industry analysis suggests the funding was unlikely to have been deployed regardless, as no projects had reached the milestone thresholds required to trigger matching government contributions.

The effective cancellation represents a significant setback for Australia's green hydrogen ambitions and implicitly redirects policy attention toward nuclear and gas as credible baseload energy solutions.

Investment Implications Across Asset Classes

Reassessing After-Tax Return Expectations

The removal of the 50% CGT discount materially reduces after-tax returns for long-term equity and property investors in higher marginal tax brackets. The structural impact flows through multiple asset classes:

-

Listed equities and ETFs: No structural advantage is preserved under the new regime. ETF investors face the same CGT treatment as direct share investors, and the psychological impact on retail participation in public equity markets is a near-term risk.

-

Residential property: The combined effect of CGT reform and negative gearing restrictions will reshape investment demand dynamics, though the magnitude of price impact remains contested.

-

Resource exploration: The minerals exploration sector faces a compounding challenge. The risk profile of early-stage exploration, where capital is deployed years before any potential realisation event, makes the 50% discount particularly important as a risk-adjusted return incentive. Without carve-outs, the effective cost of capital for junior ASX-listed resource companies increases significantly.

The Uranium Sector's Unique Rerating Opportunity

Australian uranium companies operating in ban jurisdictions trade at a discount relative to peers in permitting-friendly environments, reflecting the policy risk premium embedded in their valuations. As the probability of ban removal increases through electoral shifts, legislative progress, and international capital interest, a meaningful rerating opportunity exists that is independent of underlying uranium price movements.

Furthermore, uranium investment strategies that account for both the CGT changes and the evolving state-level policy landscape are increasingly relevant for investors seeking exposure to this sector. The scale of uranium mineralisation in Western Australia is not yet widely appreciated by generalist investors. Projects in the region are targeting resource bases that could potentially position Australia as a globally significant uranium jurisdiction, but only if the policy environment aligns with the investment cycle the IEA is now actively forecasting.

According to PwC's federal budget investment analysis, the cumulative effect of these reforms on long-term investment behaviour in Australia represents one of the most significant structural shifts seen in recent memory.

Disclaimer: This article contains forward-looking statements, forecasts, and speculative analysis based on publicly available information and sourced research. It does not constitute financial advice. Investors should conduct their own due diligence and consult a licensed financial adviser before making investment decisions. Policy timelines, legislative outcomes, and market projections referenced in this article are subject to change and involve material uncertainty.

FAQ: Australia's CGT Changes and Uranium Mining Bans

When Do the Proposed CGT Changes Take Effect?

The changes are proposed to apply from 1 July 2027, subject to parliamentary passage. They are not yet legislated.

Does the CGT Reform Affect Superannuation Funds?

The current proposals primarily target individuals, trusts, and partnerships. The specific treatment of superannuation fund assets requires further clarification through the legislative process.

Which States Currently Allow Uranium Mining in Australia?

South Australia and the Northern Territory permit uranium mining. Western Australia, New South Wales, and Queensland maintain restrictions ranging from full bans to exploration-only permissions.

Is Australia's Uranium Mining Ban a Federal or State-Level Policy?

Uranium mining regulation is primarily a state-level responsibility. The federal government does not maintain a blanket mining ban but excludes uranium from its national critical minerals list — a position that is increasingly at odds with state-level developments.

How Does Inflation Indexation Compare to the 50% Discount for Long-Term Investors?

In low-inflation environments, indexation provides substantially less relief than the 50% discount. For most historical holding periods and inflation scenarios, the 50% discount has delivered greater tax relief than indexation would have produced.

What Is ISR Uranium Mining and Why Does It Matter for Australian Projects?

In-situ recovery is a method of extracting uranium by dissolving it in place and pumping the solution to surface for processing. It has a smaller environmental footprint, lower capital costs, and a more established regulatory approval pathway than conventional mining, making it particularly relevant for projects in politically sensitive or newly permitted jurisdictions.

Want to Stay Ahead of the Next Major ASX Mineral Discovery?

As Australia's policy landscape shifts — from capital gains tax reform to evolving uranium mining regulations — the window to act on significant ASX mineral discoveries can close rapidly. Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment major mineral discoveries hit the ASX, transforming complex data across 30+ commodities into clear, actionable insights for both short-term traders and long-term investors — start a 14-day free trial today, or explore historic discovery returns to understand just how significant these opportunities can be.