June 8, 2026

The Hidden Mechanics of China's Coking Coal Market and Why Safety Shutdowns Move Global Prices

Commodity markets are rarely disrupted by a single event in isolation. More often, a visible trigger exposes a structural vulnerability that was already present, accelerating a price response that the underlying system had been primed to deliver. The 2026 wave of China coking coal safety shutdowns is a textbook illustration of this dynamic, and understanding it requires looking beyond the headlines to the industrial architecture that makes Chinese coal supply so sensitive to regulatory action.

When big ASX news breaks, our subscribers know first

Why China's Coking Coal System Is Structurally Fragile

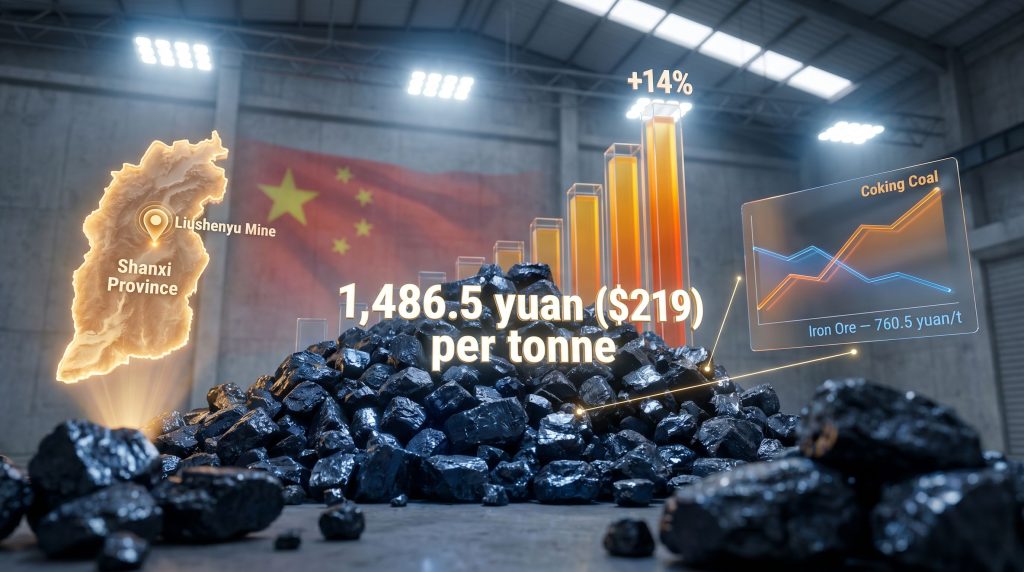

China steel and iron ore production sits at the centre of global output, accounting for roughly half of the world's annual steel volume. To sustain that scale, the country relies on an estimated 500 to 600 million tonnes per year of domestically mined coking coal, a figure that represents one of the largest single-country concentrations of any industrial raw material on Earth. The vast majority of this output flows from a relatively compact geographic cluster, with Shanxi Province functioning as the undisputed nerve centre of the entire system.

This concentration is a double-edged sword. On one hand, it enables highly efficient logistics and long-established mining infrastructure. On the other, it creates a systemic fragility where a regulatory event confined to one province can reverberate across national supply chains and, ultimately, international commodity benchmarks.

What makes Shanxi's position particularly consequential is the mix of operators involved. The province hosts both large state-controlled enterprises such as Shanxi Coking Coal Group and a substantial cohort of privately owned mines operating under varied compliance standards. This diversity of operators creates an uneven regulatory landscape where enforcement outcomes differ materially depending on ownership structure.

The Compliance Overhang That Markets Rarely Price In

One of the least discussed features of China's domestic coking coal market is the persistent gap between approved mining capacity and actual production volumes at many operations. A significant number of Chinese mines have historically operated at output levels that exceed their formally sanctioned capacity limits, a practice that regulators have intermittently targeted but rarely eliminated.

This creates what can be described as a compliance overhang: a large pool of production that exists in a legally ambiguous state and is therefore acutely vulnerable to suspension whenever regulatory attention intensifies. When a major incident forces inspectors into the field at scale, this overhang becomes an immediate supply risk.

Structural insight: The market rarely prices the full extent of this compliance overhang during periods of regulatory calm, which means that when enforcement accelerates, the price adjustment can be sharp and disproportionate relative to the immediate physical disruption.

The Liushenyu Disaster: A Catalyst With Systemic Consequences

In mid-2026, a fatal explosion at the Liushenyu mine in Shanxi killed at least 82 people, making it the deadliest coal mining disaster in China in more than 16 years. The immediate human toll was severe, but the regulatory consequences proved equally significant for markets.

Post-incident investigations uncovered evidence of deeply embedded non-compliance at the mine. Authorities found concealed tunnels and false structural barriers that had been deliberately constructed to mislead safety inspectors about the actual scale and configuration of mining operations. This was not a case of minor procedural shortfalls. It was evidence of systematic, deliberate regulatory evasion.

The nature of the violations triggered a response that went well beyond the standard post-accident safety review. Regulators launched a broadened provincial and then national inspection campaign, with Shanxi as the primary focus but with other provinces drawn into the enforcement net as well.

The Multi-Province Shutdown Cascade

The scope of production halts that followed is summarised below:

| Province | Action Taken | Timeline | Estimated Capacity Affected |

|---|---|---|---|

| Shanxi | Tunnelling suspensions; mine halts including state-owned operators | Ongoing post-accident | ~60 million t/yr halted |

| Shandong | Higher-risk mines suspended or production reduced | 22 June to 5 July; full halt 30 June to 2 July | Not fully disclosed |

| Hubei | All local coal mines suspended by safety administration | 15 June to 5 July | 17 mines / 1.71 million t/yr |

Across affected regions, approximately 60 million tonnes of annual production capacity remained halted as of the most recent reporting period. Critically, even mines that had been permitted to resume operations were producing at only 70 to 80% of pre-accident output levels, reflecting the operational disruption caused by intensive on-site inspections that slow day-to-day workflows even at compliant facilities.

How China Coking Coal Safety Shutdowns Translate Into Price Signals

The price mechanism connecting mine-level shutdowns to commodity market movements operates through a fairly direct chain of causation, but the speed and magnitude of the response depends on how tightly the physical market was balanced before the disruption began.

Coking coal futures on the Dalian Commodity Exchange rose as much as 1.9% in a single trading session, reaching 1,486.5 yuan (approximately $219) per tonne, the highest level recorded since October 2024. Month-to-date price appreciation reached approximately 14%, a rapid repricing that reflects the market's recognition that the disruption is not short-lived. Furthermore, futures subsequently settled around 1,460 yuan per tonne after partial intraday retracement.

According to analysis from Horizon Insights, the recovery in Shanxi coal production has consistently fallen short of expectations, with safety supervision remaining intensive enough to sustain meaningful tightness in the spot market. These iron ore market impacts and broader commodity ripple effects are increasingly drawing attention from global investors.

The Seaborne Transmission Mechanism

When domestic Chinese coking coal supply contracts, steel mills and coke producers face a straightforward decision: absorb higher domestic spot prices or source material from international markets. When enough buyers turn to seaborne supply, the demand pressure elevates international benchmarks, pulling prices in Australia, Canada, and Mongolia higher in tandem.

This price floor transmission effect is one of the most important and least widely understood dynamics in the global metallurgical coal complex. The Chinese domestic market, despite being technically separate from seaborne trade, functions as an anchor for international pricing because of the sheer scale of potential import demand China can direct at the seaborne market when domestic supply falters.

Key mechanism: Chinese domestic coking coal prices effectively set a gravitational pull on seaborne benchmarks. When the domestic price premium widens, it creates an arbitrage incentive that increases Chinese import demand and progressively closes the gap with international prices.

Related Commodity Divergence Worth Noting

Not all steel-related commodities moved in the same direction during this episode, which itself reveals something important about market interpretation of the event:

- Iron ore futures on Dalian declined 0.7% to 760.5 yuan per tonne, suggesting the market is reading the disruption as a supply shock to coking coal specifically, not as a signal of stronger steel demand.

- Iron ore in Singapore also fell 0.7% to $101 per tonne, reinforcing the decoupled trajectory between the two key steelmaking inputs.

- The Baltic Dry Index dropped 1.8% to 2,981 points at Friday's close, marking its sixth consecutive daily decline and suggesting that broader bulk freight demand remains under pressure despite the coking coal tightness.

This divergence is analytically significant. A genuine demand-side steel boom would typically lift both coking coal and iron ore simultaneously. The fact that iron ore is softening while coking coal surges confirms this is a supply-driven event, not a demand story.

The Blast Furnace Supply Chain Under Pressure

Metallurgical coke occupies a position in steelmaking that has no practical substitute in blast furnace operations at industrial scale. The production process requires coking coal to be heated in sealed ovens at extremely high temperatures in an oxygen-free environment, transforming the coal into a porous, high-carbon material capable of supporting the enormous weight of iron ore burden inside a blast furnace.

The quality specifications for coking coal are considerably more demanding than those for thermal coal burned in power stations. Volatile matter content, caking index, and ash content are the primary quality parameters that determine whether a coal can produce coke of sufficient strength, measured by the Coke Strength after Reaction (CSR) index, to function properly in a large blast furnace. Low-CSR coke can cause furnace instability, higher coke consumption rates, and potential damage to furnace linings.

This technical specificity means that not all coking coal is interchangeable. Premium hard coking coals from Australia's Bowen Basin command significant price premiums over lower-rank semi-soft coking coals because of their superior coke-making properties. When Chinese domestic supply of higher-quality coking coal tightens, the import demand that emerges tends to target premium grades, amplifying steel price pressures at the top of the quality spectrum.

The Cascading Cost Structure for Chinese Steelmakers

The supply shock creates a sequential cost escalation that flows through the entire steelmaking value chain:

- Coking coal spot prices rise as mine shutdowns constrain available supply.

- Coke oven operators face higher input costs, compressing margins at the coke production stage.

- Metallurgical coke prices increase, elevating the primary variable cost for blast furnace steelmakers.

- Integrated steel mill margins compress as raw material costs rise while finished steel prices may lag.

- Output discipline may emerge voluntarily, with some mills choosing to reduce blast furnace utilisation rates to avoid producing at a loss.

- Steel prices may adjust upward if demand conditions support cost pass-through, but this depends on construction and infrastructure activity.

Critical uncertainty: China's property sector and broader construction activity remain under significant structural pressure. This limits the ability of steelmakers to pass higher input costs through to steel buyers, meaning margin compression at mills could be substantial if the coking coal disruption persists for an extended period.

Duration Risk: Why This Cycle May Last Longer Than Historical Precedent

Historical analysis of Chinese coal safety enforcement cycles suggests that production typically begins recovering toward pre-event levels within four to twelve weeks of an initial disruption. However, several factors specific to the 2026 episode create credible reasons to expect a longer-than-average disruption:

- The severity of the violations uncovered at Liushenyu, including deliberately constructed deception infrastructure, is likely to trigger more thorough and prolonged inspections across the sector than a standard post-accident review.

- The nationwide expansion of inspections beyond Shanxi into Shandong and Hubei suggests regulators are treating this as a systemic compliance failure rather than a site-specific incident, meaning the inspection scope is broader and the administrative clearance process will take longer.

- State-owned vs. private operator dynamics are likely to produce uneven reinstatement timelines. State-controlled mines are generally expected to move through the inspection queue with less friction than privately owned operations, creating a bifurcated recovery pattern.

- Political calendar sensitivity is a recurring feature of Chinese coal safety enforcement. The intensity of scrutiny applied during politically significant periods tends to be sustained until those periods conclude, after which regulatory pressure often eases more rapidly.

The next major ASX story will hit our subscribers first

Global Market Implications for Coking Coal Exporters

The countries best positioned to benefit from elevated Chinese import demand during domestic supply disruptions are those with established seaborne metallurgical coal export infrastructure:

| Exporting Country | Primary Coal Type | Relevance to China |

|---|---|---|

| Australia | Premium hard coking coal (Bowen Basin) | Largest seaborne supplier; primary beneficiary of import demand increases |

| Mongolia | Hard coking coal (Tavan Tolgoi basin) | Overland supply route; growing share of Chinese imports |

| Canada | Premium hard coking coal (Peace River, Elk Valley) | High-quality supplier; benefits from broader seaborne price support |

| United States | Hard coking coal (Central Appalachia) | Smaller but meaningful seaborne volumes |

Australia's Bowen Basin region in Queensland is particularly central to this story. It hosts some of the highest-quality coking coal deposits globally, with premium hard coking coals characterised by low sulphur content, moderate ash levels, and the caking properties necessary to produce high-CSR coke. When Chinese import demand accelerates, Australian FOB prices are typically the first international benchmark to reflect the pressure.

Mongolia's role is worth examining more closely. The country's Tavan Tolgoi coal basin holds enormous reserves of coking coal accessible via overland transport directly into Inner Mongolia and Shanxi, giving it a logistical cost advantage over seaborne suppliers. However, infrastructure capacity constraints on the border crossing routes can limit the pace of volume ramp-up, even as the global crude steel outlook remains under close scrutiny.

Investor Considerations and Market Psychology

For market participants tracking the metallurgical coal complex, the 2026 China coking coal safety shutdowns cycle illustrates several patterns worth internalising for future episodes:

- Supply shocks driven by regulatory enforcement tend to be underestimated in their duration because markets initially assume that production will resume quickly, as it often has in past cycles. When the underlying violations are more serious than typical, the market repeatedly revises its recovery timeline, creating a series of upward price adjustments rather than a single sharp spike.

- The compliance overhang effect means that total shut-in capacity during major inspection campaigns often surprises to the upside. Not all of the affected production was economically marginal. Some of it was operating profitably but in violation of approved limits, meaning the supply loss is real and sustained.

- Seaborne price lag is a recurring feature of these episodes. International prices typically trail the domestic Chinese price move by days to weeks as the market waits for confirmation that import demand is genuinely accelerating. This lag can create windows for positioning in Australian or Canadian coking coal equities before the full price adjustment is reflected.

- Iron ore divergence serves as a useful signal. When coking coal rises but iron ore falls simultaneously, it confirms a supply-side disruption narrative rather than a demand-driven recovery, which is relevant for assessing how long the price support can be sustained without a corresponding improvement in steel mill economics. For broader context, the China steel outlook for 2025 and beyond further illustrates these structural tensions.

Furthermore, analysts tracking weekly coking coal production data have noted that output slowdowns during safety check intensification periods consistently exceed initial market estimates.

This article is intended for informational purposes only and does not constitute financial advice. Commodity markets involve significant risk, and past price behaviour during previous disruption cycles does not guarantee similar outcomes in future events.

Key Variables to Track as the Situation Evolves

The following indicators will be most informative in assessing the trajectory of the current supply disruption:

- Weekly Dalian coking coal futures settlement prices relative to the 1,486 yuan high-water mark established during the initial spike.

- Shanxi provincial mine restart announcements, particularly from state-owned operators, which will signal whether regulators are beginning to ease the inspection intensity.

- Chinese coking coal import volumes from Australian and Mongolian origins, which will confirm whether domestic tightness is translating into measurable seaborne demand increases.

- Coke plant operating rates in Shanxi and Hebei provinces, which will indicate whether the coal supply constraint is beginning to bite at the downstream coke production level.

- Chinese blast furnace utilisation rates, reported weekly by industry trackers, which will reveal whether steelmakers are beginning to moderate output in response to input cost pressure.

The 2026 wave of China coking coal safety shutdowns represents more than a transient price event. It reflects deep structural features of a supply system that concentrates enormous industrial output within a geographically compact, regulatory-sensitive zone. For anyone tracking the global metallurgical coal complex, understanding the mechanics behind these shutdowns, rather than simply observing the price movement, is what separates a reactive market participant from an informed one.

Want to Stay Ahead of the Next Major ASX Mineral Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly transforming complex commodity data into actionable insights for both short-term traders and long-term investors. Explore historic discoveries and their exceptional returns, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.