August 6, 2026

The Geology of Declining Empires: How Ageing Ore Bodies Are Reshaping the Global Copper Market

Long before a copper mine ships its first tonne, the geological clock is already ticking. Every large-scale copper deposit has a finite ore grade profile, and as mining progresses deeper into a resource, the concentration of recoverable copper per tonne of rock gradually diminishes. This is not a policy failure or a management shortcoming. It is the fundamental physics of ore body economics, and it sits at the centre of one of the most consequential supply stories in global commodity markets today.

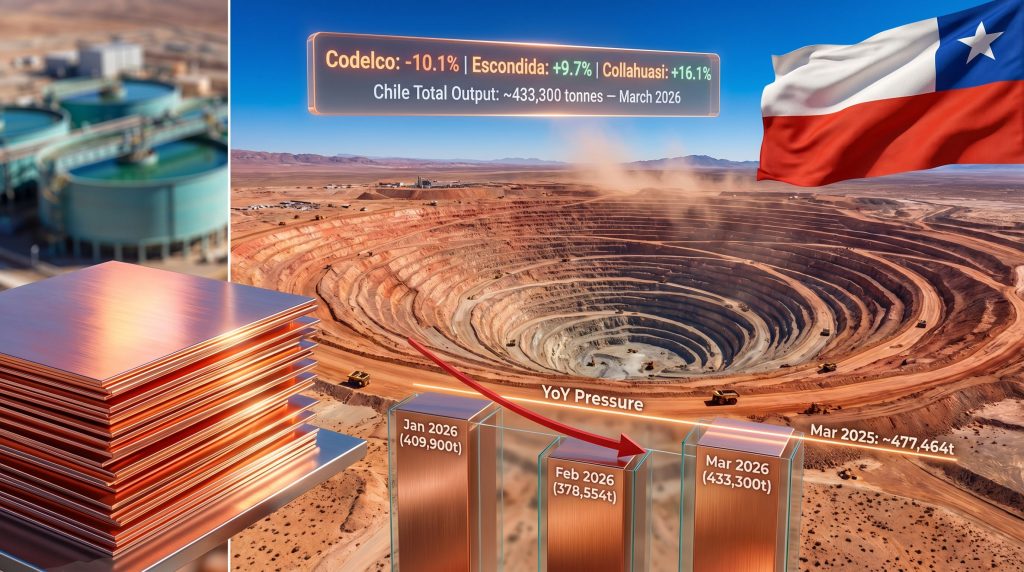

Chile, which supplies roughly one quarter of the world's copper, is confronting this reality at scale. The country's March 2026 production data, published by Chile's National Statistics Institute (INE), confirmed that the nation produced 434,314 metric tonnes of copper during the month, down from 477,464 metric tonnes in March 2025. That year-on-year contraction of 9.04% is not simply a one-month anomaly. It is the latest chapter in a production narrative that has been deteriorating for the better part of a year, driven by a complex mixture of geological depletion, infrastructure constraints, and operational disruptions at state-owned assets.

Understanding why Chile copper output falls in March, and why it matters far beyond South America, requires looking beneath the headline figures to the structural mechanics of how the world's most important copper-producing nation actually functions. For context on broader pricing dynamics, the Chile copper price forecast provides a useful market framework.

When big ASX news breaks, our subscribers know first

A Tale of Two Mines: Diverging Trajectories Within a Declining National Total

The most misleading thing about Chile's national production data is the implication of uniformity. The country does not have a single copper problem. It has multiple, highly differentiated operational stories playing out simultaneously across dozens of mines, and the aggregated national figure obscures more than it reveals.

The clearest illustration of this divergence sits in the March 2026 production breakdown:

| Mine / Operator | March 2026 Output | Year-on-Year Change |

|---|---|---|

| Codelco (state-owned enterprise) | 107,300 tonnes | -10.1% |

| BHP Escondida | 101,400 tonnes | +9.7% |

| Collahuasi (Glencore / Anglo American JV) | 49,800 tonnes | +16.1% |

| Total Chile (INE) | 434,314 tonnes | -9.04% |

Two of the country's most significant privately operated mines expanded output meaningfully. Codelco, the state-owned enterprise that has historically anchored Chile's position as the world's dominant copper producer, dragged the national total downward by a margin that private sector outperformance could not fully offset.

This divergence is not coincidental. It reflects a fundamental difference in the financial and operational conditions separating well-capitalised private operators from a state-owned entity managing ageing assets through a multi-year structural transformation programme. Escondida's recovery to 101,400 tonnes demonstrates that disciplined ore access management and sustained capital investment can generate production growth within Chile's existing geological endowment. Collahuasi's 16.1% surge reinforces the same conclusion, driven by access to higher-grade ore zones in its currently active mining panels.

Chile's copper output decline in early 2026 is not a national geological crisis. It is primarily a Codelco-specific operational challenge playing out against a backdrop of privately operated mines that are, in several cases, performing exceptionally well.

The Codelco Problem: Ore Grade Deterioration and the Cost of Transformation Delays

Codelco operates some of the oldest large-scale copper mines on earth. Chuquicamata, the enormous open pit operation in northern Chile that has been producing copper for over a century, and El Teniente, one of the largest underground copper mines in the world, are assets whose ore grade profiles have been declining for decades. As accessible, higher-grade material becomes progressively exhausted, extracting each tonne of copper requires processing significantly greater volumes of rock, consuming more energy, water, and processing capacity per unit of output.

This grade deterioration effect is not unique to Codelco. It is a sector-wide phenomenon that affects virtually every mature copper operation globally. What makes Codelco's situation particularly challenging is the combination of grade decline with operational disruptions at a moment when its transformation capital programme has not yet unlocked access to next-generation ore zones at depth. The Codelco output decline has been a key driver of this national shortfall.

The factors compounding Codelco's March 2026 output contraction include:

- Declining ore grades across legacy assets, requiring greater processing throughput to maintain equivalent copper output

- Operational disruption at El Teniente following a significant incident in mid-2025 that affected production continuity across multiple subsequent quarters

- Project transition delays in Codelco's multi-billion-dollar structural investment programme, which is designed to open access to deeper, higher-grade ore bodies across several of its flagship operations

- Water availability pressures in Chile's hyper-arid Atacama region, where regulatory constraints on industrial water usage continue to tighten

The intersection of these factors created a production environment where Codelco was simultaneously managing reduced ore quality, restricted operational capacity at a major underground mine, and a capital programme that has not yet delivered the volume uplift it was designed to generate.

Understanding Ore Grade Decline: The Physics Behind the Numbers

For investors and market observers unfamiliar with mining geology, ore grade decline deserves specific explanation because it underlies so much of what is happening in the Chilean copper sector.

Copper ore grades are measured as a percentage of copper content per tonne of rock extracted. A deposit grading at 1.5% copper yields approximately 15 kilograms of copper per tonne of material processed. As a mine progresses through its resource, the grades accessible from current working areas typically decline, meaning the same processing infrastructure yields less copper per tonne handled.

At many of Codelco's legacy operations, average ore grades have declined from levels above 1% copper in the early 2000s to levels that in some cases now sit below 0.7%, according to historical trend data from Codelco's own annual reports. This grade compression directly affects production volumes even when processing rates remain constant, and it structurally increases cost per pound of copper produced. The economic consequence is a mine that becomes progressively more expensive to operate relative to the copper it delivers. Furthermore, the Codelco production outlook remains closely watched as a barometer for Chile's overall recovery prospects.

The Rolling Decline: January Through March 2026 in Context

Chile copper output falls in March represent the continuation of a deteriorating production trend that has persisted across all three months of early 2026. Viewing the quarterly trajectory rather than any single month reveals the full weight of what Chilean copper markets are navigating:

-

January 2026: 409,900 tonnes, down approximately 3% year-on-year. Codelco contracted 2.4% to 100,200 tonnes while Escondida declined 4% to 105,000 tonnes, indicating that early in the year both major producers were facing operational pressure simultaneously.

-

February 2026: 378,554 tonnes, the weakest monthly output figure recorded in Chile in nearly nine years, representing an 8.5% sequential decline from January and a 4.8% fall against the prior year. Rainfall events in northern Chile's mining districts contributed to the monthly weakness, though these seasonal factors do not fully explain the magnitude of the decline.

-

March 2026: 434,314 tonnes, a partial volume recovery relative to February but still representing the 9.04% year-on-year shortfall confirmed by INE's official data.

The three-month pattern reveals a production environment characterised by underlying structural weakness punctuated by seasonal volatility. February's extreme low reflects both operational disruptions and adverse weather conditions, while March's partial recovery suggests that some of these transient factors have eased. However, what has not eased is the fundamental trajectory: on a rolling 12-month basis, Chilean copper production had declined for seven consecutive months as of February 2026.

Global Supply Implications: Quantifying the Gap

Chile's position as the world's largest copper-producing nation, responsible for approximately 25% of global refined copper supply, means that sustained production shortfalls do not stay within Chile's borders economically. Their consequences ripple through global commodity markets, downstream manufacturing, and energy transition infrastructure timelines. In fact, the scale of Chile's copper supply gap has become one of the most closely tracked variables in commodity analysis.

The arithmetic of the March shortfall is straightforward. Compared to March 2025, Chile delivered roughly 43,000 fewer tonnes of copper to global supply chains in a single month. If that rate of shortfall were to persist across a full calendar year, the aggregate gap would exceed 500,000 tonnes annually, a volume equivalent to the total yearly output of a mid-tier copper-producing country.

The downstream industries most exposed to this supply compression span the full breadth of modern industrial activity:

| Sector | Copper Dependency | Primary Risk from Supply Shortfall |

|---|---|---|

| Electric Vehicle Manufacturing | High (average ~60-83kg per vehicle) | Input cost inflation, production cost pressure |

| Grid Infrastructure and Renewables | Very High | Potential delays in capital project timelines |

| Consumer Electronics | Moderate | Component cost increases |

| Residential and Commercial Construction | High | Building material cost pressure |

| Industrial Machinery | High | Capital equipment cost increases |

The structural demand thesis for copper remains intact and arguably strengthening. Global electrification commitments, EV adoption trajectories, and grid infrastructure buildout across both developed and emerging economies all point toward sustained demand growth through the remainder of this decade. Consequently, when the supply side of that equation is simultaneously contracting at a major producing nation, the fundamental balance tightens in ways that have direct consequences for copper pricing. The growing copper supply crunch is increasingly driving strategic conversations across the commodity sector.

Manufacturing Decline Compounds the Story

Chile's copper production shortfall did not arrive in isolation. INE's concurrent reporting confirmed that Chile's manufacturing output fell 4.5% year-on-year in March 2026, significantly exceeding the consensus forecast of economists polled by Reuters, who had anticipated a far more modest 1% contraction. The primary driver identified by INE was a reduction in food production, reflecting broader domestic economic pressures in the Chilean economy.

For copper market analysts, the simultaneous decline in copper production and manufacturing output carries a compounding significance. Copper processing, concentrate transport, refinery operations, and logistics infrastructure all depend on a functioning industrial economy. A manufacturing sector under pressure can create secondary constraints on the copper value chain that amplify production shortfalls beyond their direct geological or operational causes.

The convergence of a 9.04% copper production decline and a 4.5% manufacturing contraction in the same reporting period functions as a dual signal for Chilean economic momentum heading into Q2 2026.

The next major ASX story will hit our subscribers first

Risk Landscape for Chilean Copper Through the Remainder of 2026

For commodity analysts and investors monitoring the global copper balance, the Chilean production environment carries a layered set of risks that extend beyond the geological and operational factors already in play:

Geological and Operational Risks:

- Continued ore grade deterioration at Codelco legacy assets without accelerated access to deeper mineral zones

- Unplanned disruptions at any of Chile's top-producing operations, including equipment failures, geological events, or labour disputes

- Water availability constraints in northern mining districts as regulatory pressure on industrial water consumption intensifies

Regulatory and Political Risks:

- Chile's evolving mining royalty framework creates ongoing uncertainty for capital allocation decisions among international operators evaluating expansion investments

- Community relations requirements and environmental compliance complexity are increasing across northern mining districts, lengthening permitting timelines for expansion projects

Macroeconomic Risks:

- Currency dynamics affecting operational cost burdens for export-oriented producers

- Global trade policy shifts that could alter demand trajectories in major copper-consuming economies, indirectly affecting Chilean production incentives

The Path to Recovery: What Needs to Happen

Codelco's multi-year structural investment programme remains the single most critical variable in Chile's medium-term production outlook. The programme is designed to unlock access to higher-grade ore bodies at depth across several of its flagship mines, replacing the declining yield of legacy working areas with next-generation ore zones that carry significantly better grade profiles.

The timeline for this transition determines when, and to what degree, Codelco's output contraction can be reversed. Acceleration of capital deployment, combined with stable regulatory conditions and the resolution of operational disruptions, could position Codelco for a production recovery beginning in late 2026 or extending into 2027. However, delays to this programme would prolong the period of structural volume constraint.

The performance of private operators offers a constructive reference point. BHP's Escondida and the Glencore-Anglo American Collahuasi operation are collectively demonstrating that Chile's geological endowment remains capable of generating production growth when capital investment is sustained and ore access management is disciplined.

For those monitoring the sector, the most informative forward indicators will be Cochilco's April and May 2026 monthly production bulletins, Codelco's quarterly operational updates on El Teniente recovery timelines, and any official announcements regarding milestones in the deeper mine access programme.

Frequently Asked Questions

Why did Chile's copper output fall in March 2026?

Chile's copper output declined primarily because of a 10.1% year-on-year contraction at Codelco, the state-owned enterprise that is the country's largest copper producer. Factors driving Codelco's decline include ore grade deterioration at legacy assets, ongoing operational disruption at El Teniente following a 2025 incident, and delays in accessing higher-grade ore at depth through its structural transformation programme.

How much copper did Chile produce in March 2026?

Chile produced 434,314 metric tonnes of copper in March 2026, according to Chile's National Statistics Institute (INE), compared to 477,464 metric tonnes in March 2025. The Chilean Copper Commission (Cochilco) reported a smaller year-on-year variance of approximately 0.7%, reflecting different measurement methodologies between the two agencies.

Which Chilean mines increased production in March 2026?

BHP's Escondida mine increased output by approximately 9.7% year-on-year to reach 101,400 tonnes, while the Collahuasi mine operated by the Glencore and Anglo American joint venture surged 16.1% to 49,800 tonnes.

What are the global supply implications of Chile's production shortfall?

With Chile supplying approximately 25% of global copper, the March 2026 shortfall represented roughly 43,000 fewer tonnes entering global supply chains compared to the prior year. Sustained shortfalls of this scale tighten the global copper balance, creating upward price pressure and potential cost inflation across copper-dependent industries including EV manufacturing, grid infrastructure, and construction.

Is Chile's copper production decline a long-term structural issue?

The rolling 12-month trend showing seven consecutive months of year-on-year decline as of February 2026 indicates that the current weakness extends beyond seasonal variation. Structural factors including ore grade deterioration and capital programme delays at Codelco suggest near-term recovery depends heavily on the pace and success of mine transformation initiatives at the state-owned operator.

Disclaimer: This article is intended for informational purposes only and does not constitute financial advice. Production figures and trend analyses are drawn from INE and Cochilco reporting as referenced in media coverage dated April 30, 2026. Forecasts and scenario analyses represent analytical perspectives and not guaranteed outcomes. Readers should conduct independent research before making investment decisions.

Want To Capitalise on the Next Major Copper Discovery Before the Market Moves?

As Chile's ageing ore bodies continue to weigh on global copper supply, the opportunity for investors lies in identifying significant new discoveries early — Discovery Alert's proprietary Discovery IQ model delivers real-time ASX mineral discovery alerts straight to subscribers, turning complex geological and commodity data into actionable investment insights. Explore historic discovery returns on Discovery Alert's dedicated discoveries page and begin your 14-day free trial today to position yourself ahead of the next major copper find.