June 4, 2026

When Commodity Cycles Bite: Understanding the Structural Forces Behind Aluminium Stock Volatility

Commodity markets have a long history of punishing equity investors during periods of cost inflation, even when underlying business fundamentals remain intact. The aluminium sector is particularly exposed to this dynamic because of its unique position at the intersection of energy-intensive production, globally traded raw materials, and cyclically sensitive downstream demand. When these three variables move against producers simultaneously, even well-managed, vertically integrated companies can see their share prices disconnect sharply from their operational performance.

This tension between short-term market pessimism and long-term structural strength sits at the heart of the pressure currently weighing on Chinese aluminium producers. Understanding why Chalco shares fall amid pressure on aluminium requires looking beyond a single trading session and examining the layered forces that drive non-ferrous metals equities in periods of macro uncertainty.

When big ASX news breaks, our subscribers know first

What Is Chalco and Why Does Its Share Price Matter to Global Aluminium Markets?

A Fully Integrated Producer Across the Entire Value Chain

Aluminium Corporation of China Limited, known internationally as Chalco, is headquartered in Beijing and operates one of the most comprehensive aluminium production networks in the world. Its activities span the complete value chain, from bauxite extraction and alumina refining through to primary aluminium smelting and downstream product manufacturing. This level of vertical integration is relatively rare in global metals production, where most companies occupy one or two segments rather than the entire spectrum.

The significance of this structure cannot be overstated. By controlling inputs at every stage, Chalco is able to reduce its exposure to the kind of raw material price volatility that can devastate the margins of non-integrated producers during commodity price cycles. When bauxite costs rise or alumina supply tightens, an integrated producer can absorb these pressures internally rather than passing them through to a higher cost base.

The company generates the majority of its revenue from alumina refining and primary aluminium sales, with additional contributions from energy operations and trading activities. Alumina remains a critical earnings pillar given China's dominant position in global refining capacity, a position that has only grown more significant as energy transition demand has expanded in recent years.

Dual-Listed Structure and Its Importance for International Capital

Chalco trades on two major exchanges simultaneously, listed as 2600.HK on the Hong Kong Stock Exchange and 601600.SS on the Shanghai Stock Exchange. This dual-listed structure has meaningful implications for how the company is priced and who can access it.

For international portfolio managers, the Hong Kong-listed shares represent one of the most direct and liquid ways to gain exposure to China's aluminium industry without the access constraints that apply to mainland-listed A-shares. Because of this, price movements in Chalco's shares often serve as a real-time barometer for global investor sentiment toward Chinese industrial commodities more broadly. When the stock falls sharply, it more commonly reflects a repricing of risk across the entire non-ferrous metals complex.

For investors seeking China commodity cycle exposure, Chalco's Hong Kong-listed shares function as a bellwether for broader sentiment shifts across the non-ferrous metals sector, making its trading patterns a useful leading indicator of institutional positioning.

How Significant Was the May 2026 Share Price Decline?

Breaking Down the Trading Session Data

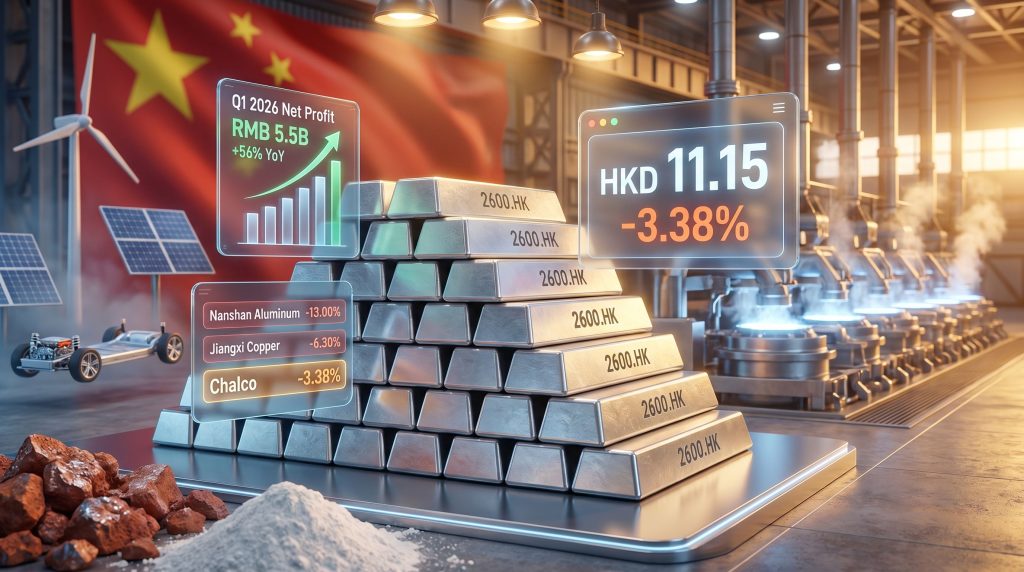

On Monday, 11 May 2026, Chalco's shares on the Hong Kong Stock Exchange closed at HKD 11.15 (USD 1.43), down from a previous close of HKD 11.54 (USD 1.48), representing a decline of 3.38% for the session. According to market data published by StockInvest.us on 12 May 2026, the stock moved through a notably volatile trading range during the session, with intraday selling pressure reaching as high as 5.05% at peak intensity before recovering partially into the close.

A detail worth noting is that despite the price pullback, technical indicators derived from the stock's moving averages remained in positive territory. This divergence between short-term price action and medium-term technical momentum is a pattern that frequently appears during sector-wide commodity selloffs, where broad risk-off flows override company-specific signals.

Peer Comparison: Chalco's Decline in Sector Context

Examining Chalco's performance against its Hong Kong-listed sector peers reveals an important nuance: the decline, while meaningful, was comparatively contained relative to several other metals and mining stocks experiencing pressure during the same period.

| Company | Approximate Decline | Exchange |

|---|---|---|

| Chalco (2600.HK) | -3.38% to -5.05% | Hong Kong |

| China Hongqiao | -4.00% | Hong Kong |

| Nanshan Aluminum International | -13.00%+ | Hong Kong |

| Chuangxin Industrial | ~-6.00% | Hong Kong |

| Jiangxi Copper | -6.30% | Hong Kong |

| Minmetals Resources | ~-6.00% | Hong Kong |

| Rusal | -1.00%+ | Hong Kong |

The dispersion within this peer group is instructive. Nanshan Aluminum International's decline exceeding 13% against Chalco's 3.38% drop suggests that investors were actively differentiating between producers on the basis of business model resilience. Integrated operations with diversified revenue streams appear to have offered some degree of insulation against the most severe selling pressure, while companies with narrower operational profiles bore a disproportionate share of the drawdown.

The contrast between Chalco's moderate decline and the double-digit falls seen at some peers indicates that vertical integration may be functioning as a partial shock absorber during sector-wide volatility, even when it cannot fully neutralise macro-driven headwinds.

What Is Driving the Pressure on Aluminium Producers?

Energy Inflation as the Primary Structural Headwind

Aluminium smelting is one of the most electricity-intensive industrial processes in existence. The electrolytic reduction process used to convert alumina into primary aluminium consumes enormous quantities of electrical energy, making power costs the single largest variable in a smelter's operating cost structure. Industry estimates consistently place energy costs at between 30% and 40% of total primary aluminium production costs, though this proportion can rise considerably during periods of power price inflation.

This structural characteristic creates an asymmetric vulnerability for aluminium producers during energy price cycles. When electricity and fuel costs rise, the impact on smelting margins is immediate and direct, while the ability to pass those costs through to customers is constrained by global LME aluminium pricing mechanisms that operate independently of any individual producer's cost base.

The consequence is that rebounding energy price inflation compresses smelting margins from below while aluminium prices may not simultaneously rise to compensate. This squeeze is reflected almost immediately in equity valuations for listed producers, as seen across the aluminum and alumina markets more broadly.

Softening Industrial Demand and Cautious Downstream Positioning

Beyond energy costs, investor sentiment toward aluminium equities in 2026 has been shaped by uncertainty around downstream demand. Furthermore, three sectors are particularly significant in this context:

- Automotive manufacturing, where aluminium demand is tied to vehicle production volumes and the pace of lightweighting adoption in both conventional and electric vehicles

- Construction and real estate, where aluminium use in structural and facade applications is sensitive to project pipeline activity and financing conditions

- Packaging and consumer goods, where demand tends to track broader economic activity and consumer confidence

When capital expenditure decisions slow across these sectors, near-term aluminium offtake projections soften, and equity markets price in a reduction in forward earnings for producers. The relationship is not always linear, but the directional impact of cautious China industrial demand on aluminium stock valuations is well-established across multiple commodity cycles.

Currency and Cross-Market Contagion

A less-discussed but important driver of non-ferrous metals stock volatility is the contagion effect that operates across commodity categories. When copper, gold, molybdenum, and other metals face simultaneous selling pressure, the sector-wide signal overwhelms individual company narratives. Institutional investors managing commodity exposure often reduce holdings across the board during risk-off periods rather than making granular distinctions between producers at different points in the cost curve.

Do Chalco's Fundamentals Support the Bearish Sentiment?

Q1 2026 Earnings: A Counterpoint to Market Pessimism

The most compelling argument against reading Chalco's share price decline as a fundamental deterioration lies in its first-quarter 2026 financial results. The company reported a net profit of approximately RMB 5.5 to 5.527 billion for the quarter, representing year-on-year growth of 56% and landing at the upper end of its guided range of RMB 5.3 to 5.6 billion.

This magnitude of earnings growth during a period of market-perceived headwinds is not a minor discrepancy. A 56% year-on-year profit increase reflects meaningful operational leverage, supported by sustained elevated aluminium prices linked to global supply tightness. The fact that this result landed at the top of guidance rather than the bottom further demonstrates management's ability to navigate the cost and demand environment effectively.

Institutional Perspectives on Aluminium Pricing and Supply

Major investment banks have published research pointing to structural dynamics in the aluminium market that could underpin price recovery over the medium term:

| Institution | Key Perspective |

|---|---|

| Morgan Stanley | Identified upward momentum in aluminium pricing supported by supply-side constraints |

| UBS | Highlighted sustained price support attributable to tightness in global refining capacity |

| JPMorgan | Forecast a supply deficit of approximately 2 million tonnes in the aluminium market by 2026 |

If a 2-million-tonne supply deficit materialises as forecast, the structural pricing support implied for primary aluminium producers would represent a meaningful tailwind for integrated producers' earnings, a dynamic that short-term equity weakness may not yet be fully reflecting.

These institutional views are not guarantees of price outcomes, and investors should treat forward projections with appropriate caution. Commodity markets are influenced by variables that can shift rapidly, including policy changes, technological disruption, and demand shocks. Nevertheless, the directional consensus toward supply deficit conditions provides useful context for evaluating whether current share price weakness is cyclical or structural in nature.

Vertical Integration as a Long-Term Competitive Moat

How Supply Chain Ownership Reduces Operational Risk

One of the least-appreciated aspects of Chalco's business model is how vertical integration functions during periods of commodity stress. When input costs rise or intermediate markets tighten, producers that rely on external suppliers for bauxite or alumina face a compounding cost pressure that integrated producers can partially neutralise through internal sourcing.

By owning capacity at every stage of the aluminium value chain, Chalco can:

- Insulate primary aluminium production from spot market alumina price spikes

- Optimise production scheduling across the chain to reduce idle capacity costs

- Capture margin at multiple stages of the value-add process rather than at a single point

- Maintain supply continuity when third-party refinery capacity becomes constrained

This structural advantage does not eliminate exposure to energy costs or global aluminium pricing cycles. However, it meaningfully reduces the volatility of the cost base relative to non-integrated producers, which is why Chalco's decline was more contained than several peers during the May 2026 selloff.

China's Aluminium Market Structure and Production Environment

China's aluminium production operates within a regulated capacity framework that plays a significant role in market discipline. Production ceiling policies limit unconstrained capacity additions, which in turn provides a degree of structural support to aluminium pricing that would not exist in a fully liberalised market environment.

The ongoing shift toward renewable energy-powered smelting within China adds another layer of complexity. Hydropower-rich regions such as Yunnan have attracted smelting capacity relocation, but seasonal water variability creates periodic output fluctuations. These dynamics create a gradually rising cost floor for Chinese aluminium production, which has implications for the global price at which supply becomes economically viable. In addition, the aluminium tariff impact on trade flows adds further complexity to this already nuanced production environment.

The next major ASX story will hit our subscribers first

Aluminium's Strategic Role in the Energy Transition

Why Structural Demand Growth Remains Intact Beyond the Cycle

Stepping back from short-term equity volatility, the long-term demand narrative for aluminium is one of the stronger stories in the materials sector. Three growth vectors are particularly significant:

- Electric vehicles: The average electric vehicle contains substantially more aluminium than an equivalent internal combustion engine vehicle, driven by lightweighting requirements that offset the additional weight of battery systems. As EV production volumes scale globally, per-vehicle aluminium intensity creates a compound demand growth dynamic.

- Renewable energy infrastructure: Solar panel mounting structures, wind turbine nacelles, and associated electrical balance-of-plant components all rely heavily on aluminium. The global buildout of renewable generation capacity represents a structurally new source of aluminium demand.

- Grid electrification and transmission: Aluminium conductors dominate high-voltage transmission line construction globally. Accelerating grid expansion required to connect renewable energy sources to consumption centres represents sustained demand from a sector where aluminium has no viable substitute at scale.

The critical insight for long-term investors is that aluminium sits at the confluence of decarbonisation and electrification, two megatrends that will drive materials consumption for decades regardless of near-term industrial cycle fluctuations.

Chalco's supply chain relevance has grown in direct proportion to these trends. Consequently, among the top aluminium companies, its capacity to supply both primary metal and downstream-processed aluminium components positions it as a potential beneficiary of rising global demand for lightweight materials in automotive manufacturing, renewable power systems, and electrification infrastructure. Mining.com has also reported on how Chalco has previously managed capacity strategically during price slumps, further illustrating the company's operational discipline.

Frequently Asked Questions: Chalco Shares and Aluminium Market Pressures

Why Did Chalco Shares Fall in May 2026?

Chalco shares fall amid pressure on aluminium due to a combination of rising energy cost pressures compressing smelting margins, sector-wide selling across non-ferrous metals in Hong Kong, and cautious investor sentiment toward industrial commodity equities during a period of inflationary uncertainty. The decline was sector-driven rather than reflective of company-specific operational deterioration.

How Much Did Chalco Shares Fall?

Shares closed 3.38% lower on 11 May 2026 at HKD 11.15 (USD 1.43), down from HKD 11.54 (USD 1.48) at the previous close, with intraday selling pressure reaching as high as 5.05% during peak volatility.

Is Chalco Profitable Despite the Share Price Decline?

Yes. Chalco reported Q1 2026 net profit of approximately RMB 5.5 billion, representing 56% year-on-year growth and landing at the upper end of its guidance range, demonstrating strong operational performance despite short-term equity market weakness.

What Makes Chalco Different from Other Aluminium Producers?

Its fully vertically integrated operating model spanning bauxite mining, alumina refining, primary smelting, and downstream processing provides greater cost stability and supply chain control than non-integrated producers. This is reflected in its comparatively moderate equity drawdown relative to sector peers during periods of market stress.

Why Is Aluminium Structurally Important Beyond the Current Cycle?

Aluminium is a critical material for electric vehicles, solar energy infrastructure, wind power systems, and grid transmission cables. These end-use sectors are tied to long-duration decarbonisation investment cycles that are largely independent of short-term industrial demand fluctuations, providing a durable structural demand tailwind for integrated producers over multi-decade time horizons.

Key Takeaways: Reading the Gap Between Sentiment and Fundamentals

- Chalco shares fell 3.38% on 11 May 2026, reaching HKD 11.15, driven by sector-wide commodity selling pressure rather than company-specific deterioration

- Energy cost inflation remains the most acute structural headwind for aluminium smelters globally, given energy's outsized share of total production costs

- Chalco's decline was notably more contained than several peer companies, with Nanshan Aluminum falling more than 13% during the same period, suggesting integrated business models offer partial insulation

- Q1 2026 net profit of approximately RMB 5.5 billion and 56% year-on-year earnings growth represent a material counterpoint to bearish equity sentiment

- Institutional research pointing to a potential 2-million-tonne aluminium supply deficit by 2026 suggests medium-term price support that may not yet be priced into current equity valuations

- Long-term demand from electric vehicles, renewable energy infrastructure, and grid electrification creates a structural growth narrative for integrated producers that extends well beyond the current commodity cycle

- Investors navigating aluminium equities should distinguish carefully between cyclical equity volatility driven by macro forces and the underlying operational strength of vertically integrated business models with durable cost advantages

This article is intended for informational purposes only and does not constitute financial advice. All references to analyst forecasts, price targets, and supply deficit projections represent third-party views subject to change and should not be relied upon as guarantees of future market outcomes. Past share price performance is not indicative of future results. Readers should conduct their own independent research before making investment decisions.

Want to Be First When the Next Major Mineral Discovery Hits the ASX?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying high-potential mineral discoveries across more than 30 commodities and converting complex data into clear, actionable investment insights — explore the historic returns major discoveries have delivered and start your 14-day free trial to ensure you're positioned ahead of the broader market.