June 23, 2026

Global macroeconomic forces are fundamentally reshaping capital allocation strategies across resource-intensive industries, with mining operations experiencing unprecedented pressure on project viability assessments. The convergence of inflation, energy transition challenges, supply chain disruption, and tightening financial conditions has created a perfect storm that challenges traditional investment frameworks developed during more stable economic periods.

What Drives Capital Project Viability Concerns in Modern Mining Operations?

The mining sector faces a dramatic shift in executive sentiment regarding capital project feasibility. Research indicates that executive anxiety surrounding project viability has escalated sharply, climbing from 30% to 50% between 2024 and 2025, representing a 20 percentage point increase that reflects mounting systemic pressures across the industry.

This surge in concerns about capital project viability in mining operations stems from multiple converging factors. Energy costs alone have created substantial pressure, with 50% of mining executives citing clean energy implementation expenses as a primary threat to project economics. Additionally, 25% of executives express specific concern about inflationary pressures affecting their capital allocation decisions, while supply chain volatility impacts approximately 74% of major projects.

Defining Capital Project Viability in Resource Extraction

Capital project viability in contemporary mining extends far beyond traditional net present value (NPV) and internal rate of return (IRR) calculations. Modern assessment frameworks must incorporate environmental, social, and governance (ESG) criteria, carbon pricing mechanisms, and regulatory compliance costs that were marginal considerations in previous investment cycles.

The temporal dimension of viability assessment has become increasingly complex. Mining executives now evaluate projects across multiple timeframes simultaneously:

• Near-term compliance windows (2-5 years) for regulatory adherence

• Medium-term energy transition requirements (5-15 years) for decarbonisation pathways

• Long-term carbon neutrality commitments (2030-2050) for climate targets

This multi-temporal evaluation framework creates compounding complexity in discounted cash flow analysis, as traditional financial models struggle to capture the interconnected risks spanning different time horizons.

The Economic Framework Behind Mining Investment Decisions

The methodological shift in project evaluation reflects changing investor expectations and capital market dynamics. Institutional investors increasingly scrutinise mining projects for alignment with net-zero emissions pathways, water stewardship capabilities, and community engagement protocols.

Modern viability frameworks incorporate both quantifiable metrics (NPV, IRR, payback periods) and qualitative variables including:

• Community acceptance and social licence to operate

• Regulatory stability and jurisdictional risk assessments

• Climate resilience and stranded asset risk valuations

• Supply chain resilience and input cost volatility

These expanded criteria necessitate sophisticated risk-adjusted return calculations that account for both traditional financial returns and non-financial performance indicators affecting long-term operational sustainability.

When big ASX news breaks, our subscribers know first

How Do Macro-Economic Forces Impact Mining Capital Allocation?

Macroeconomic volatility has emerged as a primary driver of capital project uncertainty, fundamentally altering how mining companies evaluate long-term investments. The interconnection between global economic conditions and mining project economics creates cascading effects that traditional risk assessment models struggle to capture effectively.

Global Inflation Pressures on Mining Infrastructure Development

Inflationary pressures create disproportionate impacts on mining capital projects due to their extended development timelines and capital intensity. Mining infrastructure projects typically require 5-10 years for completion, during which cumulative cost inflation compounds significantly.

A 3% annual inflation rate produces approximately 34% cumulative cost escalation across a typical 10-year project development cycle, substantially eroding expected returns. This mathematical reality forces mining companies to build larger contingency reserves into project budgets, reducing investment attractiveness and delaying final investment decisions.

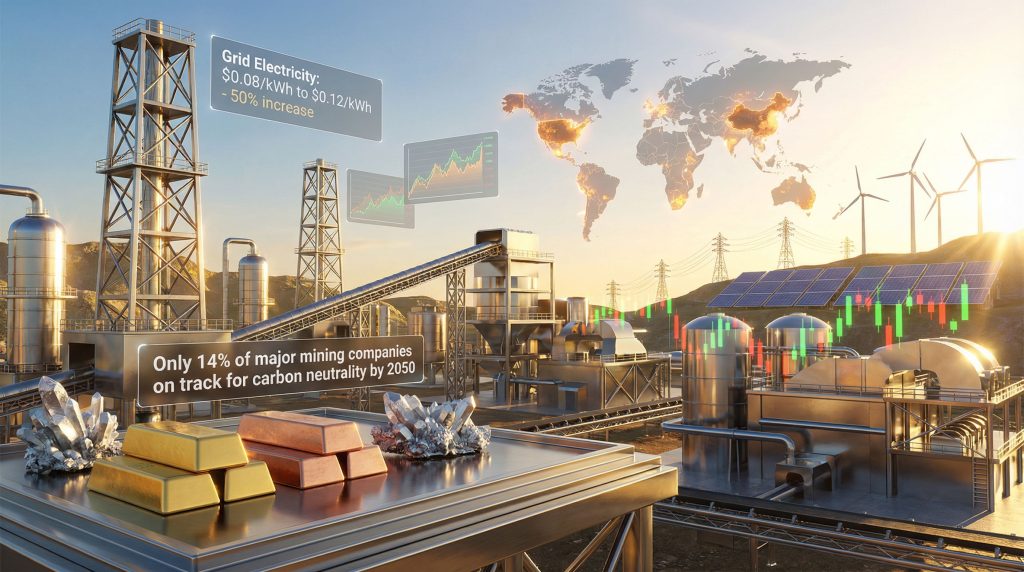

Energy-specific inflation creates the most severe impacts on mining operations. Analysis reveals dramatic cost escalation across critical energy categories:

| Energy Type | 2023 Baseline Cost | 2025 Current Cost | % Increase | Impact on CAPEX |

|---|---|---|---|---|

| Grid Electricity | $0.08/kWh | $0.12/kWh | 50% | +15-20% |

| Renewable Integration | $45/MWh | $65/MWh | 44% | +25-30% |

| Diesel (Remote Sites) | $1.20/L | $1.85/L | 54% | +35-40% |

These energy-specific inflation rates substantially exceed general inflation indices, indicating that mining's energy-intensive operations create disproportionate exposure to energy price volatility compared to less energy-dependent industries.

Interest Rate Cycles and Their Effect on Long-Term Mining Investments

Interest rate sensitivity in mining stems from the capital intensity of projects and extended payback periods. A typical major mining project requires $3-5 billion in capital investment and generates returns over 20-30 year operational lifespans, making mining projects particularly vulnerable to discount rate fluctuations.

The mathematical impact of interest rate changes on project economics is substantial. At a weighted average cost of capital (WACC) of 6%, mining project NPV calculations differ dramatically from those using a 10% WACC. An incremental 4% increase in discount rates can reduce NPV by 30-40% depending on project cash flow timing and commodity price assumptions.

Elevated interest rates create dual pressure on mining capital allocation:

• Equity investors demand higher expected returns to compensate for increased financing costs

• Debt markets impose stricter covenants and higher spreads on mining-sector borrowing

This dual compression of capital availability has effectively created a capital rationing environment where only the highest-confidence, lowest-risk projects secure financing at acceptable terms.

Currency Volatility and International Mining Project Economics

Currency volatility introduces substantial complexity to international mining capital allocation decisions. Most major mining commodities are priced in US dollars globally, while mining operations occur across diverse jurisdictions with distinct currency regimes.

Currency risk manifests through three distinct mechanisms:

• Transaction exposure during project development phases when capital is committed in local currency

• Translation exposure when consolidated financial statements convert subsidiary results into parent company reporting currency

• Economic exposure where long-term competitiveness depends on currency-adjusted commodity prices relative to local cost structures

Mining companies developing projects in emerging market currencies face particular challenges when the US dollar strengthens, as operational profitability declines while debt servicing costs denominated in foreign currency increase proportionally.

Which Structural Cost Factors Threaten Mining Project Economics?

Structural cost factors represent permanent shifts in mining industry cost structures rather than cyclical fluctuations, fundamentally altering the economic baseline for capital project evaluation. These factors create sustained pressure on project returns that traditional business cycle models cannot address.

Energy Cost Inflation and Clean Technology Implementation Expenses

Energy represents the most economically material structural cost factor threatening mining project viability. Research indicates that 50% of mining sector executives identify clean energy costs as a material concern affecting capital project economics, representing the highest individual concern category identified in industry analysis.

The energy transition creates unavoidable cost escalation for mining operations. Unlike discretionary cost reduction initiatives, energy transition represents mandatory expenses that all mining companies must absorb regardless of competitive positioning strategies. This regulatory and social requirement eliminates traditional cost management flexibility.

Grid electricity costs have increased 50% from $0.08/kWh to $0.12/kWh between 2023 and 2025, creating 15-20% CAPEX impact on mining projects. This substantial increase reflects global electricity market tightening, transmission infrastructure constraints, and demand-side pressures from industrial electrification trends.

Renewable energy integration expenses have escalated 44% from $45/MWh to $65/MWh during the same period, generating 25-30% CAPEX impact. This category encompasses solar and wind installation expenses, grid interconnection infrastructure, and energy storage requirements for supply reliability in mining operations.

Diesel costs for remote operations have experienced the most acute inflation, surging 54% from $1.20/litre to $1.85/litre, producing 35-40% CAPEX impact. This affects remote mining operations in regions like Sub-Saharan Africa, Papua New Guinea, and western Australia where grid electricity access remains unavailable.

Supply Chain Disruption Costs and Material Price Volatility

Supply chain vulnerability has emerged as a critical structural cost factor, with 74% of heavy industry executives anticipating that supply chain volatility will negatively impact major capital projects through 2028. This elevated concern percentage indicates that supply chain risk has achieved parity with traditional commodity price risk in executive consciousness.

Supply chain disruptions increase project costs 5-15% and extend project timelines 6-24 months, depending on disruption severity. These impacts cascade through project financing structures, increasing debt service costs and extending weighted average borrowing periods.

The mining industry's dependence on specialised equipment and technical services creates particular vulnerability to supply chain disruption. Critical mining equipment often requires:

• 12-18 month manufacturing lead times for major components

• Specialised technical expertise available from limited global suppliers

• Complex logistics coordination for oversized equipment transport to remote locations

Furthermore, understanding commercial risks in mining projects becomes essential for comprehensive risk management strategies.

Labour Market Constraints and Wage Inflation Pressures

Mining operations face acute skilled labour shortages that create wage inflation pressures substantially exceeding general labour market trends. The technical specialisation required for modern mining operations, combined with geographical isolation of many projects, creates structural labour market imbalances.

Key labour market constraints include:

• Ageing workforce demographics as experienced miners approach retirement

• Limited training pipeline capacity for specialised technical roles

• Geographic concentration challenges in remote mining regions

• Competition from renewable energy sector for technical talent

These constraints force mining companies to offer premium compensation packages, including rotation schedules, housing allowances, and specialised benefits that increase total labour costs 20-35% above comparable urban industrial positions.

Why Are Decarbonisation Targets Creating Investment Uncertainty?

Decarbonisation requirements represent one of the most significant structural changes affecting mining investment decisions, creating both mandatory cost increases and timeline uncertainty that traditional project evaluation methods struggle to accommodate effectively.

The Economics of Carbon-Neutral Mining Operations

Carbon neutrality commitments create fundamental tension between short-term profitability and long-term sustainability requirements. Only 14% of major mining companies are currently on track to achieve carbon neutrality by 2050, down from 18% in 2024, reflecting growing recognition of the massive capital requirements needed for comprehensive emissions reduction.

Mining companies face a cascade of overlapping challenges that fundamentally alter how they must evaluate capital project feasibility, requiring simultaneous consideration of traditional financial returns and extensive decarbonisation pathway investments.

The decline in companies meeting decarbonisation targets indicates that initial carbon reduction estimates significantly underestimated actual implementation costs and technical complexity. This realisation forces mining companies to reassess capital allocation priorities between immediate operational returns and longer-term climate compliance.

Technology Investment Requirements vs. Short-Term Profitability

Decarbonisation technology investments create immediate capital outflows with uncertain return profiles, challenging traditional mining investment criteria focused on measurable commodity production increases. Key technology categories requiring substantial investment include:

• Carbon capture and storage systems for processing facilities

• Electrification of mobile mining equipment and haul truck fleets

• Renewable energy generation and storage infrastructure

• Process efficiency optimisation through AI integration benefits

The payback periods for these investments often extend beyond traditional mining project evaluation horizons, creating tension between quarterly earnings expectations and long-term carbon reduction commitments.

Regulatory Compliance Costs and ESG Investment Mandates

Regulatory frameworks governing mining emissions continue evolving, creating uncertainty about future compliance costs and technical requirements. Mining companies must invest in decarbonisation technologies without complete certainty about final regulatory specifications or timeline requirements.

ESG investment mandates from institutional investors add additional pressure, as mining companies must demonstrate measurable progress toward emissions reduction to maintain access to capital markets. This creates a feedback loop where delayed decarbonisation investments increase future capital costs through higher borrowing spreads and reduced investor interest.

How Do Financing Conditions Affect Mining Project Viability?

Capital market conditions have tightened significantly for mining projects, creating a financing environment that favours only the most economically robust projects while constraining capital availability for marginal investments that previously secured funding.

Capital Market Access and Investor Risk Appetite Changes

Mining equity valuations have compressed as investors demand higher risk premiums for commodity exposure and operational complexity. The combination of macroeconomic uncertainty and sector-specific challenges has reduced investor appetite for mining investments requiring extended development timelines.

Institutional investors increasingly apply ESG screening criteria that eliminate mining projects failing to meet environmental and social governance standards. This screening process reduces the pool of available capital while increasing competition among qualifying projects.

Debt Financing Costs for Long-Term Mining Development

Mining project financing typically employs project finance structures that rely on non-recourse or limited-recourse debt secured by project cash flows. These structures demonstrate particular sensitivity to interest rate changes because:

• Debt service represents fixed claims on project cash flows regardless of commodity price volatility

• Refinancing risk emerges as construction loans must convert to long-term operating facilities

• Floating-rate exposure creates unhedged interest rate risk for companies without comprehensive derivatives programmes

Lenders have tightened covenant structures and increased spread requirements for mining projects, reflecting perceived increases in operational and regulatory risk across the sector.

Equity Market Valuations and Mining Sector Investment Flows

Public equity markets have assigned lower valuation multiples to mining companies, reflecting investor scepticism about long-term profitability amid rising operational costs and regulatory requirements. This valuation compression increases the cost of equity capital and reduces the attractiveness of equity financing for new project development.

Private equity and infrastructure funds have partially filled the financing gap, but typically demand higher returns and shorter investment horizons than traditional mining project timelines accommodate.

What Role Does Geopolitical Risk Play in Capital Project Assessment?

Geopolitical considerations have assumed increasing importance in mining capital allocation decisions, as traditional risk assessment frameworks prove inadequate for capturing the complexity of contemporary international resource development.

Resource Nationalism and Investment Security Concerns

Resource nationalism trends across major mining jurisdictions create uncertainty about long-term investment security and operational control. Government policies increasingly favour domestic participation in mining projects through:

• Local ownership requirements mandating domestic equity participation

• Beneficiation mandates requiring in-country processing of raw materials

• Infrastructure development obligations linking mining permits to social investment commitments

These requirements increase project complexity and capital requirements while reducing operational flexibility for international mining companies.

Trade Policy Impacts on Mining Project Economics

International trade policy uncertainty affects mining project economics through tariff risks, export restrictions, and bilateral trade agreement modifications. Understanding trade policy effects becomes crucial as mining companies must evaluate projects across multiple trade policy scenarios, complicating NPV calculations and investment decision frameworks.

Recent trade tensions have demonstrated how quickly government policies can alter mining project economics, forcing companies to build additional risk premiums into investment evaluation processes.

Critical Mineral Supply Chain Vulnerabilities

Critical mineral designation by major economies creates both opportunities and risks for mining projects. While critical mineral status can provide government support and favourable regulatory treatment, it also increases geopolitical scrutiny and potential trade restriction risks.

Mining companies developing critical mineral projects must consider national security implications and potential government intervention in operational decisions, adding complexity to traditional commercial risk assessment.

The next major ASX story will hit our subscribers first

Which Technological Solutions Can Improve Project Viability?

Technology adoption represents one of the few available strategies for mining companies to offset structural cost increases and improve capital project economics through operational efficiency and risk mitigation.

Modular Construction and Standardised Design Approaches

Modular construction methodologies offer potential cost reduction through standardisation and manufacturing efficiency. Multi-project approaches can reduce capital costs significantly, with analysis indicating potential reductions of 20% in initial phases and up to 35% at scale when applied systematically across mining operations.

Standardised design approaches enable mining companies to:

• Leverage manufacturing economies of scale across multiple projects

• Reduce engineering and design costs through template replication

• Accelerate construction timelines through prefabricated component assembly

• Improve quality control through factory manufacturing processes

Artificial Intelligence Integration for Cost Optimisation

AI integration offers substantial potential for mining cost optimisation through predictive maintenance, process optimisation, and operational efficiency improvements. Key applications include:

• Equipment performance monitoring to prevent costly unplanned downtime

• Energy consumption optimisation through demand forecasting and load balancing

• Supply chain coordination to minimise inventory costs and procurement delays

• Safety monitoring systems to reduce workplace accidents and associated costs

| Strategy Type | Implementation Cost | Risk Reduction % | ROI Timeline |

|---|---|---|---|

| Modular Design | 15-20% premium | 25-35% | 3-5 years |

| AI Integration | 10-15% premium | 20-30% | 2-4 years |

| Portfolio Approach | 5-10% premium | 30-50% | 5-7 years |

Digital Twin Technology for Risk Mitigation

Digital twin technology enables mining companies to simulate operational scenarios and optimise project design before committing capital to physical construction. This capability reduces technical risk and improves project economics through:

• Virtual testing of equipment configurations and process flows

• Scenario analysis for operational optimisation under different market conditions

• Training simulation for personnel development without operational disruption

• Predictive modelling for maintenance scheduling and equipment replacement

How Are Mining Companies Adapting Their Capital Allocation Strategies?

Mining companies are fundamentally restructuring their capital allocation approaches to address the changed risk environment, moving away from traditional single-project evaluation toward more sophisticated portfolio management strategies.

Portfolio-Based Investment Approaches vs. Individual Project Focus

The traditional model of evaluating mining projects individually has proven inadequate for managing contemporary risk complexity. Mining companies increasingly adopt portfolio approaches that:

• Diversify commodity exposure across multiple metal types and market cycles

• Distribute geographic risk across different jurisdictions and regulatory environments

• Balance development timelines to maintain consistent cash flow generation

• Optimise resource allocation across exploration, development, and operational phases

Portfolio approaches enable companies to absorb individual project failures while maintaining overall investment returns through diversification benefits.

Strategic Partnership Models for Risk Sharing

Mining companies increasingly pursue strategic partnerships to share capital requirements and operational risks across multiple participants. Common partnership structures include:

• Joint ventures for shared development costs and technical expertise

• Streaming agreements for upfront capital in exchange for future production rights

• Infrastructure partnerships for shared logistics and processing facilities

• Technology alliances for R&D cost sharing and innovation acceleration

Consequently, these partnerships enable companies to implement sophisticated capital raising strategies while maintaining operational flexibility.

Phased Development Strategies to Manage Capital Exposure

Phased development strategies enable mining companies to limit initial capital commitments while preserving expansion options based on market conditions and operational performance. This approach reduces downside risk while maintaining upside potential through:

• Modular expansion capability based on market demand and commodity prices

• Technology integration phases allowing for gradual adoption of new systems

• Market validation stages before committing to full-scale production capacity

• Financing flexibility through staged capital requirements aligned with cash flow generation

What Economic Indicators Signal Improved Project Viability Conditions?

Mining executives monitor multiple economic indicators to assess optimal timing for capital project commitments, seeking alignment between favourable market conditions and internal project readiness.

Commodity Price Stability Metrics and Forward Curve Analysis

Commodity price volatility creates uncertainty in mining project NPV calculations, making price stability a critical indicator for investment timing. Forward curve analysis provides insights into:

• Price trajectory expectations over project development timelines

• Volatility patterns that affect financing availability and terms

• Market fundamentals driving supply-demand balance projections

• Hedging opportunities for price risk management during construction phases

Sustained commodity price stability above project breakeven levels creates favourable conditions for final investment decisions and financing commitments.

Infrastructure Investment Cycles and Regional Development Patterns

Government infrastructure investment cycles significantly impact mining project economics through shared infrastructure benefits and reduced development costs. Key indicators include:

• Transportation infrastructure development reducing logistics costs

• Power grid expansion providing reliable electricity access

• Port and terminal capacity increases improving export capabilities

• Regional development programmes supporting workforce availability and community acceptance

Technology Cost Reduction Trajectories

Technology cost curves provide critical timing signals for mining companies evaluating when to implement new systems and processes. Declining technology costs create incentives to delay implementation until optimal pricing, while technology maturity reduces operational risk.

Key technology cost indicators include:

• Renewable energy system costs for mine power requirements

• Battery storage costs for grid independence and reliability

• Automation technology costs for operational efficiency improvements

• Digital infrastructure costs for data management and process optimisation

Which Regional Markets Offer the Most Favourable Investment Conditions?

Regional investment conditions vary significantly across major mining jurisdictions, creating opportunities for mining companies to optimise project location decisions based on regulatory stability, infrastructure availability, and operational costs.

Comparative Analysis of Mining Investment Jurisdictions

Mining investment attractiveness depends on multiple factors including regulatory stability, taxation frameworks, infrastructure quality, and political risk. Leading jurisdictions typically offer:

• Transparent regulatory processes with predictable permitting timelines

• Competitive taxation structures balancing government revenue with investment returns

• Established infrastructure reducing project development costs

• Skilled workforce availability supporting operational requirements

Emerging markets may offer higher potential returns but require additional risk premiums to compensate for regulatory uncertainty and infrastructure limitations.

Infrastructure Development and Regulatory Stability Factors

Infrastructure quality significantly impacts mining project economics through construction costs, operational efficiency, and export capability. Critical infrastructure elements include:

• Transportation networks connecting mines to processing facilities and ports

• Power generation and transmission providing reliable electricity supply

• Water infrastructure supporting processing requirements and community needs

• Telecommunications networks enabling digital technology implementation

Regulatory stability provides confidence in long-term investment security and operational predictability, reducing risk premiums required by investors and lenders.

Local Content Requirements and Economic Impact Considerations

Local content requirements increasingly influence mining project design and economics through mandatory domestic participation in:

• Employment and training of local workforce

• Procurement from domestic suppliers and service providers

• Value-added processing of raw materials within host countries

• Community development programmes and infrastructure contributions

While local content requirements increase project complexity and potentially costs, they can improve community relations and reduce regulatory risk through enhanced stakeholder alignment.

How Can Mining Companies Build Resilient Capital Project Portfolios?

Building resilient capital project portfolios requires sophisticated risk management approaches that address the interconnected nature of contemporary mining investment challenges while preserving flexibility to capitalise on market opportunities.

Diversification Strategies Across Commodity Types and Geographies

Effective portfolio diversification requires strategic balance across multiple dimensions to reduce overall risk while maintaining return potential. Key diversification strategies include:

Commodity diversification across metals with different market cycles and demand drivers:

• Base metals (copper, zinc) for industrial demand exposure

• Precious metals (gold, silver) for store-of-value characteristics

• Battery metals (lithium, cobalt) for energy transition participation

• Bulk commodities (iron ore, coal) for established market stability

Geographic diversification across jurisdictions with different risk profiles:

• Developed markets offering regulatory stability and infrastructure

• Emerging markets providing growth potential and resource access

• Different currency zones for natural hedging benefits

• Various political systems reducing sovereign risk concentration

Scenario Planning for Multiple Economic Environments

Contemporary mining investment decisions require robust scenario planning across multiple potential economic futures rather than single-point forecasts. Critical scenarios include:

• Inflationary environments with elevated input costs and energy prices

• Deflationary pressures from technological advancement and productivity gains

• Energy transition acceleration driving demand shifts across commodities

• Geopolitical instability affecting trade flows and supply chains

Scenario planning enables mining companies to identify investment options that perform adequately across multiple potential futures while maintaining flexibility to optimise for emerging conditions.

Contingency Planning and Flexible Investment Structures

Flexible investment structures provide mining companies with optionality to adapt to changing market conditions while limiting downside exposure. Key structural approaches include:

• Real options frameworks providing expansion and abandonment alternatives

• Staged investment phases enabling progressive capital commitment based on results

• Partnership structures allowing risk sharing and expertise access

• Technology platforms supporting multiple applications and operational improvements

Contingency planning must address both upside and downside scenarios, ensuring companies can capitalise on favourable conditions while protecting against adverse developments. In addition, recognising reducing delays as crucial levers for improving project success rates remains essential for portfolio resilience.

Furthermore, companies must stay informed about industry evolution trends to adapt their approaches effectively. The mining industry stands at a critical inflection point where traditional capital allocation approaches prove inadequate for navigating contemporary challenges. Success requires sophisticated risk management, technology adoption, and strategic flexibility that recognises the fundamental shifts in global economic conditions affecting resource development. Companies that successfully adapt their capital project evaluation and portfolio management approaches will emerge stronger from this period of uncertainty, while those clinging to outdated frameworks risk obsolescence in a rapidly evolving investment landscape.

Ready to capitalise on major mineral discoveries before the market reacts?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Understand why historic discoveries can generate substantial returns by exploring Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the market.