June 10, 2026

Global copper markets face a structural shift as the world's premier producer confronts the harsh realities of mining economics in an evolving commodities landscape. The Chilean copper industry, which has anchored global supply chains for decades, now navigates a complex convergence of geological constraints, capital allocation pressures, and technological transformation requirements that fundamentally reshape production trajectories through 2034. This Chile copper output delay represents a critical development that market participants must understand.

Market participants operating under assumptions of steady Chilean copper growth must recalibrate their supply-demand models as production dynamics enter an extended plateau phase. This recalibration extends beyond simple tonnage adjustments to encompass market share redistribution, pricing mechanism evolution, and strategic inventory management across the copper value chain.

Understanding the Fundamental Shift in Production Expectations

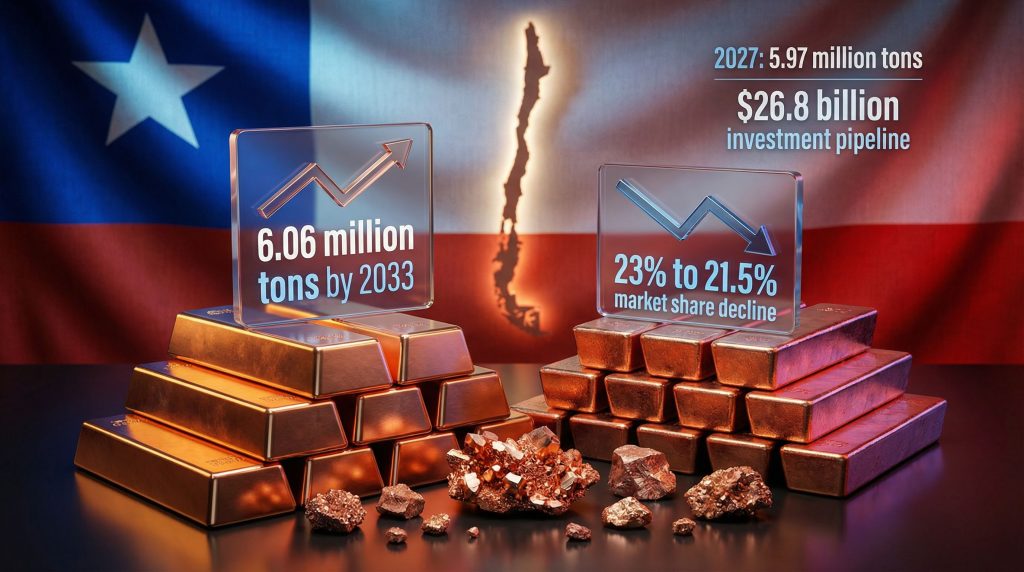

Chilean copper output projections now reflect a mature mining cycle where established operations reach natural depletion thresholds requiring significant capital investment to maintain current production levels. The revised forecasts indicate peak production delayed to 2033 at 6.06 million metric tons, representing a fundamental departure from previous growth trajectories that anticipated reaching 6.07 million tons by 2027.

This timeline extension creates a production stabilisation period through 2031 where output remains at current levels before beginning gradual recovery. The stabilisation reflects the critical threshold where existing mine productivity plateaus, requiring new project execution to offset natural depletion across Chile's mining portfolio.

The market implications extend beyond production volumes to encompass supply chain reliability and pricing volatility. Current copper prices at $5.9125 per pound reflect market recognition of supply constraints, trading significantly above conservative global copper supply forecast that projected pricing near $4.50 per pound for 2026. Meanwhile, these record high copper prices demonstrate the market's response to supply uncertainty.

Quantifying the Forecast Revisions

Chilean production adjustments create measurable gaps between previous expectations and revised reality across the forecast horizon:

| Year | Previous Forecast (2024) | Revised Forecast (2025) | Variance |

|---|---|---|---|

| 2027 | 6.07 million tons | 5.97 million tons | -100,000 tons |

| 2033 | N/A | 6.06 million tons | Peak delayed |

| 2034 | N/A | 5.86 million tons | Post-peak decline |

The cumulative production shortfall between revised and original forecasts creates an estimated gap of 500,000 to 800,000 metric tons over the 2027-2031 period. This represents production capacity that Chile would have delivered under previous projections but will not materialise under current geological and economic constraints.

Market concentration implications emerge as Chile's global production share declines from 23% in 2027 to 21.5% by 2030 before potentially recovering to 27% by 2034, contingent on successful pipeline investment execution.

When big ASX news breaks, our subscribers know first

Why Chile's Copper Output Projections Are Being Scaled Back

The fundamental drivers behind Chile's production revisions reflect structural challenges that extend beyond temporary operational disruptions to encompass long-term geological and economic realities facing mature mining jurisdictions. This Chile copper output delay stems from multiple interconnected factors.

Declining Ore Grade Challenges Across Major Operations

Ore grade degradation represents the primary technical constraint affecting Chilean copper operations, where established mines must process larger volumes of rock to extract equivalent copper quantities. This geological reality creates cascading operational impacts:

- Increased waste rock removal requirements demanding larger-scale extraction equipment

- Greater energy consumption per unit of copper produced, affecting operational economics

- More complex processing requirements necessitating advanced metallurgical techniques

- Higher capital investment thresholds for maintaining production at existing levels

Average copper ore grades globally have declined from approximately 0.8% in the 1990s to current levels where many mature operations work with 0.4-0.5% grades. Chilean major operations experience similar trajectories as deeper extraction becomes necessary to access remaining reserves.

The ore grade challenge fundamentally alters project economics by extending payback periods and increasing the minimum copper price required for project viability. When ore grades decline, mining operators face the mathematical reality that return on investment decreases unless commodity prices rise proportionally.

Mining Plan Adjustments and Operational Realities

Strategic reassessment of extraction methodologies reflects realistic production economics where marginal capacity becomes economically unviable at current commodity price levels. Chilean mining companies have recalibrated operations to prioritise higher-grade deposits while deferring lower-grade development pending improved price environments.

This operational shift toward capital discipline represents lessons learned from the 2015-2016 copper downturn when prices declined below $2 per pound and Chilean mining companies reduced capital expenditures by 40-50%. Current investment caution, despite prices above $5.90 per pound, reflects industry memory of commodity price volatility.

Infrastructure constraints compound operational challenges as existing transportation, power generation, and water supply systems approach capacity limits. The Atacama region, which hosts major Chilean operations, faces particular water availability constraints that restrict expansion capabilities regardless of ore availability.

Investment Pipeline Bottlenecks

The $26.8 billion investment pipeline projected for 2025-2029 faces execution challenges as capital allocation prioritises projects meeting higher return thresholds. The projected 20% decline in 2026 spending despite stated expansion needs indicates that available capital cannot fully execute the planned project slate.

Modern mining investment requires:

- Weighted average cost of capital (WACC) requirements of 8-12% for Chilean copper projects

- Payback period thresholds of 3-5 years for marginal project development

- Alternative investment competition from lithium, gold, and battery materials projects

Capital efficiency requirements reflect investor preference for projects with lower capital intensity and faster payback periods, reducing investment in traditional large-scale, long-duration Chilean copper expansion projects. Furthermore, mineral exploration in copper must now meet more stringent economic criteria.

How Chile's Market Share Evolution Affects Global Copper Supply

Chile's temporary market share decline during the 2027-2030 period creates supply opportunities for competing producers while potentially moderating copper price increases if demand growth remains consistent with historical patterns. This Chile copper output delay fundamentally alters global market dynamics.

Projected Market Share Trajectory Analysis

The market share evolution reflects production delays at existing Chilean operations rather than absolute capacity contraction. Chilean copper production's share trajectory indicates:

"Chile's global copper production share declines from 23% in 2027 to 21.5% by 2030, before potentially recovering to 27% by 2034, contingent on successful pipeline investments materialising."

This trajectory suggests confidence that new pipeline projects will eventually deliver incremental capacity, but acknowledges execution risks that could prevent full recovery scenarios.

If Chile produces 5.97 million metric tons in 2027 while maintaining 23% market share, implied global production reaches approximately 25.96 million metric tons. The decline to 21.5% share with lower absolute Chilean production suggests global output growth from competing producers during the transition period.

Competitive Landscape Implications

Other major copper producers may accelerate projects or maximise capacity utilisation during Chile's supply gap period. This supply elasticity determines the degree of copper price pressure markets experience:

- Peru's operations including Quellaveco (operational since 2022) continue expanding capacity

- Indonesian production at Grasberg maintains significant output levels

- Australian operations at Olympic Dam and Prominent Hill offer expansion potential

- African operations in Democratic Republic of Congo provide alternative supply sources

The competitive response capability of alternative producers determines whether Chile's reduced market share translates into supply shortages or merely market share redistribution without significant price impacts.

Geopolitical Considerations for Copper Supply Security

Chile's temporary market share decline raises strategic considerations for major copper-consuming nations regarding supply chain resilience and critical mineral security. The 1.5% share loss represents approximately 150,000-250,000 metric tons of production capacity that alternative sources must provide.

Supply concentration risks emerge if competing producers cannot efficiently scale production during Chile's plateau period, potentially creating strategic vulnerabilities for copper-dependent industries including renewable energy infrastructure and electric vehicle manufacturing.

What Economic Factors Drive These Production Revisions

Copper industry capital discipline reflects rational investor behaviour when commodity price volatility creates uncertainty about long-term project returns, even at current elevated price levels.

Copper Price Volatility and Investment Decisions

The significant divergence between current copper prices at $5.9125 per pound and conservative industry forecasts creates investment hurdle rate challenges for major mining companies. This 31% premium to forecasted price levels suggests substantial uncertainty about medium-term price trajectories.

Major mining companies typically require returns that accommodate downside commodity price scenarios, increasing project payback periods and reducing the pipeline of projects achieving required return thresholds. Capital allocation models must account for copper price scenarios ranging from $3 per pound to $7 per pound over project lifecycles.

Price uncertainty particularly affects projects with longer development timelines, as the discounted cash flow calculations become increasingly sensitive to commodity price assumptions further into the future. However, Chile registered higher copper output in February according to recent industry reports.

Operational Cost Inflation in Chilean Mining

Chilean mining operations face cost structure evolution where operational expenses have increased such that marginal production expansion requires commodity prices materially above recent historical averages. This cost inflation reflects:

- Labour cost pressures in skilled mining positions where wage inflation exceeds general economic inflation

- Energy price impacts on extraction and processing operations, particularly electricity costs for concentration processes

- Water scarcity premiums affecting operational feasibility in Chile's arid northern mining regions

- Environmental compliance costs increasing as regulatory standards evolve

Chilean mining sensitivity to USD/CLP exchange rate dynamics compounds cost pressures. When the Chilean peso strengthens against the US dollar, operational costs denominated in pesos increase relative to copper revenues in USD, reducing project returns and investment attractiveness.

Capital Efficiency Requirements in Modern Mining

The shift toward higher-return, lower-risk project prioritisation has fundamentally altered Chilean copper investment patterns. Modern mining capital allocation prioritises:

- Modular project development enabling phased investment and risk mitigation

- Technology integration reducing long-term operational costs through automation

- Shorter payback periods minimising exposure to commodity price volatility

- Higher-grade deposit focus maximising return on invested capital

Alternative investment opportunities in lithium extraction, gold mining, and battery materials compete for available capital, requiring copper projects to demonstrate superior risk-adjusted returns to secure funding. Additionally, mining industry innovation trends continue to reshape project evaluation criteria.

Which Specific Projects Could Alter Chile's Copper Trajectory

Chile's production recovery scenario depends entirely on successful execution of 13 fast-tracked copper projects identified for acceleration in 2026, representing the marginal capacity needed to achieve the projected 27% market share by 2034.

Critical Pipeline Projects Under Development

The accelerated project timeline faces execution risks as the projected 20% decline in 2026 spending creates capital constraints that may delay or reduce scope of planned developments. Without successful execution of these projects, Chile's market share remains structurally constrained below current levels.

Pipeline projects must overcome several execution challenges:

- Regulatory approval processes requiring environmental and social impact assessments

- Infrastructure development including power generation, water supply, and transportation

- Technology integration incorporating automation and digital systems

- Skilled labour availability in remote mining locations

The projects represent Chile's strategic response to production challenges, but their success depends on resolving the same geological and economic constraints that created current production delays.

Technology Integration Opportunities

Modern copper mining projects increasingly incorporate advanced technologies that can improve project returns and enable smaller-scale, modular development approaches:

- Autonomous haulage systems reducing labour requirements and improving operational efficiency

- Advanced process control systems optimising extraction efficiency and reducing waste

- Remote operation centres minimising on-site staffing needs in harsh environments

- Real-time grade tracking systems improving ore blending and processing optimisation

Technology adoption can potentially offset some ore grade degradation impacts by improving extraction efficiency and reducing operational costs, but requires significant upfront capital investment that competes with capacity expansion funding.

Infrastructure Development Requirements

Chilean copper expansion faces infrastructure bottlenecks that constrain project development regardless of ore availability or market demand. Critical infrastructure needs include:

- Power generation capacity sufficient for expanded mining and processing operations

- Water resource management systems addressing scarcity in northern mining regions

- Transportation infrastructure capable of handling increased production volumes

- Port facilities with adequate capacity for export logistics

Infrastructure development often requires multi-year timelines that extend beyond individual project schedules, creating coordination challenges across the mining sector.

How Industry Forecasts Compare with Government Projections

Divergent analytical approaches between Chile's government agency Cochilco and industry association Sonami reflect different assumptions about regulatory reform benefits, investment pipeline execution, and geological constraints. This Chile copper output delay creates ongoing forecast uncertainty.

Cochilco vs. Sonami: Divergent Analytical Approaches

The forecast methodology differences highlight fundamental disagreements about Chile's copper production potential:

| Organisation | 2026 Projection | Methodology Focus | Key Assumptions |

|---|---|---|---|

| Cochilco | Conservative stabilisation | Technical/geological data | Ore grade decline continuation |

| Sonami | 5.5-5.7 million tons | Industry investment pipeline | Regulatory reform benefits |

Cochilco's conservative approach reflects technical analysis emphasising geological constraints and operational realities, while Sonami's projections assume more aggressive investment pipeline execution and regulatory environment improvements.

The divergence indicates uncertainty about Chile's ability to overcome structural challenges through policy reform and capital investment, with market participants requiring proof of execution before accepting optimistic scenarios.

Regulatory Environment Impact Assessment

Administrative streamlining and environmental approval process improvements could potentially accelerate project timelines, but regulatory reform benefits remain theoretical until demonstrated through actual project execution.

Regulatory factors affecting Chilean mining investment include:

- Environmental approval timelines averaging 2-4 years for major projects

- Social licence requirements necessitating community engagement and benefit-sharing

- Tax policy stability affecting long-term investment attractiveness

- Mining code modifications potentially improving investment terms

The gap between regulatory reform promises and implementation reality creates execution risk that conservative forecasters incorporate into their projections.

Market Confidence Indicators

Investment community response to revised forecasts reflects cautious assessment of Chilean copper sector prospects, with credit rating implications and international investor sentiment requiring demonstration of improved execution capability.

Market confidence metrics include:

- Credit spreads on Chilean mining company debt reflecting perceived execution risks

- Equity valuations of Chilean mining companies relative to international peers

- Foreign direct investment flows into Chilean mining sector projects

- Capital market access for Chilean mining project financing

Sustained market confidence requires consistent delivery of production targets and successful project execution rather than revised forecasts and regulatory promises. In this context, Chile delays copper output peak according to recent industry analyses.

The next major ASX story will hit our subscribers first

What Are the Long-Term Implications for Global Copper Markets

Chile's production delays occur during accelerating global copper demand growth from electrification trends, renewable energy infrastructure, and electric vehicle adoption, creating structural supply-demand imbalances through 2034.

Supply-Demand Balance Projections Through 2034

Global copper demand growth projections of 2-3% annually through 2030 from electrification infrastructure development contrast with Chilean supply constraints, creating cumulative shortfalls that alternative producers must address.

The supply gap implications include:

- Strategic stockpiling considerations by major consuming nations building copper inventories

- Alternative supply source development acceleration in Peru, Indonesia, and Africa

- Recycling infrastructure investment improving secondary copper supply capabilities

- Demand destruction scenarios where higher prices reduce consumption in price-sensitive applications

Supply-demand balance projections must account for the time lag between investment decisions and production delivery, as new copper projects typically require 5-10 years from initial investment to first production.

Price Trajectory Modelling Under Different Scenarios

Copper price modelling incorporating Chilean production delays suggests three primary scenarios through 2034:

Base Case Scenario:

- Chilean production stabilises with gradual recovery post-2031

- Alternative producers provide partial supply gap coverage

- Copper prices average $6-7 per pound with increased volatility

Upside Scenario:

- Chilean pipeline investments materialise ahead of schedule

- Global demand growth moderates due to technology substitution

- Copper prices stabilise in $5-6 per pound range

Downside Scenario:

- Chilean projects face additional delays

- Global demand exceeds supply growth

- Copper prices exceed $8 per pound creating demand destruction

Investment Strategy Implications

Portfolio allocation strategies must account for copper supply constraints affecting sector valuations and geographic concentration risks in mining investments. Understanding effective copper investment strategies becomes crucial during these market shifts.

Strategic investment considerations include:

- Diversification requirements across multiple copper-producing regions

- Technology exposure to companies enabling copper extraction efficiency improvements

- Downstream integration into copper-consuming industries benefiting from supply constraints

- Alternative material exposure to potential copper substitutes in specific applications

Risk assessment frameworks must incorporate geological depletion risks, regulatory uncertainty, and capital allocation efficiency across global mining portfolios.

Frequently Asked Questions About Chile's Copper Production Outlook

When Will Chile Reach Peak Copper Production?

Chile's updated production timeline shows peak output delayed to 2033 at 6.06 million metric tons, representing a multi-year delay from previous projections targeting 2027. This timeline reflects realistic assessment of ore grade challenges, infrastructure constraints, and capital deployment requirements.

Factors that could accelerate this timeline include successful fast-tracking of the 13 identified copper projects, improved regulatory approval processes, and sustained copper prices above $6 per pound justifying accelerated investment.

Conversely, further delays could result from continued capital allocation constraints, additional regulatory hurdles, or commodity price volatility reducing investment attractiveness for marginal projects.

How Reliable Are These New Forecasts?

Cochilco's track record in previous production forecasting provides mixed reliability indicators, with historical projections often requiring revision due to changing market conditions, technological developments, and operational realities.

Forecast reliability factors include:

- Geological data accuracy improving with advanced exploration techniques

- Economic modelling assumptions requiring regular updating based on market conditions

- Regulatory environment stability affecting project execution timelines

- Technology adoption rates influencing operational efficiency improvements

Sensitivity analysis suggests current forecasts incorporate conservative assumptions about investment execution and operational efficiency, potentially understating production potential if conditions improve.

What Does This Mean for Copper Prices?

Chilean supply constraints during accelerating global demand growth create structural upward pressure on copper pricing through the forecast horizon. Current pricing above $5.90 per pound reflects market recognition of supply limitations relative to demand growth expectations.

Price trajectory implications include:

- Medium-term price support from supply constraints offsetting demand fluctuations

- Increased volatility as supply-demand imbalances create price sensitivity to operational disruptions

- Investment incentive pricing required to justify new project development in challenging geological conditions

Hedging strategies for copper price exposure must account for structural supply constraints supporting higher average pricing while preparing for increased volatility around trend levels.

Disclaimer: This analysis is based on publicly available information and industry forecasts. Actual production levels, market conditions, and commodity prices may differ significantly from projections. Investment decisions should not be based solely on these forecasts and require comprehensive due diligence and professional investment advice.

Ready to Capitalise on Copper Supply Disruptions?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant ASX copper discoveries, empowering subscribers to identify actionable opportunities ahead of broader market recognition of supply constraints. With Chile's production delays creating structural opportunities in copper markets, explore Discovery Alert's discoveries page to understand how historic mineral discoveries have generated substantial returns, then begin your 30-day free trial to position yourself strategically in today's evolving copper landscape.