May 16, 2026

When Commodity Markets Price Uncertainty as a Cost

Global energy markets have always been vulnerable to geopolitical shock, but there is a meaningful difference between markets that price expensive supply and markets that price uncertain supply. The former creates economic pain. The latter creates systemic paralysis. When refiners cannot predict whether a cargo will clear customs, whether a tanker can obtain war-risk coverage, or whether a payment route will survive regulatory scrutiny, the entire commercial planning process breaks down. That breakdown, not crude oil's nominal price, is the central energy-security challenge confronting the Trump administration as Gulf conflict reshapes global oil flows in 2026.

Understanding how to help Trump win the oil curve requires examining not just barrel counts, but the full ecosystem of logistics, finance, insurance, and legal clarity that transforms oil in the ground into usable fuel at a refinery gate. Furthermore, the trade war economic impact on global supply chains amplifies every layer of this challenge, making policy precision more critical than ever.

When big ASX news breaks, our subscribers know first

The Inventory Picture Is Not What It Appears

A Mislocation Problem Disguised as a Shortage

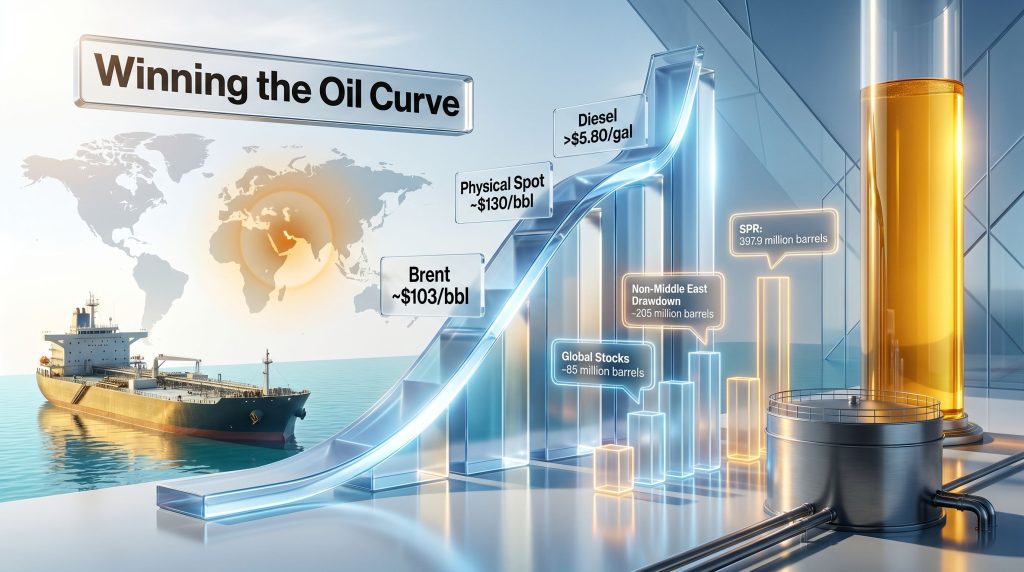

The headline inventory figures from the International Energy Agency's April 2026 Oil Market Report are alarming on the surface. Global observed oil inventories fell by 85 million barrels in March 2026. However, the composition of that number reveals something more nuanced than a simple supply shortfall.

Stocks outside the Middle East Gulf region drew down by 205 million barrels, equivalent to approximately 6.6 million barrels per day, as Strait of Hormuz transit flows were severely curtailed. Meanwhile, at the very same time:

- Floating crude storage in the Middle East region increased by 100 million barrels

- Onshore crude stocks within the region rose by an additional 20 million barrels

- China added 40 million barrels to its strategic petroleum holdings

| Region | Inventory Change (March 2026) |

|---|---|

| Global observed stocks | -85 million barrels |

| Non-Middle East Gulf stocks | -205 million barrels (-6.6 mb/d) |

| Middle East floating storage | +100 million barrels |

| Middle East onshore crude | +20 million barrels |

| China strategic additions | +40 million barrels |

The world did not simply run out of crude. Barrels became geographically trapped, legally uncertain, commercially uninsurable, or financially impractical to move. Oil sitting in floating storage that cannot obtain war-risk insurance does not function as tradeable supply. Oil that cannot be processed through a letter of credit arrangement does not reach a refinery.

The inventory crisis is, at its core, a logistics, legal clarity, and confidence problem layered on top of a genuine production disruption. This distinction is critical for policymakers because it changes the solution set entirely.

Two Price Layers: Scarcity Premium vs. Panic Premium

How the Futures Curve Became the Real Battlefield

Crude oil markets are currently carrying two distinct valuation components that analysts and trading desks are treating very differently. The first is a genuine scarcity premium reflecting actual reduced supply flow. The second is a panic premium reflecting uncertainty about whether physically available barrels can actually be lifted, insured, financed, shipped, and settled without each step in the chain demanding a wartime surcharge.

The divergence between physical and paper markets has become extreme. According to the IEA's April 2026 report, North Sea Dated crude was trading around $130 per barrel at the time of publication, roughly $60 per barrel above pre-conflict levels. Physical crude prices had surged toward $150 per barrel in spot markets. Middle distillate prices in Singapore reached record highs above $290 per barrel. These figures reflect the physical-paper disconnect at its most acute. For further context, reviewing the crude oil price trends in the lead-up to this period helps illustrate just how rapidly conditions deteriorated.

The U.S. Energy Information Administration's April 2026 Short-Term Energy Outlook provided its own quantification of the disruption:

| Benchmark | EIA April 2026 Forecast |

|---|---|

| Brent crude average (March 2026) | ~$103/bbl |

| Brent crude peak (Q2 2026) | ~$115/bbl |

| U.S. retail gasoline peak | ~$4.30/gal (April 2026) |

| U.S. diesel price peak | >$5.80/gal |

| U.S. diesel inventories | Below five-year average |

The EIA explicitly noted that its forecast is contingent on the duration of the Middle East conflict and the pace at which production outages resolve. This transforms the standard supply-demand price model into something closer to a war-duration probability model.

Why Diplomatic Language Now Functions as an Oil Market Instrument

One of the lesser-understood dynamics of the current environment is how rapidly geopolitical trade tensions move physical commodity markets. Brent crude briefly traded below $100 per barrel intraday following reports of a potential U.S.-Iran peace framework, before recovering as uncertainty returned. Oil prices also moved toward approximately $106.10 per barrel in response to attention shifting toward a Trump-Xi diplomatic meeting, demonstrating that broader U.S.-China relations are now embedded in crude pricing independently of Middle East military dynamics.

Every presidential statement, Pentagon briefing, and sanctions announcement now functions as a de facto market instrument. This is not metaphorical. It reflects the mathematical reality that futures markets price probabilities, and authoritative statements from Washington directly alter the probability distribution that underlies every forward curve month.

Strategic ambiguity may serve certain military objectives, but in commodity markets, ambiguity is directly priced as an operating cost. Precision in communication is not a diplomatic courtesy; it is an energy-security tool.

Eight Policy Levers for Winning the Oil Curve

1. A Daily Energy-Security Operating Dashboard

Markets generate risk premiums wherever verified data is absent. Silence and contradictory signals are themselves inflationary forces in commodity markets. A disciplined daily data release covering the following metrics would directly compress the panic premium:

- Hormuz transit volumes and tanker queue status

- War-risk insurance availability for commercial cargoes

- Strategic Petroleum Reserve release volumes and delivery confirmation

- Refinery utilization rates across key U.S. and allied facilities

- Crude and product inventory levels relative to seasonal norms

- Diesel and jet fuel stock positions

- LNG cargo availability and regasification slot access

- Major sanctions-license updates from OFAC and Treasury

2. Transforming the SPR Into a Predictable Market Instrument

The U.S. Department of Energy announced a release of 172 million barrels from the Strategic Petroleum Reserve as part of an IEA-coordinated 400-million-barrel emergency stock action. The EIA subsequently reported that 17.5 million barrels were released between the week ending March 20 and the week ending April 24, 2026, including 7.1 million barrels in the final week of that period. SPR stocks stood at 397.9 million barrels following these releases, structured as exchanges requiring return of the original volume plus additional barrels.

That helps, but the market requires more than volume confirmation. It requires a transparent reaction function.

Pre-announcing specific triggers under which SPR releases would be accelerated or adjusted transforms the reserve from a reactive political headline into a genuine market stabilizer. Concrete triggers would include commercial crude inventory thresholds, distillate stock levels, Brent-WTI spreads, diesel crack spreads, and tanker flow disruption metrics.

3. Prioritizing Refined Products Over Crude Benchmarks

Diesel and jet fuel power freight networks, agricultural equipment, aviation, emergency services, and military logistics chains. Crude oil alone does not. The EIA's April 2026 outlook identified diesel as particularly vulnerable given U.S. inventories sitting below the five-year seasonal average. The IEA separately flagged that feedstock disruptions and infrastructure damage were pushing middle distillate crack spreads to record highs globally.

For the next 45 to 90 days, distillates should be treated as strategic products in their own right, with targeted product swaps between allied nations and a specific focus on refinery output as distinct from crude release volumes. Understanding the broader oil market trade-war impact is consequently essential for framing these decisions within a coherent strategic context.

4. A Sanctions-and-Shipping Fast Lane for Allied Replacement Barrels

Sanctions ambiguity compounds physical scarcity by creating legal scarcity on top of it. When banks, insurers, shipowners, and refiners cannot determine whether a specific cargo, vessel, counterparty, or payment route is permissible, that barrel becomes commercially impaired even when it has no connection to sanctioned entities. The hidden sanction created by legal uncertainty is measurable in widening physical differentials.

Rapid, narrow, written guidance from Treasury, the Department of Energy, OFAC, and maritime authorities specifying exactly what can be insured, financed, shipped, blended, and paid for would eliminate this compounding effect.

5. War-Risk Insurance Support for Lawful Commercial Flows

A tanker without war-risk insurance does not move cargo regardless of military corridor protection. Reports confirmed that the CS Anthem became the second commercial U.S.-flagged vessel to exit the Strait of Hormuz under U.S. military protection, following the Alliance Fairfax. Each successfully completed and documented escorted transit provides physical-market evidence that the corridor functions, which carries direct financial significance beyond its military symbolism.

Temporary government-backed guarantees or backstop arrangements for non-sanctioned energy cargoes transiting approved corridors would reduce the panic premium attached to lawful commercial shipping. As analysts have noted, Trump cannot simply win the Strait — he must win the entire oil curve, meaning institutional confidence must accompany any military success.

6. Protecting Futures Market Integrity Without Attempting Price Control

The CFTC's position-limit framework governs 25 physically settled core referenced futures contracts, including NYMEX light sweet crude oil, NYMEX New York Harbor ULSD heating oil, and NYMEX RBOB gasoline, with commercial hedger exemptions for bona fide hedging activity. This framework exists precisely to prevent excessive concentration from distorting prices while preserving liquidity for genuine commercial users.

Intensified surveillance for manipulation, spoofing, concentrated squeezes, and suspicious options activity is appropriate and warranted. Political campaigns against market participants as a class, however, would be counterproductive. Commercial hedgers depend on speculative liquidity to execute hedges efficiently. Removing that liquidity raises hedging costs precisely when hedging protection is most critical to the real economy.

7. A Temporary Liquidity Facility for Critical Commercial Hedgers

CME's performance bond system requires margin deposits that scale with market volatility. In wartime price environments, this means that margin calls can force solvent companies to liquidate hedging positions or reduce physical procurement even when their underlying business is financially sound.

A narrowly scoped Treasury or Export-Import Bank facility, limited strictly to bona fide commercial hedgers with genuine physical exposure, would preserve hedging capacity as a national-security function rather than allowing wartime volatility to weaponize margin mechanics against the very companies that oil-dependent supply chains depend on.

8. Coordinated Allied Demand Management

The IEA's April 2026 Oil Market Report projected that oil demand would contract by 80,000 barrels per day in 2026 as a direct result of the Gulf conflict, with a 1.5 million barrel per day demand decline forecast for Q2 2026 alone, representing the sharpest contraction since COVID-19 disrupted global fuel consumption.

| Demand Impact Metric | IEA April 2026 Estimate |

|---|---|

| Full-year 2026 demand contraction | -80,000 bpd |

| Q2 2026 demand decline | -1.5 million bpd |

| Comparison benchmark | Sharpest since COVID-19 |

| Most affected products | Naphtha, LPG, jet fuel |

| Most affected regions | Middle East, Asia Pacific |

Coordinated, targeted measures with Europe, Japan, South Korea, India, and Gulf partners that reduce nonessential government fuel consumption and prioritise freight and emergency services would buy time for inventory rebuilding without triggering panic hoarding behaviour.

The Hidden Balance-Sheet Dimension

How the War Premium Functions as a Corporate Tax

There is a working capital dimension to the current crisis that receives far less attention than headline crude prices. A one-million-barrel crude cargo priced at $70 per barrel requires approximately $70 million in upfront financing before freight, insurance, letters of credit, and related transaction costs. That same cargo at $115 per barrel requires $115 million, a 64% increase in financing burden with no change in physical volume transported.

Layer margin calls on hedging positions, wider basis risk between physical and paper markets, elevated tanker insurance premiums, and tighter bank credit review onto that baseline, and the war premium becomes a direct balance-sheet constraint on energy commerce across every sector dependent on reliable fuel access. The oil price volatility guide for 2025 provides useful historical grounding for understanding how quickly these financing burdens can escalate across volatile cycles.

| Actor | Primary Balance-Sheet Exposure |

|---|---|

| Airlines | Jet fuel hedging costs; margin calls; cargo uncertainty |

| Refiners | Feedstock availability; product crack spread volatility |

| Utilities | LNG contract execution; regasification slot availability |

| Commodity traders | Cargo finance; sanctions compliance; basis risk |

| Allied importers | Replacement barrel sourcing; legal clearance delays |

The next major ASX story will hit our subscribers first

Two Scenarios for the Next 90 Days

Scenario A: The Decompression Path

If Hormuz transit volumes normalise progressively, SPR releases reach buyers on a predictable pre-announced schedule, and Washington issues clear written sanctions and shipping guidance, Brent would gradually shed the panic premium. Inventory rebuilding would proceed in an orderly fashion. Diesel and jet fuel tightness would ease. Markets would treat the conflict as a temporary logistics disruption rather than a durable structural supply risk.

Scenario B: The Structural Repricing Path

If negotiations stall or produce contradictory signals, tanker insurance markets remain impaired for non-escorted vessels, and policy communication remains ambiguous or reactive, markets will reprice oil not merely as expensive but as fundamentally unreliable. Hedging liquidity would thin. Futures-physical divergence would widen. Allied confidence in U.S. energy leadership would erode. Markets tracking oil prices in real time have already demonstrated how rapidly sentiment can shift on a single statement or headline.

Expensive oil is a demand problem that markets can adjust to over time. Unreliable oil is a systemic problem that paralyses the commercial planning of every energy-dependent industry globally. The difference between these two outcomes is not primarily military. It is institutional, communicative, and financial.

The next 45 to 90 days will determine which scenario takes hold. The United States possesses the institutional architecture, reserve capacity, regulatory tools, and allied relationships to drive the decompression scenario. Whether Washington deploys those tools with sufficient precision and discipline is the central question for those watching Trump win the oil curve — or lose it — in the months ahead.

Disclaimer: This article is for informational and educational purposes only. It does not constitute financial, investment, or legal advice. Forecasts, price projections, and scenario analyses referenced herein are drawn from publicly available government and agency reports and are subject to significant uncertainty. Readers should conduct their own due diligence before making any investment or commercial decisions.

Want To Position Ahead of the Next Major Commodity Market Shift?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly translating complex market data into actionable investment opportunities — explore historic discoveries and their returns to understand what early positioning can mean, and begin your 14-day free trial at Discovery Alert to secure a market-leading edge before the broader market catches on.