July 14, 2026

The Quiet Revolution Happening Inside Central Bank Vaults

Monetary history moves slowly until it doesn't. For decades, the architecture of global reserve management remained essentially unchanged: sovereign institutions held US Treasuries as their primary safe-haven asset, treated dollar liquidity as the default settlement mechanism, and regarded gold as a relic of a pre-Bretton Woods world. That consensus is fracturing, and central bank gold buying and US dollar debasement are now at the centre of that fracture, with the lines visible in the data.

Understanding why requires looking past daily price movements in gold and examining something far more consequential: the structural reallocation of sovereign wealth away from dollar-denominated debt and toward physical gold as a new tier of monetary collateral. This is not a speculative thesis. It is a quantifiable, ongoing process with compounding implications for investors, savers, and anyone holding paper currency as a store of value.

When big ASX news breaks, our subscribers know first

Defining the Problem: What Dollar Debasement Actually Means

The term dollar debasement is frequently misunderstood. It does not refer simply to a weaker dollar index (DXY) reading or short-term exchange rate fluctuations against major currencies. The dollar can strengthen against the euro or yen while simultaneously losing real purchasing power domestically. These are two entirely different phenomena.

Debasement, in its precise monetary definition, describes the erosion of purchasing power that results from debt monetisation: the process by which a government issues increasing quantities of currency or credit to service obligations it cannot retire through tax revenue or genuine economic growth alone. Declining trust in the US dollar as a reliable store of value is accelerating this dynamic at a structural level.

The most instructive benchmark for this process is not the Consumer Price Index, which has undergone substantial methodological revision since the Volcker era. A more structurally honest proxy is the compounding annual growth rate of US public debt, which has averaged approximately 8 to 9% per year over recent decades. Independent economists applying the original 1980s inflation measurement framework estimate that current US inflation, measured on the same scale used during the Volcker period, would register between 11 and 12%, compared to the officially reported 4.2%.

The Consumer Price Index has undergone multiple methodological revisions since the 1980s, including changes to substitution assumptions, geometric weighting, and hedonic quality adjustments. Applying the original Volcker-era measurement framework would place current US inflation between 11 and 12%, compared to the official 4.2% figure. The compounding annual growth rate of US public debt at 8 to 9% annually provides a third corroborating benchmark that tracks closely with these shadow methodology estimates.

The practical consequence of 8 to 10% real inflation compounding annually is severe. Dollar-denominated savings lose approximately 34 to 40% of purchasing power over a four-year period under those conditions, a mathematical reality that no official statistic obscures for those paying grocery bills, insurance premiums, or university tuition.

Three Inflation Benchmarks Compared

| Inflation Measure | Estimated Rate | Methodology |

|---|---|---|

| Official CPI (BLS) | ~4.2% | Current BLS methodology with substitution and hedonic adjustments |

| Shadow Stats methodology | ~11–12% | Original 1980s Volcker-era measurement framework |

| US debt CAGR (proxy) | ~8–9% | Compounding annual growth rate of federal debt as inflation correlate |

| Fed's own projection | ~3.6% | Federal Reserve internal forecast |

| Fed's stated target | 2.0% | FOMC policy objective, not achieved sustainably since 2020 |

The gap between the Fed's stated 2% inflation target and its own internal projection of 3.6% is itself revealing. The Federal Reserve has not sustainably achieved its own benchmark since 2020, and the distance between the official rate, the shadow methodology rate, and the debt-growth proxy has widened materially in recent years.

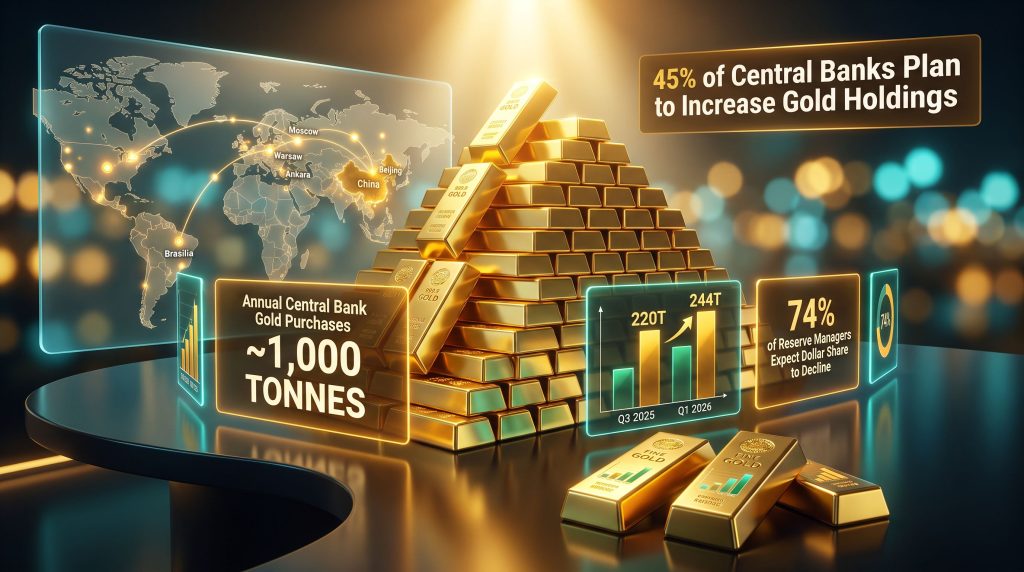

The Scale of Central Bank Gold Buying: What the Numbers Actually Show

Against this backdrop of currency credibility erosion, the behavior of sovereign reserve managers has shifted dramatically. Central bank gold buying and US dollar debasement have become inseparable narratives, with institutions globally averaging approximately 1,000 tonnes of gold purchases per year over the past four years — roughly double the pace of the preceding decade. This is not cyclical noise. It is a structural reallocation.

| Metric | Data Point |

|---|---|

| Annual average central bank gold buying (last 4 years) | ~1,000 tonnes |

| Q1 2026 estimated purchases | ~244 tonnes |

| Q3 2025 purchases | ~220 tonnes |

| Central banks planning to increase gold holdings (next 12 months) | 45% |

| Reserve managers expecting dollar share to decline | 74% |

| China consecutive months of gold accumulation (to mid-2026) | 19 months |

| Gold acquired by China by May 2026 | ~160 tonnes |

| Increase in central bank gold buying since 2022 | ~5x |

China's role in this story deserves particular attention. Nineteen consecutive months of reported gold accumulation through mid-2026, with approximately 160 tonnes acquired by May 2026 alone, represents a sustained institutional commitment that extends well beyond tactical portfolio adjustment. Furthermore, the World Gold Council's reported figures are widely considered conservative among market analysts with deep familiarity in the space.

Some credible voices in precious metals argue that actual accumulation may be 10 times higher than officially reported, given that significant sovereign buying occurs through channels that bypass conventional exchange tracking infrastructure. The scale of central bank gold demand consequently has far-reaching implications for global price discovery.

Why Physical Repatriation Matters

A parallel and underreported trend is the repatriation of physical gold from foreign custodians. Sovereign institutions that previously held gold at the Bank of England or Federal Reserve Bank of New York have begun relocating those reserves to domestic vaults. The strategic rationale is straightforward: reducing counterparty risk and eliminating exposure to sanctions in an era where financial infrastructure has been explicitly weaponised.

This is not theoretical. In 2022, the freezing of Russia's sovereign dollar reserves demonstrated to every non-allied central bank that dollar holdings carry political conditionality. The 5x increase in central bank gold buying since that event is a direct, measurable institutional response. Sovereign wealth managers in Brazil, Kazakhstan, Poland, Turkey, and across the broader Global South have systematically reallocated toward gold as a sanctions-neutral reserve asset in the years that followed.

The Geopolitical Architecture Behind De-Dollarisation

The 2022 sanctions decision functioned as a proof-of-concept for weaponised reserve infrastructure. It demonstrated, with finality, that dollar-denominated assets held in western custodian institutions can be immobilised by political decree. This is not an argument about whether that decision was justified. It is an observation about the information it transmitted to every sovereign treasury department on earth.

The result was a fundamental repricing of geopolitical risk attached to dollar reserve holdings, and gold, as a stateless, counterparty-free asset outside any sovereign's legal reach, became the natural beneficiary. As World Finance explores in detail, this structural shift reflects a broader recalibration of how sovereign institutions define monetary safety.

The BRICS Framework and Gold as Neutral Collateral

BRICS nations do not share sufficient mutual trust to support a common currency. India and China have overlapping territorial disputes. Brazil and Russia operate in entirely different economic ecosystems. What these nations share, however, is a common distrust of dollar dependency, and gold serves as politically neutral collateral for a new multilateral trading architecture.

This is not a gold-backed yuan or a formal BRICS currency. It is more accurately described as a gold-collateralised settlement framework, and the institutional infrastructure supporting it is advancing systematically. China's launch of a Hong Kong-Shanghai physical gold pricing exchange in July 2026 represents the most significant structural development in gold market architecture in decades.

The significance of this exchange is not that it will immediately reprice gold. Its significance is structural: physical settlement markets in Asia, operating with far less paper leverage than the COMEX or LBMA frameworks in New York and London, will gradually shift price discovery toward physical gold rather than paper claims. A former head of the Shanghai Gold Exchange stated publicly before western central bankers as early as 2014 that China would eventually set the gold price rather than the west. At the time, that statement was largely dismissed. It is substantially less dismissible today.

Gold as Tier-1 Collateral: An Institutional Threshold Has Been Crossed

One of the most consequential and underreported developments in global finance is the Bank for International Settlements' reclassification of gold as a Tier-1 zero-risk-weight asset under the Basel III regulatory framework. This is not a symbolic gesture. It places physical gold on equal regulatory footing with cash and sovereign debt for bank capital adequacy purposes. The Basel III gold impact represents formal institutional recognition of gold's monetary credibility.

The implication is that central banks and major commercial institutions now have a regulatory incentive to hold physical gold, not merely a portfolio preference for it. This is a qualitative threshold, not merely a quantitative one.

Morgan Stanley's 2024 recommendation of a 20% gold allocation to clients, from an institution historically dismissive of the asset, reflects the same underlying shift. When both the US Treasury and Wall Street's largest institutions begin publicly discussing gold's monetary credibility role, the asset has moved from alternative investment to mainstream institutional collateral.

When a former Federal Reserve nominee argues publicly for a gold-linked Treasury instrument, and a sitting Treasury Secretary discusses monetising the asset side of the sovereign balance sheet, the implicit admission is that the full faith and credit of the US government is no longer considered self-evidently sufficient as collateral. This is the quiet part being said out loud.

The Federal Reserve's Hidden Liquidity Architecture

Public commentary on Federal Reserve policy focuses almost exclusively on the federal funds rate and official balance sheet metrics. This creates a systematically distorted picture of actual monetary conditions.

The Fed's primary institutional function, often obscured by its public dual mandate of employment and price stability, is to provide liquidity to its member banking institutions. The Federal Reserve is constitutionally a bankers' bank, owned by private commercial banking corporations, and its operational priorities reflect that ownership structure.

Understanding this matters for gold investors because the real money supply trajectory is not fully captured by headline balance sheet figures. In the early months of new Fed leadership under Kevin Warsh, base money supply (M0) increased by an estimated $24 to $30 billion, a more expansionary posture than the final months of the preceding chairmanship, despite Warsh's publicly hawkish communications.

The Basel III Exemption Pathway

A further mechanism worth understanding: by relaxing Supplementary Leverage Ratio (SLR) requirements under Basel III, the Fed can effectively unlock approximately $90 billion in capital currently held as reserves by major commercial banks. When those institutions lever that capital at the standard 10 to 15x ratio typical of commercial banking operations, the resulting credit expansion represents over $1 trillion in new liquidity entering the system.

This is not visible in Fed balance sheet headline numbers. It operates through regulatory relief rather than direct asset purchases. But its inflationary and currency-debasing effects are functionally identical to conventional quantitative easing.

The pattern is consistent: hawkish public communication combined with structurally dovish operational mechanics. Treasury General Account drawdowns, short-end Treasury issuance, emergency facility activations, and now SLR relaxation all represent backdoor liquidity channels that expand credit without appearing on the official balance sheet in ways that generate public scrutiny.

The next major ASX story will hit our subscribers first

Bull Case vs. Bear Case: A Framework for Investors

The debasement thesis for gold is compelling, but intellectual honesty requires engaging seriously with the counterarguments.

| Dimension | Debasement Bull Case | Skeptical Counterview |

|---|---|---|

| Dollar trajectory | Structural decline in reserve share | Resilient due to unmatched liquidity depth |

| Treasury demand | Eroding trust, rising risk premium | Foreign holdings remain broadly stable |

| Gold's role | New monetary collateral anchor | Portfolio diversification tool |

| Inflation reality | 11–12% (shadow methodology) | 4.2% official, trending toward 2% target |

| Central bank buying | Structural regime change | Cyclical hedge against uncertainty |

| Timeline of dollar displacement | Accelerating, already underway | Generational, not imminent |

The skeptical case rests on several legitimate observations. The dollar index has stabilised since mid-2025. Foreign investors have not meaningfully offloaded US Treasury holdings in aggregate. The dollar retains unmatched settlement infrastructure, legal certainty, and institutional inertia that cannot be displaced in years, only in decades.

The bull case responds that these observations confuse pace with direction. A 74% majority of reserve managers surveyed by the World Gold Council expect the dollar's share of global reserves to decline. That expectation, held by the professionals managing the world's sovereign savings, is itself a directional signal independent of any short-term price action.

Gold has also surpassed US Treasuries as the top reserve asset for a growing number of central banks, a development that would have been considered implausible a decade ago. These are not goldbugs making this observation. These are sovereign reserve managers acting on it with real capital. The evolving role of gold in the monetary system increasingly reflects this institutional conviction.

Reading Equity Returns in Gold Terms

One of the most instructive analytical reframings available to investors is measuring portfolio returns not in nominal dollar terms but in gold terms. The S&P 500 has risen approximately 60% from its Q4 2021 peak through mid-2026. Measured in gold, however, the same portfolio has declined approximately 40% over the same period.

This distinction illustrates the core problem with using a debasing currency as the unit of measurement for wealth. Nominal gains in dollar terms can coexist with substantial real purchasing power losses when the measuring unit itself is losing value. This is not a manipulation of statistics. It is the arithmetic of debasement applied consistently.

What Gold Does Well, and What It Cannot Do

An honest assessment of gold as an anti-debasement asset requires acknowledging both its genuine strengths and its genuine limitations.

What gold does well:

- Stateless, counterparty-free store of value with no sovereign credit risk

- Physical gold held in allocated storage outside the banking system eliminates both banking system risk and sanctions exposure

- Multi-millennium track record as monetary collateral across diverse civilisations and monetary regimes

- Current institutional momentum from central bank buying, Basel III reclassification, and Wall Street allocation upgrades

What gold cannot do:

- Gold generates no yield, dividends, or cash flow, creating real opportunity cost in high-rate environments

- Price volatility is real and can be severe, with multi-year drawdowns occurring even within secular bull markets

- Physical storage, insurance, and custody costs reduce net returns relative to paper alternatives

- Gold does not directly address the political or structural causes of currency debasement

Alternative Anti-Debasement Asset Classes

| Asset Class | Inflation Hedge Quality | Liquidity | Counterparty Risk | Yield |

|---|---|---|---|---|

| Physical gold | High | Moderate | None | None |

| Gold ETFs | High | High | Moderate (custodian) | None |

| Equities (broad) | Moderate | High | Low | Yes |

| Real estate | High | Low | Low | Yes |

| Bitcoin | Speculative | High | Low | None |

| TIPS (inflation-linked bonds) | Moderate | High | Sovereign | Yes |

Navigating Volatility: The Secular Bull Market Framework

For investors with genuine conviction in the structural drivers of gold appreciation, the most dangerous moment is not when the thesis is wrong. It is when the thesis is right but price action is temporarily adverse, generating emotional pressure to exit.

The 1970s bull market in gold provides the most instructive historical parallel. Gold rose from $35 to $850 across that decade — an extraordinary appreciation. However, that journey included at least five corrections exceeding 20%, and a catastrophic midcycle drawdown between 1974 and 1976 in which gold lost approximately 50% of its value before ultimately rising eight times from that trough to the eventual peak.

Investors who understood the structural drivers of that bull market — sustained negative real interest rates, dollar debasement through Nixon's closing of the gold window, and accelerating debt monetisation — were positioned to maintain conviction through the drawdown. Those who did not understand the structure exited at the worst possible moment.

The present period offers a structurally stronger fundamental case than the 1970s did. Absolute debt levels are higher, global interconnection is deeper, institutional participation in gold is more sophisticated, and central bank buying and US dollar debasement are occurring simultaneously at historically unprecedented scale. The 1970s analog is instructive for understanding the character of volatility within secular bull markets. It understates the present structural argument for gold. Research from UNSW Business School further supports this view, highlighting how the surge in central bank gold reserves is underpinning this structural repricing.

Frequently Asked Questions

Why are central banks buying so much gold right now?

Central banks are increasing gold allocations primarily to reduce dependence on US dollar reserves, hedge against the risk of financial sanctions, and respond to declining confidence in US Treasury debt as risk-free collateral. The 2022 freezing of Russian sovereign dollar reserves accelerated this trend significantly, with central bank gold buying increasing approximately 5x since that event.

Does central bank gold buying signal a dollar collapse?

Not necessarily. Most analysts distinguish between diversification — reducing dollar concentration — and abandonment, which means exiting dollar assets entirely. The dollar retains dominant reserve currency status due to unmatched liquidity, settlement infrastructure, and institutional inertia. However, its share of global reserves is expected to decline, which represents a structural headwind rather than an imminent collapse.

What is the difference between paper gold and physical gold?

Paper gold, including ETFs, futures contracts, and unallocated accounts, represents a claim on gold without direct ownership of the physical metal. Physical gold held in allocated, segregated storage outside the banking system carries no counterparty risk. This distinction becomes particularly important in systemic stress scenarios, where paper claims may not be redeemable at face value.

How does money supply growth affect gold prices?

Expanding money supply, particularly M0 base money growth, increases the total quantity of currency units competing for a fixed or slowly growing supply of gold. Over multi-year periods, this relationship has historically supported gold price appreciation, though short-term price action is influenced by many additional factors including real interest rates, risk sentiment, and positioning dynamics.

Is a gold-backed US Treasury bond actually possible?

Proposals for gold-linked long-dated Treasury instruments have been publicly discussed by former Federal Reserve nominees and senior Treasury officials. While no legislation has been enacted, the fact that such proposals are being seriously debated at the highest levels of US economic policymaking signals that policymakers recognise a need to enhance the credibility of US sovereign debt. This is an implicit acknowledgement that the dollar's reserve status requires active reinforcement in ways considered unnecessary even five years ago.

The Direction of the Hockey Puck

The convergence of evidence across central bank behaviour, regulatory frameworks, geopolitical realignment, and monetary mechanics points consistently in one direction. The debate is no longer whether gold has monetary relevance. It is how quickly that relevance becomes formally institutionalised in the global financial architecture.

For individual investors, the actionable insight is not predicting short-term gold prices, which are influenced by too many variables for reliable near-term forecasting. The more important insight is understanding the purchasing power erosion occurring continuously in dollar-denominated savings, and making deliberate, informed allocation decisions accordingly.

The underlying structural forces — debt accumulation, money supply expansion, institutional gold adoption, and geopolitical reserve reallocation — have not reversed. Only the short-term price expression has fluctuated. Those who understand the direction of those forces are better positioned to maintain conviction through the volatility that any secular bull market inevitably produces.

This article is intended for educational and informational purposes only and does not constitute financial or investment advice. All forecasts, projections, and analytical frameworks referenced involve inherent uncertainty. Past performance of any asset class, including gold, does not guarantee future results. Readers should conduct their own due diligence and consult qualified financial professionals before making investment decisions.

Want to Identify the Next Major Mineral Discovery Before the Broader Market Does?

While sovereign institutions are quietly reallocating toward gold at historically unprecedented scale, Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant alerts on significant mineral discoveries — turning complex data across 30-plus commodities into clear, actionable insights for both short-term traders and long-term investors. Explore historic discoveries and their exceptional returns, then begin your 14-day free trial to position yourself ahead of the market.