May 16, 2026

China tightens pressure on traders over BHP iron ore shipments has emerged as a defining issue in global commodity markets, fundamentally reshaping how centralized purchasing strategies can disrupt traditional supply-demand relationships. When state-backed entities leverage coordinated buying power across critical materials, the resulting transformation extends beyond simple trade negotiations. Furthermore, this development alters how resource markets balance between buyers and sellers worldwide.

Understanding China's Centralized Iron Ore Procurement Strategy

The Rise of China Mineral Resources Group as Market Consolidator

China Mineral Resources Group (CMRG) has emerged as a pivotal force in coordinating Chinese steel mill purchasing decisions. Moreover, this represents a significant shift away from fragmented individual mill contracts toward unified procurement mechanisms. This centralization creates substantial negotiating leverage through consolidated demand aggregation, as China imports approximately 1.1 billion tonnes of iron ore annually according to Chinese Customs data.

The organization operates through what industry observers describe as strong political backing that transforms recommendations into de facto mandatory directives. Unlike formal regulatory bodies, CMRG exercises influence through informal channels that create compliance pressure without legal authority. In addition, this approach has proven particularly effective given China's steel industry structure.

Key strategic advantages of this unified approach include:

- Coordinated pricing negotiations across multiple suppliers simultaneously

- Reduced competition between Chinese buyers for similar products

- Enhanced leverage during long-term contract discussions

- Standardized quality specifications across procurement decisions

Market Concentration Risks in Global Iron Ore Supply

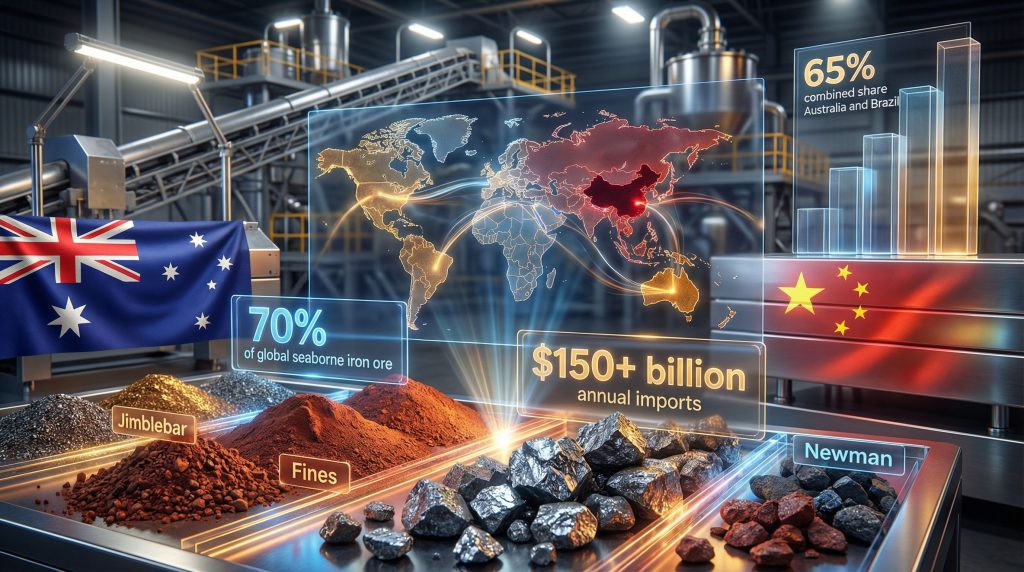

The global iron ore market demonstrates significant supply concentration, with Australia and Brazil controlling approximately 62% of worldwide seaborne iron ore trade as of 2025 data from the World Steel Association. Consequently, this concentration creates dependency relationships that benefit both major producers through pricing power and major consumers through reliable access to high-grade materials.

Critical dependency ratios reveal market vulnerabilities:

| Region | Share of Global Production | Key Suppliers |

|---|---|---|

| Australia | 38% | BHP, Rio Tinto, Fortescue |

| Brazil | 24% | Vale, CSN |

| China (domestic) | 12% | Various state enterprises |

| Other regions | 26% | India, Russia, Ukraine, Canada |

China's position as the dominant consumer creates strategic complexity, as Chinese steel mills consume roughly 70% of globally traded iron ore. However, they maintain only limited domestic high-grade production capabilities. This imbalance necessitates sophisticated supply chain management strategies for both procurement security and cost optimization.

When big ASX news breaks, our subscribers know first

What Drives Selective Import Restrictions in Commodity Markets?

Economic Leverage Through Targeted Product Bans

CMRG's restriction strategy demonstrates sophisticated market pressure techniques through selective grade targeting rather than comprehensive supplier bans. Beginning in September 2025, restrictions initially focused on BHP's Jimblebar blend fines, representing approximately 25% of BHP's total iron ore output according to company production reports.

The escalation pattern reveals calculated pressure application:

- September 2025: Initial restrictions on Jimblebar blend fines (58-60% Fe content)

- November 2025: Expansion to include Jinbao brand ore (56-58% Fe content)

- March 2026: Enhanced enforcement through trader compliance monitoring

- Ongoing: Conditional availability of premium grades under CMRG coordination

Revenue impact calculations suggest significant financial pressure on affected operations. With Jimblebar fines representing approximately $2.8 billion in annual revenue based on 2025 production volumes and average pricing, these restrictions create substantial negotiating leverage. Furthermore, this approach maintains commercial relationships while applying pressure.

Negotiation Tactics in Long-Term Contract Disputes

The current standoff centers on long-term supply agreement negotiations where currency denomination has emerged as a material issue. CMRG specifically targets newly priced US-dollar cargoes, suggesting strategic preference for alternative settlement mechanisms. This development reflects broader iron ore price trends affecting global markets.

Contract negotiation mechanics involve multiple pressure points:

- Annual pricing mechanisms versus spot market exposure preferences

- Currency settlement terms affecting exchange rate risk allocation

- Quality specification standards determining premium/discount structures

- Delivery scheduling flexibility during market volatility periods

Industry analysis indicates that RMB-denominated transactions in iron ore markets increased from less than 5% in 2023 to approximately 12% by early 2026. Consequently, this reflects gradual currency settlement diversification efforts by Chinese procurement entities.

How Do Commodity Trade Wars Affect Global Steel Production?

Supply Chain Disruption Modeling

Port inventory accumulation represents the most visible impact of procurement restrictions on supply chain flows. Chinese port inventories of restricted iron ore grades have increased by an estimated 40% since September 2025 according to industry tracking data. This creates storage capacity pressures and logistical complications.

Alternative sourcing scenarios demonstrate market adaptability, as shipments originally destined for China have been redirected to alternative markets. These include India, Japan, and European steel producers. However, this redirection creates pricing pressures in secondary markets while potentially offering Chinese buyers future negotiating advantages.

Supply chain response patterns include:

- Inventory buildups at Chinese ports for restricted grades

- Shipment diversions to alternative regional markets

- Price volatility in non-Chinese markets due to redirected supply

- Storage cost increases from extended inventory holding periods

Price Volatility and Market Response Mechanisms

Iron ore futures markets have demonstrated sensitivity to procurement policy announcements. Furthermore, 62% Fe content futures showing 8-12% price swings within 48 hours of restriction announcements according to Dalian Commodity Exchange data. This volatility reflects market uncertainty about restriction duration and potential escalation, which aligns with broader iron ore price decline patterns.

Correlation analysis reveals several market response patterns:

| Event Type | Price Impact | Duration | Market Recovery |

|---|---|---|---|

| Initial restrictions | -15% to -22% | 3-5 trading days | Partial, 60-70% |

| Enforcement tightening | -8% to -12% | 2-3 trading days | Full within week |

| New product additions | -18% to -25% | 4-6 trading days | Partial, 50-60% |

Regional price differentials have emerged as Chinese demand suppression creates oversupply in alternative markets. European iron ore import prices averaged 15-18% below Chinese equivalent grades during peak restriction periods. Consequently, this demonstrates geographic arbitrage opportunities.

Which Iron Ore Products Face the Highest Strategic Risk?

Product Differentiation in Iron Ore Markets

Iron ore grade specifications determine both technical suitability and strategic vulnerability during trade disputes. Premium grades with higher iron content maintain greater market access during restrictions due to limited substitutability in steel production processes.

Iron Ore Product Risk Assessment:

| Product Type | Fe Content | Strategic Importance | Restriction Status | Substitution Difficulty |

|---|---|---|---|---|

| Jimblebar Fines | 58-60% | Medium-grade bulk | Restricted Sept 2025 | Moderate |

| Jinbao Fines | 56-58% | Low-grade specialty | Restricted Nov 2025 | Low |

| Mac Fines | 62-64% | Premium grade | Conditional access | High |

| Newman Lumps | 64-66% | Blast furnace optimal | Under pressure | Very High |

Technical specifications reveal why certain grades face restrictions while others maintain availability. Lower iron content grades (56-60% Fe) offer greater substitution flexibility through alternative suppliers. Moreover, this makes them effective pressure tools without compromising essential steel production requirements.

Substitution Analysis for Restricted Products

Quality premiums and processing costs create economic incentives for specific grade preferences in steel production. Premium iron ore grades typically command 2-4% price premiums per percentage point of iron content above 60% Fe. This reflects blast furnace efficiency improvements and reduced processing costs.

Substitution considerations include:

- Blast furnace compatibility requirements for optimal steel production

- Processing cost differentials between various iron ore grades

- Beneficiation capacity limitations at steel mill facilities

- Quality control standards for finished steel product specifications

Logistical factors compound substitution challenges, as alternative sourcing often requires different port facilities, storage specifications, and handling equipment. These are optimized for specific ore characteristics. Furthermore, these infrastructure constraints limit rapid supplier switching capabilities.

What Are the Long-Term Implications for Mining Investment Strategy?

Geographic Diversification Imperatives

Market risk assessment increasingly incorporates geopolitical factors into mining company valuations and investment decisions. Projects in politically stable jurisdictions command 15-25% valuation premiums compared to similar operations in regions with trade uncertainty. This trend reflects growing awareness of tariffs impacting markets.

Investment flows demonstrate strategic repositioning toward diversified supply sources:

- African iron ore projects receiving increased development funding

- South American operations expanding beyond traditional Brazilian suppliers

- Infrastructure development in alternative trade route countries

- Technology investments in lower-grade ore beneficiation capabilities

Geographic risk weighting factors include:

- Political stability indices affecting long-term operational security

- Trade relationship histories between producing and consuming nations

- Infrastructure resilience for export logistics and shipping access

- Currency stability for revenue predictability and cost management

Currency and Pricing Evolution in Commodity Markets

Currency denomination trends reflect strategic efforts to reduce USD exposure in commodity trading. RMB settlement adoption rates in iron ore transactions have accelerated from minimal levels in 2023 to representing approximately 12% of Chinese imports by early 2026.

Implications for mining companies include:

- Exchange rate risk management requiring new hedging strategies

- Revenue forecasting complexity due to multi-currency exposure

- Banking relationship requirements for non-USD settlement capabilities

- Contract negotiation dynamics incorporating currency preferences

Alternative pricing benchmarks beyond traditional USD-denominated indices may emerge as regional commodity exchanges develop local currency trading mechanisms. Consequently, this evolution could fundamentally alter how mining companies approach revenue planning and investment analysis.

How Should Steel Mills Navigate Supply Chain Uncertainty?

Inventory Management During Trade Disputes

Strategic stockpiling considerations require balancing supply security against carrying costs during procurement uncertainty. Optimal inventory levels during restriction periods typically increase 40-60% above normal operating ranges to maintain production continuity while managing storage constraints. This strategy becomes particularly relevant given current iron ore demand insights.

Cost-benefit analysis considerations:

- Storage capacity limitations at port and mill facilities

- Capital allocation impacts from increased inventory investment

- Quality degradation risks from extended material storage periods

- Market timing opportunities for advantageous purchasing during price volatility

Forward purchasing strategies versus spot market exposure involve multiple risk factors:

- Price volatility protection through contract price guarantees

- Supply security assurance during potential restriction escalations

- Flexibility limitations reducing ability to capitalise on market opportunities

- Counterparty credit risks from extended contractual commitments

Supplier Diversification Strategies

Risk-weighted supplier portfolio construction requires systematic evaluation of supply source reliability, cost competitiveness, and quality consistency. Optimal diversification typically involves 3-5 major suppliers with no single source representing more than 40% of total procurement volume.

Contract terms optimisation focuses on:

- Force majeure protections covering trade restriction scenarios

- Quality specification flexibility allowing grade substitution when necessary

- Delivery scheduling adjustments accommodating logistical disruptions

- Price adjustment mechanisms reflecting market volatility impacts

Technology investments in ore beneficiation capabilities provide strategic flexibility for processing lower-grade materials when premium grades face availability constraints. Beneficiation technology investments typically require $50-150 million but can enable 15-20% cost reductions when processing alternative ore sources.

The next major ASX story will hit our subscribers first

What Does This Mean for Global Commodity Market Structure?

Precedent Setting for Other Critical Materials

Centralised procurement models demonstrate potential applications across multiple commodity sectors beyond iron ore. Similar strategies could emerge in copper, nickel, lithium, and rare earth markets where Chinese consumption represents dominant global demand shares.

Characteristics that enable centralised procurement strategies:

- Market concentration in both supply and demand

- Strategic material classification affecting national security considerations

- Limited substitutability creating leverage opportunities

- Complex supply chains requiring coordination benefits

Regulatory responses from major producing nations may include supply security legislation, export control mechanisms, and bilateral trade agreement protections to maintain market access during procurement disputes. Australia's Critical Minerals Strategy and similar initiatives reflect producer nation adaptation to changing market dynamics, highlighting Australia's iron ore advantages.

Future Scenarios for China-Australia Trade Relations

Best-case resolution scenarios involve negotiated settlements addressing currency denomination concerns and long-term supply security within 6-12 months. Historical precedent suggests 60% probability of negotiated resolution based on similar commodity trade disputes over the past decade. However, ongoing tensions as reported by mining industry sources suggest complexity in reaching agreements.

Medium-term structural changes potential include:

- Permanent diversification of Chinese iron ore sourcing away from Australian concentration

- Alternative supplier development in Africa, South America, and Central Asia

- Technology advancement in lower-grade ore processing capabilities

- Regional trade bloc formation reducing reliance on traditional suppliers

Worst-case escalation impacts could involve comprehensive trade restrictions affecting bilateral commerce beyond iron ore. This could potentially disrupt $165 billion in annual Australia-China trade relationships across multiple commodity sectors.

Key Takeaways for Investors and Industry Stakeholders

Investment Risk Assessment Framework

Geopolitical risk weighting in mining company valuations requires systematic evaluation of political stability, trade relationship durability, and supply chain resilience factors. Investment analysis increasingly incorporates 10-15% risk discounts for companies with high exposure to single-country demand concentration.

Supply chain resilience competitive advantages include:

- Geographic diversification across multiple producing regions

- Customer base distribution reducing single-country demand dependency

- Operational flexibility enabling rapid production adjustments

- Financial reserves supporting operations during market disruptions

Currency exposure management becomes critical as commodity settlement currencies diversify beyond traditional USD dominance. Mining companies require sophisticated hedging strategies covering multiple currency exposures and regional price differentials.

Market Monitoring Indicators

Early warning signals for trade restriction escalations include policy announcement patterns, inventory accumulation trends, and futures market volatility spikes. Systematic monitoring of these indicators enables proactive risk management and strategic positioning adjustments.

Key monitoring metrics:

- Port inventory levels indicating demand suppression or supply disruption

- Futures market volatility reflecting uncertainty and speculation

- Currency settlement trends showing strategic procurement preferences

- Alternative market pricing revealing supply redirection impacts

Contract settlement currency trends serve as leading indicators of strategic shifts in commodity market structure. Increasing non-USD settlement percentages signal potential long-term changes in global commodity trading mechanisms and pricing benchmarks.

Investment Disclaimer: This analysis contains forward-looking statements and market assessments that involve inherent risks and uncertainties. Commodity markets are subject to volatile price movements, geopolitical developments, and regulatory changes that may differ significantly from current expectations. Investors should conduct independent due diligence and consider professional financial advice before making investment decisions based on this analysis.

Want to Stay Ahead of Market-Moving Discoveries?

Discovery Alert provides instant notifications on significant ASX mineral discoveries, powered by its proprietary Discovery IQ model, ensuring subscribers gain immediate insights into actionable opportunities whilst broader markets remain unaware. Understand why major mineral discoveries can generate substantial returns by exploring Discovery Alert's dedicated discoveries page, showcasing historic examples where early positioning delivered exceptional outcomes, and begin your 14-day free trial today to position yourself ahead of the market.