June 4, 2026

The Geology That Built a Global Monopoly

Few commodity markets are as geographically concentrated as iodine. While critical minerals like lithium and cobalt attract the bulk of investor attention, iodine quietly underpins some of the most essential industries on the planet, from pharmaceutical contrast media to LCD display manufacturing, yet its supply base remains anchored to a single desert in northern Chile. Chile iodine investments SQM and Cosayach have come to define this concentrated supply landscape with a tenacity that no competing region has managed to disrupt.

Understanding why requires a look underground. The Atacama Desert sits atop one of the most geochemically unusual ore systems on Earth: caliche, a sedimentary formation rich in nitrate salts that also concentrates iodine at commercially viable grades through a process of ancient marine aerosol deposition and long-term evaporative enrichment. Furthermore, what makes Chilean caliche exceptional is not merely the presence of iodine, but its concentration relative to the cost of extraction.

Iodine grades in Atacama caliche deposits are substantially higher than those found in competing brine formations in Japan or Oklahoma, and the processing complexity is correspondingly lower. This creates a structural cost advantage that has proven remarkably durable over decades of global competition, closely intertwined with Chile's lithium strategy and the broader management of its irreplaceable northern desert resources.

When big ASX news breaks, our subscribers know first

Why Chilean Caliche Cannot Be Easily Replicated

The formation of iodine-rich caliche is the product of millions of years of specific climatic and geological conditions that are essentially unique to northern Chile. The hyperarid environment of the Atacama, combined with the geochemical signature of ancient marine sediments and the absence of significant rainfall leaching, has preserved iodine concentrations that would have been diluted or dispersed in virtually any other geological setting on Earth.

This matters for investors and analysts assessing supply-side risk. Competing iodine sources face structural disadvantages that cannot be resolved through capital investment alone:

- Japanese brine operations extract iodine as a co-product of natural gas production from deep subsurface brines, meaning iodine output is partly a function of gas field activity rather than iodine demand

- Oklahoma and Texas brine producers face lower iodine concentrations per unit of processed fluid, requiring larger volumes and higher energy inputs to achieve equivalent output

- Emerging Central Asian sources, including Turkmenistan and Azerbaijan, remain operationally immature and face significant infrastructure and geopolitical headwinds

- Deep-sea iodine recovery remains largely theoretical at commercial scale, with no producer having demonstrated viable economics — a dynamic broadly consistent with wider deep-sea mining concerns around feasibility and environmental risk

The result is a global supply structure that looks less like a competitive commodity market and more like a geologically mandated oligopoly.

| Producing Region | Primary Source | Estimated Global Share | Structural Constraint |

|---|---|---|---|

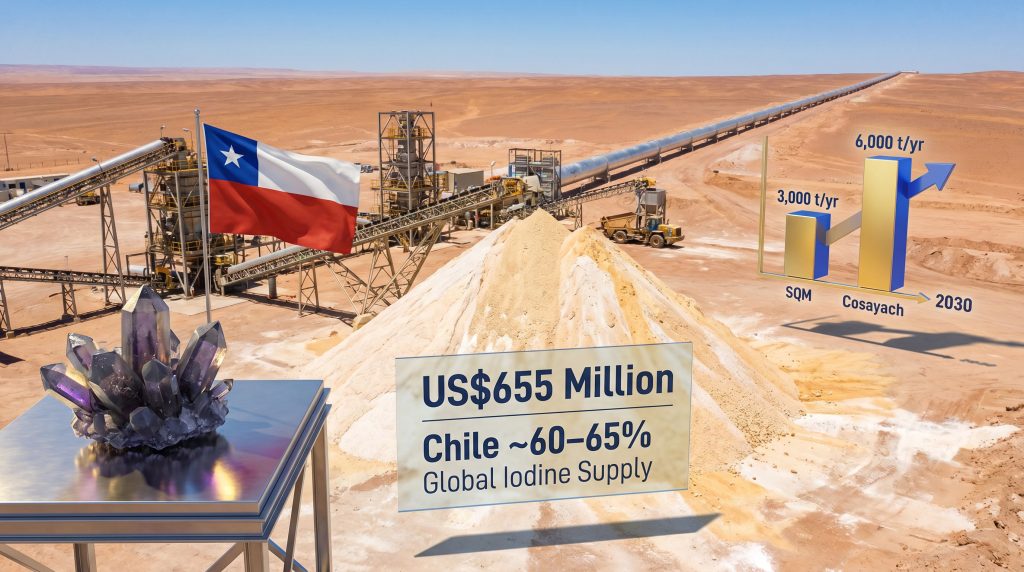

| Chile (Atacama) | Caliche ore | ~60–65% | Water scarcity, SEIA approvals |

| Japan | Deep brine (gas co-product) | ~25–30% | Gas field dependency |

| United States | Brine (Oklahoma/Texas) | ~5–10% | Lower grades, higher processing costs |

| Other (Central Asia, etc.) | Various | ~5% | Infrastructure immaturity |

Chile Iodine Investments: SQM and Cosayach Define the Expansion Cycle

The combined capital commitment from Chile's two dominant iodine producers, SQM and Cosayach, now totals approximately US$655 million, representing one of the most significant coordinated capacity expansions the global iodine market has seen in a generation. These investments are not simultaneous announcements from a shared strategy, but rather two independently motivated decisions that together signal producer-level confidence in sustained demand growth through the latter half of this decade.

SQM: Vertical Integration and the US$1.9 Billion Capex Framework

SQM's position at the top of the global iodine supply chain is supported not just by volume, but by the structural economics of its operations. The U.S. Geological Survey identified SQM as the world's largest iodine producer, with recorded output of 12,082 tonnes in 2019. What makes this figure particularly meaningful is the cost context behind it: SQM extracts iodine from caliche ore as part of a co-production process alongside nitrates, meaning the fixed operational costs of mining and ore processing are distributed across multiple revenue-generating products simultaneously.

This co-production model is a critical and often underappreciated feature of SQM's competitive position. Understanding ore mineralogy and mining economics helps contextualise why, when iodine is produced alongside potassium nitrate and sodium nitrate, the marginal cost of each additional tonne of iodine is substantially lower than it would be for a single-product operation. This structural cost advantage allows SQM to remain profitable at iodine price levels that would squeeze or eliminate standalone producers.

SQM's capital expenditure program for 2021 to 2024 totalled US$1.9 billion across its diversified mineral portfolio, with approximately US$440 million specifically directed toward caliche-based operations. Key components of this investment included:

- Expansion of caliche mining and processing infrastructure targeting 3,000 tonnes per year of iodine production capacity

- Construction of a seawater pipeline to replace freshwater inputs, directly addressing Atacama water scarcity constraints

- Downstream derivative development through a joint venture with Ajay Chemicals, extending SQM's value capture beyond raw iodine into specialty iodine compounds

| Investment Component | Allocated Capital | Strategic Objective |

|---|---|---|

| Caliche operations (iodine and nitrates) | ~US$440 million | Capacity expansion to 3,000 t/yr iodine |

| Seawater pipeline infrastructure | Included in capex | Water security and environmental compliance |

| Iodine derivatives (JV with Ajay Chemicals) | Ongoing operational | Downstream value capture |

| Total multi-year capex program | US$1.9 billion | Diversified mineral expansion (2021–2024) |

Cosayach: The Quietly Significant Second Force

While SQM commands the most public market visibility, Cosayach operates as Chile's second-largest iodine producer with a reported production capacity of approximately 6,000 tonnes per year across its northern Atacama caliche operations. As a privately held company, Cosayach maintains a considerably lower public profile than its listed counterpart, yet its operational scale makes it a structurally indispensable participant in global iodine supply.

Analytical Note: Reported production capacity figures require careful interpretation. Capacity represents a theoretical ceiling, not a guaranteed output. Ore grade variability across mining faces, equipment availability, and seasonal operational disruptions all influence actual throughput. Analysts and investors should treat headline capacity numbers as upper-bound estimates and apply utilisation discounts when modelling real-world supply volumes.

| Dimension | SQM | Cosayach |

|---|---|---|

| Global ranking | No.1 iodine producer (USGS, 2019) | No.2 Chilean iodine producer |

| Reported production capacity | Expanding to ~3,000 t/yr (post-capex) | ~6,000 t/yr (reported capacity) |

| Business model | Vertically integrated, multi-commodity | Focused caliche iodine producer |

| Capital markets profile | NYSE/ASX listed, high disclosure | Privately held, lower visibility |

| Downstream derivatives | Yes, via Ajay Chemicals JV | Limited public disclosure |

Demand Drivers: What Is Absorbing Global Iodine Supply?

Understanding why chile iodine investments SQM and Cosayach are being made at this scale requires a clear-eyed assessment of where demand is heading. Global iodine consumption is projected to grow at a compound annual rate of approximately 3 to 5 percent through 2030, driven by a diverse and largely non-cyclical set of end uses. This trajectory aligns closely with broader critical minerals demand forecasts tied to the global energy transition.

Pharmaceutical and medical applications represent the most structurally resilient demand segment. Iodinated contrast media used in CT scanning and X-ray diagnostics consumes significant iodine volumes globally, and this demand is underpinned by ageing demographics across developed economies and expanding diagnostic infrastructure in emerging markets.

LCD polarising film manufacturing has historically been a major iodine consumption vector, with iodine used to align polymer chains within the polarising layers of flat panel displays. However, this segment faces a meaningful structural headwind as OLED technology displaces LCD in premium consumer electronics. Producers and traders tracking iodine demand should model a gradual but real erosion in display-related consumption over the second half of this decade.

Agricultural and industrial applications include iodine-based disinfectants for livestock operations, animal feed supplements, and crop protection compounds. These segments offer steady, if unspectacular, volume growth tied to global food production trends.

Emerging specialty chemical and electrolyte applications represent perhaps the most speculative but potentially significant demand vector for the late 2020s. Research into iodine-based electrolyte systems for certain battery chemistries and specialty polymer applications is at early stages, but if any of these pathways achieves commercial scale, the demand implications for an already supply-constrained market could be material.

Three Strategic Readings of a US$655 Million Commitment

When two producers sharing the same geological basin announce a combined investment exceeding half a billion dollars in the same commodity, it invites interpretation beyond the headline figure. Three analytical frameworks help contextualise what this capital deployment actually signals.

Demand confidence: At its most straightforward, this level of investment reflects producer-level conviction that consumption growth will be sufficient to absorb expanded supply without triggering a price correction. Neither SQM nor Cosayach would rationally commit this scale of capital without internal demand forecasts supporting it.

Competitive pre-emption: In oligopolistic commodity markets, capacity expansion by the market leader functions partly as a deterrent signal. By building low-cost production capacity ahead of the demand curve, Chilean producers raise the barrier for new entrants from Central Asia or deepening brine operations elsewhere to compete on price. This is a textbook example of capacity-based competitive moat construction.

Infrastructure modernisation: A meaningful portion of both investment programs is directed not at new capacity creation but at replacing ageing infrastructure and meeting tightening environmental compliance requirements. The seawater pipeline component of SQM's program is the clearest illustration of this dynamic, converting what is partly a regulatory necessity into a long-term operational advantage.

Environmental Constraints and Regulatory Risk in the Atacama

The Atacama Desert presents one of the most challenging environmental operating contexts in global mining. Water availability is the binding constraint, with the region receiving less than 15 millimetres of rainfall annually in many areas, making every litre consumed by industrial operations a point of ecological and community tension.

Chile's Sistema de Evaluación de Impacto Ambiental, commonly referred to as SEIA, governs the environmental approval process for major mining expansions. Projects of the scale being undertaken by SQM and Cosayach are subject to comprehensive environmental impact assessments that can extend investment lead times by 12 to 36 months beyond initial capital commitment. This timeline risk is frequently underweighted in market analyses that treat announced capex as equivalent to near-term capacity.

Risk Callout: Environmental conflicts in northern Chile's mining regions have historically caused project delays and cost escalations. The intersection of indigenous land rights under Chile's constitutional framework, acute water scarcity, and internationally recognised biodiversity sensitivity creates a multi-stakeholder risk environment that headline capital figures do not capture.

SQM's seawater pipeline investment is a direct response to this regulatory reality, substituting desalinated or transported seawater for freshwater extraction and reducing the company's exposure to future water-use restrictions. This infrastructure investment carries both operational and reputational value in an environment where social licence is an increasingly material factor in project viability.

The next major ASX story will hit our subscribers first

Iodine as a Portfolio Stabiliser Within SQM's Multi-Commodity Strategy

One of the less discussed but analytically important aspects of SQM's iodine expansion is how it functions within a broader multi-commodity earnings structure. SQM's northern Chilean operations produce iodine and nitrates from caliche, while separate brine extraction operations at the Salar de Atacama yield lithium carbonate and lithium hydroxide. This operational architecture distributes fixed costs across multiple revenue streams and creates a natural earnings hedge, a point well illustrated by the dynamics surrounding Chile's lithium reserves and the policy decisions shaping their long-term development.

The relevance of this structure became particularly visible during the 2023 to 2024 lithium price correction, when spot lithium carbonate prices fell sharply from historic highs. During this period, SQM's iodine and specialty plant nutrition revenues provided a degree of earnings stability that pure-play lithium producers could not access. The pharmaceutical and industrial demand base for iodine does not correlate with electric vehicle production cycles, making it a genuinely countercyclical buffer within SQM's earnings profile.

For investors evaluating SQM as a portfolio holding, this multi-commodity structure is an underappreciated source of resilience. The company's iodine business is not merely an adjunct to its lithium operations; it is a structurally distinct revenue stream with different demand drivers, different customer relationships, and different price dynamics. Consequently, analysts who model SQM purely through a lithium lens risk materially mischaracterising the company's earnings stability.

FAQ: Chile Iodine Investments, SQM and Cosayach

What is the total combined investment from SQM and Cosayach in Chilean iodine operations?

Combined disclosed investment activity totals approximately US$655 million, encompassing capacity expansion, infrastructure upgrades, and environmental compliance projects across both companies' caliche operations in northern Chile. The BNamericas analysis of this investment cycle provides additional context on how these commitments are expected to reinforce Chile's global iodine leadership through the remainder of the decade.

How much iodine does SQM currently produce?

The USGS identified SQM as the world's largest iodine producer, with recorded output of 12,082 tonnes in 2019. The company's current capex program targets annual production capacity of 3,000 tonnes from its expanded caliche operations, though this figure likely reflects one operational segment rather than total company-wide output.

What is Cosayach's reported iodine production capacity?

Cosayach has a reported production capacity of approximately 6,000 tonnes per year across its northern Chilean caliche operations, making it a globally significant producer despite its relatively low public market profile.

Why does Chile dominate global iodine production?

Chilean dominance is rooted in the geological uniqueness of Atacama caliche deposits, which concentrate iodine at grades and extraction costs that competing regions cannot replicate. Decades of operational infrastructure investment have compounded this geological advantage into a durable competitive moat.

What are the primary risks to the Chilean iodine expansion timeline?

Environmental approval processes under Chile's SEIA framework can extend project timelines by 12 to 36 months. Water scarcity constraints, indigenous community rights, and broader social licence considerations represent additional risk factors that can affect both timelines and operating costs.

Disclaimer: This article is intended for informational purposes only and does not constitute financial or investment advice. Forward-looking statements regarding demand growth, production capacity, and investment timelines involve inherent uncertainty. Readers should conduct independent due diligence before making any investment decisions. All capacity and production figures cited reflect publicly available data and reported estimates; actual operational output may differ materially.

Want to Identify the Next Major Mineral Discovery Before the Broader Market?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex geological and commodity data into actionable investment insights — explore the historic returns major discoveries have generated and begin your 14-day free trial today to position yourself ahead of the market.