July 8, 2026

The Quiet Dethroning: Why Sovereign Wealth Is Migrating Away From the Dollar

Monetary history rarely announces its turning points in advance. The collapse of the Bretton Woods system in 1971, the rise of the petrodollar, the post-2008 era of quantitative easing: each transformation looked incremental until it suddenly did not. Today, a similarly structural shift is underway, documented not through market speculation but through the survey responses of the very institutions responsible for managing the world's sovereign wealth. Central banks swapping dollars for gold is no longer a fringe narrative or emerging market eccentricity. It is becoming the dominant strategy in global reserve management.

When big ASX news breaks, our subscribers know first

Two Independent Surveys, One Unmistakable Conclusion

What makes the current trend particularly credible is that two entirely separate institutional research bodies have arrived at the same findings through independent methodologies. The Official Monetary and Financial Institutions Forum (OMFIF) and the World Gold Council both published 2026 surveys documenting a structural reorientation in how central banks allocate reserves, and the data points in the same direction across every key metric.

The convergence of findings from unrelated surveys is not a coincidence. It reflects a genuine paradigm shift in institutional thinking about what constitutes a safe, neutral, and durable reserve asset. The headline figures paint a compelling picture:

| Metric | Finding |

|---|---|

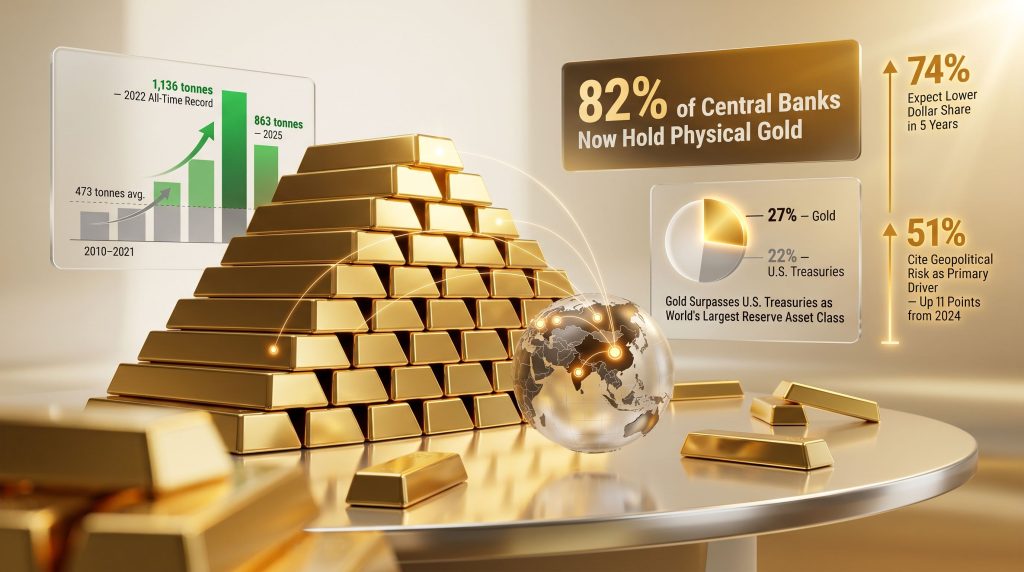

| Central banks currently holding physical gold | 82% (up from 71% one year prior) |

| Central banks planning to increase gold allocations within 1-2 years | 30% |

| Respondents expecting their dollar reserve share to fall within 5 years | 74% |

| Reserve managers citing geopolitical risk as a primary reason to hold gold | 51% (up 11 percentage points from 2024) |

| Central banks describing the world as moving toward a multipolar monetary system | 79% |

The jump in physical gold holders from 71% to 82% within a single year represents an extraordinary acceleration. Institutional reserve allocation decisions typically move at glacial speed, governed by legislation, risk frameworks, and political constraints. A shift of this magnitude within twelve months signals something more than portfolio rebalancing. It signals a philosophical recalibration of what sovereign wealth management actually means in the current era.

Understanding Reserve Currency Mechanics: Why the Dollar's Role Matters So Much

To fully grasp the significance of central banks swapping dollars for gold, it helps to understand the structural architecture that makes the dollar's reserve status so economically consequential for the United States itself. Furthermore, understanding gold in the monetary system provides essential context for interpreting the scale of this shift.

The dollar's role as the world's primary reserve currency creates what economists describe as a self-reinforcing demand loop. Because global trade in commodities, energy, and financial instruments is predominantly denominated in dollars, every nation on earth requires a substantial stock of dollar-denominated assets to conduct international commerce and service external obligations. This persistent structural demand acts as an enormous, ongoing subsidy to the American government.

The mechanism works as follows:

- Foreign central banks accumulate dollar reserves to facilitate trade and maintain currency stability

- These institutions park reserves predominantly in U.S. Treasury securities, providing low-cost financing to the federal government

- This sustained foreign demand allows Washington to run persistent fiscal deficits without triggering the borrowing cost penalties that would discipline any other sovereign borrower

- The Federal Reserve can expand the money supply more aggressively than would otherwise be possible, because excess dollars are absorbed by global demand rather than immediately circulating domestically

- Any erosion of this foreign demand tightens each of the above links simultaneously

The French economist and Finance Minister Valéry Giscard d'Estaing famously described this arrangement as the United States' "exorbitant privilege." The Congressional Budget Office projects U.S. federal debt to exceed $50 trillion by 2034, a trajectory built on the assumption that foreign appetite for dollar assets remains robust. Even a single-digit percentage reduction in that appetite, spread across more than 100 central banks, would represent hundreds of billions in reduced Treasury demand annually.

Gold's Historic Ascent to the Top of the Reserve Hierarchy

The most structurally significant development of 2026 was the confirmation by the European Central Bank that gold had surpassed U.S. Treasuries as the world's largest single reserve asset class globally. Gold now represents approximately 27% of aggregate global reserve holdings, compared to U.S. Treasuries at 22%. This is the first time in the post-Bretton Woods era that any asset has displaced U.S. government debt from the top position in global reserves.

Central bank gold accumulation has followed a dramatic upward trajectory over the past several years:

| Period | Central Bank Net Gold Purchases |

|---|---|

| 2010-2021 Annual Average | 473 tonnes |

| 2022 (All-Time Record) | 1,136 tonnes |

| 2023 | 1,037 tonnes |

| 2025 | 863 tonnes |

| H1 2025 Emerging Market Purchases | 410 tonnes (24% above 5-year average) |

The 2025 figure of 863 tonnes was the fourth-largest annual accumulation on record, despite representing a 21% decline from the prior year. Critically, it remains approximately 82% above the pre-2022 annual average, confirming that elevated accumulation is not a one-year anomaly but a sustained structural condition. According to recent analysis from OMFIF, central banks are systematically turning back to gold as a cornerstone reserve asset.

Historical Context: The 2022 record of 1,136 tonnes represented the highest level of net central bank gold purchases since tracking began in 1950, including the period before the end of the gold standard in August 1971. The current cycle has permanently reset expectations about baseline central bank demand.

Why Physical Gold Rather Than Alternative Currencies

A critical nuance in understanding this trend is recognising what gold is not competing with. Neither the Chinese yuan nor the euro is positioned to absorb the reallocation away from the dollar. Nearly all OMFIF survey respondents acknowledged that yuan holdings offer diversification, and two-thirds noted the euro's growing attractiveness in trade settlement. Yet neither currency is being accumulated as a primary reserve substitute.

The reasons are structural rather than political:

- Yuan limitations: China's capital controls restrict the free flow of yuan-denominated assets across borders, fundamentally undermining the liquidity characteristics required for large-scale reserve management. Additionally, any asset denominated in yuan carries implicit exposure to Beijing's policy decisions.

- Euro constraints: While the eurozone is a large, sophisticated economy, the euro remains a fiat currency subject to European Central Bank monetary policy and the fiscal dynamics of 20 sovereign members. It cannot offer the political neutrality that reserve managers increasingly demand.

- Gold's unique properties: Physical gold carries no issuing sovereign, cannot be sanctioned or frozen by a foreign government, has no counterparty default risk, and maintains a well-established inverse relationship with dollar purchasing power. These characteristics are irreplaceable by any fiat currency.

The Geopolitical Catalyst: When Dollar Assets Became a Liability

The single most important event reshaping central bank attitudes toward dollar-denominated reserves was the freezing of approximately $300 billion in Russian sovereign foreign exchange reserves following the 2022 invasion of Ukraine. For reserve managers in non-Western nations, this demonstrated something previously theoretical: dollar assets held in Western financial institutions could be rendered inaccessible through political decision, regardless of their technical ownership.

The survey data captures the institutional response precisely. 51% of reserve managers now cite geopolitical risk protection as a primary motivation for gold accumulation, an increase of 11 percentage points in a single year. This is not abstract concern about a hypothetical future scenario. It is a rational institutional response to an observed precedent, with many nations consequently losing trust in the dollar as a neutral reserve asset.

OMFIF head of research Andrea Correa stated that reserve managers remain strongly committed to gold despite rising prices, indicating that demand is driven by strategic necessity rather than price opportunism. This is a fundamentally different demand dynamic than retail gold investment, where price sensitivity typically moderates buying interest.

The growing preference for gold over government bonds also reflects deepening concern about sovereign debt sustainability. When asked about long-term asset preferences extending to a 10-year horizon, central banks now favour corporate bonds, then gold, then public equities. Government bonds, which once formed the unquestioned foundation of reserve portfolio construction, no longer feature in the top-tier long-term allocation preferences of most surveyed institutions. The structural driver is unmistakable: unprecedented levels of sovereign debt accumulation across major economies have eroded the creditworthiness logic that once made government bonds categorically safe.

De-Dollarization Scenarios: A Risk Framework for What Comes Next

The pace and scale of de-dollarization will determine whether the transition is economically manageable or destabilising. Three distinct scenarios present themselves:

Scenario 1: Gradual Rebalancing (Base Case)

The dollar retains reserve currency primacy but with a declining share. Gold stabilises at 25-30% of global reserve holdings. U.S. borrowing costs rise modestly, inflation remains elevated but contained. This transition unfolds over 5-10 years with sufficient time for adjustment.

Scenario 2: Accelerated De-Dollarization (Stress Case)

A triggering event — such as a U.S. debt ceiling crisis, a sovereign credit rating downgrade, or an expansion of financial sanctions against additional countries — accelerates reserve reallocation. The dollar's share of global reserves, currently approximately 58% per IMF COFER data, falls toward 40%. Gold demand intensifies, driving further price appreciation that reinforces the accumulation incentive.

Scenario 3: Systemic Rupture (Tail Risk)

A self-reinforcing depreciation cycle emerges as reduced foreign demand for dollars weakens the exchange rate, raising import costs, feeding domestic inflation, and further undermining confidence in dollar-denominated assets. The historical analogy is the collapse of Bretton Woods in 1971, though that event occurred within a structured multilateral framework. A contemporary rupture would likely unfold without an equivalent institutional safety net.

Investor Note: The scenarios above represent analytical frameworks for understanding potential outcomes, not investment recommendations. Forecasts involving sovereign debt dynamics, currency valuations, and geopolitical developments carry inherent uncertainty. Readers should seek qualified financial advice before making investment decisions based on macroeconomic trend analysis.

The next major ASX story will hit our subscribers first

What This Means for Household Purchasing Power

The decisions being made in central bank reserve committees have direct, if delayed, consequences for ordinary consumers. The transmission mechanism from sovereign reserve shifts to household prices operates through several channels:

- Reduced foreign demand for dollars weakens the exchange rate

- A weaker dollar raises the cost of imported goods, energy, and commodities denominated in other currencies

- Rising import costs spread through supply chains, contributing to broader consumer price inflation

- Households in import-dependent economies experience the erosion of purchasing power most acutely

- In severe scenarios, a self-reinforcing cycle of currency depreciation and inflationary expectation can become difficult to contain through conventional monetary policy

The sustained elevation of gold prices, even as central bank gold reserves continue to grow at historically high price levels, provides a revealing signal. Institutional buyers are not purchasing gold because they expect a short-term price gain. They are purchasing gold because they assess the long-term trajectory of fiat currency purchasing power — particularly the dollar's — as structurally compromised. This is the behaviour of institutions managing multi-generational balance sheets, not speculative traders seeking quick returns.

Moreover, central banks influencing gold prices at this scale creates a demand floor that fundamentally alters the gold market's dynamics. As Brookings Institution research confirms, the strategic importance of central bank gold holdings has grown significantly in the modern era, reinforcing why this trend warrants serious attention.

Frequently Asked Questions

Are central banks abandoning the U.S. dollar entirely?

No. Survey data from both OMFIF and the World Gold Council confirms the dollar retains its position as the world's primary reserve currency. However, 74% of respondents expect their dollar allocation to be lower within five years, and more central banks plan to reduce dollar holdings than increase them over the next year. The shift is one of strategic rebalancing, not wholesale abandonment.

Why can't the Chinese yuan replace the dollar as the reserve currency of choice?

Capital controls limit the yuan's usability as a reserve asset. A truly global reserve currency must be freely convertible and available in sufficient depth across global markets. The yuan's restricted convertibility, combined with political concerns about exposure to Beijing's policy decisions, means it cannot serve as a neutral substitute for the dollar regardless of China's economic size.

How significant is 863 tonnes of annual central bank gold purchases?

The 2025 figure of 863 tonnes sits approximately 82% above the 2010-2021 annual average of 473 tonnes. While below the 2022 record, this level of sustained accumulation across multiple years is without modern precedent and represents a structural shift in how sovereign institutions value gold relative to paper assets.

What is the relationship between U.S. sovereign debt and gold demand?

Escalating sovereign debt levels across major economies, particularly the United States where the Congressional Budget Office projects federal debt exceeding $50 trillion by 2034, undermine confidence in government bonds as long-term stores of value. As the creditworthiness logic supporting bond markets weakens, gold becomes more attractive as an asset with no issuing sovereign and no default risk.

Is gold's current price level sustainable given central bank buying?

OMFIF research indicates reserve managers continue accumulating gold despite rising prices, characterising it as a strategic necessity rather than a price-sensitive trade. This structural demand floor is qualitatively different from retail or speculative gold demand. Whether current prices are sustainable depends on factors including the pace of de-dollarization, geopolitical developments, and monetary policy trajectories across major economies.

Key Takeaways

The data from 2025 and 2026 institutional surveys tells a coherent and internally consistent story about where global reserve management is heading. In essence, central banks swapping dollars for gold reflects a broad, multi-year institutional realignment with profound implications for global finance:

- 82% of central banks now hold physical gold, up from 71% the prior year — the fastest single-year adoption increase in the survey's history

- Gold has surpassed U.S. Treasuries as the world's largest reserve asset class for the first time in the post-Bretton Woods era

- 74% of reserve managers expect to hold a smaller dollar allocation within five years

- The primary driver is geopolitical risk protection, not yield optimisation or speculative positioning

- Central bank long-term asset preferences have structurally shifted away from government bonds toward gold, corporate bonds, and equities

- Neither the yuan nor the euro is absorbing the reallocation: gold is the destination of choice

- The consequences for U.S. fiscal sustainability and household purchasing power depend critically on whether this transition remains gradual or accelerates through a triggering shock

The institutional consensus could not be clearer. When the managers of sovereign balance sheets across nearly 80 countries begin simultaneously reordering their reserve hierarchies — placing a metal with no yield above the bonds of the world's largest economy — it warrants serious attention from every investor, policymaker, and citizen whose financial wellbeing is denominated in U.S. dollars.

Want to Know Which ASX Mining Companies Could Benefit From the Surge in Gold Demand?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries — including gold — and translating complex data into actionable investment insights before the broader market catches on. Explore historic examples of major discovery returns and begin your 14-day free trial at Discovery Alert to position yourself ahead of the next significant find.