June 22, 2026

The Hidden Mechanics Behind China's Coking Coal Price Collapse

Commodity markets rarely move in straight lines, and few illustrate this better than the coking coal complex in China during the first half of 2026. Within the span of a single month, prices swung from a fear-driven spike to a sustained decline, not because underlying demand evaporated, but because the psychological weight of a supply disruption gave way to the hard data of a faster-than-expected recovery. Understanding why China coking coal prices extend loss on prospects of rising supply requires looking beyond the headline numbers and into the structural forces reshaping how traders, steelmakers, and analysts are interpreting this market in real time.

When big ASX news breaks, our subscribers know first

A Market Built on Sentiment as Much as Fundamentals

Coking coal, also known as metallurgical coal, is fundamentally different from thermal coal used in power generation. Its value is tied directly to the steel industry: specifically, to the blast furnace steelmaking process where it is converted into coke, a carbon-rich fuel and reducing agent that drives iron ore smelting. The quality of coking coal matters enormously in this context.

Higher-rank coals with low sulphur content, low ash levels, and strong caking properties command significant premiums because they produce denser, more reactive coke that performs better in large blast furnaces. For a broader view of how these dynamics intersect, the global steel production outlook provides useful context on where demand is heading.

This technical dependency on quality means the coking coal market is structurally tighter and more volatile than thermal coal markets. Supply disruptions, even temporary ones, carry an outsized psychological premium because steelmakers cannot easily substitute alternative inputs without compromising furnace efficiency or coke quality ratios.

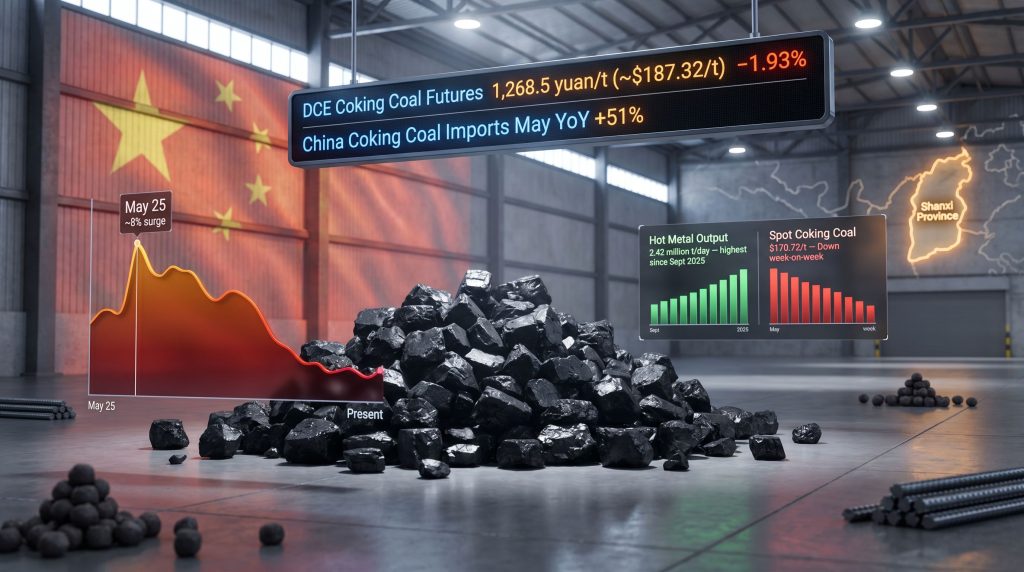

This sensitivity to supply shocks helps explain why a single mining accident in Shanxi Province in late May 2026 was sufficient to trigger a near-8% futures spike on the Dalian Commodity Exchange within days of the incident.

Key Market Data: Where Prices Stand Right Now

The following table summarises the key benchmark figures that define the current state of China's coking coal and related commodity markets as of late June 2026.

| Benchmark | Price | Movement |

|---|---|---|

| DCE Coking Coal Futures (most-traded) | 1,268.5 yuan/t (~$187.32/t) | -1.93% |

| DCE Coke Futures (most active) | 2,010.5 yuan/t | -0.74% |

| China Spot Coking Coal (mid-May) | ~$175/t | Declining trend |

| Kallanish Spot Price (May 16-23) | $170.72/t | Down week-on-week |

| DCE Iron Ore (most-traded) | 745 yuan/t | -0.13% |

| Singapore Exchange July Iron Ore | $98.95/t | +0.31% |

| Hot Metal Output (as of June 18) | 2.42 million t/day | +0.6% week-on-week |

| Shanxi Mine Resumption Rate | ~63% of suspended mines | Recovering |

The divergence between coking coal's sharp decline and iron ore's relative stability is itself a market signal worth examining closely. Furthermore, the latest metallurgical coal price update offers additional granularity on how these benchmarks have evolved over recent months.

The Shanxi Accident: How a Single Event Reshapes an Entire Market

Shanxi Province sits at the heart of China's domestic coal supply chain. It is the country's single largest coal-producing region, accounting for a substantial share of both thermal and metallurgical coal output. When a fatal mining accident struck the province in late May 2026, regulatory authorities responded with mandatory safety inspections and temporary production suspensions across multiple operations.

This is standard protocol in China's mining sector: any fatality triggers a broad inspection regime that can affect not just the site of the incident but neighbouring and affiliated mines as well. Consequently, the immediate market response was reflexive and rapid.

Coking coal futures on the DCE surged nearly 8% on May 25, a textbook fear-based reaction driven by traders pricing in an anticipated shortfall before the full scope of the disruption was known. This is a well-documented phenomenon in commodity markets: the uncertainty premium during a supply shock typically exceeds the eventual actual impact, particularly when real-time production data is not immediately available.

By mid-June, the picture had clarified significantly. Mysteel survey data, one of the most closely followed consultancy sources for Chinese steel and coal market participants, confirmed that approximately 63% of mines suspended after the accident had resumed production by June 17. This rate of recovery was faster than many market participants had anticipated, and it triggered the sentiment reversal that is now driving prices lower.

Galaxy Futures analysts captured this dynamic precisely in a market commentary, characterising the price slump as a reflection of traders rotating their attention away from supply shortage concerns and toward the reality of production resumption. Importantly, those same analysts also flagged that the situation is not entirely resolved, noting persistent uncertainty over the pace of restart at remaining suspended operations and expressing scepticism that output would return to pre-accident levels in the near term. Mining.com's analysis of coking coal losses further corroborates this cautious near-term sentiment.

China's Coking Coal Import Surge: A Secondary Pressure Source

Domestic mine restarts alone do not fully explain the scale of the price decline. An equally significant factor is the extraordinary rise in China's coking coal import volumes in 2026. However, understanding these flows requires examining both volume and origin simultaneously.

- China's coking coal imports in May 2026 surged 51% year-on-year, according to official customs data

- Year-to-date imports through May were running 25% above the equivalent period in 2025

- Traders broadly expect import volumes to continue rising through the remainder of the year

- The simultaneous acceleration of domestic supply recovery and elevated imports is compressing what had been an anticipated supply deficit

China sources its imported coking coal from a geographically diverse supplier base, each with distinct quality profiles and logistical characteristics:

| Supplier Region | Key Characteristics |

|---|---|

| Australia | Premium hard coking coal; historically dominant supplier; trade flows partially recovering |

| Mongolia | Overland supply via border crossings; growing volume significance; lower transport costs |

| Russia | Expanding market share; mid-tier coking coal quality; competitive pricing |

| Canada and USA | Smaller volumes; high-quality hard coking coal; longer shipping distances |

In addition, the quality dimension of these import flows matters for downstream users. Premium hard coking coal from Australia or North America allows steelmakers to reduce coke rates in their blast furnaces, improving both cost efficiency and environmental performance. By contrast, lower-rank imported coals from closer sources may require blending to achieve acceptable coke strength parameters, a practice known as coal blending optimisation that Chinese steel mills have developed considerable expertise in over the past decade. SP Global's commentary on Mongolian coking coal demand highlights this blending trend as particularly relevant heading into the second half of 2026.

Hot Metal Output: The Demand Signal That Complicates the Bearish Case

One of the most analytically interesting aspects of the current coking coal market is the tension between falling prices and resilient downstream demand. Average daily hot metal output, the most direct real-time indicator of iron ore and coking coal consumption at blast furnaces, rose 0.6% week-on-week to 2.42 million tonnes as of June 18, 2026. Mysteel data confirmed this as the highest daily hot metal production rate since September 2025.

This matters for several reasons. Hot metal output at multi-month highs signals that Chinese blast furnace steelmakers are not cutting production in response to market conditions. Steelmakers run their furnaces based on steel demand, profitability margins, and input availability, not futures prices. When hot metal output rises even as coking coal prices fall, it suggests the price decline is supply-push rather than demand-pull in nature.

A supply-push price decline, driven by recovering production and elevated imports, is structurally different from a demand-led collapse. It implies that once the supply overhang normalises, the price floor provided by genuine end-use demand should prevent a disorderly breakdown.

Furthermore, the China steel and iron ore market analysis demonstrates how these upstream dynamics feed through into finished steel pricing across different product categories.

The next major ASX story will hit our subscribers first

Steel Market Signals: Reading the Mixed Benchmarks

Steel product prices on the Shanghai Futures Exchange presented a mixed picture that deserves careful interpretation. Understanding which products are rising and which are falling reveals important information about where demand is strongest.

| Steel Product | Price Movement |

|---|---|

| Rebar | -0.32% |

| Hot-Rolled Coil (HRC) | -0.42% |

| Stainless Steel | -0.13% |

| Wire Rod | +0.51% |

The divergence between wire rod (positive) and flat steel products like HRC (negative) reflects the uneven distribution of demand across end-use sectors. Wire rod is primarily consumed in construction reinforcement and light manufacturing, while HRC feeds into automotive, heavy equipment, and industrial applications. The relative strength of wire rod over flat products is consistent with selective infrastructure activity, even as China's broader property sector continues to face headwinds that suppress residential construction demand.

The Three-Phase Cycle of Post-Disruption Coking Coal Markets

Markets that experience sudden supply disruptions tend to follow a recognisable pattern of price behaviour that experienced commodity traders track closely. The current coking coal episode provides a clear illustration of this cycle in action.

-

Shock Phase: The initial disruption triggers rapid futures buying as traders price in worst-case supply scenarios. The ~8% DCE spike on May 25, 2026 is a textbook example. Fear-based buying can significantly overshoot the actual supply impact.

-

Correction Phase: As production resumption data emerges and import flows accelerate, the fear premium deflates. The market reprices based on a more realistic assessment of actual supply availability. This is the phase currently underway, with China coking coal prices extend loss on prospects of rising supply serving as the clearest expression of this dynamic.

-

Stabilisation Phase: Prices find a new equilibrium anchored by genuine supply-demand fundamentals. The level at which stabilisation occurs depends on the residual gap between pre-disruption output capacity and the achieved recovery rate, overlaid by import volumes and steel sector demand.

One underappreciated aspect of this cycle in the modern era is the speed at which Phase 1 transitions to Phase 2. Real-time mine resumption surveys conducted by firms like Mysteel, which can deliver granular data on operational status within days of a disruption, have materially compressed the duration of the fear premium phase compared to earlier decades when such data took weeks to compile.

Outlook: Key Variables That Will Determine Price Direction

The near-term trajectory of Chinese coking coal prices will be shaped by several competing forces that remain genuinely uncertain. However, the iron ore market pressures currently in play add an additional layer of complexity, as trade policy and logistics costs interact with raw material pricing across the ferrous complex.

- Remaining mine restarts: With approximately 37% of suspended Shanxi mines still offline as of June 17, the pace and completeness of further resumptions will be a critical near-term price driver. Galaxy Futures analysts specifically cautioned that returning to pre-accident output levels faces meaningful obstacles.

- Import volume trajectory: Whether the 51% year-on-year import surge in May proves sustainable or begins to moderate as domestic supply recovers will influence how quickly the current supply overhang dissipates.

- Steel demand seasonality: Chinese steel demand typically strengthens in the second half of the year as infrastructure project execution accelerates. A seasonal pickup in construction activity could provide incremental support for coking coal demand.

- Iron ore inventory dynamics: Elevated portside iron ore inventories in China are currently capping iron ore price upside. A sustained drawdown of these stocks would signal increased blast furnace activity and, by extension, increased coking coal consumption. Notably, China iron ore demand trends will remain a key leading indicator for coking coal consumption volumes throughout this period.

- Regulatory environment: China's coal mine safety inspection regime remains an unpredictable variable. Any additional fatalities or enforcement actions in the sector could trigger another round of production suspensions, potentially reversing the current oversupply dynamic rapidly.

Disclaimer: This article is intended for informational and educational purposes only. It does not constitute financial advice or a recommendation to buy or sell any commodity, security, or financial instrument. Commodity markets are inherently volatile and forecasts cited within this article represent analyst views at a specific point in time. Past price behaviour is not indicative of future performance. Readers should conduct their own independent research before making any investment decisions.

Want to Capitalise on the Next Major Commodity Market Move?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex commodity data into actionable investment insights for both short-term traders and long-term investors — explore historic discoveries and their exceptional returns to understand the scale of opportunity, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.