June 10, 2026

The Geology of Scarcity: Why Chile's Copper Decline Is a Structural Story, Not a Cyclical One

Every commodity cycle eventually confronts geology. No amount of operational efficiency, capital investment, or institutional ambition can permanently defer the physics of ore grade depletion. For Chile, the world's dominant copper-producing nation, that confrontation is now well underway, and the implications for the global Chile copper production outlook and price forecasts extend far beyond a single quarterly revision.

Understanding what is happening in Chile's copper sector requires moving past headline numbers and into the mechanics of how large-scale porphyry copper deposits actually age. As copper ore grades fall, the energy input per tonne of extracted metal rises, water consumption increases, and processing infrastructure is strained across longer throughput cycles. At Chile's largest operations, this dynamic has been compressing productive output for years, and 2026 represents a point where the accumulated effect has become impossible to absorb through normal operational adjustments.

When big ASX news breaks, our subscribers know first

Why Chile's 2026 Production Revision Is More Significant Than It Appears

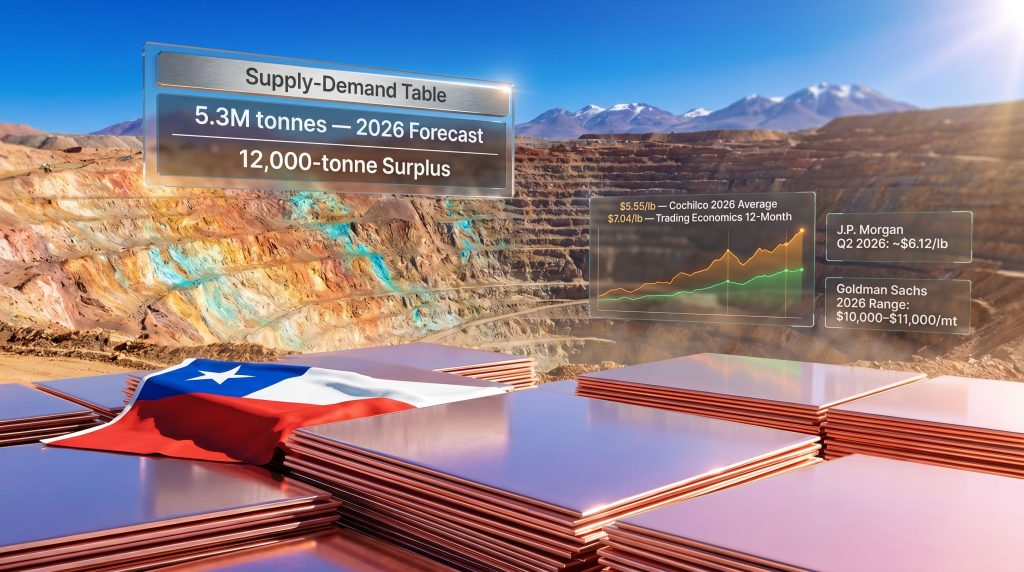

Chile's state copper commission Cochilco revised its 2026 production forecast down to 5.3 million metric tonnes, a 2% decline from prior-year output. The prior guidance had projected 5.6 million tonnes for 2026, meaning the revision represents a shortfall of approximately 300,000 tonnes. Looking further out, 2027 output is now projected to recover only to approximately 5.5 million tonnes, well below the earlier estimate of 5.97 million tonnes.

On the surface, these figures appear manageable. In context, they are not. Chile accounts for roughly 25% of global mined copper supply, which means that a structural shortfall in Chilean output does not merely affect one producer — it reshapes global supply balances. When the marginal producer in a commodity market is simultaneously the largest producer, price sensitivity to its operational performance becomes extreme. The Chile copper supply gap this creates has profound implications for global markets.

Monthly production data from Cochilco reinforces the volatility picture. Output reached 458,400 tonnes in October 2025, then dropped sharply to 378,550 tonnes in February 2026, before recovering to 434,310 tonnes in March 2026. This oscillation reflects the compound effect of maintenance cycles, unplanned stoppages, and grade variability operating simultaneously across multiple mine sites. Furthermore, Chile's copper output delay risks compounding these pressures well into the medium term.

Chilean production hit a 20-year low in 2023, and while a recovery trajectory is now underway, the pace remains well below earlier institutional projections, suggesting the structural constraints are proving more durable than originally anticipated.

The Three Structural Constraints Compressing Chilean Output

Ore Grade Depletion: The Physics That Policy Cannot Fix

Porphyry copper deposits, which dominate Chile's resource base, are characterised by large tonnage but variable grade distribution. In the earliest years of a mine's life, operators typically access higher-grade zones, generating better economic returns per tonne of rock processed. As these zones are exhausted, mining advances into lower-grade material, requiring proportionally greater throughput to maintain equivalent copper output.

This is not a speculative risk. It is the documented trajectory of nearly every large copper mine operating today. At Chile's flagship assets, average copper grades have declined meaningfully over the past decade, and the resulting efficiency losses are now appearing directly in national production statistics. The critical insight here is that grade depletion cannot be resolved through operational improvement alone. It requires either the discovery and development of new high-grade resources, or the deployment of processing technologies capable of economically handling material that was previously considered sub-economic.

A lesser-known dimension of this problem involves what mining engineers call the strip ratio, which describes the volume of waste rock that must be removed to access each tonne of ore. As deposits deepen and grades fall, strip ratios climb, adding to costs and extending the time required to maintain steady-state output. At several Chilean operations, rising strip ratios are compounding the grade depletion effect, creating a dual headwind that is structurally distinct from temporary operational disruptions.

Codelco's Infrastructure Gap and Its Investment Race Against Time

Codelco, the state-owned copper producer that is among the world's largest by output, is executing a multi-year structural investment program with a stated ambition of reaching 1.7 million tonnes per year by 2030. The Codelco production comeback effort is effectively a race against the aging infrastructure profile of its existing asset base. Several of Codelco's core mines, including El Teniente and Chuquicamata, are among the oldest continuously operating large-scale copper mines in the world, and their continued production requires ongoing capital reinvestment at a scale that is difficult to sustain without prioritisation trade-offs.

The near-term execution risk is material. Simultaneous infrastructure renewal across multiple mine sites, in a sector where skilled labour shortages and supply chain delays remain persistent, creates the conditions for cost overruns and timeline slippage. Consequently, if Codelco's production recovery lags its capital schedule, Chile's 2027 output target becomes increasingly aspirational.

Permitting Bottlenecks and the Development Timeline Gap

New project development in Chile faces extended regulatory timelines that delay the conversion of known resources into producing supply. Even where exploration has identified quality deposits adjacent to existing operations, the permitting pathway from discovery to production can span a decade or more. This creates a structural lag between the identification of resource opportunities and their contribution to national output, furthermore limiting Chile's ability to compensate for declining output at mature assets with new production.

Global Supply and Demand: How Fragile Is the 2026 Balance?

| Metric | 2025 (Estimated) | 2026 (Forecast) | 2027 (Forecast) |

|---|---|---|---|

| Global Refined Demand | ~27.8 million tonnes | 28.2 million tonnes | 28.8 million tonnes |

| Demand Growth Rate | – | +1.5% | +2.3% |

| Market Balance | Deficit ~124,000 t | Surplus ~12,000 t | Under Review |

| Chile Production | ~5.4 million tonnes | 5.3 million tonnes | ~5.5 million tonnes |

The projected shift from a 124,000-tonne deficit in 2025 to a 12,000-tonne surplus in 2026 reflects genuine supply improvement. However, a 12,000-tonne surplus in a market that consumes 28.2 million tonnes annually represents a margin of approximately 0.04%. A single unplanned shutdown at a major operation, a tailings facility incident, or an escalation of existing disruptions at Escondida or Grasberg, would be sufficient to eliminate this surplus entirely.

The demand side offers little relief. Global refined copper demand is growing at 1.5% in 2026 and 2.3% in 2027, driven by a combination of Chinese industrial activity, energy transition infrastructure, and emerging demand categories including AI data centre construction. A large-scale data centre requires copper throughout its power distribution architecture, cooling systems, and networking infrastructure, making AI buildout a structurally new demand category that was not meaningfully present in copper demand modelling five years ago.

Beyond data centres, the electrification megatrend continues to expand the copper demand base:

- Solar and wind installations require copper for wiring, transformers, and grid connection

- Electric vehicle powertrains and charging networks use substantially more copper per unit than conventional vehicles

- Grid modernisation programs across the US, Europe, and Asia are copper-intensive at the scale being planned

- Energy storage systems require copper in their manufacturing and installation

The IEA's analysis of copper reinforces this outlook, highlighting that clean energy transitions will place unprecedented pressure on copper supply chains globally. Industry analysts estimate the world may require up to 80 new sizable copper mines by 2040 to meet projected long-run demand. Given that the average development timeline for a new major copper mine spans 16 to 20 years from discovery to production, the supply pipeline challenge is already significantly crystallised.

What Major Institutions Are Forecasting for Copper Prices

Price Forecast Comparison by Institution (2025–2027)

| Institution | Timeframe | Price Forecast | Key Assumption |

|---|---|---|---|

| Cochilco | 2026 Average | $5.55/lb | Tight supply, strong demand |

| Trading Economics | End of Quarter | ~$6.35/lb | Near-term market conditions |

| Trading Economics | 12-Month Outlook | ~$7.04/lb | Demand recovery and supply lag |

| Long Forecast | May 2026 Average | ~$6.27/lb | Current trading range |

| J.P. Morgan | Q2 2026 | Macro-sensitive scenario | |

| J.P. Morgan | Q2 2027 | Demand moderation | |

| J.P. Morgan (bearish floor) | Medium-term | $11,100-$11,200/mt | Macro deterioration scenario |

| Goldman Sachs | 2026 Range | $10,000-$11,000/mt | Post-record-high correction |

Note: Conversion used is approximately $1/lb equal to $2,204/mt. All forecasts represent institutional projections subject to revision.

The Chile copper price forecast reflects Cochilco's revised 2026 estimate of $5.55/lb, representing a 12% upward revision from its prior estimate of $4.95/lb — a significant institutional acknowledgment of sustained market tightness. However, the gap between this forecast and current spot pricing above $6.00/lb in New York reflects genuine uncertainty about price sustainability. Notably, Cochilco's record-high price forecasts signal that institutional confidence in elevated pricing is strengthening.

One underappreciated dynamic in current price formation is the role of speculative positioning. When the global copper market is operating with a surplus measured in the thousands of tonnes rather than millions, even moderate speculative interest in copper futures can exert outsized influence on spot pricing, creating price moves that appear disconnected from physical supply-demand fundamentals in the short term.

The Bearish Case: What Could Pressure Prices Lower?

The downside scenario for copper pricing is primarily macro-driven rather than supply-driven. J.P. Morgan's bearish floor of approximately $11,100-$11,200/mt assumes a scenario in which global industrial activity deteriorates more sharply than base-case projections, reducing Chinese copper consumption growth below trend. A sustained property sector contraction in China, combined with weaker-than-expected infrastructure spending, could offset meaningful portions of the electrification-driven demand growth currently supporting prices.

Goldman Sachs projects a 2026 trading range of $10,000-$11,000/mt, reflecting a view that the post-record-high environment may involve price consolidation even if structural supply tightness persists. In addition, the ongoing copper supply crunch continues to underpin a floor for pricing across most institutional scenarios.

Scenario Analysis: Three Production Pathways Through 2027

Scenario 1: Base Case (Most Probable)

Chilean production stabilises at 5.3 million tonnes in 2026 and recovers to approximately 5.5 million tonnes in 2027. Codelco's structural program delivers incremental gains without material setbacks. Copper prices trade in the $5.50-$6.50/lb range, supported by narrow global surplus conditions.

Scenario 2: Upside Case (Possible)

Maintenance cycles complete ahead of schedule and processing efficiency improvements partially compensate for grade depletion. Chilean production approaches 5.7-5.8 million tonnes by 2027. Widening surplus moderates price appreciation, with copper ranging $5.00-$5.80/lb.

Scenario 3: Downside Case (Tail Risk)

Additional unplanned stoppages or permitting setbacks prevent the projected 2027 recovery. Chilean output remains flat or declines further. Deficit conditions re-emerge and copper prices push toward or beyond $7.00/lb.

The margin between these scenarios is thinner than most market participants appreciate. The 12,000-tonne projected surplus for 2026 represents less than three days of global copper consumption at current demand rates.

The next major ASX story will hit our subscribers first

What This Means for Industrial Consumers, Capital Allocators, and Macro Participants

For industrial consumers with significant copper input requirements, the combination of structural supply constraints and accelerating demand growth creates a compelling case for longer-dated supply contracts and active price hedging programs. Spot market reliance becomes increasingly costly when global surplus is measured in thousands of tonnes.

For the mining investment community, Chile's revised outlook reinforces the capital allocation case for copper project development across alternative geographies. Consequently, emerging copper districts in Africa, Central Asia, and North America are attracting increased interest from major producers seeking to diversify their production base away from jurisdictions facing structural grade decline. The performance of the largest copper mines globally will therefore play an increasingly decisive role in determining how the supply gap evolves through the decade.

For currency and macro participants, Barclays has noted that sustained elevated copper pricing supports the fiscal position and currency strength of copper-rich exporting nations including Chile, Peru, and Indonesia. AI-driven metals demand may provide an additional structural tailwind for these economies beyond the traditional electrification demand narrative.

Frequently Asked Questions

What is Chile's copper production forecast for 2026?

Cochilco has revised Chile's 2026 output forecast down to approximately 5.3 million metric tonnes, a 2% decline from prior-year output and well below the agency's earlier projection of 5.6 million tonnes.

What is causing Chile's copper production decline?

The primary drivers are declining ore grades at aging mine sites, maintenance and operational constraints, and permitting delays affecting new project development. These represent structural challenges rather than temporary disruptions.

What is the copper price forecast for 2026?

Cochilco projects a 2026 average of $5.55/lb, revised up from $4.95/lb. Spot prices have already exceeded $6.00/lb, while Trading Economics projects a 12-month outlook of approximately $7.04/lb. Institutional forecasts vary widely based on macro assumptions.

Is the global copper market in surplus or deficit in 2026?

After an estimated deficit of approximately 124,000 tonnes in 2025, a narrow surplus of around 12,000 tonnes is projected for 2026. This balance is fragile and could reverse with any significant supply disruption, making the Chile copper production outlook and price forecasts critical for monitoring.

How much new copper supply does the world need by 2040?

Industry analysis suggests the world may require up to 80 new sizable copper mines by 2040 to meet projected long-run demand from electrification, EVs, AI infrastructure, and grid expansion. This underscores just how significant the Chile copper production outlook and price forecasts will remain for global commodity markets in the years ahead.

Disclaimer: This article contains forward-looking statements, institutional forecasts, and scenario analyses. All projections are subject to change and should not be construed as financial or investment advice. Past commodity price performance is not indicative of future results. Readers should conduct independent research before making investment decisions.

Want to Position Yourself Ahead of the Next Major Copper Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly turning complex resource data into actionable investment insights for both short-term traders and long-term investors. Explore historic examples of exceptional discovery returns and begin your 14-day free trial today to gain a market-leading edge as copper's structural supply squeeze continues to reshape global commodity markets.