July 30, 2026

The Structural Logic Behind China's African Lithium Offensive

When industrial historians look back at the first quarter of the twenty-first century, China in Africa's lithium industry will likely rank among the most strategically consequential resource plays of the modern era. This was not a speculative gold rush driven by commodity price euphoria. It was a methodical, state-aligned campaign to secure upstream feedstock for the world's most important emerging industrial complex: the lithium-ion battery supply chain powering electric vehicles and grid-scale energy storage.

Understanding why Africa became the primary theatre for this campaign requires looking beyond individual company decisions toward the structural forces shaping global energy transition economics. The International Energy Agency has projected that approximately 55 new lithium mines must reach commercial production by 2035 to meet anticipated demand from battery manufacturing and EV rollout globally. That single figure defines the scale of the supply challenge and explains why Africa, with its largely untapped hard-rock lithium geology, has attracted such concentrated attention from investors operating with long time horizons and government-aligned strategic mandates.

When big ASX news breaks, our subscribers know first

Africa's Lithium Production Surge: What the Numbers Reveal

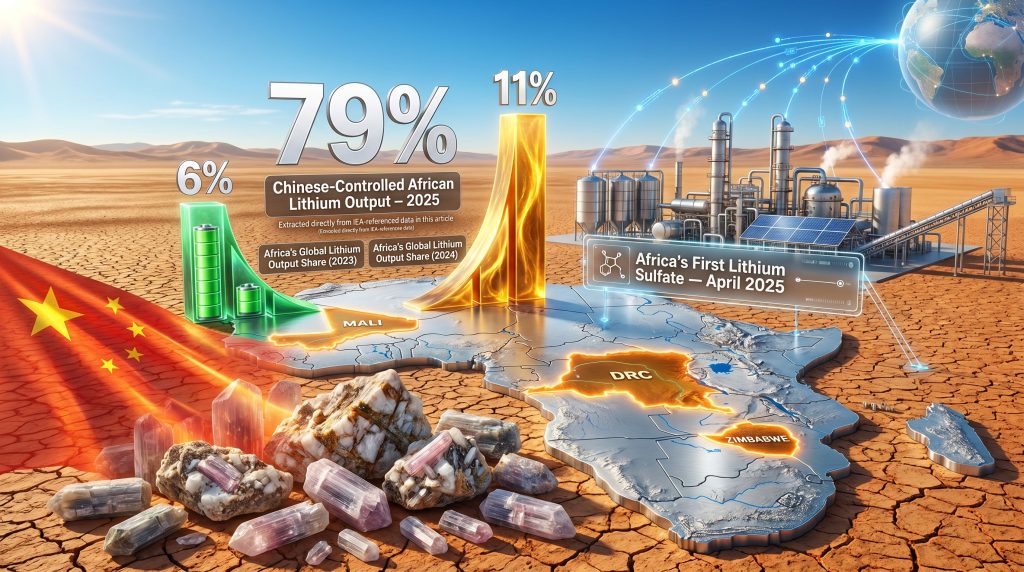

The pace at which Africa has grown its share of global lithium output is striking by any measure. According to IEA data, the continent's contribution to global lithium production more than doubled in a single year, rising from 6% in 2023 to 11% in 2024. This is not the gradual incremental growth typical of mature mining provinces. It reflects the simultaneous commissioning of multiple large-scale hard-rock operations that had been financed, constructed, and brought online within a compressed development timeline driven overwhelmingly by Chinese capital.

The trajectory is expected to steepen further as additional projects transition from development to commercial output. The anticipated start of production at Zijin Mining's Manono project in the Democratic Republic of Congo, described as one of the largest known lithium-tantalum deposits globally, is positioned to add substantial new volume to Africa's supply contribution. When combined with Zhejiang Huayou's pursuit of a controlling interest in Ghana's Ewoyaa project, the geographic spread of African lithium production is also expanding beyond its current southern and central African concentration.

| Metric | Figure |

|---|---|

| Africa's share of global lithium output (2023) | 6% |

| Africa's share of global lithium output (2024) | 11% |

| Estimated Chinese-controlled share of African output (2025) | ~79% |

| Projected Chinese-controlled share of African output (2035) | ~65% |

| China's share of global lithium refining capacity (2024) | 62% |

| New mines needed globally by 2035 (IEA estimate) | ~55 |

Why Hard-Rock Geology Matters

A less widely appreciated aspect of Africa's geological advantage is the specific character of its hard-rock lithium deposits. Spodumene lithium extraction from Africa's pegmatite formations produces a high-grade lithium aluminium silicate mineral that is technically well-matched to the feedstock requirements of Chinese battery-grade processing facilities. Unlike lithium brines, which require extensive evaporation infrastructure and produce variable lithium concentrations depending on seasonal and hydrological conditions, hard-rock spodumene mining delivers more consistent ore grades that translate into predictable concentrate quality.

This technical compatibility between African ore characteristics and Chinese processing infrastructure is a structural advantage that has reinforced Chinese investors' preference for African assets over brine-based alternatives in South America for certain applications.

Zimbabwe's Transformation: A Case Study in Chinese Industrial Strategy

No single country illustrates the depth and speed of Chinese engagement in Africa's lithium sector more comprehensively than Zimbabwe. Within the span of a few years in the early 2020s, a wave of Chinese capital transformed the country from a marginal lithium producer into Africa's largest, establishing a production base that now sits at the core of China's African lithium supply architecture.

The roster of Chinese operators active across Zimbabwe's lithium landscape reads as a who's who of China's battery materials industry:

- Zhejiang Huayou Cobalt operates the Arcadia hard-rock spodumene mine and has achieved Africa's first production of lithium sulfate, with the first exports of processed product recorded in April 2025

- Sinomine Resources controls Bikita Minerals, one of Africa's oldest and largest lithium operations, and is developing its own lithium sulfate processing facility within Zimbabwe

- Sichuan Yahua Industrial holds the Kamativi project and is similarly constructing dedicated lithium sulfate production capacity

- Chengxin Lithium operates the Sabi Star mine

- Tsingshan Holding Group is developing the Gwanda lithium project

The breadth of this ownership map means that virtually the entire productive lithium landscape in Zimbabwe sits within Chinese-controlled corporate structures. This concentration is without parallel in any other major mining jurisdiction globally, and it creates a supply dynamic in which African lithium output and Chinese industrial strategy are effectively synonymous.

The Progression Toward Battery-Grade Processing

A development that deserves particular analytical attention is the progression at the Arcadia mine toward battery-grade lithium carbonate production, as announced by Zimbabwe's Mines Minister Polite Kambamura. This advancement, coming only months after the country's inaugural lithium sulfate production milestone, signals that the value-chain integration being pursued by Chinese operators in Africa is advancing faster than many market observers had anticipated.

Lithium carbonate is a significantly higher-value product than raw spodumene concentrate, commanding premium pricing in global markets and requiring substantially more sophisticated processing technology. The fact that this capability is being established within Zimbabwe rather than exclusively at Chinese refineries represents a meaningful shift in where value is being created along the supply chain.

Beyond Extraction: The Downstream Processing Pivot

The most strategically significant evolution currently underway in China's African lithium position is the deliberate shift from raw ore extraction toward in-country processing and refining. This transition is not primarily a response to philanthropic impulses toward African development. It is a commercially rational and geopolitically adaptive strategy that serves multiple Chinese industrial objectives simultaneously.

China already controls approximately 62% of global lithium refining capacity as of 2024. By replicating processing infrastructure inside African producer countries, Chinese firms extend their value-chain dominance into new geographies while simultaneously complying with emerging export restriction regimes that could otherwise threaten their access to raw feedstock.

Furthermore, three distinct drivers are accelerating this downstream integration:

- Regulatory compliance: Zimbabwe has announced a ban on raw lithium concentrate exports effective 2027, requiring all producers to export higher-value processed products such as lithium sulfate or lithium carbonate. Chinese companies, with the capital and technical expertise to build processing plants quickly, are best positioned to comply with this policy shift ahead of the deadline.

- Supply chain resilience: Processing lithium ore within Africa before export reduces Chinese firms' exposure to disruptions along long-haul shipping routes for raw concentrate. Processed lithium compounds are more compact and stable for transport, reducing logistics costs and improving supply predictability.

- Competitive moat construction: Establishing processing infrastructure within host countries creates significant barriers to entry for rival investors. Once Chinese firms control both the mining operations and the refining facilities within a jurisdiction, alternative supply chain configurations become structurally difficult to construct.

The policy paradox embedded in Zimbabwe's beneficiation strategy deserves particular scrutiny. Export restrictions on raw concentrate were designed to force value-addition within the country, capturing more economic benefit for Zimbabwean citizens. However, because Chinese companies are the only entities with the capital, technical expertise, and integrated market relationships to build lithium processing plants at commercial scale within tight regulatory timelines, the global lithium market dynamic may effectively deepen Chinese downstream dominance rather than diversify it.

The Supply Security Imperative Driving Chinese Investment

China's industrial rationale for its African lithium campaign is straightforward when viewed through the lens of supply chain economics. China is simultaneously the world's largest lithium refiner, the dominant manufacturer of lithium-ion batteries, and the largest producer of electric vehicles. Each of these industries requires reliable, cost-competitive access to lithium feedstock. Disruptions to that feedstock access would cascade through the entire industrial system with serious economic consequences.

African hard-rock lithium deposits serve China's supply security strategy in ways that domestic resources and Australian imports cannot fully replicate. China's domestic lithium resources, while substantial, face grade and cost challenges relative to high-quality spodumene deposits in Africa and Australia. Australian supply, while technically well-matched to Chinese processing requirements, carries growing geopolitical risk as strategic competition between the two countries intensifies across multiple dimensions.

African assets, predominantly controlled by Chinese companies from the outset, provide a geographically diversified feedstock base that is far less exposed to the kind of supply disruption scenarios that a single-country dependency would create. Consequently, this logic also illuminates a speculative but increasingly credible risk scenario: What happens to Chinese battery supply chains if African production is disrupted?

Given that Chinese-controlled entities account for an estimated 79% of African lithium output in 2025, a significant production curtailment caused by policy instability, regulatory conflict, or operational failure across multiple Zimbabwean projects would create acute feedstock pressure on Chinese processors. The very concentration of ownership that gives China unparalleled supply security in normal operating conditions also creates a systemic vulnerability if that concentrated position is compromised.

Governance, Transparency, and the Development Dividend Question

The speed and scale of Chinese lithium investment across Africa has not been without controversy. Activists and investigative journalists operating in Zimbabwe and Namibia have raised documented concerns about the adequacy of environmental impact assessments at several Chinese-linked lithium projects. The rapid development timelines that Chinese companies have demonstrated as a competitive advantage may simultaneously represent a governance liability, with environmental and social impact assessments conducted under conditions that prioritise investment speed over comprehensive community engagement.

Community benefit-sharing mechanisms, including royalties, local employment quotas, and infrastructure contributions, have been criticised as insufficient relative to the scale of resource extraction occurring across Zimbabwe's lithium belt. Global Witness has documented how the transparency of licensing and concession award processes during the early 2020s investment wave has attracted scrutiny from governance reform advocates, who argue that without stronger institutional frameworks, host countries risk locking in unfavourable terms across multi-decade project lifecycles.

These concerns point to a structural tension at the heart of Africa's lithium development model: the same regulatory flexibility that enables rapid project development also creates conditions in which long-term value capture for host communities may be compromised. Resolving this tension will require institutional reforms that strengthen environmental oversight, enhance licensing transparency, and establish more robust community benefit frameworks, without sacrificing the investment climate conditions that have attracted capital at the pace required by global demand projections.

The next major ASX story will hit our subscribers first

Africa Versus Other Major Lithium Regions: A Structural Comparison

Understanding Africa's position in the global lithium supply architecture requires contextualising it against the other major producing regions and their distinct ownership, processing, and governance characteristics.

| Region | Primary Role | Dominant Corporate Actors | Processing Depth |

|---|---|---|---|

| Australia | Hard-rock spodumene mining | Albemarle, IGO, Tianqi (JV) | Limited domestic refining |

| Chile / Argentina | Brine lithium extraction | SQM, Albemarle, POSCO | Moderate domestic processing |

| China (domestic) | Mining and dominant refining | Ganfeng, Tianqi, CATL affiliates | Full value chain integration |

| Africa (Zimbabwe, Mali, DRC) | Hard-rock mining, emerging processing | Predominantly Chinese operators | Rapidly expanding |

Africa's trajectory most closely resembles Australia's early development phase, but with a critical structural distinction: Chinese ownership concentration in Africa is substantially higher from the outset than it ever was in Australia, where Western majors retain significant equity positions alongside Chinese joint venture interests. Unlike Australia's Greenbushes operation, in which Tianqi participates as a minority partner alongside Albemarle and IGO, African lithium projects are overwhelmingly majority or wholly Chinese-owned.

This ownership architecture has significant implications for how lithium produced in Africa enters global markets. Australian spodumene concentrate, even when shipped to Chinese refineries, passes through commercial arms-length transactions that preserve some degree of market pricing exposure. African lithium produced by Chinese-owned mines and processed at Chinese-owned facilities within Africa moves through what is effectively an intra-company supply chain. In addition, direct lithium extraction technologies are increasingly shaping how alternative supply chains are being evaluated globally, adding further complexity to market dynamics as African production scales.

Geopolitical Competition and the Emerging Battle for African Lithium

The recognition among Western governments and multilateral institutions that Chinese dominance in critical mineral supply chains represents a structural economic security risk has been slow to translate into meaningful competitive investment in African lithium assets. However, early signs of a more active Western engagement are beginning to emerge, creating what may become an intensifying geopolitical competition for Africa's lithium resources over the next decade.

Current Western and multilateral initiatives in African lithium remain modest relative to the entrenched Chinese position, but they signal directional intent:

- KoBold Metals (U.S.-based, technology-driven explorer) has invested in exploration licences in the area surrounding the Manono project in the DRC, representing one of the most concrete examples of Western capital entering the African lithium space at the asset level

- The European Investment Bank has committed financing support for the Uis lithium project in Namibia, introducing multilateral development finance as a tool for diversifying African lithium investment

- Zimbabwe's state-owned Kuvimba Mining is developing the Sandawana lithium project as a domestic participation vehicle, representing host-country efforts to build local industrial capacity alongside foreign investment

- The Minerals Security Partnership, involving the U.S. and allied nations, has identified African lithium assets as priority targets for alternative investment facilitation

The risk of a bifurcated global lithium supply chain is increasingly real. Moreover, critical minerals demand projections suggest that if current ownership trajectories persist, the global lithium market may evolve toward a Chinese-dominated African and domestic supply system on one side, and a smaller Western-aligned supply system centred on Australia and South American brine deposits on the other.

Such a bifurcation would have profound consequences for battery manufacturing costs, EV supply chain resilience, and energy transition timelines in markets outside China's industrial sphere. Non-Chinese battery manufacturers would face structurally higher feedstock costs and supply uncertainty, creating a competitive disadvantage that compounds over time as African production scales. Benchmark Mineral Intelligence has noted that China is set to dominate African lithium production across this decade, reinforcing concerns about the narrowing window for competitive alternatives.

This dynamic raises a question that Western policymakers have yet to answer convincingly: Can alternative investment frameworks be deployed at sufficient scale and speed to create meaningful competition for Chinese capital in African lithium, or has the window for early-mover positioning already closed in the continent's most important lithium jurisdictions?

Frequently Asked Questions: China in Africa's Lithium Industry

Which African country currently produces the most lithium?

Zimbabwe holds Africa's top position in lithium production, a status achieved through concentrated Chinese investment during the early 2020s that brought multiple major hard-rock lithium mines to commercial output within a short timeframe.

What percentage of African lithium output is controlled by Chinese companies?

Chinese-controlled entities are estimated to account for approximately 79% of African lithium output in 2025, with that figure projected to remain around 65% through 2035 as total African production expands significantly.

Why are Chinese companies building processing facilities inside Africa rather than exporting raw ore?

The shift is driven by a combination of factors: Zimbabwe's planned 2027 ban on raw lithium concentrate exports, the commercial logic of reducing logistics costs and shipping disruptions, and the strategic value of extending China's existing refining dominance into new geographies within a controlled value chain.

What is China's share of global lithium refining capacity?

According to IEA data, China accounts for approximately 62% of global lithium processing capacity as of 2024, giving it an unmatched position in the conversion of raw lithium ore into battery-grade materials.

Are Western companies investing in African lithium?

Western corporate presence at the mine-ownership level remains limited. KoBold Metals holds exploration licences near the Manono project in the DRC, and the European Investment Bank has committed financing toward the Uis project in Namibia, but these positions are substantially smaller in scale than China's entrenched production footprint across Zimbabwe, Mali, and the DRC.

What is beneficiation and why does it matter for African lithium producers?

Beneficiation refers to the processing of raw minerals into higher-value intermediate or refined products before export. African governments have increasingly mandated beneficiation as a policy tool to capture more economic value domestically rather than exporting raw ore. Zimbabwe's 2027 concentrate export ban is the most advanced example in the lithium sector, though the paradox is that Chinese companies are best positioned to comply with these mandates, potentially deepening their downstream control rather than diversifying ownership.

Key Takeaways: Reading the Strategic Architecture of China in Africa's Lithium Industry

The pattern of Chinese engagement across Africa's lithium sector is not a series of individual commercial decisions. It constitutes a coherent, multi-decade supply security strategy aligned with the long-term feedstock requirements of China's battery and EV industries. Several structural conclusions emerge from a careful examination of this strategy:

- Ownership concentration at approximately 79% of African lithium output in 2025 gives Chinese firms an influence over the continent's most important emerging critical mineral sector that has no historical parallel among foreign investor groups in African resource history

- The shift from extraction to in-country processing represents a deepening of Chinese dominance, not a dilution of it, as processing infrastructure creates long-term operational lock-in and extends value chain control into new geographic layers

- African governments face a genuine policy dilemma in which beneficiation mandates designed to capture greater domestic economic value may inadvertently entrench Chinese downstream control rather than create the ownership diversification they are intended to produce

- The geopolitical competition for African lithium is real and intensifying, but Western and multilateral alternatives remain early-stage relative to the scale, integration depth, and capital deployment speed of established Chinese investment across the continent

- The structural risk embedded in high Chinese ownership concentration, specifically the systemic vulnerability that emerges if that concentrated position is disrupted, is underappreciated in mainstream analysis and represents a material consideration for both African host governments and Chinese supply chain planners

This article draws on data published by the International Energy Agency and reporting by Ecofin Agency. All forward-looking figures and projections should be treated as estimates subject to change based on evolving market conditions, government policy decisions, and project development timelines. This article does not constitute investment advice.

Want to Track the Next Major Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — cutting through complex data across 30-plus commodities to surface actionable opportunities the moment they're announced. Explore Discovery Alert's dedicated discoveries page to understand how historic mineral discoveries have generated substantial returns, and begin your 14-day free trial today to position yourself ahead of the broader market.