June 8, 2026

The Anatomy of an Oil Market Illusion: Why Paper Barrels Don't Move Markets

There is a persistent misconception in energy market commentary that production quota announcements by major oil-producing blocs translate directly into physical supply changes. In reality, the relationship between what a cartel announces and what actually flows through pipelines and tanker routes is far more complex. Understanding this distinction is not just academic; it is the difference between misreading an oil price surge and correctly diagnosing the structural forces behind it.

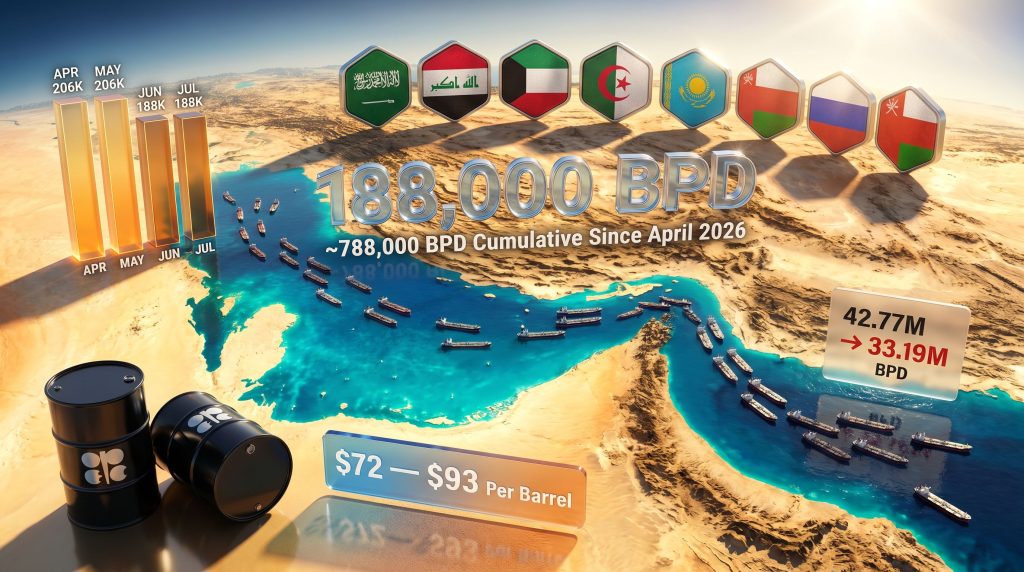

The OPEC+ oil output hike in July 2026 offers one of the clearest recent examples of this gap between policy signal and market reality. On paper, the decision looks straightforward: seven core member nations ratified a collective production quota increase of 188,000 barrels per day (bpd) effective July 2026, continuing a sequence of monthly increases that began in April. In practice, the announcement is operating inside a geopolitical and logistical environment that severely limits its real-world impact.

When big ASX news breaks, our subscribers know first

What the July Decision Actually Represents Within OPEC+'s Broader Strategy

The July OPEC+ oil output hike does not exist in isolation. It is the fourth consecutive monthly production target increase approved since April 2026, forming part of a structured plan to gradually reverse a 1.65 million bpd voluntary production cut that the group originally agreed to in 2023. That earlier cut was implemented as a demand-management tool during a period of global economic uncertainty and softer oil consumption growth.

The seven nations participating in the June 8 decision were Saudi Arabia, Iraq, Kuwait, Algeria, Kazakhstan, Russia, and Oman. Notably absent from this configuration is the United Arab Emirates, whose exit from OPEC+ earlier in 2026 directly altered the group's collective quota baseline and contributed to a downward revision in the per-month increase target. OPEC's market influence extends well beyond simple quota announcements, shaping everything from tanker scheduling to long-term supply contracts.

The monthly increment was adjusted from 206,000 bpd (used in April and May 2026) down to 188,000 bpd, a reduction directly linked to the UAE's departure. This structural change is frequently underreported but carries significant implications for how the remaining cut unwind is calculated.

The cumulative progress of the 2023 cut reversal can be mapped across the four-month sequence:

| Month | Output Increase (bpd) | Cumulative Increase Since April 2026 |

|---|---|---|

| April 2026 | 206,000 | 206,000 |

| May 2026 | 206,000 | 412,000 |

| June 2026 | 188,000 | ~600,000 |

| July 2026 | 188,000 | ~788,000 |

Following the July hike, approximately 567,000 bpd of the original cut still remains to be restored to the market, adjusted for the UAE's exit. If the current pace is maintained through August and September 2026, the full unwind could theoretically be completed by the end of Q3 2026.

| Phase | Volume Restored (bpd) | Remaining Cut (bpd) |

|---|---|---|

| Pre-July 2026 increases | ~600,000 | ~1,050,000 |

| Post-July 2026 increase | ~788,000 | ~862,000* |

| Projected completion (Aug-Sep 2026) | ~567,000 remaining | ~0 (est. end-Sep 2026) |

*Adjusted for UAE exit from the group

The Strait of Hormuz Factor: When Physical Geography Overrides Policy

To understand why the OPEC+ oil output hike in July has not translated into lower oil prices, it is necessary to examine the role of the Strait of Hormuz as a structural bottleneck in global energy trade. Furthermore, the OPEC production decisions made in recent months must be viewed through the lens of this physical constraint rather than as standalone policy signals.

The Strait of Hormuz is the narrow waterway separating the Persian Gulf from the Gulf of Oman. At its narrowest point, it measures approximately 33 kilometres wide, yet through it passes an estimated 20 to 21 million barrels of oil per day, representing roughly one-fifth of global petroleum liquids consumption. For major producers including Saudi Arabia, Iraq, Kuwait, and the UAE, the Strait is not merely a convenient route; it is the only viable export corridor for the vast majority of their crude shipments.

The ongoing US-Iran conflict, which escalated significantly in early 2026, introduced severe disruptions to Hormuz transit capacity. The consequences for physical oil supply were immediate and dramatic:

- OPEC group production averaged approximately 42.77 million bpd in February 2026, before the disruptions intensified

- By April 2026, that figure had collapsed to 33.19 million bpd

- The contraction of nearly 9.6 million bpd within two months represents one of the sharpest short-term supply dislocations in the cartel's recorded history

- Saudi Arabia, the world's largest single oil exporter, found itself unable to fully meet contracted customer obligations during this period

The critical insight here is that a quota increase announced by OPEC+ only carries genuine market weight when the physical infrastructure and geopolitical conditions exist to actually deliver those additional barrels to buyers. Throughout much of the April-July 2026 window, those conditions have remained deeply compromised.

Jorge Leon, an analyst at Rystad Energy and a former OPEC official, has publicly noted that an OPEC+ production increase carries limited market significance while the Strait of Hormuz remains closed to normal traffic. He has further flagged that once Hormuz transit capacity is restored, markets could transition very rapidly from a posture of shortage anxiety to one of surplus concern, underlining how much of the current price environment is driven by geopolitical risk premium rather than fundamental supply-demand imbalance. (Reuters, June 2026)

How Oil Prices Have Responded: Reading the Geopolitical Risk Premium

Oil price behaviour during this period illustrates the disjunction between announced policy and market fundamentals in stark numerical terms. Indeed, the oil price movements observed throughout this window reflect a market increasingly driven by transit risk rather than conventional supply-demand dynamics.

- Prices were trading near $72 per barrel immediately prior to the US-Iran conflict escalation

- At peak conflict anxiety, prices surged to approximately $93 per barrel

- By early June 2026, prices retreated toward the lower end of that range as trader sentiment shifted toward a reduced probability of sustained escalation

This $21 per barrel spread between pre-conflict and peak-conflict pricing represents the measurable geopolitical risk premium embedded in the market. Consecutive OPEC+ quota increases have failed to compress this premium because the additional supply they represent cannot physically reach buyers while Hormuz disruptions persist.

The implication for market participants is significant: current oil prices are not primarily responding to supply-demand fundamentals in the conventional sense. They are functioning as a real-time probability-weighted forecast of geopolitical resolution. When traders assess that de-escalation is more likely, prices fall. When escalation risk re-emerges, prices rise, regardless of what OPEC+ has announced in terms of production targets.

Three Scenario Pathways Once Hormuz Transit Normalises

The eventual reopening of the Strait of Hormuz to normal commercial traffic will represent a critical inflection point for global oil markets. Three broad scenarios can be mapped depending on the speed and manner of that restoration:

Scenario 1: The Rapid Surplus Reversal

This pathway involves suppressed quota volumes flooding back into the market simultaneously as transit restrictions lift. The speed of the reversal could generate a sharp price correction as buyers who had been rationing demand suddenly face a volume of competing supply that the market cannot immediately absorb. OPEC+ would likely face intense internal pressure to reimpose coordinated cuts.

Scenario 2: The Managed Gradual Reintegration

In this scenario, member nations phase physical output back in line with existing quota targets over a controlled period. Incremental supply additions are absorbed without triggering a price shock, and the 1.65 million bpd cut unwind completes broadly on schedule by late Q3 2026. This outcome requires both geopolitical stabilisation and disciplined member behaviour, neither of which can be assumed.

Scenario 3: The Structural Demand Shortfall

Post-conflict demand destruction in affected regions, particularly import-dependent economies in Asia that may have accelerated diversification efforts during the disruption, reduces net import volumes below pre-crisis levels. In this scenario, OPEC+ quota increases become structurally irrelevant as weakened demand dominates price dynamics, and oil prices stabilise well below pre-conflict levels even after supply access is restored.

OPEC+'s Internal Cohesion Problem: A Structural Fault Line

Beyond the immediate geopolitical drama, the July OPEC+ oil output hike surfaces deeper questions about the bloc's long-term structural coherence. These oil market disruptions have, consequently, exposed fragilities in the group's coordination architecture that were previously obscured by relatively stable trading conditions.

The UAE's departure from the group is not merely an administrative footnote. It signals that individual member nations with competitive production cost structures may increasingly find the constraints of group quota discipline less tolerable than the benefits of coordinated pricing power. The UAE has been aggressively investing in production capacity expansion, and binding quota frameworks limit its ability to monetise that investment at the pace it desires.

Two chronic overproducers within the remaining group, Kazakhstan and Iraq, have maintained a persistent pattern of production levels that exceed their assigned quota targets. This compliance gap is not a new development; both nations have routinely produced above agreed ceilings while making formal commitments to compensatory cuts that rarely materialise in full. The persistence of this behaviour fundamentally undermines the group's stated production figures and makes quota announcements less credible as market signals.

When actual group production runs consistently below quota targets, as it does during Hormuz disruption periods, and simultaneously some members overproduce relative to their individual allocations, the coherence of the entire quota framework becomes difficult to defend analytically.

The next major ASX story will hit our subscribers first

What This Means for Import-Dependent Economies and Energy Transition Strategy

The supply disruption has not affected all economies equally. Nations most exposed to Hormuz-dependent crude imports have faced the sharpest supply access challenges and price pressures. This cohort includes most of South and East Asia's large industrial economies, which collectively absorb a substantial share of Gulf crude exports.

Several governments have activated strategic petroleum reserves to buffer domestic markets, a tool with a finite operational window. The more structurally significant response is whether the disruption accelerates capital allocation toward energy diversification. In addition, the geopolitical oil price drivers at play here suggest that import-dependent nations face a more complex risk environment than simple commodity price hedging can address.

The argument that supply crises accelerate energy transition timelines is historically supported: the 1970s oil shocks catalysed the first major wave of energy efficiency investment and nuclear power expansion across OECD economies. Whether the 2026 Hormuz disruption produces a comparable structural reorientation depends on the duration and severity of the crisis, the cost competitiveness of renewable alternatives in affected markets, and the political will of import-dependent governments to accept higher near-term infrastructure costs for long-term supply independence.

According to reporting from Reuters, OPEC+ pressed ahead with the July output increase despite the Hormuz disruption, underscoring the bloc's commitment to its broader unwind timeline regardless of near-term physical delivery constraints.

Frequently Asked Questions: OPEC+ July Oil Output Hike

What did OPEC+ decide for July 2026 oil production?

Seven core OPEC+ member nations approved a collective output quota increase of 188,000 barrels per day effective July 2026, the fourth consecutive monthly production target rise since April 2026.

Which countries participated in the July 2026 OPEC+ output decision?

The seven participating nations were Saudi Arabia, Iraq, Kuwait, Algeria, Kazakhstan, Russia, and Oman.

Why is the July hike smaller than April and May 2026 increases?

The monthly increment was revised down from 206,000 bpd to 188,000 bpd following the United Arab Emirates' exit from OPEC+, which altered the group's collective quota baseline.

Why hasn't increased OPEC+ output brought oil prices down?

Physical export capacity from major Gulf producers remains severely constrained by ongoing disruptions to shipping through the Strait of Hormuz. Quota increases do not translate to additional barrels reaching buyers when transit infrastructure is compromised.

When could OPEC+ complete the full unwind of its 2023 production cuts?

If monthly increases of approximately 188,000 bpd continue through August and September 2026, the remaining 567,000 bpd of the original 1.65 million bpd cut could be fully restored by the end of September 2026.

What happens to oil prices if the Strait of Hormuz reopens?

Analysts have flagged the potential for a rapid price reversal, with markets potentially shifting from supply-shortage anxiety to supply-surplus concern as previously blocked volumes re-enter global trade routes simultaneously. Bloomberg's coverage of recent OPEC+ deliberations highlights how the group itself is weighing the risk of oversupply once transit normalises.

Key Takeaways for Market Participants

- Quota does not equal supply: The 188,000 bpd OPEC+ oil output hike in July is a policy directive, not a confirmed physical supply addition while Hormuz transit remains disrupted

- The risk premium is quantifiable: The gap between pre-conflict pricing near $72 per barrel and peak-conflict pricing near $93 per barrel represents approximately $21 of geopolitical risk embedded in current oil prices

- Cut unwind timeline: OPEC+ is tracking toward full reversal of its 2023 voluntary production cut by late Q3 2026, contingent on geopolitical stabilisation and continued member compliance

- Cohesion risk is real: The UAE's exit and persistent overproduction by Kazakhstan and Iraq raise structural questions about the bloc's long-term coordination capacity

- Scenario asymmetry matters: A Hormuz reopening could trigger a faster-than-expected price correction, creating asymmetric downside risk for energy markets currently priced for sustained scarcity

- Demand destruction is a wildcard: Import-dependent economies that have been forced to reduce consumption during the disruption period may not immediately restore pre-crisis import volumes, adding a demand-side variable to post-resolution price modelling

Disclaimer: This article is intended for informational purposes only and does not constitute financial or investment advice. Forward-looking statements, scenario projections, and price forecasts involve inherent uncertainty and should not be relied upon as predictive of future market outcomes. Readers are encouraged to conduct independent research and consult qualified financial advisers before making investment decisions.

Want to Stay Ahead of the Next Major Resource Discovery Before the Market Catches On?

While oil markets grapple with the gap between paper policy and physical supply, savvy investors understand that real opportunity often lies in being first to act on verified discoveries — Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant alerts on significant mineral discoveries and turning complex data into actionable investment insights. Explore historic discoveries and the returns they generated, then start your 14-day free trial to position yourself ahead of the market.