August 4, 2026

The global aluminum sector stands at a critical juncture where environmental policy intersects with industrial competitiveness in unprecedented ways. Europe's manufacturing landscape faces a fundamental reshaping as carbon pricing mechanisms evolve from theoretical frameworks into concrete market realities that will determine the continent's industrial future. The intersection of climate policy and trade war impacts creates complex scenarios where traditional competitive advantages may be inverted, and established supply chains could face complete reconfiguration.

The european aluminium industry impact of cbam represents more than a regulatory adjustment; it signals a paradigm shift toward carbon-adjusted international trade that will ripple through global manufacturing networks. Understanding these market dynamics requires examination of how carbon pricing transforms from an environmental tool into a competitive weapon that could either strengthen European industrial resilience or accelerate its decline.

What Is the Carbon Border Adjustment Mechanism and Why Does It Matter for Aluminium?

CBAM's Core Framework and Implementation Timeline

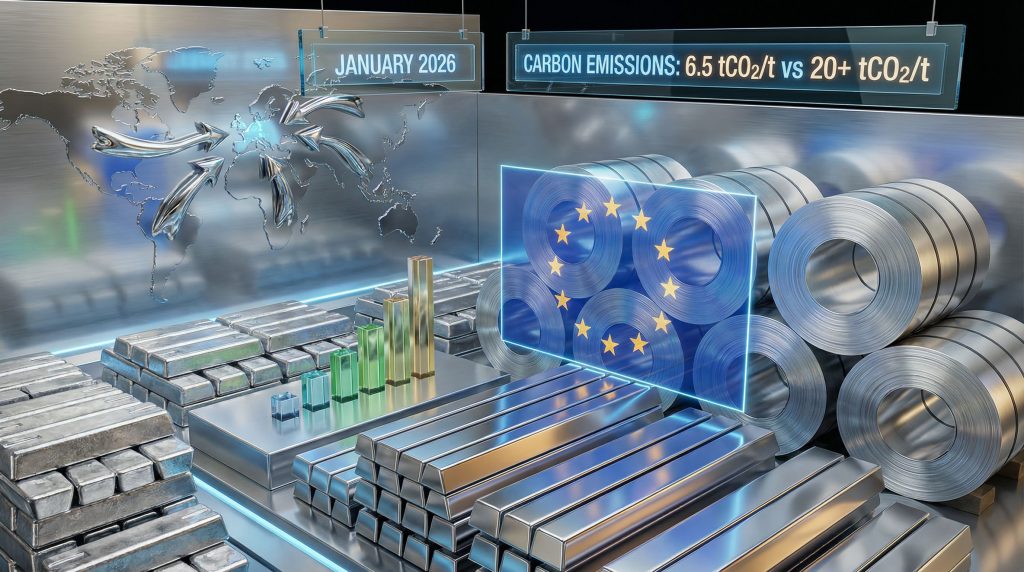

The Carbon Border Adjustment Mechanism establishes a comprehensive framework for imposing carbon costs on imports entering the European Union, with aluminum representing one of the initial sectors facing mandatory compliance beginning January 1, 2026. This definitive phase follows a transitional period from October 2023 through December 2025, during which importers reported embedded emissions data without financial penalties, allowing systems to establish baseline measurement protocols.

The scope encompasses primary aluminum, semi-finished products including sheets, plates, and extrusions, with ongoing discussions regarding expansion to downstream derivatives. Industry leaders express significant concern about implementation readiness, with Constellium CEO Jean-Marc Germain characterizing the policy as having good intentions but representing terrible implementation, noting that substantial uncertainties persist just weeks before the mandatory launch date.

Key Implementation Timeline:

- October 1, 2023 – December 31, 2025: Transitional reporting phase with no financial obligations

- January 1, 2026: Definitive phase begins with mandatory carbon cost payments

- 2026-2030: Gradual phase-out of EU ETS free allowances for domestic producers

The european aluminium industry impact of cbam extends beyond direct cost implications, creating cascading effects through supply chain verification requirements and administrative compliance burdens that smaller importers may struggle to manage effectively.

Carbon Pricing Methodology for Aluminium Imports

CBAM's pricing mechanism integrates carbon costs into European aluminum premiums, fundamentally altering the traditional London Metal Exchange price-plus-premium structure that has governed regional markets for decades. Starting January 1, 2026, all Fastmarkets European premiums inclusive of duty costs across ingots, billets, and primary foundry alloy will embed CBAM expenses directly into pricing frameworks.

The methodology creates dual pricing pathways where suppliers providing verified emissions data gain competitive advantages over those facing default emission value penalties. This verification-driven pricing structure incentivises transparency while penalising suppliers unable to document their carbon footprints through established third-party certification processes.

Emissions Calculation Framework:

- Verified Data Path: Suppliers with documented emissions face actual carbon costs

- Default Value Path: Unverified suppliers face conservative penalty rates

- Benchmark Integration: EU Commission utilises 2017-2021 production data for provisional rates

The carbon pricing methodology creates immediate market distortions where suppliers with identical production costs may face dramatically different market access expenses based solely on their documentation capabilities rather than actual environmental performance.

When big ASX news breaks, our subscribers know first

How Will CBAM Reshape European Aluminium Market Dynamics?

Cost Structure Transformation Analysis

CBAM implementation introduces a fundamental cost layer that elevates European aluminum prices above global benchmarks, creating what industry executives describe as an artificial competitiveness barrier. According to European Aluminium's analysis, CBAM raises aluminum costs throughout Europe, hindering the continent's export capabilities by making domestic production less competitive in international markets.

The cost transformation operates through multiple channels simultaneously. European manufacturers face increased input costs for CBAM-inclusive aluminum while competing against overseas producers who avoid these carbon charges entirely when exporting finished products back into European markets. This creates an inverse competitive dynamic where European manufacturers suffer cost disadvantages in both domestic and export markets.

Cost Impact Mechanism:

| Cost Component | Impact Level | Timeline |

|---|---|---|

| Direct aluminum input costs | High | Immediate (Jan 2026) |

| Energy costs (ETS allowance reduction) | High | Gradual (2026-2030) |

| Administrative compliance | Medium | Immediate |

| Supply chain verification | Medium | Ongoing |

Energy costs compound the challenge, with European production already facing electricity expenses two to three times higher than competitors in China or the United States. Furthermore, CBAM adds another cost layer while simultaneously reducing EU ETS free allowances, creating what industry leaders characterise as a double impact that undermines European industrial competitiveness rather than supporting decarbonisation objectives.

Supply Chain Reconfiguration Scenarios

The european aluminium industry impact of cbam extends beyond immediate cost increases to fundamental supply chain restructuring as buyers seek cost optimisation through alternative sourcing strategies. Market participants face strong incentives to source aluminum from outside the EU when CBAM-inclusive products carry premium pricing that cannot be passed through to end consumers effectively.

Verification requirements create additional sourcing criteria where suppliers' documentation capabilities become as important as traditional factors like price, quality, and delivery reliability. This shift favours established producers with robust environmental reporting systems while disadvantaging suppliers in regions with limited verification infrastructure.

Supply Chain Adaptation Strategies:

- Documentation-driven supplier selection based on emissions verification capabilities

- Geographic diversification toward low-carbon production regions

- Increased administrative burden for compliance management systems

- Alternative product sourcing to avoid CBAM-inclusive materials

The administrative burden assessment reveals significant compliance infrastructure costs for importers who must establish emissions data collection protocols, third-party verification relationships, and documentation management systems. These requirements favour larger importers with resources to manage complex compliance processes while potentially excluding smaller market participants.

What Are the Competitive Implications for European Aluminium Producers?

The Double Impact Challenge

European aluminum producers face simultaneous cost pressures from CBAM implementation and EU ETS free allowance reductions, creating what industry executives describe as a double impact scenario that threatens sector viability. In addition to mining industry evolution patterns affecting global supply chains, CBAM raises aluminum costs for downstream manufacturers while the gradual elimination of ETS free allowances increases energy expenses for domestic producers, compounding competitive disadvantages.

The challenge intensifies because European energy costs already exceed those in major competing regions by substantial margins. Adding CBAM costs to already elevated energy expenses creates cost structures that may prove unsustainable for energy-intensive aluminum production, potentially accelerating facility closures that have already claimed five European smelters since 2021.

Recent Smelter Closures Context:

- Five facilities closed since 2021, all electrically powered

- Lost low-carbon capacity that supported European emissions profile

- Energy cost pressures preceding CBAM implementation

- Competitive disadvantage accumulation through regulatory layers

Industry analysis suggests that current policy design achieves outcomes opposite to stated environmental objectives. Rather than supporting European decarbonisation leadership, the combined CBAM and ETS pressure weakens domestic production while potentially increasing global emissions through production migration to higher-carbon regions.

Downstream Manufacturing Vulnerabilities

The european aluminium industry impact of cbam creates cascading effects through downstream manufacturing sectors that depend on aluminum inputs for production processes. Automotive manufacturing, already experiencing 6.2% production decline in 2024 according to ACEA data, faces additional cost pressures from CBAM-inclusive aluminum at a time when the sector confronts multiple economic challenges.

Sector Exposure Analysis:

| Manufacturing Sector | CBAM Exposure Level | Competitive Risk Assessment |

|---|---|---|

| Automotive Components | Direct material cost impact | Severe displacement risk |

| Beverage Can Production | Derivative product pricing | Moderate sourcing pressure |

| Construction Materials | Structural application costs | Severe competitive disadvantage |

| Aerospace Components | Specialised alloy pricing | Moderate supply chain shifts |

The competitive vulnerability stems from scope limitations where downstream manufacturers purchasing CBAM-inclusive aluminum face cost increases while overseas competitors manufacturing identical end products avoid carbon charges entirely when importing finished goods into European markets. This creates production relocation incentives that undermine European manufacturing employment and tax base.

Consequently, original equipment manufacturers face particularly acute challenges where CBAM costs apply to aluminum and steel inputs but exclude finished vehicles, aircraft, or construction products imported from outside the EU. This scope inconsistency creates strong incentives for production relocation that could accelerate European industrial decline.

Which Global Suppliers Will Benefit from CBAM Implementation?

Low-Carbon Production Advantage Matrix

CBAM implementation creates clear winners among global aluminum suppliers, particularly those operating hydroelectric-powered smelters in regions with abundant renewable energy resources. The european aluminium industry impact of cbam essentially creates a carbon-adjusted trade preference system that rewards low-emission production regardless of other economic factors.

Regional Emission Performance Comparison:

- European average: ~6.5 tCO2/tonne aluminum production

- Global average: ~14 tCO2/tonne aluminum production

- China average: >20 tCO2/tonne aluminum production

- Hydroelectric regions (Norway, Canada): 4-8 tCO2/tonne aluminum production

Suppliers in Norway, Canada, and other regions with access to renewable energy sources gain preferential market access to European buyers who face penalty rates when sourcing from higher-emission producers. This creates investment incentives for decarbonisation technologies while providing market access premiums for verified low-carbon aluminum production.

The verification advantage extends beyond emission levels to documentation capabilities, where suppliers with established environmental reporting systems can provide the third-party verification required for optimal CBAM treatment. This administrative advantage reinforces the competitive position of developed-market producers while disadvantaging suppliers in regions with limited certification infrastructure.

Strategic Positioning for Non-EU Producers

Non-EU aluminum producers face strategic decisions regarding investment in decarbonisation technologies versus market access diversification as CBAM reshapes European demand patterns. Similarly, considerations around European critical materials supply chains influence how the carbon pricing mechanism creates clear incentives for emission reduction investments while penalising suppliers unable to document environmental performance through verified reporting systems.

Strategic Adaptation Requirements:

- Emission reduction technology investments to improve carbon footprint

- Verification infrastructure development for documentation compliance

- Market access premium capture through low-carbon positioning

- Compliance system establishment for European market participation

Investment flows toward renewable energy-powered production capacity receive additional support from CBAM's preferential treatment of low-carbon aluminum, potentially accelerating global industry decarbonisation in regions targeting European market access. However, this may simultaneously disadvantage regions lacking renewable energy resources or capital for infrastructure modernisation.

What Are the Unintended Consequences and Market Distortions?

Resource Shuffling vs. Emission Reduction Reality

The european aluminium industry impact of cbam may achieve resource shuffling rather than genuine emission reductions, according to industry analysis highlighting potential policy contradictions. European aluminum production averages 6.5 tCO2/tonne compared to global averages of 14 tCO2/tonne and Chinese production exceeding 20 tCO2/tonne, suggesting that production migration could increase global emissions.

The closure of five European smelters since 2021, all electrically powered with relatively low carbon footprints, demonstrates how cost pressures can eliminate low-emission production capacity. CBAM's additional cost burden may accelerate this trend, potentially replacing European low-carbon production with higher-emission capacity in regions with cheaper energy and less stringent environmental standards.

Environmental Impact Assessment:

- Production migration risk from low-carbon European facilities to higher-emission regions

- Global emission profile deterioration through capacity reallocation

- Carbon leakage acceleration rather than reduction

- Policy contradiction between stated environmental goals and market outcomes

Furthermore, industry executives suggest that CBAM will not create new renewable-powered smelters in Europe but rather reshuffle existing resources, potentially leaving global emissions unchanged while weakening European industrial capacity and employment.

Circumvention Risks and Loopholes

CBAM implementation creates multiple circumvention opportunities through scope limitations and enforcement gaps that may undermine policy effectiveness while creating additional market distortions. The treatment of scrap metal, derivative products, and transshipment arrangements offers potential avenues for avoiding carbon costs without reducing actual emissions.

Identified Circumvention Vectors:

- Scrap metal treatment inconsistencies creating competitive gaps between recycled and primary aluminum

- Downstream product scope limitations excluding finished goods from carbon charges

- Transshipment opportunities through non-EU processing to avoid direct CBAM classification

- Product re-labelling potential to shift goods into non-covered categories

The European Commission's exploration of expanding CBAM coverage to semi-finished and finished products acknowledges these loopholes but may create additional complexity and administrative burden without closing fundamental gaps. However, industry analysis suggests that enforcement challenges and definitional ambiguities will create ongoing circumvention opportunities regardless of scope expansion efforts.

How Should European Aluminium Companies Prepare for CBAM?

Immediate Compliance Strategies

European aluminum companies require comprehensive preparation strategies addressing both immediate compliance requirements and longer-term competitive positioning as CBAM implementation approaches. The three-week timeline between industry warnings and mandatory implementation leaves limited preparation time for complex supply chain adjustments and cost modelling exercises.

Priority Compliance Actions:

- Supply chain emissions data collection protocols for all upstream suppliers

- Third-party verification partnerships to ensure documentation compliance

- Cost modelling scenarios across different carbon pricing assumptions

- Customer communication strategies for price increase management

The verification system establishment requires immediate attention as suppliers lacking proper documentation face default emission value penalties that could significantly impact cost competitiveness. Companies must develop relationships with certified verification bodies and establish emissions data collection protocols that meet CBAM requirements.

Administrative systems require upgrading to manage the documentation, reporting, and compliance tracking requirements that CBAM introduces. These systems must integrate with existing supply chain management platforms while providing audit trails for regulatory compliance and cost allocation purposes.

Long-term Strategic Adaptations

The european aluminium industry impact of cbam demands strategic repositioning that extends beyond immediate compliance to fundamental business model adaptation. Companies must evaluate their market positioning, supply chain structures, and investment priorities in light of permanently altered competitive dynamics.

Strategic Adaptation Framework:

- Decarbonisation investment prioritisation to improve emission profiles

- Supply diversification toward verified low-carbon suppliers

- Product portfolio optimisation for CBAM-inclusive market conditions

- Geographic market rebalancing to account for cost structure changes

Investment decisions require re-evaluation considering CBAM's impact on market access and competitive positioning. Companies with options for renewable energy access or production process improvements may find accelerated decarbonisation investments economically justified through CBAM avoidance benefits.

Market positioning strategies must account for the reality that European aluminum will carry permanent cost premiums relative to global benchmarks, requiring value proposition adjustments that emphasise quality, service, or sustainability benefits that justify higher pricing structures.

The next major ASX story will hit our subscribers first

What Policy Adjustments Could Minimise Industry Disruption?

Industry-Proposed Modifications

Industry representatives advocate for significant policy modifications to address CBAM's potential negative impacts on European aluminum sector competitiveness and employment. The primary recommendation involves implementation timeline extensions to allow adequate preparation for complex compliance requirements and market adjustments.

Key Policy Modification Proposals:

- Implementation timeline extension beyond January 1, 2026 to allow proper preparation

- ETS compensation mechanism preservation to prevent double impact scenarios

- Downstream scope expansion to include finished products and reduce competitive gaps

- Indirect emission treatment refinements to address supply chain complexity

The timeline extension proposal addresses industry concerns about inadequate preparation time for complex supply chain verification systems and cost modelling requirements. Three weeks' notice for implementation of such comprehensive policy changes appears insufficient for effective industry adaptation.

ETS free allowance preservation represents another critical modification that could prevent the double impact scenario where European producers face both CBAM costs and elevated energy expenses from allowance reductions. Industry analysis suggests that maintaining some level of ETS compensation would support policy objectives while preserving European industrial capacity.

Regulatory Uncertainty Resolution Priorities

Policy uncertainty resolution requires immediate attention to enable effective industry planning and investment decision-making. Current ambiguities regarding benchmark values, enforcement mechanisms, and country-specific default rates create planning challenges that may persist beyond implementation dates.

Critical Uncertainty Resolution Requirements:

- Benchmark value finalisation for accurate cost modelling

- Anti-circumvention enforcement mechanism clarification

- Country-specific default values transparency and accuracy

- Verification standard harmonisation across certification bodies

Benchmark rate finalisation appears essential for industry cost planning, as provisional rates based on 2017-2021 data may not reflect current production realities or technological improvements. Clear, final benchmarks would enable more accurate cost modelling and strategic planning across the supply chain.

For instance, enforcement mechanism clarity affects both legitimate compliance efforts and circumvention risk assessment. Companies require understanding of how authorities will monitor and enforce CBAM requirements to ensure compliance investments achieve intended outcomes while preventing unfair competition from non-compliant importers.

What Does CBAM Mean for Global Aluminium Investment Flows?

Capital Allocation Shift Patterns

CBAM implementation fundamentally alters global aluminum investment incentives by creating premium market access for low-carbon production facilities while penalising high-emission capacity. Additionally, considering decarbonisation mining benefits alongside the european aluminium industry impact of cbam extends beyond trade flows to capital allocation decisions that will shape industry structure for decades.

Investment Flow Redirection Patterns:

- European smelter modernisation versus closure economic evaluation

- Non-EU low-carbon capacity expansion incentives through market access premiums

- Recycling infrastructure development opportunities from secondary material advantages

- Renewable energy integration projects gaining economic justification

European facilities face critical investment decisions between modernisation expenditures to improve cost competitiveness and closure decisions that may prove economically rational under new cost structures. The five smelter closures since 2021 suggest that additional capacity reduction remains possible if CBAM costs compound existing competitive pressures.

Non-EU producers with access to renewable energy resources benefit from enhanced investment economics as CBAM creates market access premiums for verified low-carbon aluminum. This may accelerate capacity development in regions like Norway, Canada, and areas with abundant hydroelectric resources while disadvantaging investment in coal or gas-powered production regions.

Market Structure Evolution Forecast

Long-term market structure evolution under CBAM points toward geographic production redistribution that may concentrate low-carbon capacity in renewable energy-rich regions while potentially reducing overall European industrial participation. This structural shift carries implications for employment, tax revenues, and strategic industrial capacity retention.

Structural Evolution Predictions:

- Primary production geographic concentration in renewable energy regions

- Vertical integration acceleration for carbon footprint control

- Technology transfer expansion to maintain European market access

- Market consolidation around low-carbon production capabilities

Vertical integration strategies may become economically attractive as companies seek direct control over emission profiles and verification documentation. Downstream manufacturers may find investment in upstream capacity provides better cost control and supply security than market-based sourcing under CBAM conditions.

Technology transfer arrangements between European companies and non-EU producers could accelerate as market access requirements drive demand for decarbonisation expertise and renewable energy integration knowledge. This could create export opportunities for European technology while potentially supporting global emission reduction objectives.

Frequently Asked Questions About CBAM and European Aluminium

Implementation and Compliance FAQs

When do CBAM payments begin for aluminum imports?

CBAM financial obligations for aluminum imports begin January 1, 2026, marking the end of the transitional reporting-only period that commenced in October 2023. The definitive phase requires actual carbon cost payments rather than just emissions data reporting.

How are embedded emissions calculated for complex aluminum products?

Embedded emissions calculations encompass both direct production emissions (Scope 1) and electricity-related emissions (Scope 2) throughout the aluminum production process. Complex products require emissions data for each production stage, with verification through certified third-party assessment bodies.

What documentation is required for emission verification?

Verification documentation includes production process emissions data, energy consumption records, electricity source verification, and third-party certification body assessments. Suppliers without verified documentation face default emission value penalties that increase CBAM costs substantially.

Market Impact FAQs

Will CBAM increase aluminum prices across Europe?

Yes, CBAM implementation will increase European aluminum pricing through carbon cost integration into regional premiums. The cost increase magnitude depends on supplier emission profiles and verification status, with high-emission or unverified suppliers facing the largest cost impacts.

How will recycled aluminum be treated under CBAM?

Recycled aluminum treatment under CBAM creates competitive advantages as secondary production typically generates lower emissions than primary aluminum production. However, scrap metal sourcing and processing emissions require documentation and verification similar to primary production requirements.

What happens if suppliers cannot provide emission data?

Suppliers unable to provide verified emissions data face application of conservative default emission values that assume higher-carbon production processes. Consequently, these default values typically result in elevated CBAM costs that reduce competitive positioning relative to verified low-emission suppliers.

Conclusion: Navigating Europe's Carbon-Adjusted Aluminium Future

Strategic Imperatives for Market Participants

The european aluminium industry impact of cbam demands immediate strategic repositioning across all market participants, from primary producers through downstream manufacturers to end-use customers. Success requires proactive adaptation rather than reactive compliance as competitive dynamics undergo permanent transformation.

Critical Success Factors:

- Emission transparency development as competitive differentiation

- Supply chain resilience building through diversified sourcing strategies

- Policy engagement intensification for implementation refinement advocacy

- Cost structure adaptation to account for carbon pricing permanence

Emission transparency becomes a competitive weapon where companies with superior environmental performance and documentation capabilities gain market access advantages. Investment in verification systems and emission reduction technologies may provide returns through preferential pricing and market positioning.

Supply chain diversification strategies require immediate implementation to reduce dependency on high-carbon or unverified suppliers. Companies with flexible sourcing capabilities can optimise cost structures while maintaining supply security under changing regulatory conditions.

Long-term Industry Transformation Outlook

The long-term transformation outlook suggests fundamental reshaping of European aluminum industry structure, with potential concentration around low-carbon production capabilities and geographic redistribution of manufacturing capacity. Policy success depends on achieving genuine emission reductions rather than resource shuffling that weakens European industry without environmental benefits.

Transformation Timeline Projections:

- 2026-2028: Initial cost impact absorption and supply chain adaptation

- 2028-2030: Potential production capacity adjustments and facility optimisation

- 2030+: Market structure stabilisation around new competitive dynamics

Furthermore, decarbonisation acceleration timeline may benefit from CBAM incentives if policy implementation achieves intended emission reduction outcomes. However, the risk of production migration to higher-emission regions could undermine global environmental objectives while weakening European industrial capacity.

Global trade pattern evolution under carbon pricing regimes positions CBAM as a precedent for similar policies in other regions. Success or failure of European implementation will influence international carbon border adjustment adoption and global trade system transformation toward carbon-adjusted competition. Moreover, understanding tariffs and investment markets dynamics alongside CBAM impacts provides crucial context for assessing the broader implications of protectionist policies on global supply chains and industrial competitiveness.

Policy Disclaimer: This analysis reflects current policy proposals and industry perspectives as of late 2025. CBAM implementation details may change before definitive phase launch, and market impacts depend on enforcement mechanisms and industry adaptation strategies that remain under development.

Looking to Capitalise on Mining and Metals Market Shifts?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, helping investors navigate evolving market dynamics like CBAM's impact on global aluminium trade. Stay ahead of policy-driven shifts and identify actionable opportunities with instant notifications of major discoveries across over 30 commodities, simplified into clear, gold-equivalent metrics.