June 6, 2026

The Hidden Bottleneck Inside the World's Largest Copper Basin

Copper markets are frequently analysed through the lens of demand. Electrification targets, electric vehicle adoption curves, and data centre buildout are the variables that dominate institutional forecasts. Yet the supply side of the equation contains a structural problem that receives far less attention: the world's single largest copper-producing nation has been deploying capital at a massive scale while generating almost no net new output. Understanding why that has happened, and what Chile copper permitting reforms are designed to do about it, is central to evaluating the real investment risk profile of copper development in the Atacama corridor today.

When big ASX news breaks, our subscribers know first

Chile Copper Permitting Reforms: The Problem They Were Built to Solve

Chile produces between 5.3 and 5.43 million tonnes of copper annually, a volume representing roughly 23 to 24% of total global mine supply. The country's fiscal architecture reflects that dependency: mining accounts for 59% of total national exports, with copper driving 80% of that mining export share. Copper mining contributes between 10% and 14% of Chile's gross domestic product, a concentration that leaves the nation's budget directly exposed to any sustained production decline.

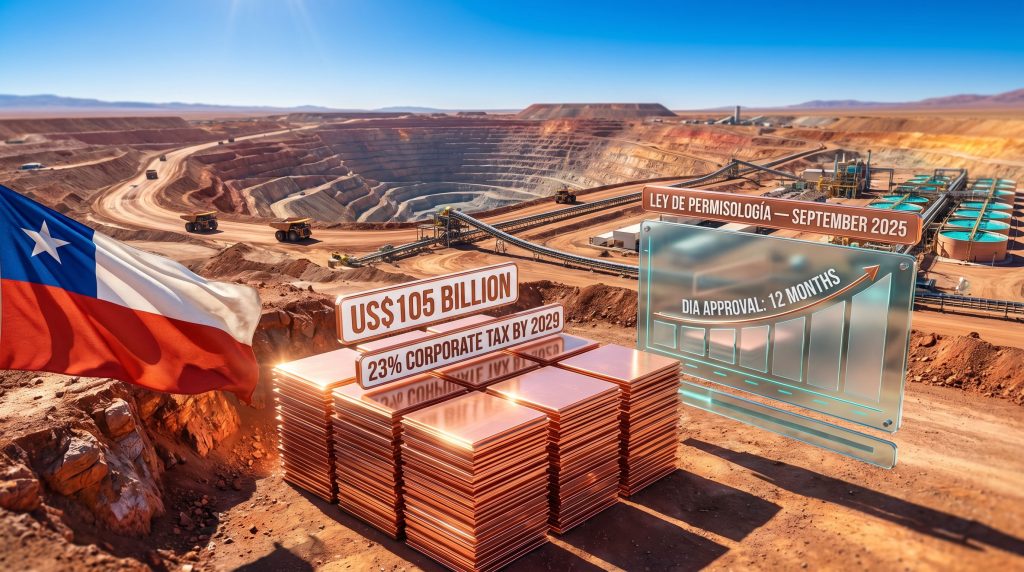

The paradox embedded in those figures becomes visible when capital deployment is examined alongside output trajectory. Capital projected to flow into Chile's copper sector through 2034 exceeds US$105 billion, with approximately 90% directed at copper-focused projects. Yet Cochilco's 2025 analysis, covering the period from 2024 to 2033, projects a production increase of only roughly 100,000 tonnes over the entire decade, reaching approximately 5.5 million tonnes by 2033.

That ratio of capital to incremental output is not a sign of normal depreciation. It is a structural signal that the majority of new investment is being consumed by the task of sustaining existing production, not building new supply.

Furthermore, three converging forces explain this dynamic:

- Ore grade decline across major operations, requiring the processing of substantially higher material volumes to extract equivalent copper output

- Greater extraction depth, increasing energy consumption, haulage costs, and capital requirements per tonne produced

- Regulatory friction in the approvals process, extending the gap between committed capital and generating production

The Chile copper permitting reforms enacted between September 2025 and April 2026 were a direct legislative response to the third of those constraints. As highlighted in Chile's copper supply gap, regulatory architecture had become a material drag on the country's ability to translate exploration success into operating mines.

What the Ley de Permisología Actually Changes

The Ley de Permisología, formally the Framework Law for Sectoral Authorizations (also referenced as LMAS), was enacted in September 2025. The law targets a 30% to 70% reduction in permitting timelines and operates as a general business facilitation measure applicable across industries, including mining, rather than as a sector-specific intervention in the mining code.

Its three principal mechanisms are:

- Streamlining – reducing the number of overlapping authorisations required across multiple government agencies, eliminating procedural duplication that historically added months or years to approval timelines

- Standardisation – establishing uniform approval criteria and documentation requirements, removing the inconsistency that made outcomes unpredictable across regions and project types

- Digitisation – deploying a centralised digital processing platform called SUPER, which functions as a single-window system through which permit applications are submitted, tracked, and coordinated across agencies in real time

The SUPER platform deserves particular attention because it addresses a dimension of permitting delay that rarely features in policy discussions: informational opacity. Under the pre-reform system, applicants often had no reliable mechanism for tracking where their application sat within the approval chain, which agency held the outstanding review, or what additional information was required. SUPER resolves that by creating a transparent, auditable process chain visible to both applicants and regulators simultaneously.

What the Reform Does Not Guarantee

The 30 to 70% reduction range is wide, and deliberately so. Outcomes at the upper end of that band would represent a transformational shift in project economics. Outcomes at the lower end represent incremental improvement. Several factors determine where any individual project lands within that range:

- Agency-level implementation quality – the legislation creates the framework, but regulatory culture at the agency level determines how faithfully it is applied

- Post-approval legal exposure – courts and environmental bodies retain the capacity to impose timelines that exceed legislated targets through challenge proceedings

- Project complexity – simpler oxide deposits with established processing analogues are more likely to benefit from the upper range of timeline compression than complex sulphide operations requiring novel processing infrastructure

The April 2026 Fiscal Stability Bill: Locking In Long-Dated Capital Certainty

Chile's second major reform instrument addresses a different dimension of investment risk. President Karst's Economic and Social Reconstruction and Development Bill, enacted in April 2026, extends the reform architecture from procedural efficiency to fiscal predictability.

| Reform Component | Enacted | Core Provision | Primary Investor Benefit |

|---|---|---|---|

| Ley de Permisología | September 2025 | 30-70% timeline reduction via SUPER platform | Faster DIA approval pathway |

| Fiscal Stability Bill | April 2026 | 25-year stability pact | Long-dated sovereign risk reduction |

| Corporate Tax Trajectory | April 2026 | 1 percentage point reduction per year to 23% by 2029 | Improved project economics |

The 25-year fiscal stability pact is structurally the more durable of the two reforms. Mine development operates on timescales that span decades, and the discount rate applied to long-dated cash flows is heavily influenced by sovereign risk perception. A stability mechanism that outlasts electoral cycles by design fundamentally alters the risk-adjusted return calculation for capital commitments that would otherwise carry significant political contingency.

Chile's political environment has shifted toward the centre-right, with both the Congress and the Chamber of Deputies currently under centre-right control. That alignment supports near-term legislative continuity. However, the 25-year pact is not contingent on political continuity to deliver its value. Its legal architecture is specifically designed to remain enforceable across administrations, which is precisely what gives it credibility as an investment instrument rather than a policy statement.

Grade Decline and the Convergence of Brownfield and Greenfield Capital Intensity

One of the least widely understood structural shifts in Chilean copper development is the narrowing cost differential between brownfield and greenfield projects. Data from a BHP site visit presentation in late 2024 indicated that brownfield and greenfield capital intensity are converging materially in Chile.

Historically, brownfield assets carried a structurally lower capital profile because existing infrastructure — established pits, road access, proximity to processing facilities — reduced upfront construction costs significantly. That advantage assumed, critically, that the brownfield resource could be accessed at comparable depths and grades to historical operations.

As ore grades decline and economic mineralisation retreats to greater depths, those assumptions break down. Brownfield operations increasingly require:

- New or substantially upgraded processing circuits capable of handling higher material throughput

- Deeper extraction infrastructure with associated haulage and ventilation requirements

- Greater water and energy consumption per unit of copper produced

The practical consequence is that the capital intensity of brownfield development at depth is converging toward levels previously associated with new-build greenfield projects, eroding the risk-adjusted return differential that traditionally made brownfield development the preferred capital allocation for mid-tier and major operators.

In this environment, the analytical distinction that matters is no longer brownfield vs. greenfield but rather infrastructure-advantaged vs. infrastructure-constrained, regardless of which development category a project nominally occupies.

Assets with genuine infrastructure advantages — low elevation, existing road access, coastal proximity, access to under-utilised processing capacity — retain material capital efficiency advantages. Assets that carry the brownfield classification without those characteristics face capital profiles approaching greenfield levels. Consequently, investors exploring the Chile copper outlook must weigh infrastructure access as a primary evaluation criterion.

The Marimaca Precedent: A Practical DIA Benchmark for Junior Developers

The Declaración de Impacto Ambiental (DIA) is the environmental impact declaration that constitutes the primary regulatory gateway in Chile's mining project approval sequence. Approval of the DIA results in the environmental permit required before construction can legally commence. Under the pre-reform system, DIA timelines were notoriously variable, with agency review fragmentation and inconsistent documentation requirements creating unpredictable delays.

The most actionable data point for developers navigating the reformed system comes from Marimaca Copper's oxide copper deposit, which obtained its environmental licence within a 12-month window. That timeline has become the practical benchmark against which junior developers are now calibrating their project approval expectations.

The significance of the Marimaca precedent extends beyond the single data point. It demonstrates that the reformed system can deliver on its stated objectives at the project level rather than merely in policy documents. For smaller developers who cannot absorb multi-year approval delays through balance sheet strength alone, the establishment of a credible 12-month benchmark fundamentally changes the risk profile of projects targeting DIA submission under the new framework.

Translating the DIA Benchmark into Project-Level Timelines

The combination of streamlined DIA approvals and fiscal stability creates a materially different development timeline framework compared to the pre-reform environment. A representative brownfield development sequence targeting post-reform approval looks as follows:

| Milestone | Target Timing |

|---|---|

| DIA Submission | Q3 2026 |

| Maiden Mineral Resource Estimate | Late 2026 |

| Pre-Feasibility Study | Early 2027 |

| Environmental Permit (12-month target) | Mid-to-late 2027 |

| Construction Period (approximately 6 months) | Late 2027 |

| Production Commencement | Late 2027 to Early 2028 |

The next major ASX story will hit our subscribers first

Processing Infrastructure Access as the Capital Efficiency Multiplier

In Chile's converging capital intensity environment, access to existing processing infrastructure is emerging as the primary differentiating variable for project economics. The most capital-efficient development pathway combines fast DIA approval with the ability to avoid constructing dedicated processing capacity entirely.

Heap-leach joint ventures utilising under-utilised solvent extraction-electrowinning (SX-EW) facilities near brownfield oxide deposits represent the clearest expression of this logic. The copper leaching process is a well-established hydrometallurgical method particularly suited to oxide copper deposits, producing cathode copper directly without the smelting and refining steps required for sulphide concentrates.

Where an existing SX-EW plant operates below capacity in the vicinity of a viable oxide deposit, the opportunity exists to compress both capital requirements and build timelines simultaneously by directing ore to that facility rather than constructing new processing infrastructure.

For developers who can structure such arrangements, the result is a non-operated cash flow pathway at a capital intensity profile that the pre-reform, pre-convergence environment would not have distinguished from conventional brownfield development. In the current environment, that distinction is significant.

The Structural Copper Demand Case and Why Reform Timing Matters

Chile copper permitting reforms do not exist in a commodity vacuum. Their significance is magnified by the demand trajectory that multiple institutional forecasters project for copper over the coming decade. In addition, the broader copper supply crunch is intensifying the urgency of reform implementation across the sector.

Three demand vectors are converging on a constrained supply base:

- Grid electrification and transmission infrastructure – copper-intensive at every stage, from generation to distribution

- Electric vehicle adoption – an EV requires approximately 3 to 4 times the copper content of a conventional internal combustion vehicle, with charging infrastructure adding further demand density

- Data centre and AI infrastructure expansion – copper-intensive cooling systems, power distribution networks, and connectivity infrastructure are scaling rapidly alongside AI workload growth

The supply response to that demand trajectory faces a fundamental constraint: vast amounts of capital are currently being deployed simply to maintain existing production levels, leaving limited incremental capacity available to address new demand. This is not a transitory condition driven by cyclical underinvestment. It reflects the compound effect of grade decline, rising extraction costs, and a permitting environment that has historically extended the gap between investment decision and first production by years.

The expectation across multiple institutional research groups is that copper prices must rise materially to incentivise sufficient new supply. This is not a minority analytical position. It reflects convergent reasoning across forecasters who approach the supply-demand balance from different methodological starting points.

How Chile's Reformed Environment Compares to Competing Copper Jurisdictions

Investor capital allocating to copper development does not evaluate Chile in isolation. The reformed permitting environment must be assessed against the practical alternatives available in competing copper geographies.

| Jurisdiction | Permitting Timeline | Fiscal Stability | Grade Profile | Infrastructure Maturity |

|---|---|---|---|---|

| Chile (post-reform) | 12-24 months (DIA pathway) | 25-year stability pact | Declining, large-scale | High – established logistics corridor |

| Peru | 3-7 years (contested projects) | Limited long-term guarantees | Moderate | Moderate – variable by region |

| DR Congo | Variable, elevated sovereign risk | Minimal | High grade, artisanal overlap | Low – significant infrastructure gaps |

| United States | 7-10+ years (federal pathway) | Moderate via IRA framework | Variable | High in established districts |

| Canada | 3-8 years (provincial variation) | Moderate | Variable | High in established provinces |

Against this comparative backdrop, Chile's reformed environment presents a materially improved timeline profile relative to most comparable jurisdictions, combined with a fiscal stability mechanism that few competing geographies can match in scope or duration. The residual risk lies in implementation: whether agency-level coordination delivers approval timelines consistent with the legislative intent, and whether the legal system reinforces rather than undermines the streamlined framework through post-approval challenge proceedings.

Key Takeaways for Investors Evaluating Chilean Copper Exposure

- The Cochilco projection of only ~100,000 tonnes of net new production over a decade of US$105 billion in capital deployment is the clearest quantitative indicator that Chile's structural supply problem is geological and regulatory, not financial

- The Ley de Permisología's 30-70% timeline reduction target represents a wide outcome range; the Marimaca 12-month DIA approval is currently the best available empirical anchor for planning assumptions at the lower end of timeline uncertainty

- The 25-year fiscal stability pact is the more durable reform instrument, directly reducing the sovereign risk discount applied to long-dated copper project cash flows

- Brownfield-greenfield capital intensity convergence means infrastructure access, not project classification, is now the primary determinant of capital efficiency in Chilean copper development

- SX-EW joint venture structures targeting under-utilised existing processing capacity represent the most capital-efficient production pathway available in the current Chilean environment

- The structural copper demand case driven by electrification, EVs, and data infrastructure is broadly convergent across institutional forecasters, providing a macro backdrop against which Chile's reformed regulatory environment carries elevated strategic significance; furthermore, investors seeking exposure may benefit from reviewing available copper investment strategies tailored to the current landscape

This article contains forward-looking analysis, including references to production timelines, permitting outcomes, and commodity price forecasts. These involve inherent uncertainty and should not be construed as financial advice. Readers are encouraged to conduct independent due diligence and consult Cochilco and International Copper Study Group publications for primary data on Chilean copper supply dynamics.

Want to Spot the Next Major Copper Discovery Before the Market Moves?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries — including copper — and delivering actionable alerts to subscribers before the broader market has time to react. Explore historic examples of major mineral discoveries and their extraordinary returns, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the next significant find.