July 25, 2026

The Hidden Fragility Inside the World's Copper Capital

Every commodity supercycle eventually confronts a hard truth: concentrated resource wealth creates economic architecture that is only as stable as the commodity beneath it. For Chile, that commodity is copper, and the country's first quarter 2026 GDP data has exposed just how vulnerable that architecture can become when the metal falters. Understanding the why behind Chile's economy contraction on mining decline requires looking beyond the headline numbers and into the geological, regulatory, and structural forces that make this story more complex than a single quarter of bad weather.

When big ASX news breaks, our subscribers know first

How Copper Became Chile's Economic Backbone

Chile holds the world's largest copper reserves and produces more of the metal than any other nation on earth. This geological endowment has shaped every dimension of the country's economic development: its fiscal architecture, its export composition, its infrastructure investment capacity, and its sovereign credit profile.

Copper consistently accounts for the majority of Chile's total export earnings. Government tax receipts are materially tied to copper royalties and corporate taxes paid by mining companies, meaning that when production volumes or prices decline, fiscal pressure follows almost immediately. The downstream effects are not abstract: weaker mining revenues translate into compressed budgets for public infrastructure, social services, and development programmes.

Furthermore, according to BNP Paribas economic research, Chile's economy remains deeply dependent on the mining sector, with little structural insulation when commodity conditions deteriorate. This dependency is not a recent development — it has been baked into the country's economic model for decades.

Structural Reality: Chile's economic model functions with copper as a macroeconomic lever. When that lever shifts, the entire growth trajectory moves with near-mechanical precision, regardless of performance in other sectors.

Lithium, gold, and silver mining have expanded their contributions in recent years, but none of these sub-sectors carries sufficient economic weight to counterbalance copper's dominance in export receipts or fiscal revenue generation. The copper price forecast for 2025 and beyond remains a critical variable in assessing how quickly Chile can stabilise its growth trajectory.

Breaking Down Chile's Q1 2026 GDP Contraction

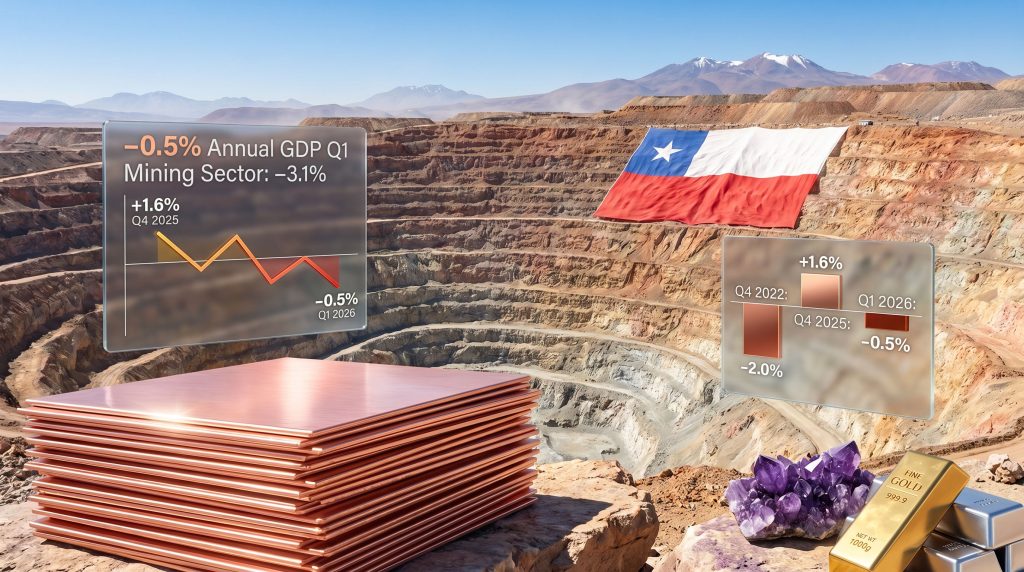

The first quarter 2026 GDP result was considerably worse than markets had anticipated. Chile's central bank data confirmed the following:

| Metric | Value |

|---|---|

| Annual GDP change (Q1 2026) | -0.5% |

| Market consensus expectation | +0.1% |

| Annual growth prior quarter (Q4 2025) | +1.6% |

| Quarterly GDP change (Q1 2026) | -0.3% |

| Prior quarterly expansion (revised) | +0.5% |

| Last comparable annual contraction | Q4 2022 (-2.0% YoY) |

The swing from +1.6% annual growth in Q4 2025 to -0.5% in Q1 2026 represents a 2.1 percentage point deterioration within a single quarter. While the absolute magnitude of the contraction is smaller than the Q4 2022 downturn, the speed of reversal is what distinguishes this event and underscores the economy's acute sensitivity to mining sector variability.

Sector-Level Breakdown

The primary drags on Q1 2026 GDP performance were concentrated in two sectors:

- Mining sector: Declined 3.1% on an annual basis, functioning as the dominant drag on headline growth

- Agriculture and forestry: Fell 5.4% annually, the steepest sectoral decline recorded in the reporting period

- Mining sector (quarterly): Contracted 1.3% quarter-on-quarter, confirming the weakness was not isolated to a single month

- Partial offsets within mining: Lithium, gold, and silver sub-sectors recorded positive growth, providing a modest cushion against the copper-driven decline

The Three Operational Factors Behind Copper's Decline

Chile's central bank attributed the mining sector's underperformance specifically to copper operations. Three distinct but interrelated factors drove the production shortfall:

- Ore grade deterioration: Lower copper mineral grades reduced extraction efficiency across key operations. This is arguably the most structurally significant of the three factors.

- Adverse weather disruptions: Climatic conditions at mine sites impacted both site accessibility and ore processing capacity during the quarter.

- Scheduled and unscheduled maintenance: Equipment and infrastructure servicing reduced production throughput across multiple operations.

Understanding Ore Grade Decline: The Factor That Doesn't Go Away

Of these three factors, ore grade deterioration deserves particular analytical attention because it is not a temporary disruption. As copper deposits mature, the concentration of copper within extracted rock progressively decreases. Miners must therefore process ever-larger volumes of material to yield equivalent copper output, a dynamic that simultaneously increases operating costs and reduces production efficiency.

This phenomenon, known within the industry as grade dilution, is a long-term structural challenge for copper mining globally. Chile's major deposits, including Escondida, the world's largest copper mine, have experienced meaningful grade decline over successive decades of operation. Average copper ore grades across Chilean operations have trended downward from roughly 1.5% copper in the early 2000s toward levels below 0.7% in recent years, according to industry data from the Chilean Copper Commission (Cochilco).

Industry Insight: Grade decline is not a crisis event. It is a slow, compounding pressure that erodes output capacity over years. The danger is that it is easily masked during periods of high prices or operational expansion, only becoming visible when multiple headwinds converge simultaneously.

The interaction between grade decline and adverse weather creates a compounding effect that single-factor analysis consistently underestimates. When ore grades are marginal, any operational interruption that reduces throughput disproportionately impacts recoverable copper tonnage. Understanding grade and permitting challenges is therefore essential for assessing the true depth of Chile's current mining difficulties.

Is This Contraction Temporary or Structural?

Distinguishing between cyclical disruption and structural deterioration is critical for anyone assessing Chile's medium-term growth trajectory. Historical precedent provides useful context.

| Period | GDP Performance | Primary Driver |

|---|---|---|

| Q4 2022 | -2.0% YoY | Broad post-stimulus slowdown |

| Mid-2025 (monthly) | -0.4% MoM | Mining output plunge of 9.3% (largest since 2017) |

| Q4 2025 | +1.6% YoY | Mining recovery and services expansion |

| Q1 2026 | -0.5% YoY | Copper mining decline (grade, weather, maintenance) |

Chile's economy stabilised within subsequent quarters following the mid-2025 monthly shock, suggesting genuine recovery capacity. However, the current episode contains a higher proportion of structural factors than previous downturns, particularly the grade decline dynamic which does not reset between quarters. Chile's copper supply gap remains a persistent concern that compounds the difficulty of any near-term recovery.

The Permitting and Investment Bottleneck

Beyond geology, regulatory dynamics represent a growing constraint on Chile's mining sector growth capacity. According to mining industry analysis, permitting — not geology — is increasingly identified as the primary reason Chile's mining sector is stalling. Approval timelines for new mining projects have extended significantly, creating a widening gap between exploration activity and production commencement.

Key aspects of this bottleneck include:

- Permitting delays are increasingly cited as the primary operational constraint on sector expansion, not geological availability

- Labour shortages at major project sites compound execution timelines for capital projects already in the approval pipeline

- The lag between final investment decision and first production contribution typically spans multiple years in large-scale copper operations

- Neighbouring Argentina is advancing its own copper development frameworks with increasing competitive intent, though Chile's established infrastructure and experienced workforce maintain meaningful structural advantages

Analyst forecasts from institutions including BNP Paribas placed Chile's 2025 full-year GDP growth at approximately 2.2%, contingent on stable mining sector performance. Key risk flags identified in those projections included volatile copper and lithium commodity pricing, fiscal consolidation pressures, and sustained investment uncertainty within the mining sector.

The Central Bank's Difficult Balancing Act

Chile's monetary policymakers face a genuinely difficult environment. Inflation accelerated during March and April 2026, partly driven by commodity price pressures linked to geopolitical conflict affecting global energy supply chains. The simultaneous presence of economic contraction and rising inflation creates a stagflationary policy dilemma.

Capital Economics analyst Kimberley Sperrfechter noted that while the weak GDP result may moderate hawkish sentiment within the central bank, policymakers are expected to maintain their primary focus on inflation management rather than pivoting aggressively toward growth support.

This assessment carries important implications:

- Rate-cutting capacity is constrained by inflation dynamics, limiting the central bank's ability to stimulate the economy through monetary channels

- Fiscal space is similarly compressed by lower mining-related tax revenues, reducing the government's counter-cyclical spending capacity

- The policy toolkit available to support growth is narrower than it would be in a single-challenge environment

The next major ASX story will hit our subscribers first

Global Copper Markets: Why Chile's Contraction Matters Beyond Its Borders

Chile's Q1 2026 copper output decline does not occur in isolation. It arrives at a moment when global copper demand projections are pointing sharply upward, driven by energy transition infrastructure buildout, electric vehicle manufacturing scale-up, and power grid expansion programmes across multiple continents.

Copper's role in the energy transition is often underappreciated in terms of volume requirements. A single offshore wind turbine requires roughly three to four tonnes of copper per megawatt of installed capacity. Electric vehicles contain approximately two to four times the copper of an equivalent internal combustion engine vehicle. Grid infrastructure upgrades required to accommodate distributed renewable generation represent some of the largest copper demand growth vectors in decades.

Against this demand backdrop, any sustained reduction in Chilean copper supply tightens global market balances with direct price implications for downstream industries worldwide. The world's largest copper producer experiencing the convergence of grade decline, weather disruption, and regulatory bottlenecks simultaneously represents a supply-side risk that commodity markets are still pricing with insufficient seriousness.

Lithium, Gold, and Silver: The Diversification Buffer Takes Shape

Within Chile's mining sector, the positive performance of lithium, gold, and silver operations during Q1 2026 deserves recognition as more than a footnote. Chile holds some of the world's largest lithium brine deposits, concentrated in the Atacama Desert's salt flat ecosystems, and growing lithium production capacity represents a genuine strategic diversification opportunity.

The Atacama lithium brines are notable for their exceptionally high lithium concentrations compared with hard-rock spodumene deposits found in Australia and elsewhere. Brine grades in the Atacama can reach 1,500 to 2,000 parts per million lithium, versus the energy-intensive processing requirements of hard-rock alternatives. This geological advantage supports lower-cost production but also requires careful water management given the hydrological sensitivity of the region.

However, lithium's current economic weight within Chile's national accounts remains insufficient to offset copper's dominant influence. Scaling Chile lithium resources to a level where they can meaningfully buffer copper cyclicality is a medium-to-long term objective, not a near-term stabilising mechanism.

The Path Forward: Structural Reform Priorities

For Chile to reduce its vulnerability to mining cycle volatility, several structural reform areas require focused policy attention:

- Permitting acceleration: Streamlining regulatory approval processes for new mining projects is the most direct mechanism for closing the investment-to-production gap

- Sectoral diversification within mining: Scaling lithium, gold, and silver operations reduces single-commodity concentration risk within the sector itself

- Broader economic diversification: Developing competitive services, technology, and manufacturing sectors reduces the entire economy's sensitivity to mining cycles

- Fiscal buffer mechanisms: Strengthening sovereign wealth fund architecture to smooth revenue volatility during mining downturns provides macroeconomic resilience

Despite Q1 weakness, Chile's medium-term mining investment pipeline remains substantive, with multiple large-scale projects in development phases. The critical variable is execution speed, and whether committed capital can be translated into operational production capacity within a competitive and increasingly contested global landscape.

Strategic Takeaway: Chile's economy contraction on mining decline is a symptom of a deeper structural condition. The country has not yet successfully decoupled its growth trajectory from the operational performance of a single commodity. The transition toward a more balanced economic architecture is genuinely underway, but it remains incomplete at the precise moment when global copper supply constraints are becoming most consequential.

Frequently Asked Questions: Chile's Economy and Mining Decline

Why did Chile's economy contract in Q1 2026?

Chile's GDP declined 0.5% on an annual basis in Q1 2026, driven primarily by a 3.1% contraction in the mining sector. Copper mining was affected by lower ore grades, adverse weather conditions, and maintenance-related production interruptions. A simultaneous 5.4% decline in agriculture and forestry compounded the overall economic weakness.

How significant is copper mining to Chile's economy?

Copper mining is the single most important driver of Chile's economic performance, contributing substantially to export revenues, government tax receipts, and GDP growth. Because of this concentration, operational disruptions in copper production can produce measurable contractions in national output within a single reporting quarter.

Is the economic contraction likely to be permanent?

The Q1 2026 contraction reflects a combination of temporary operational factors and longer-term structural pressures including ore grade decline and permitting bottlenecks. While the economy is not in structural collapse, sustained underinvestment in new mining capacity and regulatory delays pose meaningful medium-term risks to growth recovery.

How does lithium factor into Chile's economic outlook?

Lithium mining grew during Q1 2026 even as copper declined. Chile holds some of the world's largest and highest-grade lithium brine deposits, and expanding lithium production represents a strategically significant diversification opportunity. However, lithium's current economic weight remains insufficient to offset copper's dominant influence on national growth metrics.

Disclaimer: This article contains forward-looking analysis, forecasts, and economic projections based on publicly available data and third-party research. These projections are subject to revision and should not be interpreted as financial or investment advice. Readers should conduct independent research before making any investment decisions related to the mining sector or Chilean economic assets.

Want to Stay Ahead of the Next Major Mineral Discovery?

While Chile's copper sector grapples with grade decline and structural headwinds, real opportunities continue to emerge across ASX-listed mineral explorers — and Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant discoveries are announced, turning complex geological data into actionable investment insights. Explore historic discoveries and their remarkable returns, then begin your 14-day free trial to ensure you're positioned ahead of the broader market.