June 22, 2026

The Hidden Architecture of a Market Under Stress: Aluminium's Most Dangerous Supply Chokepoint

Most commodity market disruptions unfold along a single axis. A mine floods, a port closes, a labour dispute halts output. Recovery is linear, and the market adjusts. What is unfolding across West Asia in 2026 is structurally different, and West Asia aluminium supply disruptions are precisely what make this situation so consequential for global aluminium pricing through 2027 and beyond.

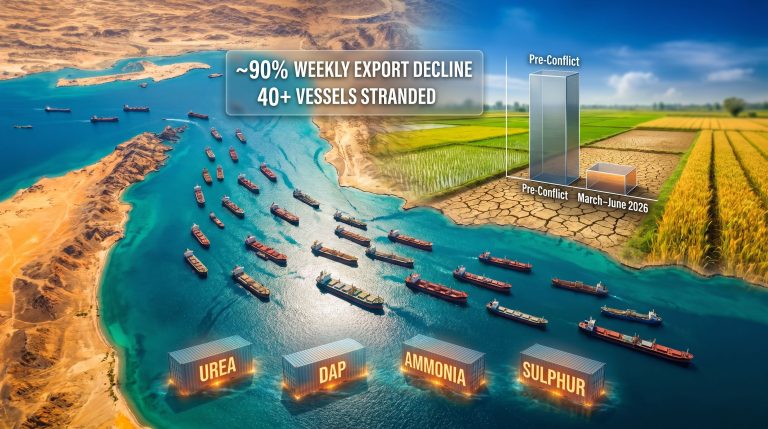

The region is not experiencing one disruption. It is experiencing three simultaneously: physical damage to smelting infrastructure, interruption to the natural gas supply that powers those smelters, and severe bottlenecks along the Strait of Hormuz. Each of these alone would be manageable. Together, they create a recovery constraint that the global aluminium market has not encountered in its modern form.

When big ASX news breaks, our subscribers know first

Why West Asia Aluminium Supply Disruptions Carry Disproportionate Global Weight

West Asia contributes approximately 8 to 10% of global primary aluminium output, a share that exceeds what the raw geography might suggest. The UAE and Bahrain have built large-scale smelting operations that have historically served buyers across Europe, Asia, and North America. Their competitive positioning has rested on three structural pillars: access to subsidised or low-cost natural gas, deep-water port infrastructure capable of handling bulk alumina imports, and geographic proximity to the Strait of Hormuz as an export artery.

That geographic advantage has now become a liability. The Strait of Hormuz handles an outsized share of global aluminium trade flows, and its disruption does not simply delay shipments. It physically traps inventory inside a region that is simultaneously losing production capacity. The result is a compounding feedback loop: less metal is being produced, and less of what remains can reach global buyers.

Furthermore, broader shifts in aluminium and alumina markets globally have already been testing supply chain resilience heading into this crisis, making the current disruption even harder to absorb.

Why Aluminium Smelters Are Uniquely Difficult to Restart

A detail that often escapes general market commentary is how technically constrained aluminium smelter restarts actually are. Unlike steel furnaces or oil refineries, aluminium pot lines operate as continuous electrolytic processes. When a pot line is shut down and the molten bath solidifies, the frozen cryolite and aluminium mixture must be carefully removed before the pot can be relined and recommissioned. This process alone can take several months per pot, and a full smelter contains hundreds of pots operating in parallel.

The implication is critical: even if geopolitical conditions resolve tomorrow, the physical act of restarting damaged smelting capacity in Bahrain and the UAE cannot be compressed into weeks. Industry analysts now expect Bahrain's production to return to pre-conflict levels no earlier than mid-2027, with UAE capacity recovery projected toward the end of 2027. These are not conservative assumptions — they reflect the engineering reality of aluminium smelter recommissioning under the best-case scenario.

Smelter restarts in the region are bound not by political timelines but by metallurgical ones. An interim agreement reopening the Strait of Hormuz does not put a single additional tonne of aluminium into production.

Quantifying the Production Loss: What the Revised Forecasts Actually Mean

Goldman Sachs, in its revised analysis of the West Asian supply situation, has cut its regional production estimates by 660,000 tonnes for 2026 and a further 1,000,000 tonnes for 2027, reflecting the delayed restart assumptions outlined above. The cumulative two-year production loss from the region now approaches 1.66 million tonnes, a figure that reshapes the entire global supply-demand balance.

| Metric | Previous Estimate | Revised Estimate | Change |

|---|---|---|---|

| West Asia output loss (2026) | Baseline | -660,000 tonnes | Significant downgrade |

| West Asia output loss (2027) | Baseline | -1,000,000 tonnes | Substantial downgrade |

| Global aluminium deficit (2026) | 570,000 tonnes | 720,000 tonnes | +150,000 tonnes wider |

| Global aluminium surplus (2027) | 1,300,000 tonnes | 590,000 tonnes | -710,000 tonnes narrower |

| Bahrain recovery timeline | H2 2026 | Mid-2027 | Delayed 6-9 months |

| UAE recovery timeline | H2 2026 | End-2027 | Delayed 6-12 months |

The 2027 surplus figure deserves particular attention. Prior to this crisis, the market was broadly positioned for a significant supply overhang in 2027, with 1.3 million tonnes of surplus expected to weigh on prices and compress margins for producers. That cushion has now been reduced to approximately 590,000 tonnes, fundamentally altering the risk profile for buyers and sellers alike who structured long-term contracts around the original forecast.

LME Price Signals and What the Forward Curve Reveals

On June 19, 2026, the LME aluminium cash offer price stood at $3,400 per tonne, representing a modest easing of 0.06% from the prior session. The 3-month bid and offer prices settled at $3,397.50 and $3,398 per tonne respectively, while the December 2027 contracts declined more sharply, with bid and offer prices falling 0.47% to $3,175 and $3,180 per tonne.

| Contract | Price (USD/tonne) | Movement |

|---|---|---|

| Cash Bid | $3,399 | -0.07% |

| Cash Offer | $3,400 | -0.06% |

| 3-Month Bid | $3,397.50 | -0.07% |

| 3-Month Offer | $3,398 | -0.09% |

| December 2027 Bid | $3,175 | -0.47% |

| December 2027 Offer | $3,180 | -0.47% |

| LME Asian Reference Price | $3,396.50 | Stable |

| LME Alumina (Platts) | $307.10/t | Unchanged |

The forward curve structure reveals something important about market psychology. The backwardation between spot prices ($3,400/t) and December 2027 contracts ($3,175-$3,180/t) tells a specific story: participants broadly believe supply will normalise over the two-year horizon, but they are uncertain about how quickly. The steepness of the decline also reflects the diminished surplus expected in 2027, which is now significantly smaller than what the market was pricing six months ago.

The Gap Between Market Pricing and Institutional Forecasts

A tension worth highlighting for investors and procurement professionals is the spread between where forward markets are pricing aluminium and where institutional analysts believe it should trade.

| Timeframe | Previous Forecast | Revised Forecast | Current Forward Price |

|---|---|---|---|

| Q3 2026 | $3,200/t | $3,300/t | ~$3,400/t |

| Full Year 2027 Average | $2,750/t | $2,950/t | ~$3,250/t |

Goldman Sachs has revised its Q3 2026 LME aluminium forecast upward to $3,300 per tonne from $3,200 per tonne, and lifted its full-year 2027 average to $2,950 per tonne from $2,750 per tonne. Despite these upgrades, the bank remains structurally bearish relative to current market pricing, suggesting the market may be overpricing near-term supply risk relative to what fundamental models support.

For buyers locking in forward contracts, this divergence creates genuine execution risk. If institutional forecasts prove accurate, those contracting at current forward prices of $3,250 to $3,400 per tonne may be building in costs above where the market ultimately settles.

Inventory Dynamics: A Thin Buffer Against Further Shocks

LME registered aluminium stocks on June 19 stood at 315,525 tonnes, having declined by 1,000 tonnes (0.32%) from the prior session. Live warrants totalled 247,575 tonnes, while cancelled warrants sat at 67,725 tonnes.

The cancelled warrant figure is particularly telling. Cancelled warrants represent metal that has been earmarked for physical delivery out of LME warehouses and is no longer available as a market buffer. With nearly 22% of registered stocks already earmarked, the effective available inventory cushion is thinner than the headline figure suggests. In a market already facing a 720,000-tonne deficit in 2026, this leaves limited room to absorb additional supply disruptions without pushing spot prices higher.

The alumina Platts price holding steady at $307.10 per tonne is an upstream signal worth monitoring. Reduced West Asian smelting activity has paradoxically freed up some alumina supply for other global buyers in the short term. However, if smelter restarts accelerate materially in 2027, a rapid reactivation of alumina demand from the region could create a secondary tightening in the upstream alumina market, propagating cost pressure further along the value chain. According to recent analysis on supply disruptions rattling the aluminium sector, this upstream-downstream feedback dynamic is increasingly concerning institutional buyers and producers alike.

Regional Fallout: Which Markets Bear the Heaviest Burden

Europe and the United States

Both regions import meaningful volumes of primary aluminium from West Asia, particularly high-purity grades used in automotive body sheet, aerospace components, and food-grade packaging. Rerouting shipments away from the Strait of Hormuz is adding freight costs and extending lead times, with regional physical premiums in Rotterdam and the US Midwest already reflecting the tighter availability environment.

In addition, US aluminium tariffs have already been reshaping how North American buyers structure their import strategies, and the West Asian disruption is now layering additional complexity on top of an already strained procurement environment. Buyers who would normally source spot tonnage from Gulf-origin material are now competing for the same replacement volumes from other origins, creating a compressive effect on available supply across major consuming markets simultaneously.

India: A Secondary Impact Zone

India's exposure operates through a different channel. Indian downstream manufacturers and secondary smelters rely on scrap aluminium flows from Gulf sources as a key input. Disruption to those flows is tightening domestic recycling economics, while elevated global premiums are filtering through to export-oriented Indian manufacturers serving European end-markets.

Higher freight costs from rerouting and rising input costs represent a margin squeeze for Indian producers who operate in competitive, price-sensitive segments of the global value chain. Consequently, end-user sectors worldwide are grappling with the present aluminium chaos, with knock-on effects spreading well beyond the Gulf region itself.

Sectors with the Highest Exposure

| Sector | Exposure Level | Primary Risk |

|---|---|---|

| Automotive | High | Tight primary aluminium supply for body sheet and castings |

| Construction and Extrusion | High | Reduced availability of billet and extrusion ingot |

| Packaging (Foil and Can) | Medium-High | Price inflation on rolling slab inputs |

| Aerospace | Medium | Speciality alloy supply chain disruption |

| Consumer Electronics | Medium | Upstream cost pressure on aluminium components |

The next major ASX story will hit our subscribers first

Indonesia and China: The Arithmetic of Replacement Supply

Indonesia's Accelerating Ramp-Up

Indonesian primary aluminium output is tracking approximately 89% higher year-on-year in 2026, reflecting faster-than-expected commissioning at major integrated facilities in the Morowali and Weda Bay industrial corridors. Projects associated with Adaro, Taijing Morowali, and Juwan Weda Bay have moved through commissioning ahead of schedule, prompting Goldman Sachs to revise Indonesia's production forecast to 1.7 million tonnes in 2026 and 2.9 million tonnes in 2027.

This trajectory positions Indonesia as the world's fastest-growing primary aluminium producer over the current planning horizon, a structural shift that will have lasting implications for regional trade flows and the competitive positioning of the top aluminium producers operating at higher cost bases elsewhere.

China Operating Above Its Nominal Capacity Ceiling

China's aluminium production forecasts have been revised to 45.6 million tonnes in 2026 and 46.3 million tonnes in 2027, both figures exceeding China's nominal 45 million tonne administrative capacity cap. The persistence of strong smelting margins is incentivising production at rates that technically breach the official ceiling, a pattern that has occurred before in Chinese industrial policy but which carries its own regulatory risk if Beijing moves to enforce the limit more strictly.

The incremental output growth from China between 2026 and 2027 amounts to approximately 700,000 tonnes, meaningful but insufficient on its own to bridge the West Asian shortfall. Furthermore, China's industrial demand dynamics remain a critical variable, as domestic consumption trends will ultimately influence how much incremental Chinese production actually flows into export markets versus being absorbed internally.

Why Timing Matters More Than Volume

West Asia Production Loss (2026-2027 combined): ~1,660,000 tonnes

Indonesia Incremental Growth (2026-2027 estimated): ~1,200,000 tonnes

China Incremental Growth (2026-2027 estimated): ~700,000 tonnes

Net Position: Volume partially covered, but timing mismatch creates a persistent deficit window

The critical insight here is not whether Indonesia and China can replace West Asian volume in aggregate. On an annualised basis, by late 2027, they largely can. The problem is the timing mismatch: the losses are occurring now, while the replacement volumes are ramping gradually over 18 to 24 months. That gap sustains the global deficit through most of 2026 and into the first half of 2027 regardless of what happens geopolitically.

Two Scenarios That Will Define Where Prices Land Through 2027

Scenario A: Slow Recovery

- Bahrain and UAE smelter restarts proceed at or slower than current projections (mid-to-late 2027)

- The global aluminium surplus in 2027 is largely neutralised, with the market remaining broadly balanced

- LME aluminium prices are supported near $3,250 per tonne through 2027

- Producers with unaffected capacity in China, Indonesia, and Australia-linked supply chains capture superior margins

- Downstream buyers face sustained cost pressure through mid-2027

Scenario B: Faster Recovery

- Geopolitical resolution accelerates smelter restarts into H1 2027, ahead of current projections

- West Asian, Indonesian, and Chinese supply converge simultaneously, expanding the 2027 surplus toward 1.2 million tonnes

- LME aluminium prices compress toward $2,750 per tonne by late 2027

- Buyers who locked in long-term contracts at 2026 peak prices carry above-market input costs

- High-cost producers face margin pressure as the surplus builds

| Variable | Slow Recovery | Fast Recovery |

|---|---|---|

| 2027 Global Balance | Broadly balanced | +1.2Mt surplus |

| LME Price (2027 average) | ~$3,250/t | ~$2,750/t |

| West Asia Restart Date | Mid to End 2027 | Q1 to Q2 2027 |

| Indonesia Ramp Speed | On track | Accelerated |

| China Output | At or above cap | At or above cap |

The Structural Reconfiguration of Global Aluminium Trade Routes

Beyond the immediate price and supply dynamics, the West Asia aluminium supply disruptions are accelerating a longer-term reconfiguration of how aluminium moves around the world. Shipping insurers and freight operators are repricing Strait of Hormuz transit risk not as a temporary event premium but as a permanent structural feature of Gulf-origin aluminium trade.

Alternative routing through the Red Sea and around the Cape of Good Hope is adding an estimated two to four weeks to delivery timelines on affected trade lanes. This is not simply a cost issue. Extended lead times force buyers to carry more inventory buffer, tying up working capital and reducing the flexibility of just-in-time procurement models that the automotive and electronics sectors have spent years optimising.

The broader implications also connect to how steel and aluminum tariffs have already reshaped trade flows, meaning that supply chain planners are now navigating a dual challenge of policy-driven and geopolitical-driven disruption simultaneously. The question that will define supply chain strategy over the next decade is whether the Strait of Hormuz risk premium becomes permanently embedded in the cost structure of Gulf aluminium, and whether that permanently erodes the competitive advantage that made West Asian smelters attractive to global buyers in the first place.

If Hormuz transit risk is now a structural rather than episodic cost, the economics of sourcing West Asian aluminium for European and North American buyers fundamentally change over the medium term.

Frequently Asked Questions

What percentage of global aluminium output comes from West Asia?

West Asia accounts for approximately 8 to 10% of global primary aluminium production, with the UAE and Bahrain as the two anchor producers. Their combined output makes regional disruptions materially significant for global trade balances, particularly for European and North American importers.

How long will production losses persist?

Based on current industry assessments, Bahrain's recovery to pre-conflict output levels is not expected before mid-2027, while UAE capacity is projected to recover by end-2027. These timelines are constrained by physical smelter damage and gas supply restoration requirements, not solely by geopolitical conditions.

What is the current global aluminium deficit forecast for 2026?

The global aluminium market is now forecast to record a deficit of 720,000 tonnes in 2026, widened from a prior estimate of 570,000 tonnes, driven by the downward revision to West Asian production.

Which countries are providing replacement supply?

Indonesia and China are the primary offset sources. Indonesia is forecast to produce 1.7 million tonnes in 2026 and 2.9 million tonnes in 2027, while China is projected at 45.6 million tonnes in 2026 and 46.3 million tonnes in 2027, both figures representing upward revisions from earlier estimates.

What are the revised LME aluminium price forecasts?

Revised institutional forecasts place LME aluminium at approximately $3,300 per tonne for Q3 2026 and a full-year 2027 average of $2,950 per tonne, though current forward markets are pricing materially higher levels, suggesting potential downside if supply recovers faster than expected.

How does this affect downstream manufacturers?

Sectors including automotive, construction, packaging, and aerospace face elevated input costs and tighter spot availability through at least mid-2027. Buyers who built procurement strategies around a large 2027 surplus scenario may need to revise their cost and inventory assumptions materially.

This article contains forward-looking statements, price forecasts, and scenario analyses drawn from publicly available institutional research and market data. All forecasts involve uncertainty and should not be construed as investment advice. Readers should conduct their own due diligence before making procurement or investment decisions based on any projections contained herein.

Want to Capitalise on the Next Major Commodity Discovery Before the Broader Market?

The aluminium supply shock unfolding across West Asia underscores how rapidly commodity market dynamics can shift — and how critical it is to act on significant discoveries the moment they are announced. Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries across more than 30 commodities, turning complex market data into actionable insights the moment they hit the exchange — explore historic examples of exceptional discovery returns and begin your 14-day free trial today to position yourself ahead of the market.