July 11, 2026

The Geology Won't Lie: Understanding Chile's Deepening Copper Supply Crisis

Every commodity supercycle eventually confronts a geological ceiling. For copper, that reckoning is arriving faster than most market participants anticipated, and nowhere is this more visible than in Chile, the country that has anchored global copper supply for decades. What is unfolding across Chile's major mining operations in 2026 is not the kind of short-term disruption that self-corrects within a quarter or two. It is a convergence of structural, operational, and environmental pressures that are simultaneously suppressing output at the world's most important copper-producing nation.

Understanding why Chile copper output falls sharply across top miners requires looking beyond the monthly production figures and examining the underlying forces that have been building for years beneath the surface.

When big ASX news breaks, our subscribers know first

Chile's Role as the World's Copper Foundation

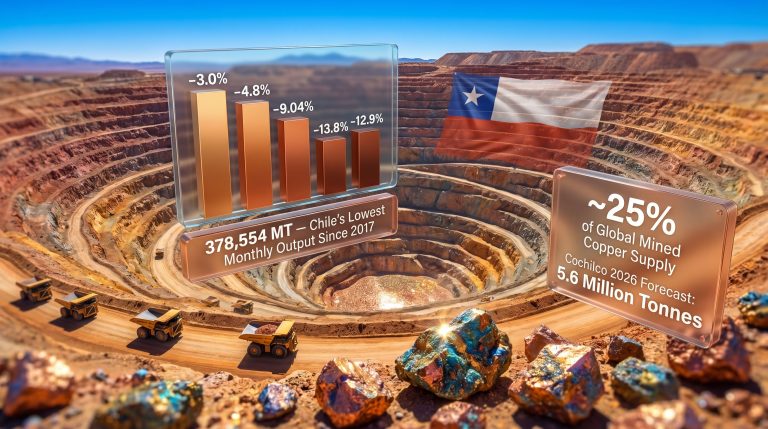

Copper markets are not distributed evenly across the globe. Chile holds a uniquely dominant position, contributing approximately 25 to 27% of total global mined copper supply. This concentration means that production trends within Chile's borders function as a direct barometer for international commodity markets. When Chilean output rises, global supply buffers thicken. When it contracts, the entire market feels the pressure.

The country's copper sector is deeply embedded in its macroeconomic architecture. Copper royalties and export revenues feed directly into government fiscal frameworks, sovereign credit profiles, and public investment capacity. Chile recorded its first GDP contraction since 2023 in early 2026, with mining sector weakness identified as a central contributing factor, illustrating how tightly the fortunes of the copper industry are woven into the national economy.

The authoritative data underpinning all of this analysis flows from Cochilco, the Comisión Chilena del Cobre, Chile's state copper commission responsible for tracking and publishing official production data across all major mining operations.

Reading the Data: A Pattern That Demands Attention

Monthly production figures can be distorted by weather events, brief operational pauses, or scheduled maintenance. What makes 2026 different is the persistence and breadth of the decline across multiple operations simultaneously. Furthermore, the Chile copper supply gap has been widening well before these monthly reports confirmed the scale of the problem.

Consider the trajectory across recent months:

- March 2026: National output contracted 9% year-on-year

- April 2026: The decline accelerated to 13.8% year-on-year

- May 2026: Output fell a further 12.9% year-on-year to 423,623 metric tonnes

- Q1 2026 total: Output reached 1.21 million tonnes, representing a 5.8% annual decline

Three consecutive months of substantial output reductions, spread across the country's largest and most technically sophisticated mining operations, cannot be attributed to isolated incidents or seasonal variation.

The simultaneous contraction at Codelco, the world's largest copper producer by volume, and BHP's Escondida, the world's single largest copper mine, removes any reasonable interpretation that this is localised operational noise.

Four Forces Compressing Chilean Copper Output

Ore Grade Deterioration: The Geological Reckoning

At the heart of Chile's production decline lies a phenomenon that geologists have been tracking for years but that commodity markets are only now fully pricing in. Chile's porphyry copper deposits, the geological formations that made the country a mining superpower, are experiencing long-term ore grade deterioration.

Porphyry systems are among the largest copper deposits on Earth, but they are not uniform. The highest-grade zones are typically mined first during a deposit's early years, a practice known in the industry as high-grading. As operations mature, miners progressively access lower-grade material, meaning more rock must be extracted, crushed, and processed to yield the same volume of refined copper.

This matters enormously for operational economics. Lower ore grades translate directly into:

- Higher energy consumption per tonne of copper produced

- Increased water demand for processing lower-concentration ore

- Greater reagent requirements, particularly for oxide ore processing

- Elevated per-unit production costs that compress margins even at strong copper prices

Grade deterioration is the primary structural driver behind output declines at Escondida, Collahuasi, El Abra, and Spence. This is not a problem that can be resolved through improved management practices or capital investment alone. It reflects the natural depletion curve of mature deposits that have been among the most intensively mined on the planet.

The El Teniente Incident and Its Cascading Effect

A fatal accident at Codelco's El Teniente mine in July 2025, which claimed six lives, triggered significant operational disruptions that extended well into 2026 production figures. El Teniente recorded a 29.5% year-on-year output decline in January 2026 and a 26.5% contraction across Q1 2026, making it the most severely affected operation in Codelco's portfolio during this period.

Safety-related shutdowns carry consequences that extend far beyond the immediate halt in production. Regulatory reviews, workforce management restructuring, modified operating protocols, and the psychological impact on the workforce can suppress productivity across multiple quarters. This is an aspect of mining risk that financial models frequently underestimate. Codelco production trends provide further context on how these operational setbacks compare with historical performance benchmarks.

Water Scarcity in the Atacama: An Escalating Constraint

The Collahuasi mine, jointly operated by Glencore and Anglo American in Chile's Tarapacá region, explicitly cited inadequate water supply as a contributing factor to its production shortfall. In May 2026, Collahuasi's output fell 19.3% to 31,000 tonnes.

Water access in the Atacama Desert region is not simply a logistical inconvenience. It sits at the intersection of regulatory frameworks, indigenous community rights, and increasingly severe hydrological stress driven by long-term climate shifts. Mining operations that rely on freshwater extraction are facing progressively tighter constraints, and desalination infrastructure, while a viable long-term solution, requires substantial capital investment and years to bring online at meaningful scale.

The Sulfuric Acid Supply Squeeze

A lesser-discussed but operationally significant factor is the tightening supply of sulfuric acid, a critical reagent in heap leach processing of copper oxide ores. Operations across Codelco, BHP, and Anglo American's Chilean portfolio that rely on oxide processing have faced elevated input costs as sulfuric acid supply chains tightened.

This cost pressure is particularly insidious because it compounds the margin erosion already caused by lower ore grades. Even when copper prices remain elevated, rising reagent costs can erode the economic viability of processing lower-grade oxide material, effectively reducing the economically recoverable resource base. Indeed, the broader copper supply crunch unfolding globally makes Chile's internal challenges all the more consequential for downstream markets.

Mine-Level Performance: Where the Losses Are Concentrated

| Mine | Operator | May 2026 Output | Year-on-Year Change (May) | Q1 2026 Decline | Primary Driver |

|---|---|---|---|---|---|

| Escondida | BHP | 108,800 tonnes | -17.6% | -9.3% | Ore grade decline |

| El Teniente | Codelco | Not disclosed | -29.5% (Jan 2026) | -26.5% | Safety incident disruption |

| Collahuasi | Glencore / Anglo American | 31,000 tonnes | -19.3% | -11% | Grade decline, water scarcity |

| Spence | BHP | Not disclosed | -33.3% (Jan 2026) | -34.4% | Ore grade deterioration |

| El Abra | Codelco (49%) | Not disclosed | N/A | -19.5% | Grade deterioration |

| Codelco (Total) | State-owned | 106,300 tonnes | -18.3% | -7.5% | Multiple operational factors |

The breadth of this table is striking. Not a single major Chilean operation recorded output growth during this period. The declines range from severe to catastrophic at the individual mine level. According to reporting from Mining.com, the April contraction was particularly pronounced, with manufacturing output also declining in parallel — reinforcing the view that Chile's economic headwinds extend well beyond mining alone.

Global Market Consequences: Supply Tightening at the Worst Possible Moment

The timing of Chile's production contraction could hardly be more consequential for global copper markets. Demand is accelerating from multiple structural sources simultaneously:

- AI data centre infrastructure requires copper-intensive power systems, cooling infrastructure, and high-voltage cabling

- Electric vehicle manufacturing uses between three and four times the copper content of a conventional internal combustion engine vehicle

- Renewable energy grid expansion, including solar, wind, and battery storage, is intensely copper-dependent at every stage of construction and connection

Against this demand backdrop, a sustained multi-month contraction from a supplier responsible for roughly a quarter of global mine output creates a structural tightening dynamic. This provides meaningful support for copper price floors over the medium term. The Chile copper price outlook for the remainder of 2026 reflects precisely these supply-side pressures feeding into forward pricing models.

Glencore's decision to reduce its 2026 copper output forecast from 930,000 tonnes to 840,000 tonnes, citing Collahuasi challenges, provides a corporate-level confirmation of what the Cochilco data shows at the national level. A 90,000-tonne downward revision from a single major diversified miner is not a routine guidance adjustment. It reflects an acknowledgment that the operational challenges are not recoverable within the fiscal year.

The next major ASX story will hit our subscribers first

Structural Shift or Temporary Dip? Evaluating the Recovery Thesis

The critical question for market participants is whether Chilean output can recover meaningfully, and over what timeframe.

| Scenario | Core Assumptions | 12-Month Outlook |

|---|---|---|

| Base Case | Grade decline continues; El Teniente partial recovery; no new major incidents | Output stabilises at 5 to 8% below 2025 levels |

| Bear Case | Additional safety events; water restrictions intensify; sulfuric acid costs escalate | Output contracts a further 10 to 15%; copper price pushes above $5.50/lb |

| Bull Case | Escondida operational improvements; Collahuasi water resolution; Codelco capex delivers | Partial recovery to within 3% of 2025 baseline by Q4 2026 |

The structural argument is difficult to dismiss. Chile has not brought a major new copper mine into production at a scale sufficient to offset grade-driven losses at existing operations. Greenfield copper development timelines span 10 to 15 years from discovery to first commercial production, meaning near-term supply relief from new Chilean projects is not a realistic scenario.

However, some portion of the current decline is attributable to the El Teniente safety incident, a non-recurring event that will eventually allow partial normalisation of output as regulatory reviews conclude and operational rhythms stabilise. BHP's ongoing investment in Escondida's processing infrastructure also creates a credible pathway for modest throughput improvements, even if underlying grade continues to trend lower. Monitoring global copper production trends from other producing nations will also be essential in determining whether any offsetting supply growth can emerge elsewhere in the near term.

Key Indicators for Market Participants to Monitor

For those tracking copper supply fundamentals, the following leading indicators will signal whether Chile's output trajectory is stabilising or deteriorating further:

- Monthly Cochilco production reports remain the most direct and authoritative data source for tracking individual mine performance

- Codelco capital expenditure disclosures signal management confidence in operational recovery capacity and timeline

- BHP Escondida quarterly operational updates, particularly grade profiles and mill throughput data

- Glencore guidance revisions for Collahuasi, where further downward adjustments would confirm that water and grade challenges are worsening

- Chile government water rights policy developments in the Atacama region, which could simultaneously affect multiple major operations

- Global sulfuric acid pricing trends, functioning as a real-time proxy for input cost pressure across Chile's oxide copper processing operations

Additionally, Trading Economics' Chile copper production data offers a useful real-time reference for tracking official monthly output figures as new Cochilco releases become available.

Frequently Asked Questions

Why is Chilean copper output falling so sharply in 2026?

The decline reflects four overlapping pressures: structural ore grade deterioration at major porphyry deposits, operational disruptions following a fatal incident at El Teniente in July 2025, water supply constraints at Collahuasi in the Atacama region, and rising input costs driven by sulfuric acid supply tightness across oxide processing operations.

Which Chilean copper mines have been most severely affected?

BHP's Spence mine recorded the steepest quarterly decline at 34.4% in Q1 2026, followed by Codelco's El Teniente at 26.5% and Collahuasi at 19.3% in May 2026. BHP's Escondida, the world's largest copper mine, fell 17.6% in May 2026 alone.

What does Chile's copper output decline mean for copper prices?

Sustained supply contraction from a nation responsible for roughly a quarter of global mined copper, combined with accelerating demand from electrification and digital infrastructure buildout, creates upward pressure on copper price floors. The tightening supply-demand balance supports a constructive medium-term price outlook.

Can Chilean copper production recover quickly?

Partial recovery is possible as El Teniente normalises operations. However, ore grade deterioration, which is the primary structural driver, is a geological reality that cannot be quickly reversed. Full recovery to pre-2026 output levels would require either major new mine development or significant processing technology improvements, neither of which delivers results in the near term.

Summary: What the Numbers Are Telling the Market

- Chile's national copper output fell 12.9% year-on-year in May 2026 to 423,623 metric tonnes, following declines of 13.8% in April and 9% in March

- The world's largest copper producer (Codelco) and the world's largest copper mine (BHP's Escondida) both recorded double-digit output declines in the same month

- Four distinct forces are driving the contraction: geological grade decline, safety-related operational disruption, water scarcity, and sulfuric acid input cost pressure

- Glencore reduced its 2026 copper guidance by 90,000 tonnes, confirming the supply shortfall extends beyond a single operator

- Chile's Q1 2026 GDP contracted for the first time since 2023, with mining weakness as a primary contributing factor

- Greenfield development timelines of 10 to 15 years mean near-term supply relief from new projects is structurally impossible

This article is intended for informational purposes only and does not constitute financial advice or a solicitation to trade in any financial instrument. Readers should conduct their own due diligence before making investment decisions. Production forecasts, price scenarios, and market projections involve inherent uncertainty and may not reflect actual outcomes.

Want to Know Which ASX Copper Explorers Could Benefit From Chile's Supply Crisis?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries — including copper — and delivering actionable alerts before the broader market has a chance to react. Explore historic discovery returns on Discovery Alert's dedicated discoveries page to understand the scale of opportunity that major mineral finds can generate, and begin your 14-day free trial today to position yourself ahead of the next significant ASX copper discovery.