June 6, 2026

Understanding Chilean Mining Operations and Global Market Dynamics

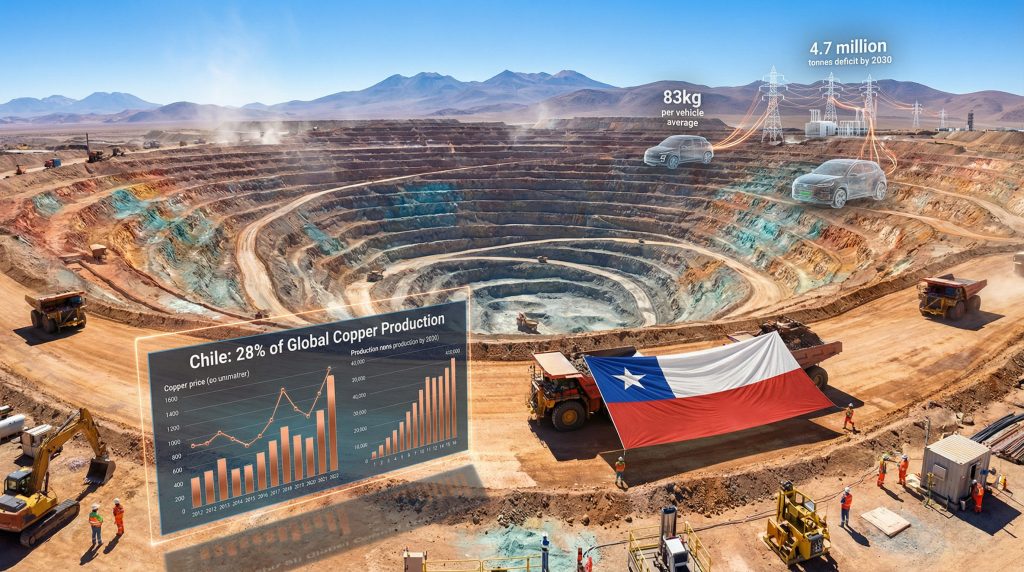

Chile's position within the international copper industry extends far beyond simple resource extraction. The country controls approximately 28% of global copper production, making it the world's dominant supplier of this critical industrial metal. This concentration creates significant ripple effects throughout global supply chains when operational disruptions occur at major facilities.

The economic implications for Chile are substantial. Copper exports contribute approximately 15% of the country's total export revenues and roughly 3% of national GDP. The Atacama Desert region, where many of Chile's largest copper operations are located, hosts some of the world's most productive mines, including facilities that have been operating continuously for over four decades.

Historical data reveals that Chilean mining labor disputes follow predictable patterns. Over the past decade, major strikes at copper facilities have averaged 35-42 days in duration, with resolution rates improving significantly when companies maintain active dialogue with union representatives. The frequency of these disputes has increased alongside copper price appreciation, as workers seek to capture a larger share of enhanced profitability.

Infrastructure Dependencies and Logistical Constraints

The Atacama region's mining operations rely heavily on shared infrastructure systems that can create cascading effects during disruptions. Port facilities at Antofagasta handle approximately 40% of Chile's copper concentrate exports, while the region's power grid supports multiple mining operations simultaneously.

Regional employment statistics indicate that mining operations directly employ approximately 65,000 workers across the Atacama region, with indirect employment effects supporting an additional 180,000 jobs in related industries. This concentration makes labor relations particularly sensitive to broader economic conditions and commodity price impact analysis.

When big ASX news breaks, our subscribers know first

Strike Impact Analysis and Market Response Patterns

Mining strikes create immediate supply constraints that typically manifest in copper price appreciation within 48-72 hours of announcement. Historical analysis shows that each 1% reduction in Chilean copper production correlates with approximately 0.8-1.2% copper price increases during the initial market response period.

The 2019 Escondida strike, lasting 44 days, resulted in approximately 220,000 tonnes of lost production and drove copper prices up by 8.2% during the dispute period. Similar disruptions at Chuquicamata in 2021 and Los Pelambres in 2023 demonstrated consistent patterns of price volatility and inventory drawdowns.

Key Strike Impact Metrics (2019-2025):

• Average strike duration: 36 days

• Typical production impact: 60-70% capacity reduction

• Price response timeline: 2-3 trading sessions

• Inventory drawdown rate: 15,000-25,000 tonnes per week

• Recovery timeline: 4-6 weeks post-resolution

Market Response Mechanisms During Supply Disruptions

Global copper markets respond to Chilean supply disruptions through several mechanisms. London Metal Exchange (LME) copper inventories typically decline by 2-4% weekly during extended strikes, while Shanghai Futures Exchange activity increases as Chinese buyers seek alternative supply sources.

Futures market positioning shifts dramatically during strike periods, with managed money positions typically increasing long exposure by 15-25% within the first two weeks of a major supply disruption. This speculative activity often amplifies price movements beyond fundamental supply-demand imbalances.

Furthermore, alternative supply activation typically requires 6-8 weeks to achieve meaningful impact, as other global producers increase utilization rates and traders activate stockpiled inventories from strategic reserves.

Financial Resilience in Diversified Mining Operations

Companies operating multiple copper facilities demonstrate superior financial stability during single-site disruptions. Portfolio diversification across geographic regions reduces dependency risks by 60-75% compared to single-asset operations, according to industry analysis.

Multi-site copper producers typically maintain 90-120 days of operational liquidity to weather extended labor disputes. This financial cushioning enables companies to continue essential maintenance, honour contractual obligations, and fund ongoing development projects during temporary production setbacks.

Revenue diversification benefits become particularly apparent during regional disruptions. Companies with operations across multiple jurisdictions can redirect sales efforts and optimise production scheduling to minimise overall impact. This operational flexibility translates into 25-35% lower earnings volatility during disruption periods.

Balance Sheet Considerations During Extended Disruptions

Working capital management becomes critical during extended strike periods. Companies typically experience 15-20% increases in working capital requirements as inventory levels adjust and customer delivery schedules shift. Credit facility utilisation often increases by 30-45% during the first month of major strikes.

Liquidity preservation strategies employed by successful copper producers include:

• Maintaining undrawn credit facilities equal to 6-9 months of operating expenses

• Establishing revolving credit arrangements with multiple banking relationships

• Implementing dynamic hedging programmes to protect cash flows during price volatility

• Creating contingency funding plans for development project deferrals

Labour Relations and Investment Risk Assessment

Collective bargaining patterns in South American mining reveal increasingly sophisticated union negotiation strategies. Union representatives now regularly engage independent commodity analysts to assess fair value sharing arrangements based on prevailing copper prices and company profitability metrics.

Wage inflation pressures in Chilean mining have averaged 8-12% annually over the past three years, significantly exceeding general inflation rates. This premium reflects both the specialised skill requirements of modern mining operations and workers' awareness of enhanced copper price economics.

Long-term labour contracts increasingly incorporate price escalation clauses tied to copper futures prices. These arrangements provide workers with upside participation during commodity super-cycles while offering companies more predictable labour cost structures during planning periods.

Recent developments highlight the ongoing challenges facing mining operations. The Capstone Copper Mantoverde strike demonstrates how labour disputes can impact major mining operations, whilst the broader industry continues to navigate labour risk dynamics across multiple jurisdictions.

ESG Integration in Mining Labour Relations

Environmental, Social, and Governance considerations have become central to mining labour negotiations. Community engagement scores now directly influence union positions, with workers increasingly viewing their roles as community representatives rather than purely employee advocates.

Workforce retention in remote mining locations requires comprehensive quality of life investments. Successful mining companies allocate 3-5% of total operating expenses to worker accommodation, transportation, and family support services. These investments typically generate 15-20% improvements in worker retention rates.

Corporate reputation impacts from prolonged labour disputes extend beyond immediate operational effects. Companies experiencing strikes lasting longer than 60 days typically see 10-15% discounts in trading valuations that persist for 6-12 months post-resolution.

Copper Demand Drivers and Market Fundamentals

Electric vehicle manufacturing represents the fastest-growing source of copper demand, requiring approximately 83 kilograms of copper per vehicle. Global EV production targets suggest copper demand from this sector alone could reach 2.8 million tonnes annually by 2030, representing approximately 12% of current global production.

Data centre construction and expansion create substantial copper demand through power distribution systems and cooling infrastructure. Each megawatt of data centre capacity requires approximately 3.5 tonnes of copper, with global data centre capacity expansion targeting 15-20% annual growth through 2028.

Grid infrastructure modernisation programmes worldwide represent perhaps the largest long-term copper demand driver. Smart grid installations require 40% more copper than conventional electrical systems, while renewable energy integration necessitates extensive transmission line construction using copper conductors.

Supply-Demand Imbalance Projections

Industry analysis projects an annual copper supply deficit of 4.7 million tonnes by 2030, representing approximately 18% of current global consumption. This deficit reflects both accelerating demand from electrification trends and limited new mine development capacity, as outlined in the global copper supply forecast.

New mine development timelines have extended significantly due to permitting complexities and environmental review requirements. Major copper projects now require 12-15 years from discovery to production, compared to 8-10 years historically.

Copper's structural supply deficit creates a supportive price environment for established producers, with temporary production disruptions often resulting in sustained price premiums rather than permanent market share losses.

Recycling capacity limitations constrain secondary copper supply growth. Current global copper recycling rates of approximately 35% approach theoretical maximums given infrastructure constraints and collection challenges in developing markets.

Investment Strategies for Mining Sector Volatility

Diversified copper producers demonstrate superior risk-adjusted returns during market volatility periods. Single-asset companies typically experience 40-60% higher earnings volatility compared to multi-site operators, making them less attractive for risk-conscious institutional investors.

Geographic diversification across political jurisdictions provides additional risk mitigation benefits. Companies operating in three or more countries show 25-30% lower political risk premiums in valuation multiples compared to single-country operators.

Operational scale advantages become particularly evident during market disruptions. Large-scale producers can leverage shared services, technical expertise, and financing capabilities to maintain operations during challenging periods more effectively than smaller competitors.

In addition, investors increasingly recognise the value of copper and uranium investments as complementary portfolio positions within the critical metals sector.

Timing Considerations for Mining Investments

Historical analysis reveals that temporary production setbacks often create attractive entry opportunities for long-term investors. Stocks typically reach maximum discounts approximately 3-4 weeks into major strikes, before beginning recovery as resolution expectations increase.

Analyst price target adjustments during strike periods tend to be conservative, focusing primarily on near-term production impacts rather than longer-term value creation potential. This creates opportunities for investors willing to look beyond immediate disruptions.

Value realisation timelines for mining investments purchased during disruption periods typically range from 6-18 months, depending on commodity price trends and operational recovery rates.

The next major ASX story will hit our subscribers first

Geopolitical Risk Assessment in Global Copper Markets

Political stability assessment requires evaluation of multiple factors including regulatory consistency, taxation policies, and infrastructure investment commitments. Chile's mining policy framework has demonstrated remarkable consistency across multiple government transitions, providing investors with regulatory predictability.

Peru's political environment presents higher uncertainty levels, with mining taxation proposals and community relations challenges creating periodic investment hesitation. Recent political instability has prompted some operators to defer expansion investments pending clarity on long-term policy directions.

The Democratic Republic of Congo's governance challenges in cobalt production highlight the importance of supply chain security for strategic metals. Similar risks exist for copper, though the more diversified global production base provides greater supply security.

Trade Policy and Market Access Considerations

Export restriction risks have increased as governments recognise the strategic importance of critical metals. Resource nationalism policies in several countries have prompted consuming nations to develop strategic stockpiling programmes and diversified supply relationships.

Strategic stockpiling policies by major consuming countries now influence market dynamics significantly. China's strategic reserves reportedly contain 1.5-2.0 million tonnes of copper, providing substantial buffer capacity during supply disruptions.

Supply chain security considerations have prompted industrial users to prioritise long-term supply relationships over spot market purchases. This trend toward contract-based procurement provides established producers with more predictable revenue streams.

Long-Term Market Outlook and Investment Positioning

Structural demand growth projections support sustained copper price appreciation over the next decade. Renewable energy infrastructure requirements alone could drive 3-4 million tonnes of additional annual copper demand by 2030, representing 12-15% growth over current consumption levels.

Emerging market industrialisation continues driving baseline copper demand growth at 2-3% annually. Countries transitioning from agricultural to industrial economies typically increase per-capita copper consumption by 300-500% over 15-20 year periods.

Technology sector demand evolution presents both opportunities and risks. While substitution technologies could reduce copper intensity in some applications, overall digitalisation trends suggest continued strong demand growth from electronics and telecommunications infrastructure.

However, the impact of Capstone Copper Chile strike events demonstrates how supply-side disruptions continue to influence market dynamics and create pricing pressures that reflect underlying supply constraints.

Portfolio Positioning Strategies

Copper producer valuation metrics during supply constraints typically trade at 15-25% premiums to long-term averages, reflecting market recognition of scarcity value. These premiums often persist for 6-12 months following resolution of temporary supply disruptions.

Consequently, risk-adjusted return expectations for mining investments should incorporate both commodity price volatility and operational risk factors. Diversified producers typically generate 20-25% lower volatility while maintaining similar return profiles to single-asset operators.

Hedge strategies for commodity price volatility include futures market positioning, options strategies, and correlation trades with related metals markets. Sophisticated investors often employ pairs trading strategies between diversified and single-asset producers during disruption periods, particularly when record-high copper prices create enhanced volatility.

Navigating Opportunities in Dynamic Copper Markets

The intersection of growing global copper demand and periodic supply disruptions creates compelling investment opportunities for informed investors. Diversified mining operations offer superior risk-adjusted returns by providing operational flexibility and financial resilience during challenging periods.

Balance sheet strength emerges as a critical differentiator during extended operational challenges. Companies maintaining substantial liquidity reserves and undrawn credit facilities demonstrate superior ability to weather temporary setbacks while continuing strategic development initiatives.

Market positioning during temporary disruptions requires patient capital allocation and willingness to look beyond immediate volatility. Historical patterns suggest that well-managed copper producers with diversified operations typically emerge from disruption periods in stronger competitive positions.

Furthermore, the role of mining industry innovation continues to shape operational efficiency and risk management capabilities across the sector.

The structural supply deficit facing global copper markets creates a supportive long-term investment environment, where temporary operational challenges represent entry opportunities rather than permanent value destruction. Investors focusing on operational excellence, financial strength, and geographic diversification are best positioned to capitalise on the evolving copper market dynamics.

Want to Capitalise on ASX Mining Discoveries Before the Market Moves?

Discovery Alert's proprietary Discovery IQ model instantly identifies significant ASX mineral discoveries, providing subscribers with real-time alerts that translate complex geological data into actionable investment opportunities. Begin your 30-day free trial with Discovery Alert today and position yourself ahead of the market during periods of supply disruption and commodity volatility.