June 9, 2026

The Geological Lottery: Why Only a Handful of Gold Deposits Ever Reach 2 Million Ounces

The global gold mining industry has been living off the discoveries of the 1990s and early 2000s for longer than most investors realise. Since 2010, the rate at which the industry has replaced mined ounces with newly discovered reserves has fallen dramatically, with major producers consistently consuming more gold than explorers are finding. In this context, a multi-million-ounce undeveloped deposit in a jurisdiction with established mining infrastructure is not merely interesting — it is structurally scarce.

That scarcity forms the essential backdrop for understanding why Challenger Gold's Hualilán project in Argentina's San Juan Province has attracted sustained attention from the gold investment community. With a declared mineral resource of 2.8 million ounces gold-equivalent (AuEq), Hualilán sits in a category occupied by very few undeveloped assets in Latin America. The question is no longer whether the deposit is significant — the numbers confirm that it is. The more useful question is how the project gets from resource to revenue, and what the realistic development pathways look like across a range of scenarios.

This article is intended for informational purposes only and does not constitute financial advice. All financial projections, production targets, and scoping study metrics discussed are forward-looking estimates subject to material risks and uncertainties. Investors should conduct their own due diligence.

When big ASX news breaks, our subscribers know first

San Juan Province: Structural Geology Meets Investment Opportunity

Argentina's Andean belt is home to some of the most geologically productive mineralised systems in the Western Hemisphere. San Juan Province, in particular, occupies a section of the Central Andes where deeply penetrating structural faults have historically channelled hydrothermal fluids rich in gold, silver, and base metals into favourable host rocks.

The mineralisation style at Hualilán reflects this setting. The deposit exhibits characteristics of both epithermal and mesothermal gold systems, meaning the gold has been deposited across a range of crustal depths and temperatures. This dual-character mineralisation is important for a reason that is often overlooked in surface-level analysis: epithermal zones typically yield higher-grade, near-surface ore suitable for early-stage mining, while deeper mesothermal structures can sustain longer mine lives at consistent grades. The combination underpins the project's multi-commodity output profile of gold, silver, and zinc.

What makes San Juan strategically compelling beyond its geology is the presence of existing processing infrastructure in the region. The Casposo Argentina Mining processing plant, located approximately 165 kilometres from Hualilán, provides an immediate pathway to production without the timeline and capital burden of constructing a greenfield processing facility. Furthermore, understanding the mineral deposit tiers relevant to a project of this scale helps contextualise why Hualilán commands such attention from the investment community.

Argentina's Investment Climate: Reading the Regulatory Landscape

Argentina's mining sector has long carried a jurisdiction risk premium that has suppressed valuations relative to comparable assets in Chile or Peru. Currency controls, export taxes, and periodic policy reversals have historically made international capital cautious.

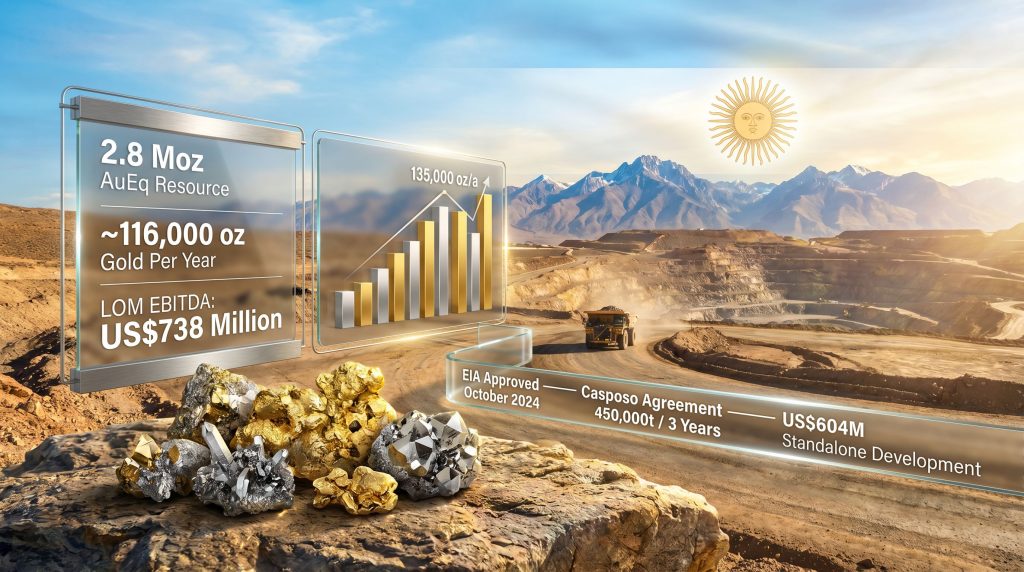

However, the regulatory architecture has evolved meaningfully. Argentina's RIGI large investment incentive framework, combined with provincial-level mining codes in San Juan that provide additional stability guarantees, creates a layered legal structure that is more investor-friendly than the country's general macro environment might suggest. The critical milestone for Hualilán specifically was the Environmental Impact Assessment (EIA) approval granted in October 2024, which removed one of the most significant regulatory gatekeepers standing between exploration and production.

It is worth noting that EIA approval does not eliminate all regulatory exposure. Royalty frameworks, export tax structures, and community consultation requirements remain active variables. The peso's structural weakness also creates an ongoing asymmetry: operating costs carry local currency exposure while revenues are denominated in US dollars, which can work in a project's favour during periods of peso depreciation but introduces complexity in cost forecasting.

Project Fundamentals: What the Numbers Actually Mean

The headline metrics for Challenger gold production at Hualilán Argentina are drawn from a scoping study covering a high-grade core development case. Understanding what these figures represent in context is essential for accurate interpretation.

| Metric | High-Grade Core Case |

|---|---|

| Total Mineral Resource | ~2.8 Moz AuEq |

| Annual Gold Production Target | ~116,000 oz |

| Annual Silver Production | ~440,000 oz |

| Annual Zinc Production | ~9,175 tonnes |

| Life-of-Mine EBITDA | US$738 million |

| Full Standalone Development Capex | US$604 million |

| Long-Term Production Target | ~135,000 oz/a gold |

| Near-Term Toll Milling Output | ~90,000 oz AuEq over 3 years |

A few dimensions of this data deserve closer examination. The multi-commodity revenue stream is not simply a marketing feature — it has genuine economic significance. Silver and zinc by-product credits reduce the effective all-in sustaining cost (AISC) per gold ounce, which improves margin resilience during gold price downturns. Zinc, in particular, is a commodity with strong industrial demand tied to galvanising and battery technology, providing a degree of structural demand support.

The US$738 million life-of-mine EBITDA figure needs to be understood as a scoping-level estimate under a specific set of commodity price assumptions. Consequently, the gold price outlook is especially relevant here — at US$2,000 per ounce, project economics look materially different than at US$2,500 or US$3,000 per ounce. Given that gold has traded above US$2,300 for extended periods recently, the scoping metrics may actually prove conservative under elevated price scenarios — but the inverse also applies if prices retreat.

Key Insight: Capital intensity at approximately US$4,470 per annual ounce (based on US$604 million total investment against a 135,000 oz/a target) sits within the typical range for mid-tier underground and combined open-pit/underground gold operations in South America. Projects with by-product credits from silver and zinc effectively reduce the net capital intensity further when modelled on a gold-equivalent basis.

The Two-Stage Development Architecture: Logic and Limitations

What Toll Milling Actually Does for a Junior Developer

Toll milling is a production arrangement in which a mining company extracts ore from its own deposit and transports it to a third-party processing facility, paying a fee for crushing, grinding, and metal recovery services. For junior miners without the balance sheet to fund standalone processing infrastructure, it provides a bridge between resource delineation and full-scale production.

Challenger has secured a toll-milling agreement with Casposo Argentina Mining covering approximately 450,000 tonnes over a three-year period, structured around 90-day batch processing cycles. The operational logic is straightforward: extract, transport, process, recover, sell, and repeat — building cash reserves and operational track record simultaneously.

The limitations are equally real and worth acknowledging:

- The 165-kilometre transport distance introduces ore haulage costs that compress margins relative to a co-located processing scenario

- Batch processing creates cash flow lumpiness — revenue is recognised in cycles rather than continuously, which affects working capital management

- Throughput and scheduling decisions at the Casposo plant are ultimately controlled by a third party, introducing a layer of operational dependency

- Grade dilution during transport and handling can modestly reduce recoveries compared to on-site processing

Despite these constraints, the near-term production target of approximately 90,000 oz AuEq over three years from toll milling represents a meaningful cash flow opportunity. Execution of a 24-month mining contract with MAPAL and completion of the first production blast signal that operational readiness has advanced beyond the planning stage.

The Pathway to a Standalone Mine

Stage Two is where the project's full potential is realised. At US$604 million total investment, standalone development is a capital-intensive undertaking that will require either a substantial equity raise, project finance arrangements, a strategic partnership with a larger producer, or some combination of all three.

The strategic value of Stage One in this context is often underappreciated. Cash flows generated during toll milling not only fund ongoing exploration and development activities but also provide proof-of-concept data — real production numbers, actual recovery rates, demonstrated logistics capability — that materially de-risk the project in the eyes of project finance lenders and potential joint venture partners. In addition, progressing toward a definitive feasibility study during this phase is essential to unlocking the capital required for Stage Two.

Comparable Projects and M&A Context

| Metric | Hualilán (Challenger Gold) | Typical Junior Argentine Gold Project |

|---|---|---|

| Total Resource (AuEq Moz) | ~2.8 Moz | 0.5 to 1.5 Moz |

| Annual Production Target | ~116,000 oz Au | 30,000 to 80,000 oz Au |

| Development Pathway | Toll milling to standalone mine | Typically single-stage |

| EIA Status | Approved (October 2024) | Variable |

| Processing Agreement | Secured (Casposo, 450kt/3 years) | Rarely secured pre-construction |

The scarcity of multi-million-ounce undeveloped gold deposits globally gives Hualilán a specific relevance in the M&A landscape. Major and mid-tier gold producers have consistently demonstrated willingness to pay acquisition premiums of 30 to 60 percent above in-situ resource value for assets in Latin America that offer credible development pathways, particularly where permitting milestones have already been cleared. Indeed, gold M&A activity across the sector reinforces how rare fully permitted, multi-million-ounce assets truly are. Whether Challenger Gold pursues development independently or attracts a strategic acquirer, the EIA approval and operational contracts significantly strengthen its negotiating position.

Development Milestones: Sequencing the Path Forward

| Development Phase | Key Milestone | Status |

|---|---|---|

| Environmental Approvals | EIA granted | Completed — October 2024 |

| Mining Contractor | 24-month contract with MAPAL | Executed |

| Processing Agreement | Casposo deal (450kt over 3 years) | Executed |

| First Production Activity | Initial production blast | Completed |

| Toll Milling Phase | ~90,000 oz AuEq over 3 years | In progress |

| Feasibility Study | Scoping to DFS progression | Anticipated mid-to-late 2020s |

| Standalone Construction | US$604 million capital deployment | Subject to financing |

| Peak Annual Production | ~135,000 oz/a gold target | Long-term objective |

The next major ASX story will hit our subscribers first

Three Scenarios for How This Plays Out

Scenario A: Organic Progression Through Cash Flow Reinvestment

The toll-milling campaign delivers approximately 90,000 oz AuEq over three years, generating operating cash flows that fund ongoing resource expansion drilling. An updated resource estimate with higher confidence classification supports a bankable feasibility study. Project financing is secured on the strength of the completed study, and standalone development proceeds with Challenger retaining operational control at a target production rate of 135,000 oz/a.

Scenario B: Strategic Partnership Accelerates the Timeline

A mid-tier or major producer identifies Hualilán as a reserve replacement opportunity and either acquires a controlling interest or enters a joint venture structure that shares the US$604 million capital burden. This pathway accelerates Stage Two development but introduces dilution for existing shareholders. Given precedent transactions in South American gold M&A, a deal in this structure could imply a significant re-rating of the asset's implied value per resource ounce.

Scenario C: Extended Toll Milling with Deferred Capital Commitment

Financing conditions tighten, gold prices soften, or macroeconomic instability in Argentina elevates the risk premium on project finance. Challenger extends the toll-milling arrangement, potentially with additional processing partners, and defers the standalone development decision while continuing resource expansion drilling. The asset continues generating cash flow and growing its resource base, creating optionality at the cost of delayed full-scale production.

Strategic Takeaway: Each of these pathways leads to a different outcome for shareholders, but all three scenarios are supported by the structural de-risking already achieved. The EIA approval, secured mining and processing contracts, and first production blast collectively represent the kind of concrete operational progress that separates genuine development-stage assets from projects that exist primarily on paper.

What Investors and Analysts Should Monitor

For those tracking Challenger gold production at Hualilán Argentina, the following metrics and events carry the most analytical weight:

- Toll-milling recovery rates from initial batch campaigns, particularly whether head grades mined align with resource model predictions

- Quarterly resource update announcements reflecting results from ongoing drilling programs — given the resource remains open in multiple directions, upgrades are plausible; furthermore, interpreting drill results accurately is critical to assessing whether the resource model is holding up in practice

- Progress toward a Definitive Feasibility Study (DFS), which is the critical document for unlocking project finance at the scale required for Stage Two

- Argentina's macroeconomic trajectory, particularly any shifts in export tax frameworks or mining royalty structures that could affect USD-denominated project economics

- Gold price movements, given the meaningful sensitivity of life-of-mine EBITDA to price assumptions across the US$2,000 to US$3,000 range

- Capital raising activity, including any announcements regarding strategic investors, streaming agreements, or equity placements that would signal financing progress for standalone development

The broader global context reinforces the structural case. Latin America supplies approximately 25 to 30 percent of annual global gold production, with Argentina historically contributing a fraction of what its geological endowment would suggest is achievable. If Hualilán reaches full production at the 135,000 oz/a target, it would represent one of the more significant single-site gold operations in the country's modern mining history — a benchmark that underscores both the scale of the opportunity and the complexity of the path required to realise it.

Want to Track the Next Major Gold Discovery Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — transforming complex mineral data into actionable investment insights the moment they hit the exchange. Explore Discovery Alert's discoveries page to see the historic returns major mineral discoveries have generated, and begin your 14-day free trial today to position yourself ahead of the market.