May 12, 2026

What Drives China's Historic Coal Import Contraction?

Global energy markets are witnessing a fundamental shift as traditional demand patterns undergo structural transformation. The world's largest energy consumer has dramatically reduced its reliance on overseas coal supplies, marking the most significant annual contraction in thermal commodity imports since the early 2010s. This shift represents more than cyclical market dynamics, signalling deeper changes in energy infrastructure and strategic resource planning across major economies as energy transition challenges reshape global markets.

Domestic Production Surge vs. Import Dependency

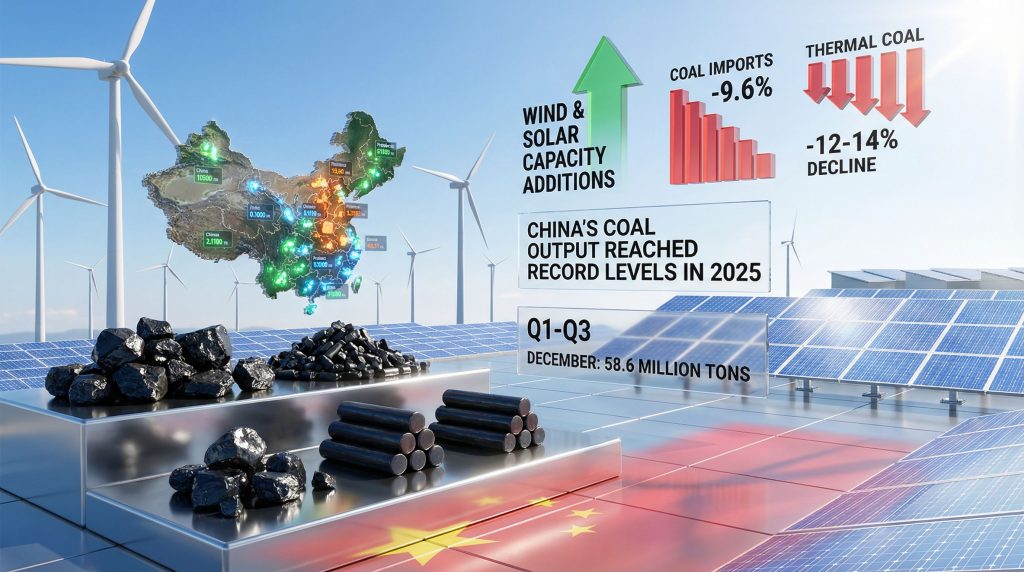

China's coal imports annual drop reached unprecedented levels in 2025, with the nation importing 490 million tons compared to 539 million tons in 2024, representing a 9.6% decline. This marks the largest annual decrease in over a decade and the first contraction since 2022's pandemic-affected period. Unlike previous declines driven by external shocks, this reduction stems from fundamental supply-demand rebalancing.

Domestic coal output reached elevated production levels throughout 2025, creating a substantial price differential favouring local suppliers. Chinese thermal coal prices hit four-year lows, fundamentally altering the economic calculus that previously made imports attractive. The cost competitiveness analysis reveals several key factors:

- Transportation cost elimination for domestic supplies versus seaborne imports

- Currency stability with yuan-denominated domestic purchases versus USD-priced international contracts

- Reduced port handling fees and logistics complexity

- Strategic self-sufficiency objectives prioritising energy security over pure cost optimisation

This domestic price advantage represents a structural shift rather than temporary market conditions, as sustained high production capacity continues supporting local supply adequacy.

Renewable Energy Displacement Effects

The most significant driver behind reduced coal demand stems from unprecedented renewable capacity additions. Wind and solar installations created the first thermal power generation decline since 2015, with coal-fired electricity generation dropping 1.6% annually. November 2025 data showed an even steeper 4.2% decline, indicating accelerating displacement rates.

Key renewable substitution metrics:

- Grid integration capacity expanded sufficiently to handle intermittent renewable sources

- Load factor improvements in renewable installations reduced backup thermal generation requirements

- Energy storage deployment supported grid stability during renewable output fluctuations

- Industrial demand shifting toward cleaner electricity sources where available

This substitution effect operates differently across China's regional power grids, with coastal provinces showing higher renewable displacement rates compared to interior regions still dependent on coal-fired baseload generation. Furthermore, this transition reflects broader energy security in transition dynamics affecting global resource allocation.

When big ASX news breaks, our subscribers know first

How Do Supply Chain Disruptions Reshape Coal Trade Patterns?

International coal trade flows have undergone dramatic reconfiguration as traditional supplier relationships face both geopolitical pressures and economic restructuring. The concentration of supply sources has intensified, creating new vulnerability patterns while established trade routes experience significant volume reductions.

Geographic Supplier Concentration Analysis

Mongolia and Russia captured approximately 78% market share in Chinese coal imports during 2025, representing a substantial concentration risk compared to historically diversified supply sources. This concentration stems from several converging factors:

- Complete cessation of U.S. coal shipments due to tariff implementation and trade policy changes

- Indonesian production cut announcements affecting China's historically largest foreign supplier

- Overland transport advantages from Mongolia and Russia versus seaborne logistics

- Currency and payment mechanisms facilitating bilateral trade relationships

Indonesia's status as China's top foreign supplier faces pressure from government decisions to reduce coal output in 2026. These production cuts signal sovereign resource policy prioritisation over export revenues, creating supply constraints that China must address through alternative sources or domestic production increases.

The geographic concentration creates logistical bottlenecks through limited transport infrastructure:

| Transport Route | Capacity Constraints | Seasonal Factors | Cost Structure |

|---|---|---|---|

| Trans-Mongolian Railway | Limited throughput capacity | Winter weather delays | Lower than seaborne |

| Russian overland routes | Infrastructure maintenance needs | Permafrost affecting rail lines | Currency exchange benefits |

| Seaborne alternatives | Port congestion issues | Monsoon season disruptions | Higher total delivered cost |

Coking vs. Thermal Coal Market Divergence

Metallurgical coal imports demonstrated resilience with Q1 2025 growth of 2%, contrasting sharply with thermal coal's 12-14% decline through September. This divergence reflects fundamental differences in substitutability and industrial demand patterns.

Coking coal characteristics driving import persistence:

- Quality specifications requiring specific carbon content, ash composition, and volatile matter percentages for steel production

- Domestic blending requirements where Chinese coking coal needs international supplies to meet metallurgical standards

- Steel industry resilience maintaining operational requirements despite broader economic headwinds

- Limited substitute availability from domestic sources at required quality levels

Thermal coal vulnerability factors:

- Direct renewable competition from wind and solar capacity expansions

- Interchangeable supply sources between domestic and imported materials

- Power generation efficiency improvements reducing overall coal consumption per unit of electricity

- Industrial heating alternatives including natural gas and renewable electricity

Russia's coking coal exports to China increased 4.29% despite international sanctions, highlighting the specialised nature of metallurgical coal trade and the difficulty of rapidly substituting strategic industrial inputs. In addition, these patterns mirror the energy exports challenges faced by traditional resource exporters globally.

What Economic Indicators Signal Long-Term Energy Policy Shifts?

Price volatility patterns throughout 2025 revealed the complex interaction between seasonal demand, strategic inventory management, and structural energy transition policies. These economic indicators provide insight into whether current trends represent permanent demand destruction or temporary market adjustments.

Price Volatility and Market Response Mechanisms

Table: China Coal Import Price Dynamics 2025

| Period | Domestic Price Trend | Import Competitiveness | Volume Response |

|---|---|---|---|

| Q1-Q3 | Weak/Declining | Low attractiveness | -11.1% imports |

| Q4 | Rising/Strengthening | Increased buying interest | +12% December |

| Annual | Mixed signals | Structural decline | -9.6% total |

The December surge to 58.6 million tons represents the highest monthly import volume of 2025, driven by winter heating demand and potential inventory management strategies. This 43% increase above the annual monthly average of approximately 41 million tons demonstrates continued price sensitivity and seasonal responsiveness despite structural decline trends.

Market mechanism analysis reveals:

- Price arbitrage opportunities still influence short-term import decisions

- Inventory cycle management by power plants and industrial consumers

- Forward purchasing behaviour anticipating potential 2026 supply constraints

- Regional demand variations with northern China showing stronger winter import demand

Strategic Stockpiling vs. Consumption Patterns

The relationship between imports and actual consumption diverged significantly in 2025, with strategic inventory considerations playing an increasingly important role in purchase timing decisions. Government energy security policies enabled this transition by providing adequate strategic reserves to buffer supply variability.

Strategic inventory management factors:

- Seasonal heating requirements necessitating Q4 stockpiling for winter demand

- Supply chain risk mitigation given concentrated supplier base

- Price volatility hedging through opportunistic purchasing during favourable market conditions

- Grid stability reserves supporting renewable energy integration requirements

This inventory-driven demand pattern suggests that monthly import volatility will increase even as annual totals decline, with procurement decisions increasingly driven by strategic rather than immediate operational requirements. Consequently, these developments align with broader tariff-driven market impacts affecting global trade patterns.

How Does China's Coal Decline Impact Global Energy Markets?

The ripple effects of reduced Chinese coal demand extend far beyond bilateral trade relationships, fundamentally altering global supply-demand balances and forcing structural adjustments throughout the international energy commodity complex.

Seaborne Trade Contraction Effects

Global thermal coal trade declined 5% to approximately 945 million tons in 2025, with the Asia-Pacific region leading the contraction at a 7% reduction. China's 490 million tons of imports represent approximately 52% of global seaborne coal trade, making the country's demand shifts the primary driver of international market conditions.

Regional trade rebalancing patterns:

- India's opportunistic purchasing capturing some supplies previously destined for China at more favourable pricing

- Southeast Asian importers (Vietnam, Philippines, Thailand) showing modest demand increases

- Japan and South Korea maintaining stable import volumes despite regional supply shifts

- European coal demand remaining structurally constrained by climate policies and gas substitution

The mathematical relationship between China's import reduction and global oversupply creates deflationary pressure throughout 2026, as approximately 49 million tons of annual supply must find alternative markets or face production curtailment.

Geopolitical Implications of Import Source Concentration

China's increasing reliance on Mongolia and Russia for 78% of coal imports creates new geopolitical dynamics while reducing traditional supplier relationships. This concentration shift carries both strategic benefits and vulnerability risks.

Advantages of concentrated sourcing:

- Enhanced bilateral relationship leverage in broader diplomatic negotiations

- Currency diversification reducing USD exposure in energy transactions

- Transport infrastructure development supporting overland trade routes

- Supply chain reliability through established government-to-government frameworks

Concentration risk factors:

- Single-point-of-failure vulnerability if Mongolia-Russia transport infrastructure faces disruption

- Limited pricing competition with fewer alternative suppliers maintaining market positions

- Sanctions exposure affecting Russian energy trade financing and logistics

- Weather-dependent transport during severe winter conditions affecting overland routes

Canadian and Australian suppliers maintained market positions despite overall volume declines, focusing on premium coking coal grades where quality specifications limit substitution options.

What Investment Opportunities Emerge from China's Energy Transition?

The structural shift away from coal imports creates both challenges and opportunities across multiple sectors, with investment implications extending from infrastructure development to resource company valuations and technology deployment priorities.

Infrastructure Development Priorities

Renewable energy grid integration requires massive capital deployment to support the coal displacement driving import reductions. Key infrastructure investment areas include:

- Ultra-high voltage transmission lines connecting remote renewable generation capacity with industrial demand centres

- Grid-scale energy storage systems managing intermittency from wind and solar installations

- Smart grid technologies optimising renewable energy dispatch and reducing backup generation requirements

- Industrial electrification infrastructure supporting direct renewable energy consumption in manufacturing

Coal power plant retirement schedules create substantial replacement demand for generation capacity. Approximately 40-60 GW of aging coal capacity faces retirement decisions over the next five years, requiring alternative generation sources or demand reduction measures.

Energy storage deployment represents the fastest-growing infrastructure category, with battery storage installations growing 150-200% annually to support renewable integration requirements. However, this transition parallels the mining industry evolution occurring across global resource sectors.

Resource Sector Implications for Major Miners

Diversified mining companies demonstrate varying exposure levels to China's coal imports annual drop:

BHP Group:

- Iron ore operations benefit from continued Chinese steel production despite coal weakness

- Copper assets positioned for renewable energy infrastructure demand growth

- Coking coal exposure remains strategically valuable given metallurgical coal import resilience

- Thermal coal divestiture strategy reduces structural headwinds from Chinese demand shifts

Rio Tinto:

- Battery minerals portfolio (lithium, copper) supports energy transition infrastructure

- Iron ore dominance maintains Chinese industrial demand exposure

- Aluminium operations benefit from renewable energy adoption in power-intensive industries

- Limited thermal coal exposure provides insulation from import decline trends

Coal-focused mining operations face structural demand headwinds requiring strategic repositioning toward alternative markets or asset optimisation strategies.

Strategic Implications for Energy Security and Trade Policy

The transformation of China's coal import patterns reflects broader strategic considerations balancing energy independence objectives with economic efficiency requirements and climate policy commitments.

Energy Independence vs. Economic Efficiency Trade-offs

China's preference for higher-cost domestic coal over cheaper imports demonstrates strategic value calculations extending beyond pure economic optimisation. Key trade-off considerations include:

Energy security premiums:

- Supply chain disruption insurance through domestic production capacity maintenance

- Currency stability benefits avoiding USD exposure in energy procurement

- Employment considerations supporting domestic mining regions and related industries

- Strategic reserve management maintaining adequate emergency supply capabilities

Economic efficiency costs:

- Higher electricity generation costs from domestic coal versus imported alternatives

- Regional price disparities between coastal import-dependent areas and interior production regions

- Infrastructure investment requirements supporting domestic production and transport capacity

- Opportunity costs of capital deployed in coal versus renewable energy infrastructure

This balance suggests that energy security considerations increasingly outweigh pure cost optimisation in Chinese energy policy decision-making.

Future Demand Scenarios and Market Adaptation

Industrial sector coal consumption patterns continue evolving as manufacturing processes adapt to changing energy costs and availability. Key adaptation mechanisms include:

- Process electrification in cement, chemicals, and steel production where technically feasible

- Efficiency improvements reducing coal consumption per unit of industrial output

- Fuel switching programmes toward natural gas or renewable electricity where economically viable

- Regional industrial migration toward areas with lower energy costs or cleaner electricity grids

Power generation fuel mix transformation accelerates through 2026-2028, with renewable capacity additions consistently exceeding thermal retirements. This trend supports continued structural decline in coal import demand despite seasonal and cyclical variations.

Export-oriented industries face adjustments to changing energy costs, potentially affecting:

- Manufacturing competitiveness in energy-intensive export sectors

- Carbon border adjustment exposure as international climate policies evolve

- Supply chain reconfiguration optimising for domestic renewable energy availability

Investment Disclaimer: The analysis presented reflects current market conditions and policy trends that may change significantly. Commodity markets involve substantial price volatility and political risks. Investment decisions should consider multiple scenarios and professional financial advice.

The next major ASX story will hit our subscribers first

Frequently Asked Questions About China's Coal Import Trends

Will China's Coal Imports Recover in 2026?

Seasonal patterns suggest potential Q1 2026 restocking activity following the strong December 2025 import surge, but long-term trajectory indicators point toward continued structural decline rather than cyclical recovery.

Recovery-supporting factors:

- Winter heating demand extending into Q1 requiring inventory replenishment

- Indonesian production cuts potentially creating temporary supply scarcity and import attractiveness

- Price volatility opportunities for strategic purchasing during favourable market conditions

Structural decline drivers:

- Renewable capacity additions continuing to displace thermal generation requirements

- Domestic production adequacy maintaining cost advantages over imported supplies

- Policy support consistency for energy transition and self-sufficiency objectives

Most likely scenario: Total 2026 imports ranging 450-480 million tons, representing further modest decline with increased monthly volatility around strategic procurement timing.

How Does This Affect Global Coal Prices?

Reduced Chinese demand creates persistent oversupply conditions in seaborne thermal coal markets, with regional price differentials emerging between different coal grades and transport-accessible regions.

Price impact mechanisms:

- Excess supply pressure from approximately 49 million tons of reduced Chinese import demand

- Supplier competition intensification for remaining import markets (India, Southeast Asia, Europe)

- Quality premium expansion as buyers become more selective with reduced overall volumes

- Transport cost arbitrage opportunities between seaborne and overland delivery routes

Regional price differentiation:

- Newcastle thermal coal facing broader downward pressure from Asian demand weakness

- Premium coking coal grades maintaining better pricing support from steel industry demand

- Lower-grade thermal coal experiencing steepest price pressures as substitute fuels gain competitiveness

Furthermore, China's falling coal demand illustrates how domestic renewable energy expansion directly reduces import requirements. Expected 2026 price trajectory: Continued weakness in thermal coal with 10-15% further declines possible, while premium coking coal shows greater price resilience due to specialised industrial demand.

Are You Looking to Capitalise on Energy Transition Opportunities?

Discovery Alert's proprietary Discovery IQ model provides real-time alerts on significant ASX mineral discoveries, including critical battery minerals and resources driving the energy transition away from traditional fuels like coal. Explore why historic mineral discoveries have generated exceptional returns for early investors and begin your 30-day free trial today to position yourself ahead of the market in this rapidly evolving sector.