August 9, 2026

Energy Import Dependencies and Critical Supply Chain Vulnerabilities

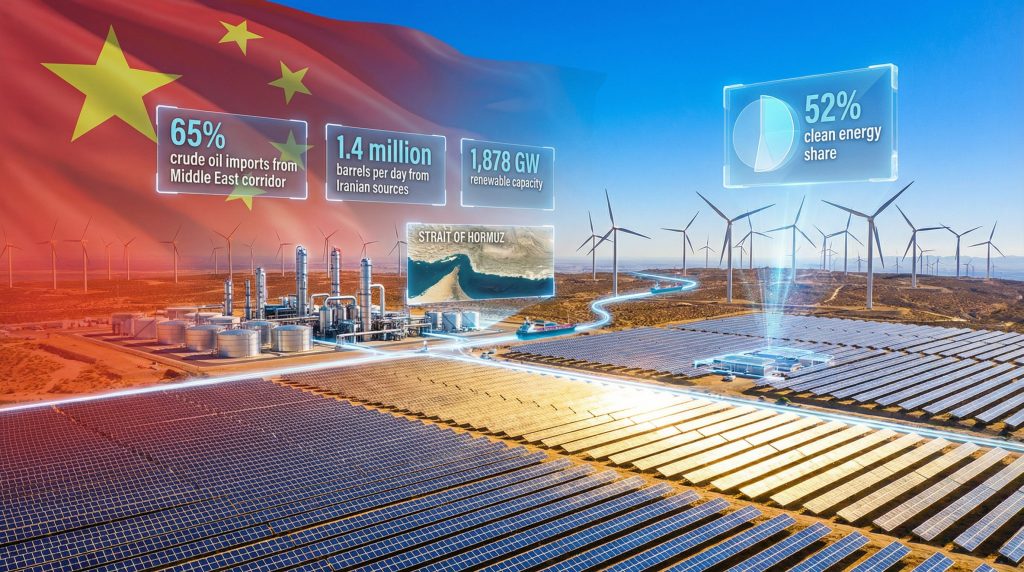

China's position as the world's largest crude oil importer has created a complex web of dependencies that define its current China energy security landscape. The nation imports approximately 10-11 million barrels daily, with roughly 65 percent originating from Middle Eastern sources, creating what energy analysts term critical pathway dependency through maritime chokepoints.

The Strait of Hormuz represents the most significant vulnerability in this supply architecture. Daily crude oil transits through this narrow waterway exceed 4-5 million barrels destined for Chinese refineries, representing approximately 85-90 percent of China's seaborne crude imports. This concentration creates economic and technical barriers to alternative routing, as diversion through extended Indian Ocean routes adds 10-14 transit days and $1.50-3.00 per barrel in transport costs.

Strategic Buffer Capacity Assessment

China maintains strategic petroleum reserves estimated at 900-950 million barrels across distributed storage facilities, with rapid deployment capacity of 100-150 million barrels. This inventory level provides approximately 60-70 days of import coverage, positioning China among the highest reserve-holding economies relative to consumption patterns. The combination of onshore inventory plus in-transit volumes creates dual-layer strategic depth, with approximately 25-40 million barrels perpetually en route to Chinese discharge facilities.

Independent refineries constitute a particular vulnerability vector within China energy security framework. These facilities, concentrated in Shandong province, process approximately 4-4.5 million barrels daily and demonstrate higher Iranian crude feedstock reliance than state-owned refiners. Iranian crude historically comprises 20-30 percent of independent refinery feedstocks, creating disproportionate exposure during sanctions periods that could force curtailment of 800,000-1,000,000 barrels daily of processing capacity.

When big ASX news breaks, our subscribers know first

Geopolitical Risk Assessment and Strategic Response Mechanisms

The evolving Middle East conflict landscape demonstrates how geopolitical tensions reshape China energy security calculations. Commercial shipping disruptions through the Strait of Hormuz, while temporarily halting normal transit patterns, reveal both vulnerabilities and resilience mechanisms within China's supply chain architecture. Furthermore, the potential oil price rally 2025 could significantly impact China's import costs and strategic planning.

Oil price volatility during recent disruptions reflected moderate market responses, with crude futures experiencing 8-15 percent intraday swings. This measured reaction, compared to historical conflict precedents that produced $20-30 price movements, suggests market confidence in offsetting supply buffers and limited duration expectations for major disruptions.

Supply Disruption Cascade Analysis

A theoretical Strait closure for 30 days would prevent approximately 300-330 million barrels from reaching Chinese refineries through normal routing. China's rapidly deployable reserves would address 30-45 percent of this shortfall, requiring alternative sourcing for the remaining 200 million barrels at premium prices historically ranging 20-50 percent above baseline levels.

Refining curtailment mechanics involve complex technical adjustments requiring 7-10 days for throughput reductions of 15-20 percent. Product shortages would materialise within 2-4 weeks, affecting gasoline and diesel markets across Asia-Pacific regions. This timeline creates political pressure to maintain imports despite premium pricing, limiting practical demand destruction options.

The 2022 Russian energy embargo provides relevant precedent for disruption response. China absorbed approximately 700,000-800,000 barrels daily of disrupted Russian imports through inventory draw-down and rapid supply diversification to Kazakhstan, Saudi Arabia, and Iraq. Consequently, the US-China trade war impact on global markets continues to shape energy relationships and strategic partnerships.

Geographic Supply Diversification Strategies

Russian energy partnerships represent the most quantified diversification achievement within China energy security planning. Crude imports from Russia increased from 250,000-300,000 barrels daily in 2010 to approximately 1.5-1.6 million barrels daily by 2025, surpassing Saudi Arabia as China's largest supplier source.

The Eastern Siberia Pacific Ocean pipeline system delivers 600,000-700,000 barrels daily directly to China's processing infrastructure. This land-based corridor eliminates maritime chokepoint vulnerabilities while providing 10-12 day transit times compared to 30-40 days for Middle Eastern seaborne shipments.

African Market Integration Framework

| African Supplier | Daily Volume (barrels) | Strategic Significance |

|---|---|---|

| Angola | 400,000-500,000 | Primary West African source |

| Congo | 200,000-300,000 | Expanding production capacity |

| Nigeria | 100,000-150,000 | Light crude quality advantages |

| Equatorial Guinea | 50,000-80,000 | Equity investment partnerships |

Chinese national oil companies hold operatorship or significant equity stakes in African petroleum production, providing preferential access to output increments. These long-term equity crude investments create supply security independent of spot market dynamics or geopolitical disruptions affecting traditional Middle Eastern suppliers. In addition, developments in Saudi exploration licenses could impact global supply dynamics and China's strategic positioning.

Domestic Production and Energy Independence Initiatives

China's domestic crude production maintains approximately 3.6-3.8 million barrels daily, providing substitution capacity unavailable to pure-import-dependent Asian competitors. The policy framework targeting 80 percent indigenous energy production by 2030 encompasses both conventional petroleum resources and coal-to-liquids expansion programmes. However, challenges such as US oil production decline could create new opportunities for China's domestic energy sector.

Unconventional resource development includes shale oil exploration in Xinjiang and offshore drilling expansion in the South China Sea. These initiatives, whilst expensive relative to imported alternatives, provide strategic value through supply chain control and reduced external vulnerability exposure.

The coal reserve utilisation strategy follows a "first build, then destroy" policy approach, expanding coal-fired capacity in the near term while simultaneously developing renewable alternatives. This dual-track methodology ensures energy security during the transition period while maintaining long-term decarbonisation commitments.

Renewable Energy Infrastructure and Grid Modernisation

China's renewable energy transformation represents the most comprehensive approach to long-term energy independence within the global economy. Total renewable capacity reached 1,878 GW in 2024, with solar installations generating 366 TWh and integrated wind capacity providing substantial grid-scale power generation.

What Are China's Clean Energy Deployment Metrics?

The 2030 targets include 1,200 GW of combined solar and wind capacity, achieving 52 percent clean energy share across national electricity generation. Grid parity achievement in solar installations eliminates subsidy requirements whilst offshore wind expansion enhances maritime energy security capabilities.

Ultra-high voltage network investments totalling $80 billion enable efficient power transmission across China's vast geography. AI dispatch optimisation and smart grid integration provide flexible load management, while $28 billion in battery and hydrogen storage systems address intermittency challenges inherent in renewable generation.

Flexible coal retrofitting allows existing thermal plants to provide backup generation during renewable output variability. This technological approach maximises existing infrastructure value while supporting grid stability throughout the energy transition process. Furthermore, the natural gas forecast suggests continued importance of fossil fuel backup during renewable transitions.

Critical Minerals and Supply Chain Control

China's dominance in battery mineral production creates strategic leverage within global clean energy transitions. Leadership in lithium, cobalt, and rare earth production extends from mining operations through refining and value-added manufacturing, providing vertical integration across the entire supply chain.

Domestic critical mineral development reduces reliance on overseas suppliers whilst expanding processing capacity scales China's position in battery and renewable energy equipment manufacturing. African and Latin American partnerships supplement domestic resources through long-term supply agreements and equity investments in mining operations.

Technology Export Positioning

Clean energy equipment manufacturing capabilities enable China to export solar panels, wind turbines, and battery systems globally whilst maintaining domestic supply chain security. This dual advantage supports both energy independence objectives and economic competitiveness in emerging technology sectors.

Processing capacity scaling ensures that raw material imports undergo value-added manufacturing within China, capturing economic benefits whilst building technological expertise in advanced energy storage and generation systems.

The next major ASX story will hit our subscribers first

Carbon Neutrality Integration with Energy Security

The 2060 net-zero pathway requires coordinated fossil fuel phase-out whilst maintaining energy supply reliability throughout the transition period. Peak emissions achievement in 2024 provides earlier-than-expected progress toward long-term climate commitments whilst accelerating clean technology deployment.

Industrial competitiveness considerations balance environmental objectives with economic security requirements. Energy cost advantages through domestic renewable production support manufacturing sectors whilst export market positioning in clean technology creates new revenue streams replacing traditional energy exports. For more detailed analysis of China's energy strategies, the China Energy Security report provides comprehensive insights.

Financial system stability mechanisms address energy price shock mitigation through strategic reserves, flexible generation capacity, and international cooperation frameworks. These integrated approaches ensure that climate transition enhances rather than undermines overall China energy security objectives.

Investment Frameworks and Capital Allocation

Multi-trillion yuan investment pipelines support renewable infrastructure development across solar, wind, and hydroelectric generation capacity. Grid modernisation receives substantial capital allocation for transmission and distribution upgrades necessary to accommodate distributed renewable generation and electric vehicle charging infrastructure.

Strategic reserve expansion includes both traditional petroleum stockpiles and next-generation energy storage systems. Emergency stockpile capacity increases provide buffer against supply disruptions whilst battery and hydrogen storage facilities support grid stability and renewable energy integration.

Risk Management Portfolio Approach

Geographic diversification strategies balance supplier relationships across multiple regions whilst technology hedging maintains parallel investment in fossil and renewable energy infrastructure. Diplomatic relationship energy components integrate Belt and Road Initiative projects with bilateral supply agreements and technology transfer partnerships.

Multi-variable risk assessment systems enable scenario planning across different disruption possibilities, from temporary supply interruptions to permanent shifts in global energy markets. Policy flexibility mechanisms provide rapid response capabilities during crisis periods whilst maintaining long-term strategic direction.

Comparative Global Energy Security Analysis

China energy security position demonstrates both vulnerabilities and advantages relative to other major economies. Import dependency ratios exceed those of the United States and Russia but compare favourably to Japan and South Korea, which lack significant domestic production capacity and maintain smaller strategic reserves.

Strategic reserve capacity rankings place China among the top three globally in absolute terms, though per-capita metrics remain moderate. Renewable transition speed leadership provides competitive advantages in clean technology manufacturing whilst reducing long-term fossil fuel import requirements.

Manufacturing scale benefits enable cost leadership in solar panels, wind turbines, and battery systems, creating economic advantages that support both domestic energy security and export competitiveness. Resource access through Belt and Road Initiative energy projects expands supplier diversity whilst technology innovation capacity supports next-generation energy system development.

Future Risk Scenarios and Adaptive Strategies

Multiple chokepoint closure scenarios require simultaneous disruption of Persian Gulf terminals, alternative shipping routes, and overland pipeline systems. Such comprehensive supply disruption would necessitate unprecedented inventory draw-down combined with emergency demand management measures including industrial curtailment and transportation restrictions.

Technology sanctions escalation represents an emerging vulnerability as clean energy component restrictions could slow renewable deployment and grid modernisation programmes. Climate transition acceleration creates stranded asset risks in conventional energy infrastructure whilst potentially disrupting established supply relationships.

Strategic Resilience Mechanisms

Scenario planning protocols incorporate multi-variable analysis of simultaneous risks across geographic, technological, and political dimensions. Rapid response capability development includes pre-positioned alternative supply agreements, emergency production capacity, and conservation measures deployable within weeks rather than months.

International cooperation expansion through multilateral energy security partnerships provides mutual assistance frameworks during crisis periods whilst technology sharing agreements accelerate innovation in energy storage, grid management, and renewable generation efficiency. According to the World Energy Investment 2024 report on China, sustained investment flows continue supporting these strategic objectives.

The integration of short-term supply security with long-term transformation objectives positions China energy security architecture for sustained resilience across multiple risk scenarios. Strategic continuity in diversification investments, combined with technological innovation priorities and international partnership development, creates comprehensive energy security capabilities extending well beyond traditional supply chain management approaches.

This analysis incorporates insights from energy market specialists and reflects current understanding of China energy security developments as of 2026. Readers should consult established energy research institutions for ongoing coverage of Asian energy markets and geopolitical risk assessment.

Ready to Capitalise on China's Energy Transition Opportunities?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, including critical minerals essential to China's renewable energy infrastructure development. Access immediate insights into actionable trading opportunities within the lithium, cobalt, and rare earth sectors that underpin global energy security transformations through Discovery Alert's discoveries page, and begin your 14-day free trial today at discoveryalert.com.au.