June 11, 2026

The Hidden Carbon Ledger: Why Aluminium Supply Chains Face a Reckoning Before 2028

Global manufacturing has long operated on the assumption that border taxes capture what crosses a frontier, not what was burned to create it. That assumption is being systematically dismantled. The EU Carbon Border Adjustment Mechanism represents a fundamental rethinking of trade-embedded carbon accountability, and for aluminium-intensive industries, the complexity runs far deeper than most procurement teams have yet appreciated.

The core challenge is not compliance with an import duty. It is the reconstruction of a carbon biography for every material that entered a factory before a finished product was shipped to Europe. This is the defining challenge of CBAM aluminium precursor emissions tracing, and understanding its mechanics is now a strategic imperative for any manufacturer with European market exposure.

When big ASX news breaks, our subscribers know first

Why the 2028 Expansion Is a Structural Break, Not an Incremental Update

During CBAM's initial operational phase, the compliance model was demanding but administratively navigable. Importers of unwrought primary aluminium, steel, cement, and fertilisers faced a relatively linear calculation: identify the emissions intensity of a specific metallurgical process, obtain or apply default values, and surrender the corresponding certificates.

The 2028 expansion fundamentally changes the geometry of this obligation. Rather than targeting simple upstream commodities, the mechanism extends to approximately 180 downstream product categories, with heavy machinery and specialised industrial equipment accounting for around 94% of these newly targeted goods. Commercial vehicle components, industrial robots, agricultural tractors, gearboxes, chassis structures, road wheels, and thermal management assemblies all fall within the expanded scope.

For aluminium, this matters enormously. The metal is not just a commodity input at the border of Europe. It is embedded, transformed, and assembled multiple times before it arrives inside a finished good. The CBAM framework does not exempt that embedded history. It requires its full accounting.

"The mechanism does not simply tax what a factory emits at its gates. It taxes the cumulative carbon history embedded in every material that entered those gates. For aluminium-intensive manufactured goods, this distinction fundamentally rewires compliance strategy."

What CBAM Precursor Emissions Tracing Actually Means

CBAM aluminium precursor emissions tracing refers to the process of identifying, quantifying, and verifying the greenhouse gas emissions embedded within upstream input materials — legally defined as precursors — that are incorporated into finished goods subject to EU carbon border adjustment obligations.

A precursor under EU CBAM regulatory architecture is any material that is physically incorporated into a finished good and whose production generated greenhouse gas emissions. For aluminium, this classification spans multiple product forms:

| CN Code Range | Product Category | CBAM Precursor Role |

|---|---|---|

| 7601 | Unwrought primary aluminium | Foundational precursor with highest embedded emissions |

| 7604 | Aluminium bars, rods, and profiles | Intermediate precursor from extrusion processes |

| 7606-7607 | Aluminium plates, sheets, strip, and foil | Rolled intermediate precursors |

| 7608-7610 | Tubes, pipes, and structural components | Fabricated precursors entering complex assemblies |

The classification system matters because each CN code category carries different typical emissions intensities, different production processes, and different documentation requirements. An OEM importing a complex piece of agricultural machinery cannot treat all aluminium content identically. Each component must be traced to its specific production origin.

The Carbon Leakage Problem That Made Downstream Expansion Inevitable

The original CBAM design contained a structural vulnerability that European policymakers recognised relatively quickly. If an EU-based automotive manufacturer bears the embedded cost of EU carbon allowances when purchasing domestic aluminium, but a foreign competitor can import a finished vehicle component without triggering any border adjustment, then carbon leakage is not prevented. It is displaced downstream.

This is the fundamental policy logic behind capturing complex manufactured goods within CBAM scope. The mechanism must follow the aluminium through its value chain transformations, not simply intercept it at the ingot stage. Furthermore, the broader push for electrification and decarbonisation across heavy industry is amplifying regulatory pressure on embedded carbon in traded goods.

Sectors Facing the Highest Precursor Tracing Burden

The aluminium-intensive sectors most exposed to the downstream expansion include:

- Commercial vehicle manufacturing — chassis, structural frames, and powertrain housings all incorporate primary aluminium precursors

- Agricultural machinery — tractors and harvesting equipment contain significant cast and extruded aluminium components

- Industrial robotics — lightweight structural frames rely heavily on extruded profile precursors

- Thermal management systems — radiators and heat exchangers incorporate rolled aluminium precursors from multiple production origins

- Gearbox and transmission assemblies — precision cast aluminium housings introduce deep-tier tracing requirements

Mapping the Aluminium Value Chain From Bauxite to Finished Component

Understanding where CBAM obligations begin requires a clear picture of the full aluminium production sequence:

Bauxite Extraction

↓

Alumina Refining (currently excluded from CBAM product scope)

↓

Primary Aluminium Smelting via Electrolysis (CN 7601) ← Highest direct emissions node

↓

Casting, Rolling, or Extrusion into Intermediate Forms (CN 7604–7607)

↓

Fabrication into Complex Components (Tier 3–4 supplier level)

↓

Final Assembly into Finished Manufactured Good (Tier 1 supplier or OEM)

↓

EU Import — CBAM Obligation Triggered

An important structural detail here is that alumina refining sits upstream of the primary smelting stage but has been excluded from the current CBAM product scope. This exclusion is deliberate and rests on a specific regulatory rationale that supply chain managers must understand when mapping their initial precursor exposure.

The regulatory boundary for aluminium begins at the smelting installation level, not at the refining stage. Alumina is treated as a processing intermediate rather than a separately tradeable CBAM good in the current framework. According to European Aluminium's position on CBAM, this boundary definition has significant implications for how the sector approaches compliance structuring.

The practical implication is that when an OEM imports a finished commercial vehicle component, the compliance obligation does not stretch back to the bauxite mine. It stretches to the specific smelting installation where primary aluminium was produced and to the specific casting or extrusion facility where it was transformed into the relevant intermediate precursor.

Why OEMs Must Trace Beyond Tier 1 Suppliers

This is where the compliance burden becomes operationally significant. When an OEM imports a complex finished product such as a commercial vehicle gearbox housing, the legal obligation does not permit reliance on a Tier 1 assembler's declaration alone. The framework requires tracing back through the production network to identify the Tier 3 extrusion facility and obtain verified emissions data from the Tier 4 smelting plant.

This transforms the purchasing function into something closer to a forensic audit of global metallurgical networks. The OEM becomes responsible for understanding not just what it bought and from whom, but where each material input was produced, by what process, using what energy source, and with what resulting emissions intensity.

The Two-Track Compliance System: Verified Data vs. Default Values

CBAM operates a two-track system for emissions data that creates a direct financial incentive for supply chain transparency.

| Data Source Type | Description | Risk Level | Compliance Quality |

|---|---|---|---|

| Installation-specific verified data | Actual emissions confirmed by accredited verifier at the production facility | Low | Highest quality and preferred by regulators |

| Supplier-declared data (unverified) | Emissions figures provided by supplier without third-party verification | Medium | Acceptable with documented caveats |

| EU default values | Regulatory fallback values applied when supplier data is unavailable | High | Compliant but typically financially penalising |

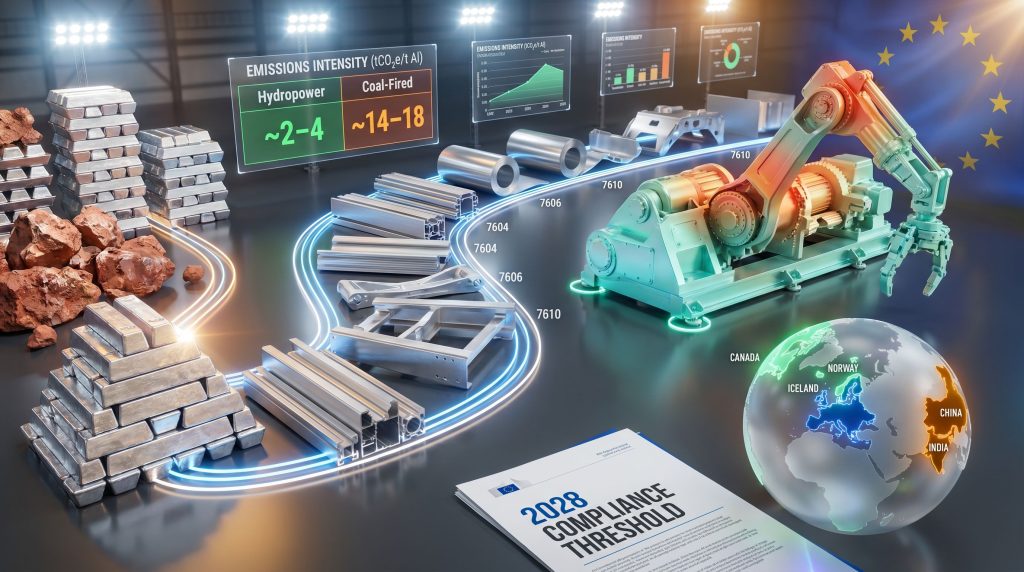

"Critical financial consideration: Relying on EU default emissions values rather than verified supplier-specific data typically results in higher reported embedded emissions, which directly increases CBAM certificate costs. For aluminium, where smelting energy sources vary dramatically between hydropower-intensive producers and coal-grid-dependent facilities, the difference between actual and default values can be commercially decisive."

For an aluminium smelter running on Icelandic hydropower, actual direct emissions per tonne of primary aluminium may fall in the range of 2 to 4 tCO2e. For a coal-grid-dependent Chinese smelter in northern provinces, the figure can reach 14 to 18 tCO2e or higher. If a supply chain manager cannot obtain verified data for the hydropower-sourced material and must apply a conservative default, they may be paying CBAM certificate costs on phantom emissions that do not actually exist in their supply chain.

What Installation-Level Reporting Requires From Upstream Smelters

Verified installation-specific data is not simply a number on a supplier invoice. The regulatory framework requires that emissions data be traceable to a specific production installation and confirmed by an accredited third-party verifier. The minimum data package that must be collected from each upstream facility includes:

- Production installation name, geographic location, and operator identity

- Production route classification, distinguishing primary electrolysis from secondary remelting

- Energy source mix used at the smelting or casting installation

- Direct Scope 1 emissions per tonne of output at the installation level

- Verification status and the identity of the accredited verifier, where applicable

- CN code classification of the specific aluminium output supplied

The accredited verifier role is new to many supply chain managers. These are third-party organisations accredited under EU standards to confirm that an installation's emissions reporting methodology is sound and that its declared figures are defensible under regulatory scrutiny.

The next major ASX story will hit our subscribers first

The Pre-Consumer Scrap Classification Gap

One of the least understood dimensions of current CBAM aluminium compliance is the treatment of pre-consumer scrap. Under the existing methodology, pre-consumer aluminium scrap is assigned zero embedded emissions. This classification rests on the logic that scrap is a residual material from prior production rather than a freshly produced primary input.

However, this creates a meaningful traceability gap. Imported remelted scrap can enter EU supply chains without triggering the same carbon cost obligations as primary aluminium, even when its actual production history is unverifiable. This is not a technical loophole in the sense of deliberate evasion. It is a genuine methodological ambiguity that the European Commission has identified and is actively reviewing.

The policy debate currently centres on two competing approaches:

- Single default carbon value applied uniformly to all secondary aluminium regardless of production route

- Differentiated primary and secondary route treatment that distinguishes between post-consumer scrap with traceable domestic origins and pre-consumer industrial scrap of uncertain provenance

If the European Commission moves toward reclassifying pre-consumer scrap as a standalone CBAM product with an assigned carbon value, the implications for recycled aluminium trade flows would be substantial. Operations that have structured their supply chains around zero-emissions secondary material would face a recalculation of their CBAM obligations.

"Importers using secondary aluminium should monitor this regulatory development closely. A reclassification of pre-consumer scrap is not confirmed, but the policy trajectory suggests the zero-emissions assumption should not be treated as permanently stable."

The Indirect Emissions Exclusion: A Strategic Watch Point

Current CBAM methodology for metals applies only to direct Scope 1 emissions, meaning the greenhouse gases physically released at the production installation. Indirect Scope 2 emissions, representing the carbon intensity of electricity consumed during production, are currently excluded from the metals framework.

For virtually any other industrial sector, this distinction would be relatively minor. For aluminium, it is structurally significant. Primary aluminium production via electrolysis is one of the most electricity-intensive industrial processes on earth. The energy cost of separating aluminium from alumina typically accounts for the majority of the total lifecycle carbon footprint of the metal when production occurs on a coal-dominated grid.

The exclusion of indirect emissions from the current CBAM metals framework means that the carbon cost of grid electricity consumed during electrolysis is not yet captured at the border. Consequently, if this exclusion is reversed in a future regulatory review, the competitive disadvantage for coal-powered smelting nations would increase substantially. The relative attractiveness of renewable energy in mining and smelting operations would intensify further as a result.

Geography as Carbon Destiny: Production Origin and CBAM Exposure

The decision of where to source primary aluminium precursors is increasingly a carbon cost decision, not merely a commercial one. The emissions intensity differential between production regions is dramatic:

| Production Region | Dominant Energy Source | Estimated Emissions Intensity (tCO2e/t Al) | CBAM Exposure Level |

|---|---|---|---|

| Middle East (Gulf producers) | Natural gas | ~8-10 | High |

| China (northern provinces) | Coal-fired grid | ~14-18 | Very High |

| Russia | Mixed hydro and thermal | ~4-8 | Medium to High |

| Canada, Norway, Iceland | Hydropower | ~2-4 | Low |

| India | Coal-dominated grid | ~15-19 | Very High |

These differentials translate directly into CBAM certificate cost gaps that compound across the volume of aluminium precursors embedded in finished goods. For a manufacturer importing a significant volume of aluminium-intensive machinery into Europe, the choice between a coal-grid Chinese precursor source and a hydropower Canadian or Norwegian source could represent a material cost differential per unit imported after 2028.

This is reshaping procurement strategy in ways that are only beginning to be understood at the corporate level. Supply chain origin decisions that were previously driven by unit price, logistics cost, and lead time now carry an additional dimension: verified carbon intensity and its CBAM certificate cost consequence. In addition, the rise of green metal production initiatives is beginning to influence how low-carbon aluminium sources are evaluated and certified globally.

A Step-by-Step Framework for Precursor Tracing Compliance

For OEMs and importers beginning to build their CBAM precursor tracing capability, the following workflow provides a structured starting point:

-

Product Decomposition — Identify all aluminium-containing components within the finished good and assign their relevant CN codes based on the specific aluminium form present in each component.

-

Supplier Tier Mapping — Chart the full supplier network from the Tier 1 assembler back to Tier 4 smelting installations, identifying the production country and specific facility for each node in the chain.

-

Emissions Data Collection — Request installation-specific emissions data from each upstream supplier, prioritising smelting and casting or extrusion stages where the highest emissions intensities are concentrated.

-

Data Verification Assessment — Determine whether supplier-provided data meets CBAM verification standards or whether EU default values must be applied due to absent or non-conforming supplier documentation.

-

Precursor Emissions Aggregation — Calculate the weighted embedded emissions per tonne of aluminium precursor for each component, taking into account the production route and verified energy source mix.

-

CBAM Declaration Preparation — Compile verified precursor emissions data into the required EU CBAM reporting format prior to importation, ensuring traceability documentation supports each declared figure. The official EU CBAM implementation guidance for installation operators provides further detail on these requirements.

-

Certificate Obligation Calculation — Determine the volume of CBAM certificates required based on total embedded emissions across all aluminium precursors contained in the finished good.

Technology Enablers for Precursor Data Management

The data management burden of multi-tier precursor tracing is not trivial. Emerging technology solutions addressing this challenge include:

- Digital supply chain platforms that create structured data flows from smelting installation to OEM compliance function

- Blockchain provenance tools that create immutable records of material origin and production process classification

- Emissions registries that store verified installation-level carbon data accessible to downstream customers during their declaration preparation

- Automated CN code classification systems that reduce manual categorisation error across complex bill-of-materials structures

None of these tools eliminates the underlying requirement for supplier cooperation and installation-level data access. They are enablers, not substitutes, for genuine supply chain transparency.

Frequently Asked Questions on CBAM Aluminium Precursor Compliance

What is a precursor under CBAM for aluminium products?

A precursor is any upstream aluminium input material, such as unwrought primary aluminium, extruded profiles, or rolled sheets, whose embedded production emissions must be identified and reported as part of the CBAM declaration for a finished manufactured good incorporating that material.

Does CBAM apply to aluminium components inside finished machinery?

Yes. Under the 2028 expansion of CBAM scope, complex downstream manufactured goods incorporating aluminium components become subject to border carbon adjustment. The embedded emissions of aluminium precursors within those goods must be traced and declared to EU customs authorities.

What happens if a supplier refuses to provide emissions data?

Where verified installation-specific data cannot be obtained, importers must apply EU-published default emissions values. These defaults are set conservatively and typically produce higher CBAM certificate costs than actual supplier-specific figures would generate for low-carbon production facilities.

Is recycled or secondary aluminium exempt from CBAM precursor tracing?

Not entirely. Pre-consumer scrap currently carries a zero-emissions classification under existing methodology, but this classification is under active policy review. Importers relying on secondary aluminium should treat this classification as provisional rather than permanent.

How far back in the supply chain must an importer trace aluminium precursor emissions?

The obligation extends to the production installation level, meaning the specific smelting or casting facility where the aluminium precursor was produced. Tier 1 supplier declarations alone are legally insufficient where upstream installation-level data is accessible.

Strategic Priorities Before the 2028 Enforcement Deadline

The compliance clock for the 2028 CBAM downstream expansion is already running. Manufacturers that treat precursor tracing as a late-stage administrative task rather than a strategic supply chain transformation will face both financial exposure and competitive disadvantage.

The priority actions for aluminium-intensive OEMs and importers include:

- Renegotiating supplier contracts to include mandatory emissions data disclosure clauses with specified verification standards and delivery timelines

- Conducting scenario modelling to quantify the CBAM certificate cost differential between high-carbon and low-carbon precursor sources across the full product portfolio

- Building internal carbon accounting capability capable of aggregating multi-tier precursor emissions data into compliant declaration formats

- Prioritising supply chain reorientation toward verified low-carbon aluminium sources in advance of 2028 enforcement, allowing procurement teams time to qualify new suppliers and establish data flows

"Manufacturers that establish verified, low-carbon aluminium supply chains before 2028 will not only reduce their CBAM certificate obligations. They will gain a structural pricing advantage over competitors still reliant on opaque, high-emissions precursor networks. The data mandate is simultaneously a compliance burden and a market differentiation opportunity."

The 80/20 Principle Applied to Precursor Compliance

A practical insight for organisations navigating the data collection challenge is that precursor emissions are not uniformly distributed across aluminium value chains. The primary smelting stage, CN code 7601, consistently accounts for the overwhelming majority of total embedded emissions across virtually every downstream aluminium product category.

This means that a compliance strategy that prioritises obtaining verified, installation-specific data for the smelting node in each precursor chain will capture the vast majority of total CBAM certificate exposure with a fraction of the total data collection effort. Verified data for casting and extrusion stages adds precision but contributes far less to total certificate cost than the smelting origin.

This 80/20 logic does not eliminate the need for full-chain tracing. EU regulators require documentation for all precursor nodes. However, it does provide a practical sequencing principle for organisations with limited compliance resources in the period leading up to 2028. Furthermore, the broader context of mining decarbonisation is reshaping the economic case for low-carbon upstream sourcing well beyond CBAM compliance alone.

The transformation underway is deeper than a regulatory compliance adjustment. OEMs are being restructured into carbon auditors of global metallurgical networks, and the aluminium supply chains that emerge from the 2028 transition will be fundamentally different from those that existed before it. Australia's emerging role in green metals leadership positions it as an increasingly relevant supplier of verified low-carbon aluminium precursors for exactly these new trade dynamics.

Want To Stay Ahead Of The Mineral Discoveries Driving The Green Metals Revolution?

As low-carbon aluminium sourcing becomes a strategic imperative ahead of the 2028 CBAM expansion, the race to secure verified, sustainable supply chains is reshaping global commodity markets — and Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly identifying actionable opportunities in the metals and materials sectors powering this transition. Explore historic examples of major mineral discoveries and their exceptional market returns, then begin your 14-day free trial to position yourself ahead of the market.