May 12, 2026

When Trade Corridors Fracture: Aluminium Markets in the Age of Geopolitical Shock

Commodity markets have always been sensitive to geography, but the events unfolding across the Persian Gulf region in 2026 are delivering a masterclass in just how fragile global supply chains can become when a critical transit corridor comes under sustained pressure. The aluminium industry, long accustomed to managing price volatility and logistical complexity, is now navigating something qualitatively different: a structural rerouting of trade flows driven not by market forces, but by conflict.

Understanding what is happening requires looking beyond the headline export numbers. The real story involves the interaction between geopolitical disruption, smelter economics, arbitrage dynamics, and the limits of supply substitution across product categories. China aluminium exports amid Gulf turmoil have become one of the defining commodity narratives of 2026, and the implications extend well beyond the current moment.

When big ASX news breaks, our subscribers know first

The Persian Gulf as a Structural Chokepoint for Aluminium

The Strait of Hormuz has long been recognised as a critical bottleneck for energy commodities, but its role in the aluminium supply chain is less widely appreciated. Gulf Cooperation Council nations, particularly the UAE, Bahrain, and Saudi Arabia, have built significant primary aluminium production capacity over the past two decades, leveraging access to competitively priced energy and proximity to growing Asian and European demand centres.

GCC producers collectively account for roughly 9% of global primary aluminium output, a share that may appear modest in isolation but carries outsized significance when removed from available supply simultaneously. The approximately seven weeks of active conflict in the region as of late April 2026 has created cascading disruptions across the aluminium value chain:

- Alumina deliveries to Middle Eastern smelters have been interrupted, constraining raw material availability at a fundamental level

- Regional smelter utilisation rates have fallen as alumina feedstock becomes unreliable

- Cargo insurance premiums on Gulf-origin metal have risen sharply, raising the delivered cost even for shipments that do proceed

- Buyers in Asia, the Americas, and Southeast Asia have shifted procurement strategies away from long-term Gulf supply agreements toward opportunistic spot purchasing from alternative origins

The estimated global supply gap resulting from these disruptions has reached approximately 5 million tonnes, a figure that places enormous pressure on alternative producing nations to fill the void. That pressure has fallen most heavily on China. Furthermore, tariff-driven supply chain shifts are compounding these pressures, reshaping where buyers can realistically source replacement material.

It is worth noting that the Gulf disruption is not simply creating a temporary hole in supply. It is accelerating a structural repositioning of aluminium trade routes that could persist well into 2027 if the conflict remains unresolved. Buyers who have pivoted away from Gulf supply relationships are not guaranteed to pivot back, even after hostilities cease.

China's April 2026 Export Surge: Reading the Data Correctly

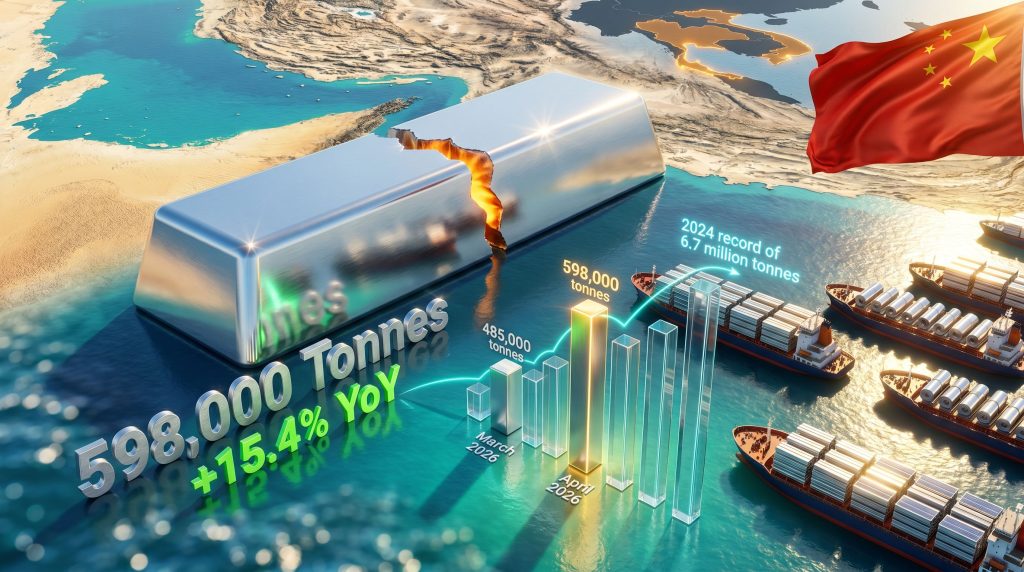

China's April 2026 export performance for unwrought aluminium and aluminium products came in at 598,000 metric tonnes, according to data published by SMM. That figure represents a 15.4% increase compared with the 518,000 tonnes shipped in April 2025 and stands as the strongest single-month export result since December 2024, when volumes reached 506,000 tonnes.

The cumulative picture is equally significant. Year-to-date exports for January through April 2026 have already reached 2.05 million tonnes, positioning China on a trajectory that could match or surpass the 2024 full-year record of approximately 6.7 million tonnes.

| Period | Export Volume | Key Context |

|---|---|---|

| April 2026 | 598,000 tonnes | Strongest month since Dec 2024 |

| April 2025 (comparison) | 518,000 tonnes | YoY base period |

| December 2024 (prior peak) | 506,000 tonnes | Previous monthly high |

| Q1 2026 | 1.46 million tonnes | +6.5% YoY |

| Jan–Apr 2026 YTD | 2.05 million tonnes | On pace for record year |

| 2024 Full-Year Record | 6.7 million tonnes | Benchmark for 2026 trajectory |

Several intersecting forces are driving this acceleration simultaneously. Alumina cargoes originally destined for Gulf smelters have been rerouted to Chinese ports, pushing Chinese alumina imports to a two-year high and providing smelters with cost-competitive feedstock that supports near-peak production rates. At the same time, domestic inventory overhang within China is suppressing ex-works prices, which widens the export arbitrage window by making it more financially attractive to ship metal internationally than to sell into a saturated home market.

The spread between international LME-linked aluminium prices and Chinese domestic prices has reached its widest point since 2022, creating a powerful financial incentive for Chinese producers and traders to direct metal toward export channels. This kind of arbitrage dynamic tends to be self-reinforcing in the short term: higher export volumes reduce domestic surplus, which gradually supports domestic prices, while international premiums eventually compress as more Chinese supply enters the market. In addition, commodity market volatility is amplifying these pricing dynamics across multiple metals simultaneously.

The Semi-Finished Shift: A Structural Export Evolution

A detail that deserves closer attention is the composition of China's outbound aluminium shipments. The export mix in 2026 is not dominated by primary ingot. Chinese producers are increasingly shipping value-added semi-finished products, including:

- Aluminium extrusions used in construction and industrial applications

- Automotive-grade sheet for vehicle body and structural components

- Packaging aluminium for food, beverage, and pharmaceutical sectors

- Solar panel frames and mounting systems tied to clean energy infrastructure

- Electric vehicle battery housing components and thermal management structures

- Wind turbine structural components and nacelle elements

This shift toward higher-value exports reflects both the maturation of Chinese downstream processing capacity and the specific demands of overseas buyers who need finished-specification material rather than raw ingot. It also has an important implication for supply substitution: buyers seeking primary ingot of specific purity grades may find Chinese export offerings only partially aligned with their requirements.

Can China Actually Replace GCC Aluminium Supply?

This is the central question facing procurement teams, traders, and policymakers watching the situation develop. The honest answer involves recognising both the genuine capabilities China brings to the table and the structural barriers that prevent full substitution.

Where Chinese Supply Has a Clear Advantage

China's position as the world's dominant aluminium producer is not simply a matter of scale. It reflects decades of investment in smelting capacity, downstream processing, logistics infrastructure, and established commercial relationships across Asian and emerging markets. Key advantages include:

- Production scale: Chinese smelter capacity operating near cyclical highs in 2026, supported by rerouted alumina supply

- Export infrastructure: Mature port capacity, established freight relationships, and flexible logistics networks capable of rapid volume scaling

- Product breadth: A wide range of semi-finished specifications available for rapid deployment into overseas supply chains

- Price competitiveness: Despite rising freight costs, the domestic price discount relative to international markets sustains export economics in many trade lanes

Where Substitution Faces Real Limits

Volume capacity is necessary but not sufficient for supply substitution. Product specification, purity grade, delivery terms, contractual structures, and geopolitical trade relationships all determine whether Chinese metal can functionally replace Gulf supply for any specific buyer in any specific application.

Several barriers constrain the substitution thesis:

- Product grade misalignment: GCC producers, particularly in the UAE and Bahrain, are internationally recognised for high-purity primary aluminium production. Chinese export volumes skew heavily toward alloyed and semi-finished material, which does not satisfy buyers requiring standard primary grade ingot for remelting or casting.

- Freight cost escalation: The same Gulf conflict driving demand for China aluminium exports amid Gulf turmoil is also disrupting global shipping lanes and pushing freight rates higher. On a delivered-cost basis, China's price advantage narrows significantly for buyers in distant markets.

- Trade policy constraints: US tariff impacts and aluminium tariffs substantially limit substitution options for North American buyers. This is not a hypothetical barrier; it is an active structural feature of the market that redirects Chinese export flows away from the United States regardless of the supply gap.

- Stockpiling distortion: Markets like Thailand are exhibiting aggressive inventory accumulation behaviour, including documented air freight purchases of alloy products to manage near-term supply risk. While this behaviour absorbs Chinese export volumes in the short term, it creates a potential demand cliff once the Gulf conflict stabilises and buyers find themselves sitting on excess inventory.

Market-by-Market Substitution Assessment

| Importing Region | Primary Demand Driver | Chinese Supply Feasibility |

|---|---|---|

| Thailand | Urgent semi-finished alloy demand | High |

| Vietnam | Manufacturing and downstream processing | High |

| South Korea | Automotive and electronics supply chains | Moderate to High |

| India | Infrastructure and packaging demand | Moderate |

| Mexico | Re-export and manufacturing hub activity | Moderate |

| United States | Limited by trade measures on Chinese aluminium | Low to Moderate |

The Arbitrage Mechanics Behind China's Export Acceleration

For readers less familiar with how commodity arbitrage functions in metals markets, it is worth explaining the mechanics driving China's export surge at a structural level. When domestic prices in a producing country fall below international prices by an amount exceeding the cost of shipping, insurance, and any applicable tariffs, producers and traders face a straightforward financial incentive to export rather than sell locally.

In China's case, several factors have compressed domestic aluminium prices relative to international benchmarks:

- Elevated domestic production supported by rerouted alumina supply has increased the volume of metal competing for domestic buyers

- China's industrial demand has not accelerated fast enough to absorb the production surge across key sectors

- Inventory at Chinese exchange warehouses and producer facilities has built up, applying downward price pressure at the point of sale

- International spot markets, tightened by Gulf supply disruption, have pushed LME-linked regional premiums to multi-year highs

The result is an arbitrage window that is, by some measures, the widest seen since 2022. This differential does not need to be enormous to drive significant export acceleration; even a modest per-tonne advantage, multiplied across hundreds of thousands of tonnes of monthly volume, creates compelling economics for large-scale export activity.

Arbitrage windows in commodity markets are inherently self-correcting over time. As Chinese exports increase global supply availability, international premiums compress. As domestic inventory depletes, Chinese ex-works prices recover. The key question for 2026 is whether the Gulf disruption will persist long enough to sustain the arbitrage window through the second half of the year.

2026 Export Trajectory: Scenario Analysis

Mapping the potential full-year outcome for China aluminium exports amid Gulf turmoil requires examining three distinct scenarios, each driven primarily by the duration and resolution of the Persian Gulf conflict.

Base Case Scenario

The Gulf conflict remains active through mid-2026 but shows signs of de-escalation by Q3. Chinese exports sustain elevated monthly volumes through June, then moderate as the arbitrage window begins to narrow. Full-year 2026 exports match the 2024 record of approximately 6.7 million tonnes.

Upside Scenario

Sustained conflict through Q3 2026 combined with continued aggressive stockpiling by Southeast Asian and clean energy sector buyers pushes monthly volumes above 600,000 tonnes in May and June. Full-year exports materially exceed the 2024 record, potentially approaching 7.2 to 7.5 million tonnes.

Downside Scenario

Rapid conflict resolution in the Gulf enables GCC smelters to resume full production within weeks. Alumina supply normalises, regional premiums compress quickly, and the export arbitrage window narrows sharply. Buyers who have over-stockpiled face inventory management challenges, creating a demand cliff for Chinese exporters. Full-year volumes fall short of the 2024 record.

The May to June 2026 window is widely regarded as a potential peak period for semi-finished export volumes, driven by buyers seeking to build buffer inventory before any supply-side normalisation.

Key Variables Shaping the Outcome

- Duration and territorial scope of active Persian Gulf hostilities

- Speed of GCC smelter production recovery once alumina supply resumes

- Chinese domestic demand trajectory across infrastructure, automotive, and property-linked segments

- LME aluminium price direction and its evolving relationship with Shanghai Futures Exchange pricing

- Freight rate movements on China to Southeast Asia and China to Middle East trade lanes

- Trade policy developments in major importing markets, particularly the United States and European Union

The next major ASX story will hit our subscribers first

Strategic Implications for Procurement and Supply Chain Planning

For businesses whose operations depend on aluminium inputs, the 2026 disruption offers several lessons that extend beyond the immediate crisis.

Diversification as Non-Negotiable Risk Management

Procurement teams that had concentrated sourcing relationships with Gulf producers are bearing the greatest cost of the current disruption. The baseline standard of maintaining supply relationships across at least two non-correlated geographic origins has never looked more prudent.

Specification Alignment Before Substitution

Before committing to Chinese semi-finished or alloyed material as a substitute for Gulf primary ingot, downstream manufacturers need to verify that the available product specifications actually match their processing requirements. Accepting material that does not meet application standards creates quality risk that can be more costly than the original supply disruption.

Stockpiling Discipline

The aggressive inventory accumulation being observed in markets like Thailand is understandable as a short-term risk management response, but it carries medium-term risk. Buyers who over-stockpile at current elevated prices may face significant mark-to-market losses if the Gulf conflict resolves quickly and international premiums compress. Consequently, scenario planning should explicitly account for a rapid supply resumption outcome.

Trade Policy Monitoring

The regulatory environment governing aluminium trade is dynamic. US and EU trade measures affecting Chinese aluminium can change with relatively short notice, and buyers operating in or sourcing for these markets need to maintain active monitoring of applicable tariff and non-tariff barriers.

The Broader Geopolitical Lesson for Critical Metals Markets

Aluminium's vulnerability to Persian Gulf disruption is not an isolated phenomenon. The 2026 episode adds a critical industrial metal to a list that already includes oil, liquefied natural gas, and shipping capacity as commodities whose global supply architectures are acutely sensitive to Strait of Hormuz stability.

For clean energy supply chains, the exposure is compounded. Solar panel frames, EV battery structures, and wind turbine components all rely heavily on aluminium. A sustained disruption to Gulf aluminium supply creates cost and availability pressure simultaneously across multiple clean energy manufacturing sectors, at precisely the moment when production scale-up is most critical.

The strategic case for supply chain regionalisation and allied-nation sourcing frameworks has been reinforced by the 2026 disruption in ways that will likely shape industrial policy discussions for years to come. Whether this translates into concrete investment in non-Gulf, non-Chinese primary aluminium capacity in Australia, Canada, Norway, or other producing nations remains to be seen. What is clear is that the appetite for such diversification has increased substantially among buyers who have lived through the current disruption.

Frequently Asked Questions

Why did China's aluminium exports rise 15% in April 2026?

China's April 2026 aluminium exports reached 598,000 tonnes, a 15.4% year-over-year increase driven by Gulf conflict-related supply disruptions, a widening price premium between international and Chinese domestic markets, rerouted alumina imports supporting elevated smelting output, and accelerated stockpiling behaviour among overseas buyers.

Which countries are buying the most Chinese aluminium in 2026?

Thailand, Vietnam, South Korea, India, and Mexico are among the most active importers of Chinese aluminium in 2026. Thailand has been particularly notable for urgent semi-finished alloy purchases, including air freight shipments to manage near-term supply risk.

Can China fully replace GCC aluminium supply?

Not on a like-for-like basis. While China has the volume capacity to partially offset GCC supply losses, differences in product grade, rising freight costs, and trade policy barriers particularly in the United States limit full substitutability across key markets.

What is the 2026 outlook for Chinese aluminium export volumes?

Full-year 2026 exports are on track to match or potentially exceed the 2024 record of approximately 6.7 million tonnes, with May and June 2026 expected to represent a peak window for semi-finished product shipments if current conditions persist.

How long could this export surge last?

The duration is directly tied to the Persian Gulf conflict timeline. A rapid resolution could narrow China's export arbitrage window quickly, while a prolonged conflict could sustain elevated export volumes through the second half of 2026 and potentially into 2027.

This article contains forward-looking statements, scenario projections, and market analysis based on information available as of May 2026. Commodity markets are subject to rapid change driven by geopolitical, regulatory, and macroeconomic factors. Nothing in this article constitutes financial, investment, or procurement advice. Readers should conduct independent due diligence before making any commercial or investment decisions.

Want to Stay Ahead of the Next Major Commodity Market Shift?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across aluminium, copper, and more than 30 other commodities — cutting through market complexity to deliver actionable insights before the broader market reacts. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the next major market move.