June 9, 2026

Why the Monetary Architecture of the Past Five Decades May Be Breaking Down

The global financial system has operated without a formal monetary anchor since 1971, when the United States severed the last institutional link between the dollar and gold. The end of the gold standard fundamentally altered how sovereign debt functioned, with government bonds filling that role by providing capital preservation, yield, and liquidity to institutional portfolios worldwide. Yet the structural assumptions underpinning that arrangement — namely that sovereign debt is a reliable store of value, that central banks can credibly target 2% inflation, and that fiat currencies are inherently superior to hard assets — are now being tested in ways not seen in living memory for most Western investors.

The gold remonetization thesis is not simply a price prediction. It is a structural argument about what happens when monetary credibility erodes slowly, then suddenly, and which assets benefit when that transition reaches a tipping point.

When big ASX news breaks, our subscribers know first

What Is the Gold Remonetization Thesis? Defining the Framework

Remonetization vs. a New Gold Standard

The gold remonetization thesis does not require a formal return to the gold standard. Instead, it describes a more gradual and arguably more powerful process: gold reclaiming a functional monetary role through its increasing adoption as a reserve asset, a collateral instrument, a balance sheet strengthening tool, and an inflation hedge by sovereign institutions and large capital allocators globally.

Academic research on gold price discipline, including foundational work on the conditions under which gold-based monetary constraints actually deliver stability, makes a critical finding. Such a regime only produces durable monetary outcomes when the underlying institutional commitment is both permanent and credible. A gold accumulation strategy that can be reversed under political pressure is not remonetization — it is simply tactical diversification.

The distinction matters enormously for investors. Genuine remonetization implies a structural, multi-decade shift in gold in the monetary system. Tactical diversification implies a cyclical trade that reverses when risk appetite returns.

The Critical Academic Warning: Credibility Is Everything

Economic research on gold monetization regimes, including the work of Flood and Garber on price discipline and speculative attack dynamics, establishes three non-negotiable conditions for any gold-based monetary framework to function without destabilising speculative runs:

- A permanent and credible institutional commitment to the regime

- Coordinated adjustment of the fiat money supply to align with gold reserve levels

- Market confidence that policymakers will not abandon the framework under stress

Without all three, the history of gold-linked monetary systems suggests that speculative attacks on gold reserves become structurally inevitable. This is why distinguishing between genuine remonetization and government gold mobilisation schemes — such as India's domestic gold monetisation programme, which aimed to recirculate household gold holdings rather than restore gold as a monetary anchor — matters so much analytically.

The Macro Environment Supporting the Remonetization Case

The macroeconomic backdrop of 2025 provides a more compelling structural argument for gold than any single geopolitical event or rate decision. Consider the following data landscape:

| Macro Indicator | Historical Baseline | 2025 Reality |

|---|---|---|

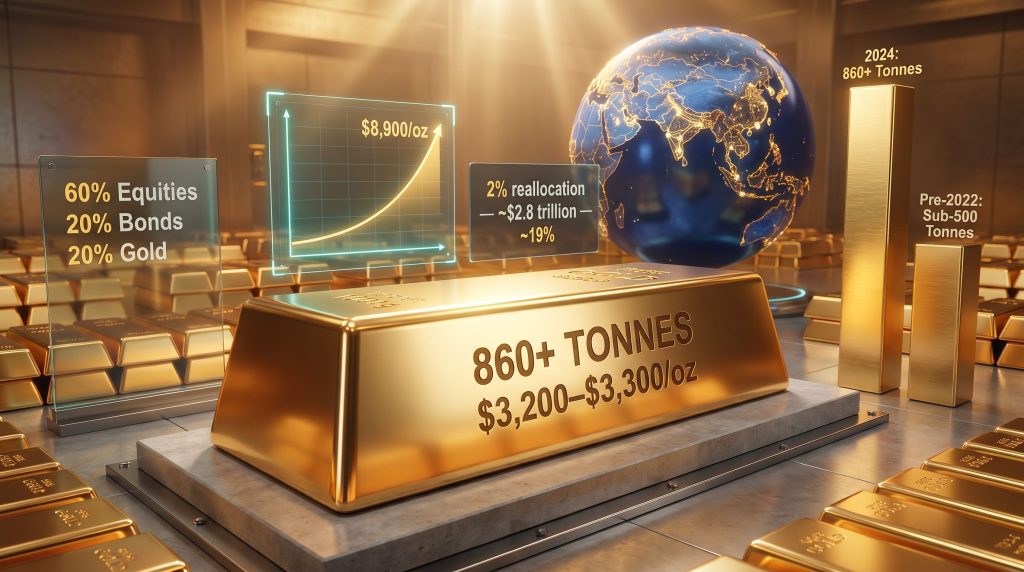

| Global Government Debt Growth (20 years) | GDP-linked expansion | Approximately 3x growth vs. approximately 2x GDP growth |

| Central Bank Gold Demand (annual) | Sub-500 tonnes pre-2022 | 860+ tonnes in 2024; 250+ tonnes in Q1 2025 |

| Gold ETF Outflows (March 2025) | Moderate seasonal variation | 86 tonnes, near-panic levels among Western investors |

| GDX Free Cash Flow Margin | 4.2% in 2023 | Approximately 25% in 2025 |

| Top 10 Producer Free Cash Flow | Approximately $10 billion baseline | Approximately $30 billion, effectively tripled |

Global government debt has tripled over two decades while global GDP has barely doubled. The Federal Reserve has now operated above its own 2% inflation target for more than 63 consecutive months, a duration that suggests the target has lost its anchoring credibility regardless of official communications. Furthermore, the bond market, which has historically served as capital preservation infrastructure for institutional portfolios, has entered what can only be described as a structural bear market.

Capital competition is intensifying simultaneously. Infrastructure buildout, Gulf sovereign fund investments in pipelines, accelerating OECD defence spending programmes, and a pipeline of large IPOs are all competing for the same pool of institutional capital. Consequently, this competition creates a crowding dynamic that makes reallocation into hard assets structurally more attractive over time.

The Six Vectors of Gold Remonetization: A Multi-Dimensional Framework

The gold remonetization thesis is best understood not as a single driver but as six partially independent vectors that reinforce each other as they develop. Not all six need to fully materialise for gold prices to reach significantly higher levels.

Vector 1: Sovereign Accumulation as Monetary Insurance

Central bank gold reserves have grown by more than 1,000 tonnes in each of the past three consecutive years. The 2022 sanctions imposed on Russia's foreign exchange reserves served as a critical inflection point, demonstrating to reserve managers globally that sovereign foreign currency holdings are not unconditionally secure. Gold, which cannot be frozen, sanctioned, or digitally disabled, became the obvious alternative reserve asset.

Emerging market central banks remain significantly underweighted in gold relative to their Western counterparts, suggesting substantial runway for continued accumulation even if the pace moderates from recent highs.

Vector 2: Private Capital Reallocation Away from Fixed Income

A 2% reallocation from the approximately $140 trillion global fixed income market into gold would represent roughly $2.8 trillion in new demand, equivalent to nearly one-fifth of the entire investable gold market, estimated at approximately $15 trillion.

The scale of potential capital flows from bonds into hard assets is staggering when expressed in these terms. Current institutional gold allocations make the opportunity even more striking:

- Family offices currently hold less than 2% of total assets in gold

- Pension funds hold even less, with many at effectively zero allocation

- In 1980, gold represented approximately 8% of institutional portfolios

A significant cohort within large institutions can be described as having closed gold convictions, meaning they understand the structural case for gold but remain unable to act due to career risk, mandate restrictions, and institutional inertia. As bond market stress persists, pressure on those mandate constraints will build.

Vector 3: Central Bank Balance Sheet Recapitalisation Through Gold Revaluation

Rising gold prices passively strengthen sovereign balance sheets without requiring any policy action. Across the eurozone, unrealised gains on gold reserves held by European central banks have exceeded 1.2 trillion euros as gold prices have surged. This silent recapitalisation dynamic is increasingly being recognised by central bank officials as a legitimate form of balance sheet equity.

The United States presents the most dramatic potential example. American gold reserves are still carried on official books at $42 per ounce, a legacy accounting convention from the post-Bretton Woods era. A mark-to-market revaluation to current spot prices would generate more than $1.1 trillion in paper equity with no additional purchasing required. This is not a peripheral accounting curiosity — it is a policy lever receiving serious attention in monetary policy circles.

Vector 4: Tokenisation and Digital Gold Infrastructure

Physical gold is entering digital settlement and collateral frameworks through tokenisation platforms, transforming its functional role from a passive reserve held in vaults to active financial infrastructure. Tether, the digital currency issuer, has accumulated nearly 200 tonnes of physical gold stored in Swiss Alpine vaults, reportedly ranking as the second-largest gold buyer in the world during certain recent months. The integration of gold into digital finance expands both the accessibility and utility of gold as a monetary instrument.

Vector 5: Portfolio Architecture Transformation Among Major Institutions

The traditional 60/40 portfolio framework is being structurally challenged. Morgan Stanley has publicly proposed a 60/20/20 allocation model consisting of 60% equities, 20% bonds, and 20% gold. Prominent macro investors including Stan Druckenmiller, Jeff Gundlach, and Ray Dalio have publicly advocated hard asset diversification. These are not fringe voices — they represent the leading edge of a potential institutional reallocation that has, by most measures, barely begun.

Vector 6: Western Central Bank Re-Entry as a Wildcard Scenario

Several nations hold minimal gold reserves relative to their economic size and gold production capacity. These gold-light countries — including Canada, Australia, Japan, and the United Kingdom — represent a potential wildcard in the remonetisation thesis. Policy frameworks that require domestically mined gold to be offered to the national central bank before export, or deliberate gold accumulation programmes to restore confidence in sovereign currencies, could add an entirely new demand vector not currently priced into market expectations.

The $140 Trillion Bond Market: Gold's Largest Potential Demand Catalyst

The arithmetic of even a marginal reallocation from fixed income into gold is structurally significant in a way that most mainstream financial analysis underestimates.

| Allocation Scenario | Capital Entering Gold | Percentage of Investable Gold Market |

|---|---|---|

| 1% reallocation from the $140 trillion bond market | Approximately $1.4 trillion | Approximately 9% |

| 2% reallocation | Approximately $2.8 trillion | Approximately 19% |

| 5% reallocation, matching 1980 institutional levels | Approximately $7 trillion | Approximately 47% |

The key friction is institutional rather than analytical. Many bond managers already understand the structural deterioration in fixed income as a capital preservation vehicle. However, the barriers to acting on that understanding are career risk, mandate restrictions, and the inertia of multi-decade portfolio conventions. As bond market volatility persists and real yields remain negative in inflation-adjusted terms, the pressure on those barriers will compound.

Is the Current Gold Correction a Warning or a Secular Bull Market Reset?

Gold tested a significant downside zone before recovering, and the immediate narrative focused on stronger-than-expected employment data, a dramatic repricing of Federal Reserve rate expectations, and the resulting surge in Treasury yields. That is the daily tape. The structural thesis operates on an entirely different timeframe.

The Mount Everest framework offers a useful analytical perspective. At nearly 8,900 metres in height — which corresponds closely to the long-term price target outlined in detailed remonetisation analysis — Everest cannot be climbed in a single push. Climbers must stop at base camps, acclimatise to altitude, and recover before continuing upward. Gold's 60%-plus return in dollar terms over the prior year represented an extraordinary ascent. A period of digestion and base-building is not a failure of the thesis — it is a necessary condition for the next leg higher.

Framework: Signs a Bull Market Has NOT Ended

- The gold-to-silver ratio remains elevated in the high 50s. At secular bull market peaks, this ratio has historically compressed to between 16 and 30, indicating that silver has not yet meaningfully outperformed gold.

- Commitment of Traders positioning at recent highs did not reach the extreme net-long levels that have historically accompanied secular tops.

- Mining sector M&A has remained disciplined. Euphoric bull market peaks are characterised by irrational mega-deals — no such pattern has emerged.

- Western ETF outflows of 86 tonnes in March 2025 signal bearish sentiment and panic among short-term holders, not distribution-phase euphoria from long-term bulls.

The $4,000 level represents a significant psychological support zone. Seasonal analysis of gold price behaviour identifies the window from mid-June to late August as historically corresponding to cycle lows, with price recovery typically commencing from that seasonal trough.

The next major ASX story will hit our subscribers first

Why Gold Sells Off on Rate Headlines Despite the Remonetization Case

One of the most frequently misunderstood dynamics in gold markets is the apparent contradiction between a structural remonetisation thesis and gold's tendency to sell off sharply during geopolitical or rate shock events.

The explanation lies in liquidity mechanics. On days when daily traded gold volume reached $550 billion, gold was the first asset liquidated by institutions facing margin calls or redemptions, precisely because it offered the tightest bid-ask spreads and the largest available profits. This is not a signal about gold's long-term monetary role — it is a function of its unique liquidity characteristics within diversified portfolios.

The 2008 parallel is instructive. When Lehman Brothers collapsed and the broader financial system came under acute stress, gold sold off sharply. Conventional analysis treated this as evidence that gold failed as a crisis hedge. What followed, however, was a multi-year surge in gold prices as the fiscal and monetary consequences of the crisis played out. The same dynamic is now relevant.

The Correlation Trap: Market participants frequently misread gold's short-term reaction to geopolitical or rate events as a signal about its long-term trajectory. Historical data consistently shows that the inflationary and fiscal consequences of major crises — not the crises themselves — drive gold's most significant appreciation phases.

On the Federal Reserve specifically, the incoming Fed chair has signalled a preference for the trimmed PCE as a favoured inflation indicator. This particular measure notably failed to register the 2021 inflation surge during its early stages, raising legitimate questions about whether it understates structural price pressures. The Federal Reserve has now operated above its 2% inflation target for over 63 consecutive months. The practical implication is that structurally higher inflation is being tacitly accepted, while official communications maintain the appearance of 2% targeting.

China's Strategic Role in the Global Gold Story

China's relationship with gold operates on multiple levels simultaneously, and conflating retail household demand with strategic institutional accumulation produces confused analysis.

Since the Shanghai Gold Exchange commenced operations, China has imported an estimated 28,000 tonnes of gold. China is simultaneously the world's largest gold producer and retains 100% of its domestically mined output, meaning not one ounce of Chinese-produced gold enters the international export market. Official Chinese gold reserve figures are widely understood to significantly understate actual holdings.

One analytically compelling thought experiment relates to trade surplus dynamics. China's approximately $1.2 trillion annual trade surplus, when divided by gold at certain price levels, implies that gold could theoretically serve as the mechanism for trade rebalancing that politicians in both the United States and China are unwilling to achieve through direct currency adjustment. Shadow gold price calculations, based on backing the US monetary base with gold at current reserve levels, suggest theoretical valuations well above $20,000 per ounce.

The centre of gravity in global gold demand has demonstrably shifted eastward. China and India together account for more than 50% of physical gold demand. Western investor sentiment, while influential in short-term price discovery, no longer determines the structural trajectory of the market.

The Indian household buyer, often described as among the most consistently well-timed gold accumulators globally, purchases gold on every significant price dip. This behavioural pattern, embedded in cultures where currency debasement has been experienced across multiple generations, represents a structural demand floor that operates independently of Western financial market conditions.

The Mining Sector: Free Cash Flow Transformation and the Generalist Problem

The financial transformation of the gold mining sector over the past decade deserves more attention than it typically receives from generalist investors.

- GDX free cash flow margins expanded from 4.2% in 2023 to approximately 25% in 2025

- The top 10 global gold producers generated approximately $30 billion in free cash flow in the most recent annual period, triple the prior baseline

- Margin expansion of approximately sixfold since 2015 was driven almost entirely by gold price leverage rather than volume growth

Despite this financial transformation, gold and silver mining stocks represent approximately 1% of the global equity market. The sector has not attracted meaningful generalist institutional capital, despite the cash flow metrics that would command attention in any other industry context.

The reason is partly communicational. Mining executives have historically defaulted to geological complexity in investor presentations rather than delivering simple, cash-flow-focused narratives. Furthermore, a thoughtful concept emerging from within the sector is the corporate gold standard, an approach under which gold and silver miners would retain 5% to 10% of their own production on their balance sheets rather than selling all output immediately.

When generalist capital does begin flowing into the sector at scale, liquidity dynamics will direct it toward large-cap producers and royalty and streaming companies first. Smaller mid-cap developers and junior explorers will benefit later in the cycle as risk appetite expands, but they are not the primary entry point for institutional capital moving out of mainstream equity allocations.

Investment Framework: Signals That Would Qualify a Panic-Level Entry Point

- Extreme outflows from gold and mining ETFs including GDX, GDXJ, and SILJ reaching multi-year highs

- Sentiment indicators reaching deeply oversold readings across multiple frameworks

- Commitment of Traders positioning reaching historically low net-long levels

- High-profile mainstream commentary declaring the gold bull market definitively over

- Gold testing the $4,000 major psychological support level

- Seasonal alignment with the historical mid-June to late-August low window

Long-Term Price Architecture: Valuation in a Remonetization Scenario

The most important question for investors is not whether gold will reach any specific price target in any specific timeframe. It is whether this is a normal commodity price cycle or a monetary system reorganisation.

| Valuation Framework | Implied Gold Price Range |

|---|---|

| Current spot price, mid-2025 | Approximately $3,200 to $3,300 per ounce |

| Base case decade-end target under inflationary scenario | Approximately $8,900 per ounce |

| Shadow price, US monetary base fully backed by gold | Above $20,000 per ounce |

| Shadow price, international monetary base coverage | Significantly higher |

The $8,900 target, when expressed as an annualised return from the beginning of the current decade to 2030, implies a compound annual growth rate of approximately 14.5%. This is below the approximately 19.7% annualised return already realised since the decade began, suggesting the trajectory remains consistent with the original framework rather than requiring acceleration.

If the gold remonetization thesis is correct, then current price levels — even after a substantial multi-year bull run — represent deep undervaluation relative to gold's theoretical monetary weight in a system where sovereign debt credibility is structurally impaired.

Frequently Asked Questions: Gold Remonetization Thesis

What does gold remonetization actually mean?

It describes a process by which gold gradually reclaims a functional monetary role in the global financial system, not through a formal gold standard, but through its increasing adoption as a reserve asset, collateral instrument, and inflation hedge by central banks and institutional investors.

Is gold being remonetized right now, or is this a long-term theory?

The evidence suggests both. Central bank accumulation, balance sheet revaluation dynamics, tokenisation infrastructure, and portfolio architecture shifts are all current, observable developments. The full implications will take years to price into markets. In addition, global gold ETF flows are providing further real-time evidence of shifting institutional sentiment that supports the broader structural argument.

How does central bank buying support the remonetization thesis?

Three consecutive years of purchases exceeding 1,000 tonnes, combined with the strategic motivations revealed by the 2022 Russia sanctions, indicate that reserve managers are treating gold as monetary insurance rather than simply a commodity holding.

What is the shadow gold price and how is it calculated?

The shadow gold price represents the theoretical price at which gold would need to be valued to back a monetary base with physical gold reserves. Applied to the US monetary base alone, this calculation implies a price above $20,000 per ounce at current reserve levels.

What would cause the gold remonetization thesis to fail?

A credible and sustained restoration of fiscal discipline across major sovereign borrowers, a genuine return of inflation to 2% on a durable basis, and a structural strengthening of government bond markets as capital preservation instruments would all represent meaningful challenges to the thesis. For a detailed long-term investment thesis covering gold miners and explorers, independent research from specialist consultancies offers additional perspective on the sector-specific dimensions of this framework.

Key Takeaways: The Remonetization Thesis in Summary

The gold remonetization thesis rests on three converging foundations. First, the structural deterioration of sovereign bonds as a reliable capital preservation vehicle after decades of debt expansion that has significantly outpaced economic growth. Second, the observable, multi-year accumulation of gold by central banks operating from strategic motivations that have little to do with short-term price expectations. Third, the early-stage reallocation by private institutional capital from fixed income into hard assets — a process that remains at its earliest stages relative to historical precedent.

Short-term price corrections, however sharp and psychologically uncomfortable, do not invalidate a thesis operating on a monetary system timescale. The analogy of altitude acclimatisation on a long mountain climb is more analytically useful than daily tape analysis for investors trying to understand where gold fits in a portfolio constructed for the decade ahead.

The actionable framework for investors across different conviction levels begins with understanding that the entry point — when panic indicators align with seasonal patterns and technical support levels — is likely to feel deeply uncomfortable when it arrives. Having a structured process, a defined list of quality names, and predetermined allocation levels removes the psychological barrier that causes most investors to miss the best entry opportunities in any secular bull market.

Readers interested in exploring the broader themes of gold's evolving monetary role and the structural arguments behind long-term price targets may find value in reviewing publicly available macroeconomic research and investment commentary, including discussions featured on financial media platforms such as Kitco News and the annual In Gold We Trust report published by Incrementum AG, which offers detailed multi-framework analysis of gold's position within the global monetary system.

This article is for informational purposes only and does not constitute financial advice. All price targets, forecasts, and scenario analyses referenced herein involve significant uncertainty. Past performance of any asset class is not indicative of future results. Readers should conduct their own research and consult qualified financial advisers before making investment decisions.

Ready to Capitalise on the Next Major Mineral Discovery Before the Market Does?

While the gold remonetisation thesis plays out across sovereign balance sheets and institutional portfolios, Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — transforming complex geological and commodity data into actionable insights for investors at every level. Explore how historic discoveries have generated extraordinary returns and begin your 14-day free trial today to position yourself ahead of the broader market.