June 21, 2026

The Hidden Architecture of Mineral Power: Why What Happens Between China and Japan Reshapes Every Supply Chain on Earth

Most commodity markets move on the logic of price, volume, and demand cycles. Critical mineral markets, however, increasingly move on something far less predictable: the decision-making of a single dominant processor operating within a geopolitical framework that treats raw material flows as instruments of statecraft. Understanding why China cuts Japan off from heavy rare earths requires stepping back from the bilateral dispute itself and examining the structural architecture that made this moment not just possible, but arguably inevitable.

The current situation between Beijing and Tokyo is not simply a trade disagreement. It is a live demonstration of what supply chain concentration looks like when diplomatic relationships deteriorate, and it carries lessons that extend well beyond Japan's borders.

When big ASX news breaks, our subscribers know first

Understanding Heavy Rare Earths: Why the Distinction Matters Enormously

The rare earth elements are frequently discussed as a single category, but this framing obscures a critical internal division. The 17 rare earth elements split broadly into two groups: light rare earth elements (LREEs) and heavy rare earth elements (HREEs). While both matter industrially, the HREE category carries disproportionate strategic weight relative to its production volume.

The materials at the centre of the current Japan supply disruption illustrate why:

- Dysprosium functions as a thermal stabiliser in neodymium-iron-boron (NdFeB) permanent magnets. Without dysprosium additions, these magnets lose their magnetic strength at the elevated operating temperatures found in EV drive motors and military guidance systems. There is no commercially viable substitute performing the same function at scale.

- Terbium enhances magnet coercivity at high temperatures, enabling performance in aerospace hardware and advanced military applications. Like dysprosium, it is incorporated into NdFeB magnets through a technique called grain boundary diffusion, which minimises the quantity required while preserving performance.

- Yttrium oxide underpins advanced ceramics, phosphor materials used in displays and lighting, and laser applications. Its industrial footprint is broad and not easily consolidated onto a single replacement material.

- Gallium, while technically a minor metal rather than a rare earth, has been bundled into the same export control framework. It is essential for compound semiconductors, specifically gallium arsenide and gallium nitride, which form the basis of 5G infrastructure, radar systems, and high-efficiency solar cells.

What makes this group particularly difficult to substitute is not scarcity in the geological sense. These elements exist in the Earth's crust in commercially workable concentrations in multiple locations globally. The barrier is processing complexity. Rare earth processing challenges are chemically demanding, capital-intensive, and require decades of accumulated industrial expertise. This is why controlling separation and refining infrastructure creates leverage that ore mining alone cannot replicate. Furthermore, understanding the broader rare earth processing challenges makes clear why this structural bottleneck persists.

The Processing Dominance Problem: Where the Real Chokepoint Lives

| Material | China's Estimated Share of Global Processing | Primary End-Use Sectors |

|---|---|---|

| Dysprosium | ~90%+ | EV motors, defence magnets |

| Terbium | ~90%+ | Aerospace, military hardware |

| Yttrium | ~70-80% | Ceramics, phosphors, lasers |

| Gallium | ~80%+ | Semiconductors, 5G, radar |

"The fundamental vulnerability is not that China mines most of these materials. It is that China processes most of them. An ore body in Australia or Canada does not become a usable industrial input until it passes through separation and refining. Controlling that step means controlling access to the final product, regardless of where the raw ore originates."

This architectural reality is what allows Beijing to activate export controls with an immediacy that alternative supply chains simply cannot match. Building a new separation facility takes years of permitting, construction, commissioning, and operational refinement. Signing an export control order, however, takes considerably less time.

From Diplomatic Friction to Supply Shutdown: The Timeline That Changed Everything

The sequence of events leading to the current supply halt followed a clear escalatory logic:

- November 2025: A diplomatic dispute erupts between Beijing and Tokyo rooted in Japan's public positioning on Taiwan. The fault line had been developing for months before it crystallised into a formal breakdown in bilateral relations.

- December 2025: Chinese exports of dysprosium, terbium, yttrium oxide, and gallium to Japan effectively cease. Chinese customs data confirms the halt, with only negligible yttrium shipments recorded as exceptions over the subsequent months.

- January 2026: Beijing formally tightens export controls targeting Japan within a codified regulatory framework, moving the restriction from apparent policy practice to explicit legal architecture.

- February 2026: Two additional rounds of export control tightening follow in rapid succession. Notably, these controls specifically name major Japanese industrial conglomerates, including the shipbuilding and aero engine divisions of Mitsubishi Heavy Industries, representing a precision escalation targeting defence-adjacent industrial capacity.

- May 2026: Japan's Trade Minister Ryosei Akazawa travels to Beijing for meetings, becoming the most senior Japanese official to engage China directly since the dispute began, signalling Tokyo's recognition that diplomatic resolution may need to run parallel to any supply chain mitigation strategy.

2010 vs 2026: Two Pressure Campaigns, Very Different Architectures

The 2010 Senkaku/Diaoyu fishing boat incident triggered a notable slowdown in Chinese rare earth exports to Japan that permanently altered how governments and industries thought about supply chain vulnerability. The rare earth supply chain importance was firmly established during this period. The 2026 episode shares surface similarities but differs in several structurally important ways:

| Dimension | 2010 Dispute | 2026 Export Freeze |

|---|---|---|

| Trigger | Senkaku/Diaoyu fishing vessel incident | Taiwan-related diplomatic tensions |

| Materials targeted | Broad rare earth category | HREEs plus gallium; named conglomerates targeted |

| Duration at reporting | Weeks to months | 4+ months and continuing |

| Japan's preparedness | Low | Moderate; stockpiles built post-2010 |

| Legal mechanism | Informal and contested | Formally codified regulatory framework |

| Geopolitical context | Bilateral dispute | Embedded in wider US-China trade conflict |

For further historical context on the 2010 China-Japan rare earths dispute, the shift to a formalised, legally grounded export control apparatus in 2026 is particularly significant. It indicates that Beijing has developed a mature instrument capable of being deployed with precision against specific countries and companies. This is qualitatively different from informal export throttling and signals a permanent upgrade in China's toolkit for economic statecraft.

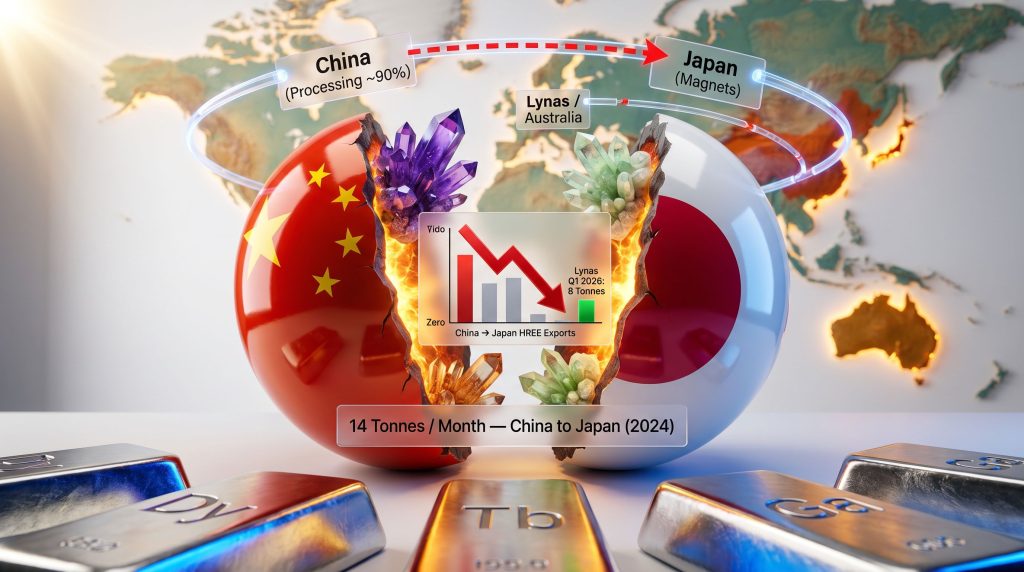

Quantifying the Gap: What the Production Numbers Actually Reveal

No single data point better illustrates the scale of the supply challenge than the comparison between what China was shipping to Japan and what the rest of the world can currently produce.

In the first quarter of 2026, Lynas Rare Earths, the world's first commercial producer of separated terbium and dysprosium outside China, produced 8 tonnes of those two materials combined. In 2024, China was exporting approximately 14 tonnes per month of the same materials to Japan alone.

"To put that in perspective: China's monthly dysprosium and terbium exports to a single customer country exceeded the entire quarterly output of the world's leading alternative producer by a factor of more than 20 on a monthly basis. This is the structural reality that makes near-term replacement of Chinese HREE supply not just difficult but functionally impossible within any compressed timeframe."

Lynas, which operates processing facilities in Malaysia with additional infrastructure in development in Australia and France, has also launched a gallium project in Australia. Japan has provided financial backing to Lynas as part of a deliberate long-term supply diversification strategy. However, as researchers at Project Blue have noted, replacing Chinese HREE supply at meaningful scale is a multi-year endeavour requiring sustained capital commitment and continued operational scaling.

How Japan's Industrial Base Is Absorbing the Shock

The impact of the export freeze is unevenly distributed across Japan's industrial landscape. The sectors most exposed share a common characteristic: deep dependence on HREE-containing components with limited near-term substitution pathways.

Industries facing the greatest immediate pressure:

- Rare earth magnet manufacturing: Japan is the world's largest producer of rare earth magnets outside China. Major producer Shin-Etsu has reportedly halted acceptance of new orders for dysprosium-containing magnets, a direct operational response to input supply constraints that signals downstream disruption is already propagating through the supply chain.

- Automotive and EV production: NdFeB magnets enhanced with dysprosium are embedded in the drive motors of electric and hybrid vehicles. Mitsubishi Motors disclosed in February 2026 that it had secured rare earth supply only through mid-year, creating visible forward uncertainty in its production planning.

- Semiconductor and electronics manufacturing: Gallium restrictions directly affect compound semiconductor production pipelines serving consumer electronics, telecommunications, and defence electronics manufacturers.

- Defence and aerospace: The explicit naming of Mitsubishi Heavy Industries' aero engine and shipbuilding divisions in Beijing's targeted controls introduces supply chain risk into Japan's defence industrial base in a manner that carries strategic implications beyond commercial disruption.

What Buffers Exist and Where They Fall Short

Japan entered this episode meaningfully better prepared than it was in 2010, though not sufficiently insulated to absorb a sustained total halt. In addition, the critical minerals demand surge has further complicated the supply picture globally. Key buffers include:

- Strategic stockpiles built following the 2010 experience have provided a buffer. Japan's industry ministry has confirmed that stockpile releases are occurring where necessary, though precise quantities remain undisclosed for strategic reasons.

- Reduced HREE intensity in magnet manufacturing has been achieved through grain boundary diffusion techniques, which allow manufacturers to use less dysprosium per magnet while maintaining performance specifications. This reduces but does not eliminate dependency.

- Import diversification has lowered Japan's dependence on Chinese rare earth imports from roughly 90% around 2010 to approximately 60% by the mid-2020s, according to World Economic Forum estimates. This improvement is real but insufficient to absorb a complete export halt from the dominant supplier.

- Component maker resilience: TDK Corporation has indicated it does not currently anticipate major near-term impact and is actively working to diversify its supply base, suggesting varying levels of preparedness across the manufacturing ecosystem.

Notably, China continues to export finished rare earth magnets to Japan and global markets at normal volumes. This detail deserves careful attention: Beijing appears to be targeting raw material inputs rather than downstream manufactured products, which likely reflects its own commercial interest in maintaining magnet export revenue while simultaneously pressuring Japan's domestic magnet manufacturing capacity.

The Broader Strategic Logic: Precision Coercion and the New Mineral Weapon

The Japan episode fits within a wider pattern that represents a fundamental evolution in how resource concentration translates into geopolitical leverage. China's rare earth export restrictions have, consequently, become one of the most closely watched policy instruments in global trade.

Three structural realities have now been empirically demonstrated by the current situation:

- Processing dominance creates faster-acting leverage than mining dominance. The ability to restrict access to separated, refined materials can be exercised almost immediately. Building replacement processing capacity takes years. This asymmetry is the core of China's strategic advantage in critical minerals.

- Export controls can be deployed with surgical precision. The targeting of named corporate divisions, rather than broad industry categories, demonstrates a level of policy sophistication that moves beyond blunt economic pressure toward targeted disruption of specific industrial capabilities, particularly those with defence relevance.

- Geopolitical risk now structurally reprices critical mineral investment. The episode reinforces that HREE supply chains cannot be evaluated purely on commercial fundamentals. Political risk premiums are permanent features of any investment or procurement decision involving Chinese-processed materials.

The parallel with China's rare earth trade strategy toward the United States during the ongoing trade conflict is not incidental. It reflects a coherent strategic framework in which critical mineral access functions as a lever across multiple geopolitical fronts simultaneously.

The next major ASX story will hit our subscribers first

The Path to Resilience: What Actually Needs to Happen

Closing the gap between current alternative supply capacity and the scale of Chinese HREE exports requires progress across multiple dimensions simultaneously. No single intervention is sufficient.

Five structural levers that must be activated in parallel:

- Prioritise separation and refining investment over mining investment. The bottleneck is not ore in the ground. It is the infrastructure to convert ore into separated, usable material. Capital allocation needs to reflect this reality.

- Expand strategic stockpile depth for defence-critical materials. Government reserves need to cover disruption windows measured in years, not months, particularly for dysprosium and terbium given their irreplaceable role in defence magnet applications.

- Scale rare earth recycling and urban mining programmes. Recovering HREEs from end-of-life EV motors, wind turbines, and industrial magnets reduces primary supply dependency and creates a partially China-independent feedstock stream over time.

- Accelerate magnet design innovation. Continued development of reduced-HREE or HREE-free permanent magnet formulations represents the most durable long-term solution, though timelines to commercial scale remain uncertain.

- Build allied supply chain coordination frameworks. Bilateral and multilateral arrangements linking Japan, Australia, the EU, the United States, and Canada can create distributed processing capacity that no single country can blockade simultaneously.

Current trajectory analysis suggests that meaningful, scaled alternative HREE supply is a 5 to 10-year horizon under optimistic assumptions. Near-term mitigation relies on stockpile drawdowns, demand reduction in the most HREE-intensive applications, and partial substitution where technically feasible. The Japan situation makes clear that the window of vulnerability is open now and that diplomatic normalisation remains a near-term variable that supply chain diversification alone cannot replace.

Moreover, China's rare earth export restrictions serve as a stark reminder that this challenge is not unique to Japan. Any nation whose industrial base depends on Chinese-processed HREEs faces structurally similar risks should its diplomatic relationship with Beijing deteriorate.

This article is intended for informational purposes only and does not constitute financial or investment advice. Forward-looking statements regarding supply timelines, geopolitical outcomes, and market developments involve inherent uncertainty and should not be relied upon as predictions of future events.

Frequently Asked Questions: China Cuts Japan Off From Heavy Rare Earths

What specific materials has China stopped exporting to Japan?

Chinese customs data confirms that exports of dysprosium, terbium, yttrium oxide, and gallium to Japan have effectively halted since December 2025, with only minimal yttrium shipments recorded as exceptions in the months that followed.

Why are dysprosium and terbium so critical to Japan's industrial base?

Japan is the largest producer of rare earth permanent magnets outside China. Dysprosium and terbium are essential additives that allow NdFeB magnets to maintain magnetic performance at elevated operating temperatures, a non-negotiable requirement for EV drive motors, wind turbine generators, and military guidance systems. No commercially viable substitute currently performs this function at scale.

How does the 2026 situation compare to the 2010 rare earth dispute?

The 2026 restrictions are more formally codified, more precisely targeted, and embedded within a broader geopolitical context involving simultaneous US-China trade tensions. Japan is better prepared than in 2010 due to stockpile building and diversification investment over the intervening years, though not sufficiently so to absorb a total halt in HREE supply indefinitely.

How dependent is Japan on Chinese rare earths today?

Japan's dependence on Chinese rare earth imports has declined from approximately 90% around 2010 to roughly 60% by the mid-2020s, according to World Economic Forum estimates. This improvement reflects stockpiling, diversification investment, and reduced material intensity in manufacturing but remains insufficient to absorb a complete export shutdown from the dominant supplier.

Can alternative producers replace Chinese HREE supply in the near term?

Not at meaningful scale. Lynas Rare Earths produced 8 tonnes of dysprosium and terbium combined in the first quarter of 2026. China was exporting approximately 14 tonnes of those same materials to Japan alone every month in 2024. The production gap is large and cannot be closed on a short timeline.

What is Japan currently doing to manage the supply disruption?

Japan has confirmed stockpile releases where necessary, has provided financial backing to alternative producers including Lynas Rare Earths, and its Trade Minister engaged Beijing directly in May 2026. Japanese manufacturers are accelerating supply diversification efforts, reducing HREE intensity in product designs where technically feasible, and in some cases pausing acceptance of new orders for HREE-dependent products.

For further reporting on rare earth supply chain developments and the evolving geopolitics of critical minerals, Mining Weekly at miningweekly.com provides ongoing coverage across global markets.

Want to Stay Ahead of the Next Major Critical Minerals Discovery?

As geopolitical pressures reshape critical mineral supply chains, Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries — including rare earths and strategic commodities — and delivering actionable insights directly to subscribers. Explore historic examples of what major mineral discoveries can return and start your 14-day free trial today to position yourself ahead of the market.