June 7, 2026

Central Asian rare earth processing capabilities have emerged as a critical component of global supply chain diversification strategies, representing a fundamental shift from decades of concentrated production models. The region's established industrial infrastructure, combined with strategic geographic positioning between major economies, creates unique opportunities for companies seeking alternatives to traditional processing pathways. The recent Lindian Resources Kazakhstan rare earth plant deal exemplifies this strategic shift in the critical minerals energy transition.

Kazakhstan's hydrometallurgical facilities offer compelling advantages through their integration of existing uranium processing expertise with rare earth applications, leveraging decades of metallurgical knowledge and established regulatory frameworks. This convergence of capabilities positions Central Asian operations as viable alternatives for Western manufacturers requiring secure supply chains.

How Does Kazakhstan's Processing Infrastructure Compare to Global Standards?

Central Asian Hydrometallurgical Capabilities Assessment

The SARECO facility in Stepnogorsk represents a sophisticated approach to rare earth processing, incorporating commissioned cracking, leaching, and precipitation circuits with comprehensive analytical capabilities. Originally developed through a strategic partnership between Kazatomprom and Sumitomo Corporation in 2010, this infrastructure demonstrates the successful transfer of Japanese processing technology to Central Asian operations.

Technical specifications reveal substantial processing capacity designed for modern environmental compliance standards. The facility's sulphuric acid bake and water leach methodology achieves exceptional recovery rates, with total rare earth extraction reaching 91-94% efficiency levels. Independent validation by the Australian Nuclear Science and Technology Organisation confirms these performance metrics across varied feedstock compositions.

The processing configuration eliminates traditional bottlenecks associated with radioactive material handling. Furthermore, uranium and thorium levels in final products consistently measure below detection limits, removing requirements for specialized radionuclide removal circuits and simplifying downstream logistics substantially.

Operational Benchmarking Against International Facilities

Processing Performance Metrics:

- Total Rare Earth Oxide Recovery: 91-94% extraction efficiency

- Neodymium-Praseodymium Recovery: 93-97% extraction rates

- Overall MREC Recovery: 85-90% total rare earth oxide content

- Annual Processing Capacity: 12,500 tonnes monazite concentrate throughput

- Infrastructure Advantages: Existing rail access, low-cost power availability, established workforce

Comparative analysis with Chinese processing facilities reveals competitive technical performance while maintaining Western-acceptable quality standards. In addition, the Central Asian location provides significant cost advantages through reduced labour expenses and favourable utility pricing, particularly electricity costs that remain substantially below Western industrial rates.

Environmental compliance frameworks align with international standards while benefiting from streamlined permitting processes. Moreover, Kazakhstan's industrial zone structure facilitates rapid operational scaling without extensive regulatory delays common in other jurisdictions.

When big ASX news breaks, our subscribers know first

What Are the Strategic Implications of Non-Chinese MREC Production?

Supply Chain Diversification Imperatives

Western defence and aerospace manufacturers increasingly prioritise supply chain security over purely cost-based procurement decisions. The concentration of rare earth processing capabilities within China creates strategic vulnerabilities that government agencies and major contractors actively seek to mitigate through geographic diversification.

Kazakhstan's position as the world's largest uranium producer demonstrates proven capability in complex mineral processing operations. Consequently, this operational heritage translates directly to rare earth applications, providing confidence in scaling production to meet industrial demand requirements.

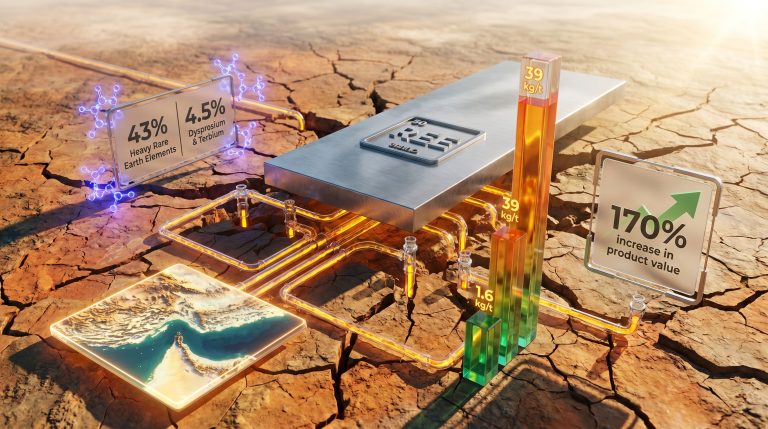

The Lindian Resources Kazakhstan rare earth plant deal exemplifies this strategic shift, positioning integrated production capabilities outside traditional Chinese supply chains. However, ongoing US‑China trade impacts continue to influence supply chain decisions across the sector. This transaction structure enables Western customers to access processed rare earth products without dependence on Chinese processing infrastructure.

Market Positioning for Integrated Producers

Vertical integration across concentrate production and downstream processing creates multiple value capture opportunities unavailable to single-stage operators. Companies controlling both mining and processing operations can optimise product allocation based on market conditions, customer preferences, and pricing dynamics.

The integration model provides enhanced negotiating leverage in offtake discussions by offering flexibility in product specification and delivery terms. For instance, customers benefit from direct engagement with processing operators rather than managing multiple supplier relationships across the value chain.

Strategic Advantages Include:

- Enhanced Margins: Value capture across multiple processing stages

- Customer Control: Direct engagement with end-users and specification development

- Supply Security: Reduced dependence on third-party processing arrangements

- Market Responsiveness: Rapid adjustment to demand fluctuations and pricing changes

How Do Acquisition Costs Compare Across Processing Development Models?

| Development Approach | Capital Investment Range | Timeline to Production | Risk Profile |

|---|---|---|---|

| Greenfield Construction | $500M – $1B+ | 5-8 years | High execution risk |

| Brownfield Acquisition | $15M – $50M | 1-2 years | Moderate operational risk |

| Joint Venture Partnership | $10M – $30M | 6-18 months | Shared risk profile |

| Technology Licensing | $5M – $20M | 2-3 years | Technology dependency |

Capital Efficiency Analysis

The acquisition approach demonstrates remarkable capital efficiency compared to greenfield development alternatives. Traditional rare earth processing facility construction requires substantial capital commitments, often exceeding $500 million for comprehensive operations, with development timelines spanning 5-8 years before commercial production begins.

Brownfield acquisitions present compelling alternatives through immediate access to operational infrastructure. The SARECO facility acquisition at $15 million total consideration represents approximately 97% cost reduction versus comparable greenfield construction, while accelerating production timelines by 3-6 years.

Financial Structure Benefits:

- Deferred Payment Terms: $12 million payable upon commercial production achievement

- Performance Alignment: Payment structure tied to operational success metrics

- Reduced Capital Risk: Immediate infrastructure access eliminates construction uncertainty

- Faster Revenue Generation: Operational capability within 12-24 months versus multi-year development

The transaction structure protects balance sheet flexibility while securing critical processing capabilities. Furthermore, this approach enables resource allocation toward feedstock development and customer engagement rather than infrastructure construction, aligning with broader industry consolidation trends.

What Role Does Kazakhstan Play in US-Central Asia Critical Mineral Strategy?

Bilateral Cooperation Framework Analysis

The November 2025 Memorandum of Understanding between the United States and Kazakhstan represents a formalisation of strategic cooperation frameworks that extend beyond traditional trade relationships. This bilateral agreement encompasses exploration, processing, and development initiatives across multiple critical mineral categories.

The C5+1 Critical Minerals Dialogue creates institutional mechanisms for sustained cooperation between US agencies and Central Asian governments. These frameworks facilitate technology transfer, investment protection, and regulatory harmonisation essential for large-scale mineral development projects.

US development finance institutions increasingly engage with Kazakhstan projects through direct lending and risk mitigation instruments. In addition, this financial infrastructure provides pathways to capital unavailable through traditional commercial channels, particularly for strategic mineral initiatives aligned with US supply chain objectives.

Regional Processing Hub Development

Kazakhstan's established uranium processing expertise creates natural synergies with rare earth operations. The country's metallurgical workforce possesses transferable skills applicable to complex hydrometallurgical processes, reducing training requirements and operational risk.

Industrial zone infrastructure facilitates integrated operations through established utility networks, transportation corridors, and regulatory frameworks. These advantages compress development timelines while reducing infrastructure investment requirements for new operations.

Government support mechanisms include streamlined permitting processes, foreign investment incentives, and bilateral trade facilitation measures. Moreover, Minister Yersaiyn Nagaspayev emphasised Kazakhstan's strategic positioning in global rare earth supply chains, specifically highlighting the integration of upstream feedstock with midstream processing capabilities as a pathway toward downstream permanent magnet manufacturing.

How Does Monazite Processing Technology Impact Production Economics?

Feedstock Quality Optimisation

Monazite concentrate quality significantly influences processing economics through recovery rates, reagent consumption, and final product specifications. Independent testwork validation reveals Kangankunde monazite contains approximately 55% total rare earth oxides, with neodymium and praseodymium comprising 18-20% of the rare earth composition.

These specifications enable exceptional processing performance through established sulphuric acid bake methodologies. The high-grade nature of the feedstock reduces reagent consumption per unit of final product while maximising recovery rates across critical elements.

Technical Performance Metrics:

- Feedstock Grade: 55% total rare earth oxide content

- Critical Elements: 18-20% neodymium-praseodymium composition

- Processing Recovery: 91-94% total extraction efficiency

- Final Product Quality: 85-90% recovery to mixed rare earth carbonate specification

The absence of significant uranium and thorium contamination eliminates specialised handling requirements while simplifying regulatory compliance. However, this characteristic reduces operational complexity and enhances customer acceptance, particularly for Western markets with stringent radioactive material restrictions.

By-Product Revenue Stream Analysis

Integrated processing operations generate valuable by-product streams that contribute meaningfully to project economics. Phosphate-based materials derived from monazite processing command established market prices across multiple applications.

By-Product Market Opportunities:

- Trisodium Phosphate: $300-700 per tonne market pricing

- NP(S) Fertiliser: $300-600 per tonne commercial value

- Local Market Integration: Agricultural sector demand for phosphate products

- Waste Stream Elimination: Complete utilisation of processing residues

Revenue diversification through by-product sales reduces dependence on rare earth pricing while improving overall project margins. Furthermore, local agricultural markets provide immediate offtake opportunities for phosphate-based fertilisers, creating additional revenue streams aligned with regional economic development objectives.

What Are the Investment Implications for Rare Earth Market Participants?

Sector Consolidation Trends

The rare earth processing sector demonstrates increasing consolidation as companies seek vertical integration advantages. Strategic acquisitions enable rapid capability expansion while avoiding lengthy development timelines and substantial capital commitments associated with greenfield projects.

Market participants recognise processing capabilities as strategic assets commanding premium valuations due to their scarcity outside China. Consequently, the limited number of operational facilities creates competitive advantages for companies controlling established infrastructure, particularly in light of volatile uranium market dynamics.

Investment Drivers Include:

- Supply Chain Control: Reduced dependence on third-party processing arrangements

- Margin Enhancement: Value capture across multiple production stages

- Customer Relationships: Direct engagement opportunities with end-users

- Strategic Positioning: Geographic diversification away from Chinese supply chains

Production Timeline and Market Impact Assessment

Commercial production targeting Q4 2026 positions early market entrants advantageously relative to competing development projects. The compressed timeline from acquisition to production creates immediate market presence while competitors continue multi-year development programs.

Annual processing capacity of 12,500 tonnes monazite concentrate translates to approximately 10,000-11,250 tonnes mixed rare earth carbonate production based on established recovery rates. This production volume represents meaningful supply addition to non-Chinese processing capacity.

Western market integration requires customer validation processes, quality certification, and supply chain logistics development. Furthermore, early engagement with potential customers accelerates market acceptance while building long-term commercial relationships essential for sustained success.

The next major ASX story will hit our subscribers first

How Do Environmental and Regulatory Factors Influence Processing Operations?

Kazakhstan Regulatory Environment

Kazakhstan's industrial regulatory framework incorporates modern environmental standards while maintaining operational flexibility essential for competitive processing operations. The established industrial zone structure provides clear guidelines for environmental compliance, waste management, and discharge standards.

Permitting processes benefit from government experience with complex metallurgical operations through the uranium sector. This regulatory familiarity reduces approval timelines while ensuring appropriate environmental oversight of processing activities.

Regulatory Advantages Include:

- Streamlined Permitting: Established frameworks for metallurgical operations

- Environmental Compliance: Modern standards aligned with international practices

- Operational Flexibility: Industrial zone benefits and utility infrastructure

- Government Support: Strategic mineral processing incentives and facilitation

International Standards Alignment

Western market acceptance requires compliance with stringent quality and traceability standards that extend beyond basic product specifications. Kazakhstan processing operations must demonstrate consistent quality control, environmental stewardship, and supply chain transparency.

Certification processes involve third-party validation of processing methods, environmental practices, and product quality consistency. These requirements create barriers to entry while protecting established operators meeting international standards.

The elimination of radioactive contamination in processed products significantly simplifies international logistics and regulatory compliance. Moreover, Western customers prioritise suppliers capable of providing products meeting strict nuclear material regulations without specialised handling requirements.

What Strategic Scenarios Could Impact Central Asian Rare Earth Processing?

Geopolitical Risk Assessment

Regional stability factors influence long-term operational viability and investment attractiveness for Central Asian processing operations. Kazakhstan's strategic relationships with major economies provide operational stability while maintaining independence from potential trade disruptions affecting other regions.

The country's neutral positioning in major power relationships creates advantages for Western companies seeking reliable supply chains. This geographic and political positioning reduces exposure to trade tensions while maintaining access to global markets.

Risk Mitigation Factors:

- Political Stability: Established government frameworks and international relationships

- Geographic Positioning: Strategic location between major economic zones

- Economic Diversification: Multiple sector development reducing dependence risks

- Infrastructure Development: Continued investment in industrial and transportation capabilities

Market Demand Projections

Permanent magnet demand growth drives rare earth consumption across multiple industrial sectors. Electric vehicle production expansion creates sustained demand for neodymium and praseodymium, the critical elements comprising 18-20% of processed monazite concentrate.

Defence and aerospace applications command premium pricing for secure supply sources, particularly materials processed outside Chinese facilities. However, this market segment prioritises supply security over cost optimisation, creating opportunities for non-Chinese processors to capture enhanced margins.

Wind turbine manufacturing represents another significant demand driver requiring substantial permanent magnet content. Consequently, the renewable energy sector's expansion creates sustained rare earth demand while aligning with environmental and energy security objectives across Western markets.

Kazakhstan's Position in the Global Rare Earth Value Chain

Strategic Value Proposition Summary

Kazakhstan's processing capabilities represent a convergence of established metallurgical expertise, strategic geographic positioning, and government support for critical mineral development. The integration of uranium processing experience with rare earth applications creates operational synergies unavailable in other jurisdictions.

Cost-effective acquisition of processing infrastructure eliminates traditional barriers to market entry while providing immediate operational capabilities. This approach contrasts favourably with multi-billion dollar greenfield development requirements that extend timelines and increase execution risk substantially.

The Lindian Resources Kazakhstan rare earth plant deal demonstrates the viability of this acquisition-based strategy while establishing precedents for future transactions. Furthermore, this aligns with broader mining innovation trends as Western companies seeking processing capabilities can leverage established infrastructure rather than developing new facilities from inception.

Future Development Pathways

Expansion opportunities exist through additional processing capacity development, technology transfer arrangements, and regional hub development initiatives. Kazakhstan's position as a uranium processing leader creates natural pathways for rare earth sector growth.

Technology transfer from established processing operators enables capability enhancement while reducing development risk. Strategic partnerships with Western technology providers facilitate knowledge transfer and operational optimisation across multiple facility locations.

Regional hub development leverages Kazakhstan's central position for processing feedstock from multiple Central Asian sources. This approach creates economies of scale while diversifying supply sources and reducing dependence on single mining operations.

The strategic framework positions Kazakhstan as a critical link in Western rare earth supply chains, providing secure processing capabilities outside Chinese control while maintaining competitive cost structures. According to industry analysis, this positioning creates sustainable competitive advantages for companies establishing operations within the region.

"The strategic acquisition of the SARECO facility represents a transformational opportunity for Western companies to secure rare earth processing capabilities outside traditional Chinese supply chains while leveraging established infrastructure and proven technology," according to industry analysts.

Investment Disclaimer: This analysis contains forward-looking statements and projections based on current market conditions. Rare earth processing operations involve substantial technical, operational, and market risks. Investors should conduct independent due diligence and seek professional advice before making investment decisions. Past performance and projected returns do not guarantee future results.

Ready to Capitalise on the Next Critical Minerals Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, including critical minerals and rare earth opportunities, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Explore historic examples of exceptional returns from major mineral discoveries on Discovery Alert's discoveries page and begin your 14-day free trial today to secure your market-leading advantage.