July 11, 2026

The Geological Clock Is Running Out on the World's Copper Heartland

There is a concept in mining economics called the "grade treadmill" — the phenomenon where producers must process ever-increasing volumes of ore just to maintain flat output levels, because the copper concentration in each tonne of rock keeps declining. For decades, Chile ran ahead of this treadmill through sheer scale, world-class deposits, and continuous investment. In 2026, the treadmill is winning.

Understanding why Chile copper output falls sharply across top miners requires looking past any single month's data or any individual operational disruption. The story is geological, structural, and long in the making — and its implications extend well beyond Santiago or Santiago's copper commission offices into every corner of the global energy transition supply chain.

When big ASX news breaks, our subscribers know first

Chile's 2026 Production Data: A Pattern That Demands Attention

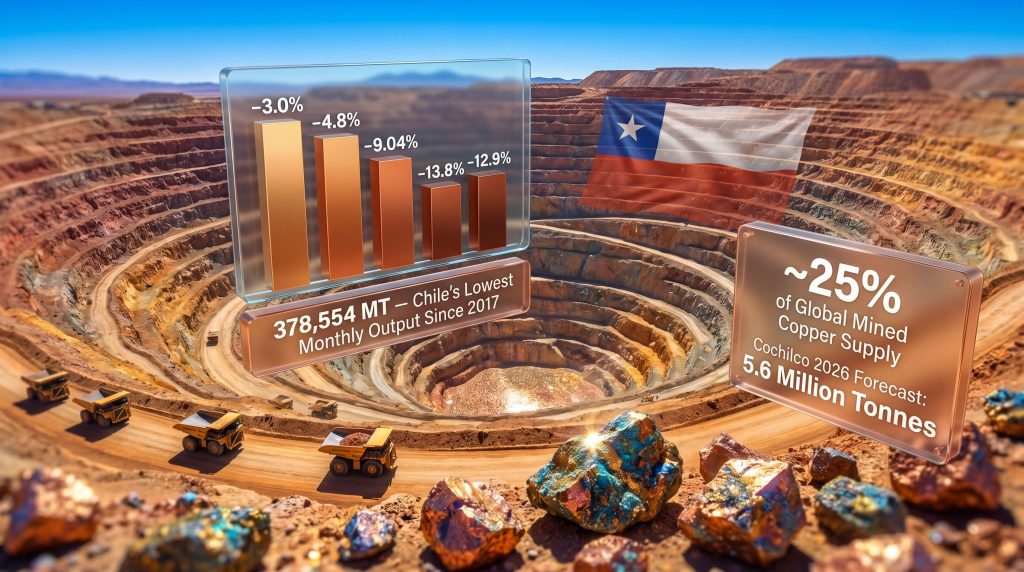

Monthly output figures from Cochilco, Chile's state copper commission, tell a remarkably consistent story through the first half of 2026. What began as a modest contraction in January has deepened into double-digit year-on-year declines by the second quarter:

| Month | Output (Metric Tons) | YoY Change |

|---|---|---|

| January 2026 | 413,712 | −3.0% |

| February 2026 | 378,554 | −4.8% |

| March 2026 | 434,314 | −9.04% |

| April 2026 | 399,954 | −13.8% |

| May 2026 | 423,623 | −12.9% |

The February 2026 reading of 378,554 metric tons represented the lowest monthly copper output Chile had recorded since March 2017 — a nine-year low that strips away any argument that these figures represent routine variance.

What makes this data particularly significant is the acceleration of the decline rate. A three percent contraction in January is manageable within normal operational tolerances. A sustained double-digit contraction across April and May, with no single catalytic event to blame, points toward something far more durable. Furthermore, the Chile copper price outlook remains deeply intertwined with how quickly these production trends can be reversed.

Cochilco's full-year 2026 production forecast sits at 5.6 million tonnes, a figure that already embeds a recovery assumption for the second half of the year. Given that the first five months have tracked consistently below trajectory, that assumption is being stress-tested with each passing week.

The Grade Problem: What Ore Concentration Decline Actually Means

Understanding Copper Ore Grades

For non-specialists, ore grade refers to the percentage of actual copper metal contained within each tonne of extracted rock. A deposit grading at 1.0% copper yields ten kilograms of recoverable copper per tonne of ore processed. A deposit at 0.5% yields five kilograms per tonne — meaning you need to mine, crush, and process twice the rock to get the same output.

Chile's major open-pit copper mines were developed during an era when ore grades in the Atacama and surrounding regions were genuinely exceptional by global standards. Deposits like Escondida, El Teniente, and Collahuasi were world-class precisely because of their high-grade ore bodies near surface. Decades of production have consumed the highest-grade material, and operations have progressively moved deeper and into lower-grade zones.

This is not a Chilean anomaly — it is a global copper mining phenomenon. The average ore grade of copper deposits being mined worldwide has fallen from roughly 1.6% in the 1990s to around 0.6% today across many major producing regions. Chile's mines are experiencing this trajectory in concentrated form, given how long and intensively they have been operated.

The Processing Cost Multiplier

Lower ore grades do not merely reduce output — they multiply costs across the entire mining value chain:

- More ore must be blasted, loaded, and transported to yield the same copper

- Processing plants must handle greater throughput, consuming more water and energy per unit of copper produced

- Tailings volumes increase, creating greater storage and environmental management obligations

- Acid consumption in heap-leach operations rises disproportionately as grades fall

- Capital intensity per pound of produced copper escalates, compressing margins even at elevated copper prices

In Chile's arid northern regions, where most major copper operations are concentrated, water scarcity compounds the grade problem. As mines require more water to process lower-grade ore, they face increasing competition for a resource that is already critically constrained in the Atacama Desert environment.

Mine-by-Mine Analysis: Where the Losses Are Concentrated

Codelco's Aging Asset Portfolio

Codelco, the state-owned entity that remains the world's largest copper producer by reserve base, recorded a 7.5% year-on-year decline in Q1 2026 aggregate output. Its El Teniente mine in the Andes delivered a particularly steep contraction of 29.5% versus January 2025 performance levels. El Teniente is the world's largest underground copper mine by production volume — a distinction that reflects both its scale and the extraordinary engineering required to operate at depth.

May 2026 data showed Codelco's total output falling 18.3% year-on-year to just 106,300 metric tonnes. For a company that underpins Chile's national treasury through dividend payments to the government, sustained underperformance of this magnitude carries fiscal implications that extend well beyond the mining sector. The Codelco production strategy will consequently be under intense scrutiny as the year progresses.

Codelco has publicly acknowledged the need for a major capital restructuring to modernise its legacy asset portfolio, including deep-level mine transitions that convert aging open-pit operations to block-cave underground mining configurations. These transitions are technically complex, multi-billion dollar undertakings that unfold over years rather than quarters.

BHP's Escondida and Spence: Different Problems, Same Trend

BHP (ASX: BHP) operates two of Chile's most consequential copper assets, and both delivered disappointing 2026 results:

| BHP Asset | May 2026 Output | YoY Change |

|---|---|---|

| Escondida | 108,800 tonnes | −17.6% |

| Spence | Not disclosed for May | −34.4% (Q1 basis) |

Escondida, operating near Antofagasta in northern Chile, is the world's single largest copper mine by annual output. Its May 2026 production of 108,800 metric tons represented a 17.6% year-on-year decline. Escondida also recorded a 9.3% contraction in Q1 2026, suggesting the deterioration is not confined to a single operational quarter.

Spence's 34.4% year-on-year decline in Q1 2026 is among the steepest recorded at any major Chilean copper asset in recent years. Spence has undergone significant capital investment through the Spence Growth Option project, which expanded sulphide ore processing capacity. Despite this investment, production metrics have deteriorated materially, pointing to ore quality challenges that capital expenditure alone cannot fully offset.

Collahuasi: Volatility Around a Declining Mean

The Collahuasi joint venture, operated by Anglo American and Glencore in northern Chile's Tarapaca region, illustrates how dramatically individual mine performance can oscillate even within a declining overall trend. After posting a 16% output surge in March 2026 that briefly bucked the national trajectory, Collahuasi reverted sharply in May with a 19.3% year-on-year decline to 31,000 metric tonnes.

This volatility is characteristic of large open-pit operations where ore feed quality, plant utilisation rates, and maintenance scheduling can produce significant month-to-month variation. However, the May result confirms that the March surge was episodic rather than the beginning of a sustained recovery.

Expansion Projects That Were Supposed to Solve the Problem

Quebrada Blanca's Troubled Ramp-Up

One of the most closely watched developments in Chilean copper has been the ramp-up of Teck Resources' Quebrada Blanca Phase 2 (QB2) expansion in Chile's Tarapaca region. Originally conceived as a transformative addition to Chilean copper supply, QB2 had its 2026 production guidance cut substantially — from an original range of 280,000 to 310,000 tonnes down to 200,000 to 235,000 tonnes.

The primary driver of this guidance reduction has been complications with waste storage infrastructure and delays in achieving optimised throughput rates. This is not an uncommon challenge in large-scale mine expansions, but the timing is particularly unfortunate given that QB2's incremental production was supposed to partially offset the grade-driven losses at legacy operations.

Structural Insight: When expansion projects fail to hit their production targets precisely at the moment legacy assets are contracting, the compounding effect on national output can be severe. Chile is currently experiencing both sides of this equation simultaneously.

Why New Mines Take So Long to Matter

Even if new exploration discoveries were made in Chile today, the timeline from discovery to first production at a major greenfield copper project typically spans 15 to 20 years when accounting for:

- Resource definition drilling and feasibility studies (3 to 5 years)

- Environmental and permitting processes (2 to 7 years, highly variable)

- Construction and commissioning (3 to 5 years)

- Ramp-up to nameplate capacity (1 to 3 years)

Consequently, the new copper project pipeline globally is insufficient to compensate for near-term losses at established producers. This pipeline reality means the copper supply available in the 2030s is largely determined by decisions and discoveries made today — and those decisions are not being made at the pace the market will eventually require.

What This Means for Global Copper Markets

Supply Concentration Risk in a Critical Mineral

Chile's position supplying approximately 25% of global mined copper means its structural output decline creates a geographic concentration problem for downstream industries that is difficult to solve quickly. Chile's copper supply gap is increasingly recognised as one of the most consequential near-term risks in global commodity markets. Alternative producing nations face their own constraints:

- Peru, the world's second-largest copper producer, has faced persistent community opposition and operational disruptions at several major assets

- The Democratic Republic of Congo, home to significant copper growth potential, is navigating complex regulatory terrain — as evidenced by tax authorities sealing offices at Glencore's Kamoto Copper operation in mid-2026 over an alleged payment dispute

- Australia holds meaningful copper reserves but lacks the near-term production scale to compensate for Chilean losses

The Demand Acceleration Problem

Chile copper output falls sharply across top miners at precisely the wrong moment — during a period of accelerating structural copper demand driven by electrification. Electric vehicles require roughly three to four times more copper than internal combustion engine equivalents. Grid infrastructure upgrades, offshore wind installations, and solar panel manufacturing all require substantial copper inputs that are non-substitutable in current technology configurations.

Prominent mining investor Frank Giustra has publicly stated that the copper market will need approximately six new mines brought into production every year through 2050 to satisfy projected demand growth — a figure that highlights the gap between what the industry is currently delivering and what the energy transition mathematically requires. In addition, the broader copper supply crunch is compounding these challenges at a global level.

Macquarie analysts noted in July 2026 that copper prices have been running ahead of near-term physical market fundamentals, with global stockpiles continuing to build even as Chilean production contracts. This apparent contradiction reflects the market pricing forward scarcity rather than current surplus — a dynamic that has historically preceded significant price dislocation when inventory buffers exhaust.

The Grade Treadmill at a Global Scale

What Chile is experiencing at a national level is a microcosm of the challenge facing the entire global copper mining industry. As higher-grade, near-surface ore bodies are depleted worldwide, the industry is progressively forced to:

- Process lower-grade material at higher cost

- Access deeper ore zones requiring more energy-intensive extraction methods

- Develop deposits in geologically or jurisdictionally challenging locations

- Invest in technologies like in-situ recovery and bioleaching that can unlock previously uneconomic ore bodies

None of these solutions are quick, cheap, or logistically simple — and collectively, they suggest that the cost of producing copper is structurally rising, independent of commodity price cycles.

The next major ASX story will hit our subscribers first

Investor and Strategic Implications

Reading the Data as a Forward Indicator

For commodity analysts and investors, Chile's 2026 monthly production data functions less as a snapshot of current conditions and more as a leading indicator of multi-year supply constraints. Five consecutive months of year-on-year decline, accelerating in magnitude, with no single correctable cause, is a fundamentally different signal than a one-month disruption from a labour dispute or weather event.

Important Disclaimer: This article contains forward-looking assessments based on publicly available production data and analyst commentary. Commodity markets are influenced by numerous variables including macroeconomic conditions, policy changes, and technological developments. This content does not constitute financial advice.

Key variables worth monitoring for investors tracking the Chilean copper situation include:

- Monthly Cochilco production reports and whether the rate of year-on-year decline stabilises, deepens, or reverses through H2 2026

- Quebrada Blanca's progress toward its revised 2026 production guidance range

- Codelco's capital allocation announcements related to its legacy asset transformation programme

- Water access and environmental permitting timelines for proposed processing expansions across northern Chile

- Copper inventory levels at LME and COMEX warehouses as a near-term demand signal

The Longer-Duration Thesis

The structural thesis for copper is not new, but Chile's 2026 data provides increasingly concrete evidence that the supply side of the equation is eroding in real time. The combination of declining ore grades at legacy operations, underperforming expansion projects, and a global development pipeline that cannot match projected demand growth creates conditions that fundamentally support elevated copper prices over a multi-year horizon — even if near-term price movements remain subject to inventory dynamics and macroeconomic sentiment.

Chile's copper sector is not collapsing. It remains the world's most important single source of mined copper. However, the era of volume-driven output growth from existing Chilean deposits appears to be giving way to a new phase characterised by higher costs, lower grades, and the ongoing challenge of replacing what geology is progressively taking away.

Production data referenced in this article is sourced from Cochilco (Chile's state copper commission). Additional market context draws on reporting and analyst commentary published by Mining.com. Readers seeking further detail on Chile's copper production statistics can access Cochilco's official data portal directly.

Want to Know Which ASX Copper Explorers Could Benefit From Chile's Supply Crunch?

As Chilean copper output continues its structural decline, the opportunity to identify the next significant ASX copper discovery has never been more compelling. Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries the moment they are announced, turning complex geological data into actionable insights — and you can explore why major copper discoveries have historically generated extraordinary returns on Discovery Alert's dedicated discoveries page. Begin your 14-day free trial today and position yourself ahead of the market.