August 6, 2026

When the World's Copper Giant Stumbles, Everyone Feels It

Global commodity markets operate on the principle that supply disruptions at the source ripple outward with amplifying force. When a single nation controls roughly a quarter of the world's copper production, its monthly output figures carry weight far beyond their immediate numerical value. Chile occupies precisely that position, and the production data emerging from the Andean nation in early 2026 is sending signals that industrial planners, commodity traders, and supply chain strategists cannot afford to ignore.

Chile copper output falls in March 2026 by 9.04% year-on-year, a contraction that moves the narrative well beyond the realm of seasonal variability and into territory that demands structural explanation. Understanding what is driving this decline, which operations are responsible, and what it means for global copper availability requires unpacking several layers of operational, geological, and economic complexity.

When big ASX news breaks, our subscribers know first

Chile's Structural Position in Global Copper Markets

Chile's dominance in global copper production is not simply a function of geological fortune, although the Andean copper belt is among the richest mineral endowments on earth. It reflects decades of infrastructure investment, operational development, and the build-out of processing capacity across some of the world's largest and most technically complex mining operations.

Accounting for approximately 25% of worldwide copper production, Chile sits in a category of its own. The next largest producers, including Peru and the Democratic Republic of Congo, trail at a significant distance. This concentration means that Chilean production data functions as a real-time barometer for global copper supply conditions. Monthly figures released by Chile's national statistics agency, INE, and the Chilean Copper Commission (Cochilco) feed directly into pricing models, supply chain forecasts, and inventory management systems used by manufacturers across Asia, Europe, and North America.

Copper's significance extends far beyond its industrial applications. Economists and market analysts have long treated copper demand and pricing as a proxy for global economic activity, referencing the metal's penetration across construction, transportation, electrical infrastructure, and increasingly, clean energy technologies. Furthermore, as Reuters reported via Kitco News, copper is widely considered an economic bellwether precisely because its end-use applications span so many sectors simultaneously.

This makes the distinction between cyclical output fluctuations and structural supply deterioration critically important. A temporary production dip caused by equipment maintenance or adverse weather is absorbed by markets with minimal lasting impact. A sustained, multi-month pattern of declining output rooted in geological and operational realities is an entirely different signal, carrying implications for long-term supply adequacy. In this context, the Chile copper outlook for the coming quarters deserves close scrutiny.

What the March 2026 Production Numbers Actually Show

Breaking Down the Headline Decline

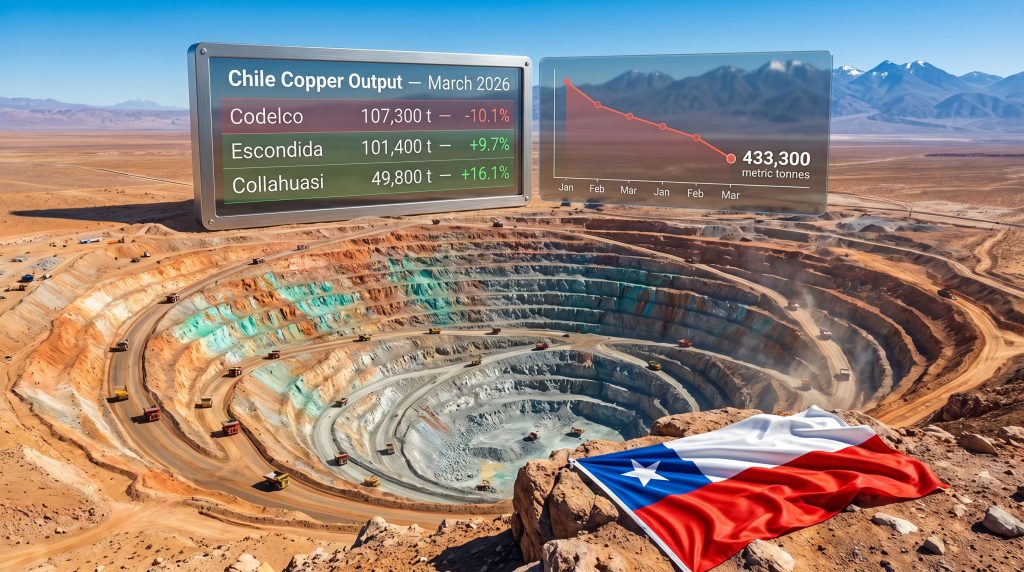

According to official data reported by Chile's national statistics agency INE and published by Reuters, Chilean copper output in March 2026 reached 434,314 metric tonnes, down from 477,464 metric tonnes in March 2025. This represents a year-on-year contraction of 9.04%, a substantially more severe decline than preliminary estimates had suggested.

| Month | Output (Metric Tonnes) | Year-on-Year Change |

|---|---|---|

| January 2026 | 409,900 | -3.0% |

| February 2026 | 378,554 | -4.8% |

| March 2026 | 434,314 | -9.04% |

Rather than the declining trend moderating as the quarter progressed, the year-on-year contraction rate accelerated sharply in March. February 2026 recorded production figures that represented the lowest monthly output in nearly nine years, and while March showed a nominal volume recovery from that trough, the steepening of the year-on-year decline tells a more troubling story. The comparison base from March 2025 was evidently strong enough that even a volumetric recovery looks deeply negative against it.

Manufacturing Output: A Compounding Economic Signal

The copper production data did not arrive in isolation. INE simultaneously reported that Chilean manufacturing production contracted by 4.5% in March 2026, with the state agency attributing the primary driver to reduced food production activity. This figure missed the consensus forecast of economists polled by Reuters, who had anticipated a more modest 1.0% manufacturing decline, making the actual result a miss of 3.5 percentage points against expectations.

The simultaneous deterioration of both copper output and broader manufacturing activity reinforces a picture of synchronised industrial weakness rather than a sector-specific anomaly.

The combination of these two datasets is important context for investors and industrial buyers. When copper output and general manufacturing contract together, it becomes harder to attribute the decline to isolated operational factors. Consequently, the data points toward a broader economic environment that is restraining industrial activity across multiple sectors.

Which Mines Are Driving the Divergence in March Performance?

Codelco: The Weight of Legacy at the World's Largest Copper Producer

No analysis of Chilean copper production is complete without examining Codelco, the state-owned mining company that has held the title of the world's largest copper producer for decades. The company's March 2026 performance has been identified as the most significant negative contributor to Chile's aggregate output figures, with production declining approximately 10% year-on-year during the period.

Codelco's operational challenges are not new, but their compounding nature has become increasingly difficult to offset. The company's mine portfolio consists largely of mature, legacy operations that were developed during an era when near-surface, high-grade ore bodies were still accessible. Those deposits have been progressively worked through over decades of extraction, leaving the company increasingly reliant on deeper, lower-grade ore zones that are both more expensive and more technically complex to mine.

The Codelco production strategy involves executing a multi-year structural renewal program designed to transition key operations from open-pit to underground mining configurations. However, these capital-intensive transitions have repeatedly encountered timeline extensions, creating output gaps that cannot be bridged through efficiency improvements alone. The fundamental challenge is that accessing the next generation of ore bodies requires years of development investment before any material production benefit is realised.

Escondida and Collahuasi: Private Operations Providing a Partial Offset

In contrast to Codelco's trajectory, two of Chile's other major copper operations recorded meaningful production growth in March 2026, demonstrating that the weakness is not uniformly distributed across the sector.

BHP's Escondida mine, widely recognised as the world's largest known copper deposit by reserve size, produced approximately 101,400 metric tonnes in March 2026, representing year-on-year growth of close to 10%. This performance marks a significant recovery from January 2026, when Escondida had itself been recording a year-on-year decline of around 4%, suggesting meaningful operational improvement through the quarter.

The Collahuasi mine, operated as a joint venture between Glencore and Anglo American, delivered the strongest growth among major operations, with output of approximately 49,800 metric tonnes reflecting year-on-year growth of roughly 16%. Collahuasi's performance highlights that operational execution quality and ore body access vary considerably even within a single mining jurisdiction.

| Operation | Operator | March Output (MT) | YoY Change |

|---|---|---|---|

| Codelco (consolidated) | State-owned | ~107,300 | ~-10% |

| Escondida | BHP | ~101,400 | ~+10% |

| Collahuasi | Glencore / Anglo American | ~49,800 | ~+16% |

Note: Mine-level figures are based on outline estimates and require independent verification against Cochilco official data releases and company disclosures.

The divergence between state-owned and privately operated mines raises questions about the comparative operational and capital allocation frameworks governing each. Privately operated mines with clearer commercial mandates may be better positioned to execute on productivity improvement programmes and access new ore zones without the bureaucratic and political considerations that can influence state enterprise decision-making.

The Structural Forces Suppressing Chilean Copper Production

Ore Grade Deterioration: The Geological Reality Beneath the Numbers

The single most persistent constraint on Chilean copper output is not temporary or fixable through capital investment alone. It is geological. As copper mineralisation in mature deposits is progressively extracted, the remaining ore grades decline. This is not a management failure or a policy shortcoming. It is a mathematical inevitability in any finite mineral system.

Ore grade deterioration operates through a mechanism that compounds over time:

- Early extraction phases target the highest-grade, most economically accessible ore bodies, delivering strong production at relatively low cost

- Mid-life phases see declining average grades as the best material is depleted, requiring larger volumes of ore to be processed per tonne of copper produced

- Mature phases require miners to process significantly greater ore volumes, consuming proportionally more energy, water, and processing reagents per unit of copper output

- Deep transition phases involve capital-intensive underground development with years of investment before new ore zones contribute meaningfully to production

In Chile's northern desert mining region, where water availability is a genuine constraint and energy costs are significant, declining ore grades translate directly into rising operating costs per tonne. This cost inflation is structurally embedded and does not respond to short-term pricing incentives. Indeed, Chile's copper supply gap is increasingly shaped by these geological realities rather than temporary operational factors.

Capital Allocation and Project Timeline Delays

Beyond ore grade dynamics, the execution risk associated with major capital transitions has emerged as a significant near-term production headwind. Transitioning from open-pit to underground mining configurations is among the most complex and capital-intensive undertakings in the resource sector. These projects involve:

- Developing underground shaft and decline infrastructure that may require 3-7 years before ore production commences

- Managing the production gap that occurs when open-pit ore access is exhausted before underground ore flows begin

- Maintaining equipment fleets capable of operating in both configurations during transition periods

- Managing workforce skill requirements that differ between surface and underground mining environments

- Navigating increased regulatory and safety compliance requirements for underground operations

When these projects experience delays, as has been the case at multiple Codelco operations, the production gap widens and total output suffers. This dynamic is structural in nature and can persist for multiple years.

Environmental and Seasonal Context

Northern Chile's climatic conditions, particularly the summer rainfall season and logistics disruptions associated with Pacific weather events, do periodically affect operational throughput. These factors likely contributed to February 2026's sharp contraction. However, they cannot explain a sustained seven-month rolling decline, and importantly, no major labour disputes were recorded in Chile's copper sector during early 2026.

This eliminates industrial action as a contributing variable and points analysis squarely toward geological and operational factors.

When external disruption factors like strikes and extreme weather are absent, persistent production declines carry a more concerning interpretation: they reflect the underlying performance envelope of the ore bodies and operations themselves.

Copper's Bellwether Status and Why This Data Matters Beyond Mining

The Metal That Reads the Economy

Copper's penetration across virtually every category of industrial and infrastructural activity gives its supply and demand dynamics a macro-economic significance that few other commodities can match. Its applications span:

- Electrical infrastructure: Power generation, transmission, and distribution systems

- Construction: Wiring, plumbing, structural applications across residential and commercial sectors

- Transportation: Automotive wiring harnesses, with significantly elevated copper content in electric vehicles

- Renewable energy: Solar photovoltaic systems, wind turbines, and battery storage installations

- Industrial machinery: Motors, controls, heat exchangers, and manufacturing equipment

- Telecommunications: Network infrastructure, data centres, and communications hardware

The breadth of these applications means that copper demand responds to economic activity across nearly every sector simultaneously. Disruptions to supply from the world's dominant producing nation therefore carry implications that extend well beyond commodity pricing.

Supply-Side Tightening Against an Accelerating Demand Backdrop

The timing of Chile's production weakness coincides with a period during which global copper demand projections are being revised upward, driven primarily by energy transition infrastructure requirements. The electrification of transport, the build-out of renewable energy generation capacity, and the expansion of electrical grid infrastructure in emerging economies all represent demand growth vectors that were not present at scale during previous commodity cycles. Furthermore, a broader copper supply crunch appears increasingly likely given the compounding nature of these structural challenges.

The intersection of structural supply constraints from the world's largest producer with accelerating demand from energy transition investment creates the conditions for a sustained period of supply-demand tension in copper markets.

This is not a prediction of specific price outcomes. It is an observation about directional market forces that commodity consumers, industrial planners, and capital allocators need to incorporate into their planning frameworks. Sustained output declines from Chile, when demand growth remains intact, compress the global supply buffer and increase price sensitivity to incremental supply or demand shifts.

The next major ASX story will hit our subscribers first

Frequently Asked Questions

Why did Chile's copper output fall in March 2026?

Chilean copper production contracted 9.04% year-on-year in March 2026 to 434,314 metric tonnes, down from 477,464 metric tonnes in the same month of 2025. The primary contributors were structural production challenges at Codelco, the state-owned mining giant, including declining ore grades at legacy operations and delays in transitioning to next-generation ore zones. Partial offsets came from strong performance at Escondida and Collahuasi, both of which recorded meaningful year-on-year growth. Data was reported by Chile's national statistics agency, INE.

How significant is Chile to global copper supply?

Chile produces approximately 25% of the world's total copper output, making it the dominant single-nation supplier by a substantial margin. Its production data directly influences global copper pricing, supply chain planning for industrial manufacturers, and investment decisions across the mining sector.

Is the March 2026 decline part of a longer trend?

The data strongly suggests so. February 2026 recorded near-decade low monthly output, and the rolling 12-month production trajectory has been negative for an extended period. The acceleration of the year-on-year decline rate from earlier quarters to the -9.04% recorded in March reinforces the structural interpretation of the weakness.

What is Codelco's challenge in maintaining copper output?

Codelco is navigating the most operationally complex period in its history, transitioning a portfolio of ageing, mature mining operations toward deeper, lower-grade ore bodies through a capital-intensive structural renewal programme. The transition involves years of investment before production benefits are realised, creating an unavoidable output gap during the transition period.

How does a sustained Chilean production decline affect industrial copper consumers?

Industrial buyers of copper, including manufacturers of electrical equipment, EV components, construction materials, and renewable energy infrastructure, face a tighter supply environment if Chilean declines persist. This typically translates into higher raw material costs and reduced pricing flexibility, particularly when global demand growth is simultaneously accelerating.

Forward-Looking Implications for Global Copper Supply

Near-Term Outlook: No Quick Recovery at the Dominant Producer

The March 2026 data offers limited grounds for near-term optimism about Chilean aggregate output. While Escondida and Collahuasi's strong performances provide a partial buffer, Codelco's structural challenges operate on a multi-year timeline. Capital project completions and underground ore zone access cannot be accelerated beyond the constraints of geological and engineering reality.

The manufacturing data reinforces this caution. A 4.5% manufacturing contraction that was 3.5 percentage points worse than economist consensus suggests the broader Chilean industrial economy is facing headwinds that could affect the investment and operational environment across the mining sector.

Medium-Term Supply Risk Assessment

For market participants with 12-36 month planning horizons, several risk factors warrant monitoring:

- Codelco project delivery timelines: Any further delays in structural renewal projects extend the output gap and reduce the probability of near-term recovery in state-miner production

- Grade trajectory at legacy operations: Ore grade data from Codelco's major mines will determine whether current production levels represent a floor or whether further deterioration is possible

- Private operator performance sustainability: The strong results at Escondida and Collahuasi need to be evaluated against their own ore grade trajectories and capital investment programmes to assess durability

- Chilean project pipeline: Limited near-term new project commissioning across the broader Chilean sector reduces the probability of meaningful capacity additions offsetting grade-driven losses

- Global demand acceleration: Energy transition investment timelines in major economies will determine the pace of demand growth intersecting with constrained supply

Strategic Considerations for Copper Market Participants

Industrial consumers should treat Chilean monthly production data as a leading supply risk indicator rather than a lagging economic statistic. The divergence between state and privately operated mine performance also suggests that corporate governance and operational management frameworks materially influence outcomes even within the same geological and regulatory environment.

For investors monitoring copper market dynamics, the combination of structural supply constraints, production declines at the world's largest single producing nation, and accelerating demand from electrification infrastructure represents a thematic framework worthy of sustained attention. However, commodity market forecasting carries substantial uncertainty, and no production trend or demand projection should be interpreted as a guarantee of specific price or market outcomes.

This article is intended for informational purposes only and does not constitute financial or investment advice. Commodity markets involve significant uncertainty, and past production trends are not necessarily indicative of future outcomes. Readers should conduct their own due diligence and consult qualified financial advisers before making investment decisions.

Want to Stay Ahead of the Next Major Copper Discovery on the ASX?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant alerts on significant mineral discoveries — including copper — so subscribers can identify actionable opportunities before the broader market reacts. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin a 14-day free trial today to secure a market-leading edge.