July 11, 2026

Nevada's Copper-Gold Porphyry Landscape: Why Most Deposits Stay Buried

Porphyry copper-gold systems represent some of the largest accumulations of economic metal on Earth, yet the majority never reach production. The obstacle is rarely geological. It is almost always metallurgical, financial, or logistical. When all three barriers dissolve simultaneously, a deposit that sat dormant for decades can transform into a commercially compelling mine almost overnight. That convergence is precisely what is unfolding at the P2 Gold Gabbs project in Nye County, Nevada, a copper-gold deposit types that prior operators understood well enough to drill but never well enough to develop.

When big ASX news breaks, our subscribers know first

What Makes the Gabbs Project Geologically Distinct From Nevada's Gold Mines

The vast majority of Nevada's gold production has come from tertiary epithermal systems, relatively young volcanic deposits where gold precipitated from hydrothermal fluids into fracture zones and fault structures. These are the types of deposits that built the Carlin Trend and the Walker Lane's historical reputation. The P2 Gold Gabbs project sits in an entirely different geological category.

Gabbs is hosted in Jurassic-age rocks, roughly 150 to 180 million years old, formed as part of an ancient oceanic island arc that was subsequently accreted onto the western margin of the North American continent. A monzonite or porphyry intrusive system then penetrated this island arc terrane, creating the copper-gold mineralisation that exists across the property today. The age difference alone, tens of millions of years older than the surrounding epithermal systems, places Gabbs in a completely separate genetic category from its neighbours.

This geological distinction has a practical consequence. The deposit exhibits the structural geometry and mineralogy of a classic copper-gold porphyry rather than a high-sulphidation or low-sulphidation epithermal system. That means broader, more continuous mineralisation at lower grades distributed across enormous tonnages, rather than the high-grade, narrow veins that characterise epithermal mining. The tradeoff is one of scale versus grade, and at Gabbs, scale is the thesis.

Porphyry Ore-Control Geometry and What It Means for Resource Confidence

One of the more technically valuable aspects of the Gabbs deposit is its predictable ore-control geometry. Across multiple drill holes at both the Sullivan and Lucky Strike zones, the same pattern repeats: a barren gabbro hanging wall transitions downward into mineralised quartz monzonite, which carries the economic copper-gold values. This consistency, described by the on-site team as almost repetitious in its reliability, is exactly what a resource geologist wants to see.

When the same ore-control marker appears hole after hole, it means the geological model is robust and drilling surprises are rare. The uppermost 10 to 30 feet of the monzonite horizon consistently carries the highest-grade material, which also simplifies mine planning by concentrating the richest ore near the top of each mineralised interval. A regional analogue at the Ann Mason copper deposit near Yerington, approximately 100 miles to the north, displays a similar geochemical signature and provides a rare three-dimensional cross-section of what a deeply exposed porphyry system of this type looks like from top to bottom.

The SART Processing Breakthrough and Why It Changes the Economics

The history of the Gabbs district is, in part, a history of missed timing. Operators working the ground in the 1980s and 1990s encountered the same copper-gold association that P2 Gold is developing today. The problem was not the ore. It was the process plant. When gold and copper occur together in a heap-leach cyanide circuit, copper consumes cyanide at a disproportionate rate, dramatically inflating reagent costs and destroying the economics of gold recovery.

Without a reliable way to handle both metals simultaneously, prior operators were forced to treat the deposit as either a copper play or a gold play, and neither worked independently at economic scale. Furthermore, understanding cut-off grade economics in a dual-metal system like this one is essential to appreciating why earlier development attempts fell short.

SART technology, an acronym for Sulfidization, Acidification, Recycling, and Thickening, resolves this problem directly. The SART circuit strips copper from the cyanide solution before it can consume the reagent, precipitates it as a copper sulphide product, and then recycles the recovered cyanide back into the leach circuit. The result is simultaneous copper and gold recovery from a single heap-leach operation, with the copper effectively paying back much of the cyanide cost rather than destroying it.

The practical significance is substantial: a characteristic that made Gabbs uneconomic under one processing regime becomes a revenue diversifier under another. SART processing converts the copper-gold association from a technical barrier into a by-product credit that strengthens the overall financial model.

Resource Scale Across the Three Known Zones

The P2 Gold Gabbs project covers approximately 4,500 hectares across 543 unpatented and one patented lode mining claims in Nye County. Three distinct mineralised zones have been identified within this footprint.

| Resource Zone | Estimated Tonnage | Current Status |

|---|---|---|

| Sullivan | ~80-90 million tonnes | Defined; 24-hole infill program underway |

| Lucky Strike | 120-150 million tonnes (management estimate) | Expansion drilling active; 47 holes planned |

| Gold Ledge | Not yet quantified | Between permit areas; drilling deferred |

| Total Project Target | 150-200+ million tonnes | Across all zones combined |

The grade profile across the deposit averages approximately 0.5 to 0.6 grams per tonne gold and 0.2 to 0.3 percent copper, with an estimated silver credit of three to four million ounces over the life of the mine. These are not high-grade numbers by narrow-vein standards, but in a bulk-tonnage porphyry context, they are commercially meaningful when applied to 150 million tonnes or more of mineralised material.

Lucky Strike: The Zone That Keeps Expanding

When the current programme launched, Sullivan was the better-drilled and better-understood zone. Lucky Strike had seen comparatively little historical work despite displaying very similar surface characteristics. That asymmetry represented an exploration opportunity rather than a concern, since the underlying geological framework was already established.

Infill drilling at Lucky Strike has progressively confirmed grade continuity and structural extensions that historical programmes simply did not test. One standout intercept from the current programme returned a broad interval of approximately 175 feet averaging roughly one gram per tonne gold, with a richer sub-interval of 65 feet at approximately two grams per tonne gold and 0.35 percent copper. Within that sub-interval sits a high-grade core of five feet, or approximately 1.52 metres, at 183 grams per tonne gold and 4.0 percent copper.

Visible gold was also identified in the core from this interval, a detail not commonly associated with bulk-tonnage porphyry intercepts and one that signals locally elevated free gold rather than purely refractory mineralisation. The project team's current assessment is that Lucky Strike will ultimately eclipse Sullivan in total tonnage, potentially reaching the 120 to 150 million tonne range once the full thickness of the system has been drilled.

Gold Ledge, the third zone situated between Sullivan and Lucky Strike, remains unquantified. Current permitting constraints require the two active permit areas to remain at least one mile apart, which temporarily limits work in the ground between them. A third permit application for Gold Ledge represents future upside that is not yet captured in any resource estimate.

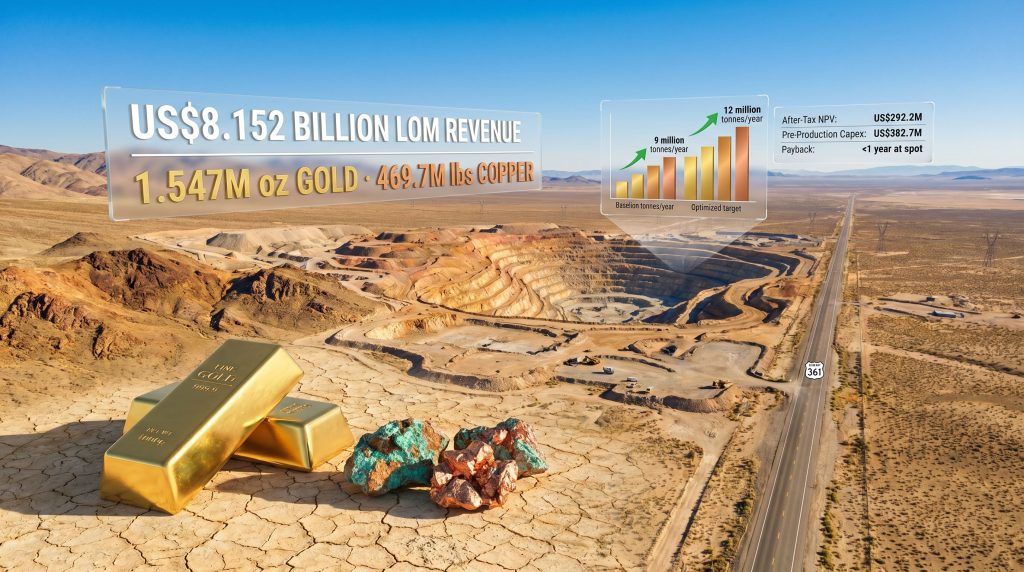

How the Optimised Mine Plan Compares to the Original PEA

The existing preliminary economic assessment established a baseline for the project, but the development team has been explicit that it represents a starting point rather than a finished blueprint. The optimisation work underway targets two specific changes that materially alter the project's financial profile.

| Metric | PEA Baseline | Optimised Target |

|---|---|---|

| Throughput | 9 million tonnes per year | 12 million tonnes per year |

| Mill Start-Up | Year 6 | Year 3 |

| Average Annual Gold Production | ~110,000 oz | 150,000+ oz |

| Mine Life | 14.2 years | Under review |

| After-Tax NPV (5% discount) | US$292.2 million | To be updated in feasibility study |

| Pre-Production Capital | US$382.7 million | Under feasibility review |

| LOM Revenue | US$8.152 billion | Upward revision expected |

| Payback Period | Less than 1 year at spot | Maintained or improved |

Increasing throughput from nine to twelve million tonnes per year lifts annual gold production by roughly 35 percent. Pulling the mill start-up forward from year six to year three accelerates cash generation and shortens the payback window. When combined with infill grades at Lucky Strike running above historical averages, the case for upward revision in the definitive feasibility study is clear. It is worth noting, however, that these are management targets rather than completed study outputs, and investors should treat them as directional rather than confirmed until the feasibility study is published.

Infrastructure: What Is Already Solved Before Construction Begins

One of the genuinely differentiated characteristics of the P2 Gold Gabbs project is the degree to which infrastructure is already in place. For most greenfield mining projects, infrastructure is the largest single risk item on the development schedule, requiring years of engineering, permitting, and capital expenditure before a single tonne of ore is processed.

| Infrastructure Element | Status at Gabbs | Typical Greenfield Requirement |

|---|---|---|

| Paved road access | In place (Highway 361) | Often requires new road construction |

| Power transmission | Lines cross claim block | May require 20-50+ mile line extension |

| Water rights | Secured | Typically a multi-year application process |

| Historical drill roads | Extensive on-site network | None; all disturbance is new |

| Nearby workforce | Gabbs, Hawthorne (45 min), Fallon (60 min) | May require fly-in/fly-out infrastructure |

The water rights position is particularly notable given the hydrogeological challenge the project faces. Groundwater sits at approximately 400 to 450 feet below surface, while the planned pit extends to roughly 1,000 feet. Pit dewatering will be required, and production wells and monitoring bores are currently being drilled at both zones to characterise the aquifer ahead of pump testing.

The nearby Paradise Peak pit, a historic operation that produced approximately 40 million ounces of silver and one million ounces of gold before encountering sulphide ore, provides a real-world local precedent for managing water in a Nevada pit of comparable depth.

There is also a less obvious permitting benefit embedded in the historical drill road network. Under current environmental baseline protocols, only new ground disturbance counts against threshold calculations. Since the existing road network across the Gabbs claim block was created by prior operators, P2 Gold's ongoing drilling programme is not creating the same permitting exposure that a genuinely greenfield operator would face.

The nearby community of Gabbs, home to what is understood to be one of the longest continuously operating mines in the United States, provides a local workforce already oriented toward mining rather than one that needs to be built from scratch. Larger population centres at Hawthorne and Fallon extend that labour pool further.

The next major ASX story will hit our subscribers first

Permitting Strategy and Development Timeline

Nevada's mining claims framework is one of the more well-understood regulatory environments in the global mining industry. The process is structured and predictable, even if not fast. P2 Gold's stated approach has been to run baseline studies, engineering work, and metallurgical test programmes concurrently rather than sequentially, compressing the timeline without cutting corners.

The dual-permit structure, one application for Sullivan and a separate one for Lucky Strike, reflects the regulatory requirement that the two active areas remain separated by at least one mile. Both permit applications are being advanced in parallel, which is itself a form of risk management: if one application encounters a delay, the other continues moving forward.

Development milestone schedule:

| Milestone | Target Date |

|---|---|

| Updated Mineral Resource Estimate | Q3 2026 |

| Feasibility Study Completion | Q4 2026 |

| Full Project Permitting | End of 2027 |

| Construction Commencement | 2027-2028 |

| First Production (Heap-Leach Oxide) | Late 2027 to Early 2028 (CEO guidance) / 2029 (project guidance) |

The staged heap-leach start for oxide material is a deliberate capital efficiency strategy. Oxide ore, which is fully oxidised near surface, responds to conventional heap-leach cyanidation without requiring a ball mill or flotation circuit. Starting with oxides allows revenue generation and cash flow to begin well before the larger and more capital-intensive sulphide processing facility is commissioned. The feasibility study, once complete, feeds directly into the Mining Plan of Operation and establishes the technical terms of reference for the subsequent Environmental Impact Statement process.

Financing Structure: NSR Royalties as an Alternative to Equity

Capital markets for mining development have increasingly moved toward royalty and streaming structures as alternatives to large equity raises. For a project requiring approximately US$382.7 million in pre-production capital, the dilution implied by a conventional equity raise would be substantial at current market valuations.

P2 Gold is pursuing approximately US$290 million in construction financing through the sale of a net smelter returns royalty. This structure transfers a percentage of future revenue to the royalty buyer in exchange for upfront capital, without requiring the issuing company to issue new shares. Franco-Nevada holds an existing 2 percent NSR royalty on the project, with a US$6.5 million repurchase option attached.

Royalty financing has become increasingly standard for mid-scale development projects precisely because it preserves equity value for existing shareholders while providing the capital needed to advance construction. The trade-off is a permanent revenue sharing obligation rather than a one-time dilution event.

Key Risks Investors Should Understand

No development-stage project is without risk, and a balanced assessment of the P2 Gold Gabbs project requires acknowledging where uncertainty remains.

| Risk Category | Nature of Risk | Mitigation in Place |

|---|---|---|

| Hydrogeology | Groundwater at 400-450 ft; pit depth to 1,000 ft | Production and monitoring wells being drilled; pump testing planned |

| Metallurgical | SART circuit operational complexity | Metallurgical test work well advanced |

| Permitting | Dual-permit structure; Gold Ledge deferred | Concurrent rather than sequential permitting |

| Commodity price | Revenue split across gold, copper, silver | Diversified by-product credit structure |

| Capital | US$382.7M pre-production capex | NSR royalty financing pathway identified |

The hydrogeology question deserves particular attention. A 1,000-foot pit that intersects an aquifer at 400 to 450 feet requires a long-term dewatering programme, which adds both capital and operating cost. Furthermore, interpreting drill results from zones with variable water ingress adds an additional layer of complexity to resource modelling. The current well programme is designed to quantify this challenge before the feasibility study is finalised, not after. That sequencing is appropriate.

This article contains forward-looking statements and financial projections based on management guidance and a preliminary economic assessment. Readers should not treat these figures as guarantees of future performance. Mining projects carry inherent geological, financial, permitting, and operational risks. Independent due diligence is recommended before making any investment decision.

Where the P2 Gold Gabbs Project Stands Among Nevada's Development Assets

Measuring any development-stage asset requires looking at several dimensions simultaneously rather than reducing it to a single metric. On scale, the Gabbs project targets life-of-mine gold production of 1.547 million ounces and 469.7 million pounds of copper across an estimated total revenue profile of US$8.152 billion. On infrastructure, the project enters feasibility with road access, power transmission, secured water rights, and a workforce community already in place. On geology, the ore-control pattern is predictable, the regional analogues are well understood, and the resource model has held up consistently across a growing drill hole database.

The combination of a sub-one-year payback period at spot gold and copper prices, a staged heap-leach entry point that reduces initial capital requirements, and a Lucky Strike zone that keeps delivering results above historical expectations places the project in a commercially meaningful production tier for the current gold and copper price environment.

What remains to be confirmed is the updated resource estimate in Q3 2026, the feasibility study in Q4 2026, and the permitting outcomes through 2027. Each of these represents a near-term catalyst with the potential to materially re-rate the project. For investors tracking development-stage copper-gold assets in Tier 1 North American jurisdictions, the P2 Gold Gabbs project presents a case study in how the convergence of the right technology, the right infrastructure, and the right commodity price environment can revive ground that prior generations simply could not make work.

Want to Catch the Next Major Copper-Gold Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across 30+ commodities — including copper-gold systems like those reshaping Nevada's development landscape — and delivers actionable alerts directly to subscribers ahead of the broader market. Explore how historic mineral discoveries have generated substantial returns for early movers, and begin your 14-day free trial at Discovery Alert to position yourself at the forefront of the next major find.