July 16, 2026

The Race to Control How Battery Metals Are Priced

Commodity markets have always been battlegrounds for economic influence. Whoever controls the benchmark controls the terms of trade, the cost of hedging, and ultimately the flow of capital across entire industries. For most of the twentieth century, that power resided in London and New York. However, the clean energy transition has reshuffled the deck, placing materials like lithium at the centre of a new geopolitical contest over pricing authority — one that China is prosecuting with calculated precision.

The planned launch of China lithium hydroxide futures on the Guangzhou Futures Exchange (GFEX) represents the most consequential development in battery metal derivatives since lithium carbonate contracts debuted in July 2023. It is not merely a financial market story. It is a strategic move embedded within a much larger project of commodities pricing sovereignty that Beijing has been building for over a decade.

When big ASX news breaks, our subscribers know first

What Makes Lithium Hydroxide Pricing So Strategically Important

To appreciate why this moment matters, it helps to understand what lithium hydroxide actually does within the battery supply chain and why its pricing mechanism has outsized consequences for the entire EV industry. Furthermore, the critical minerals demand surge reshaping global trade makes this question more urgent than ever.

Lithium hydroxide monohydrate is the critical input for nickel-cobalt-manganese (NCM) and nickel-cobalt-aluminum (NCA) battery chemistries — the cathode technologies that power premium, long-range electric vehicles. These are the batteries found in high-performance passenger cars and advanced commercial EVs where energy density per kilogram is the defining engineering constraint.

Lithium carbonate, by contrast, serves lithium iron phosphate (LFP) chemistries dominant in mass-market, standard-range vehicles where cost-per-kilowatthour matters more than energy density. This chemical distinction creates two fundamentally separate supply chains, procurement cycles, and risk profiles.

A cathode manufacturer producing NCM material for a premium automaker cannot substitute lithium carbonate pricing as a hedging reference for its lithium hydroxide exposure. The products serve different markets, carry different purity requirements, and respond to different demand drivers. Yet until recently, the derivatives toolkit available to manage these distinct risks was incomplete, particularly on the Chinese side of the market.

The table below captures the essential structural differences between the two lithium futures markets as they exist today:

| Characteristic | Lithium Carbonate (GFEX) | Lithium Hydroxide (CME) |

|---|---|---|

| Primary Battery Chemistry | LFP | NCM / NCA |

| EV Segment | Mass-market, standard-range | Premium, long-range |

| Settlement Method | Physical delivery | Cash-settled (financially settled) |

| Reference Currency | Chinese yuan (CNY/tonne) | USD per kilogram |

| Price Reference | GFEX domestic index | Fastmarkets CIF CJK assessment |

| Overseas Participation | Opened mid-2026 | Available internationally |

| Minimum Purity Specification | Battery-grade | 56.5% LiOH minimum |

The gap in China's derivatives toolkit is evident. While GFEX provides domestic hedging infrastructure for LFP-oriented lithium carbonate, there is no equivalent yuan-denominated instrument for the hydroxide market that supplies premium NCM/NCA cathode producers. Chinese battery manufacturers that use lithium hydroxide must consequently hedge using CME contracts denominated in US dollars, introducing foreign exchange exposure that partially undermines the effectiveness of the hedge itself.

How the Existing CME Contract Actually Functions

Understanding what China is moving to challenge requires a clear picture of how the incumbent benchmark operates. The CME Group's lithium hydroxide futures contract is financially settled, meaning no physical commodity changes hands at expiry. Instead, open positions are closed out against Fastmarkets' assessed price for battery-grade lithium hydroxide monohydrate meeting a minimum purity threshold of 56.5% LiOH, quoted in USD per kilogram on a CIF China, Japan, and South Korea (CJK) basis.

This cash-settled structure has proven highly accessible for international financial participants, trading houses, and producers who want price exposure without the logistical complexity of physical delivery. You can explore CME lithium hydroxide futures data to better understand the contract's recent growth trajectory.

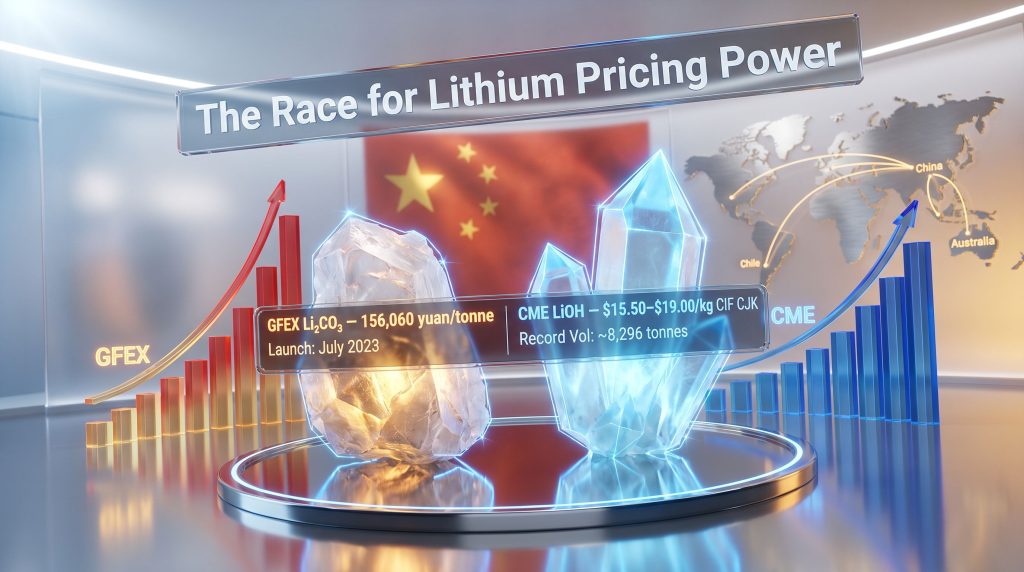

The contract has gained meaningful traction, with CME recording a record weekly traded volume of approximately 8,296 tonnes in early January 2026 — a figure that signals growing institutional interest in lithium derivatives as a risk management tool.

Price dynamics during this period were also notable. The Fastmarkets benchmark range in early January 2026 reached $15.50 to $19.00 per kilogram CIF CJK, a sharp repricing from the prior week's range of $12.00 to $15.50 per kilogram. The near-term forward curve exhibited a structure known as contango, where futures prices sit above current spot levels, signalling that the market anticipated continued tightening or demand recovery ahead.

Contango environments increase the cost of carry for participants holding long hedge positions, as rolling forward contracts from one expiry to the next typically involves buying at a premium. However, they simultaneously create roll-yield opportunities for traders with structured short positions or those providing liquidity to the curve.

This dynamic is worth understanding for any market participant considering the implications of a competing Chinese benchmark. If GFEX launches a physically delivered, yuan-denominated hydroxide contract with a contango structure that differs from the CME curve, producers and traders operating across both markets will face basis risk between the two contracts — a spread that can fluctuate independently of the underlying lithium fundamentals.

What the Evidence Suggests About China's Launch Timeline

According to reporting by Reuters published on Mining.com, two sources with direct knowledge of the matter confirmed that GFEX is actively working toward a lithium hydroxide futures launch before the end of 2026. One source indicated October as a possible debut date, while the other suggested a broader fourth-quarter window. Both sources requested anonymity given that they were not authorised to speak publicly on the matter.

The preparatory groundwork visible in exchange filings provides material corroboration of this timeline. Chinese lithium producers Chengxin Lithium and Yahua Group filed applications in June 2026 to become approved lithium hydroxide delivery warehouse operators for GFEX — a foundational requirement for any physically delivered futures contract that needs certified domestic storage facilities.

Separately, Yahua's marketing director indicated the company's intention to have its lithium hydroxide product formally listed as a deliverable-grade brand on the Guangzhou exchange. This brand listing mechanism is a well-established feature of Chinese commodity futures markets, where individual producers' output must be certified before it can be used to settle physical delivery obligations.

The significance of these preparations extends beyond administrative procedure. Warehouse certification and brand listing are typically among the final operational steps completed before a contract launches, suggesting that GFEX's internal development work is substantially advanced.

Key preparation indicators observed ahead of the anticipated launch include:

- Formal exchange filings from major Chinese lithium refiners seeking delivery warehouse certification

- Producer-level brand listing applications for specific hydroxide products to qualify as deliverable against the contract

- Exchange operational readiness assessments conducted across logistics and quality assurance infrastructure

- Analyst commentary indicating material advancement in preparatory work

- GFEX's concurrent move to open lithium carbonate futures to overseas investors, signalling a broader internationalisation strategy

China's Established Playbook for Commodity Benchmark Building

The GFEX lithium hydroxide initiative does not emerge from a vacuum. It follows a well-documented pattern that China has executed across multiple commodity classes over the past fifteen years, progressively building domestic futures infrastructure before expanding access to international participants. In addition, understanding the China steel iron ore outlook illustrates how this playbook has already played out across a different commodity class.

The iron ore futures on the Dalian Commodity Exchange provide perhaps the most instructive precedent. China, as the world's largest iron ore importer, developed domestically focused iron ore derivatives before gradually opening them to overseas traders. Over time, the Dalian contract became a significant Asian pricing reference operating alongside the Singapore Exchange's iron ore swaps, creating a dual-benchmark environment.

The yuan-denominated crude oil futures launched on the Shanghai International Energy Centre (INE) in 2018 represent an even more explicit geopolitical challenge to Western pricing dominance, directly targeting the Brent and WTI benchmarks. While INE crude has not displaced Brent or WTI, it has established a functioning domestic reference that serves Chinese refiners and traders, reducing their mandatory reliance on foreign benchmarks.

The May 2026 GFEX lithium carbonate contract settlement at approximately 156,060 yuan per tonne illustrates how the existing Chinese benchmark already carries significant market weight within domestic pricing networks, even before full internationalisation. This figure was closely watched by regional producers and traders as a reference point.

The pattern across iron ore, crude oil, and now lithium is consistent: China builds domestic liquidity first, certifies quality and delivery infrastructure, then opens access to international participants to bid for benchmark status. Each iteration of this playbook has succeeded in establishing a credible Chinese alternative to Western-controlled price references, even where outright displacement has not occurred.

The Geopolitical Architecture Behind the Move

China's rationale for establishing domestic hydroxide futures extends well beyond financial efficiency gains for its domestic industry. The country processes an estimated 60 to 70 percent of the world's lithium into battery-grade compounds, yet for years operated as a price-taker on USD-denominated benchmarks set by Western price reporting agencies. Shifts in the global lithium market have further intensified this strategic asymmetry.

This asymmetry between processing dominance and pricing influence has been a persistent source of strategic frustration within Chinese industrial policy circles. A nation that converts the majority of global lithium supply into the material that actually enters battery cells arguably has more right to anchor the pricing mechanism than a financial exchange operating in a jurisdiction with minimal lithium conversion capacity.

The establishment of yuan-denominated hydroxide futures would deliver several specific strategic advantages simultaneously:

- Chinese NCM/NCA cathode producers gain a hedging instrument denominated in their functional currency, eliminating USD foreign exchange exposure from their risk management

- GFEX gains expanded market depth and product breadth, enhancing its credentials as a multi-product battery metals exchange

- Chinese pricing agencies and assessed benchmarks gain a reference transaction base that could eventually compete with Fastmarkets' CIF CJK assessment

- International lithium producers supplying Chinese converters face potential pressure to accept yuan-denominated contracts referenced to GFEX rather than USD contracts referenced to CME

- Beijing acquires an additional instrument of economic statecraft in any future trade or supply chain dispute involving battery materials

For Australian hard-rock lithium miners, Chilean brine producers, and African emerging producers who sell into Chinese conversion facilities, the implications are particularly significant. If GFEX hydroxide futures achieve sufficient liquidity and credibility, the pricing architecture for the entire upstream supply chain could gradually shift — with consequences for how project economics are modelled, how offtake agreements are structured, and how investment decisions are made across the global lithium industry.

The next major ASX story will hit our subscribers first

Three Scenarios for How This Could Unfold

The launch of GFEX China lithium hydroxide futures does not guarantee any particular market outcome. Several distinct scenarios are plausible depending on how liquidity develops, whether overseas participation is extended, and how global market participants respond.

Scenario One: Rapid Adoption and Benchmark Displacement

If China's major lithium refiners, NCM cathode producers, and battery cell manufacturers adopt GFEX hydroxide futures as their primary hedging instrument, CME contract volumes could face sustained structural erosion. Yuan-denominated pricing could become the de facto Asian reference for hydroxide within two to three years of launch. However, this outcome requires a degree of domestic market coordination that has historically taken several years to achieve.

Scenario Two: Parallel Benchmark Coexistence

Both CME and GFEX operate simultaneously, serving different counterparty preferences. Western-oriented producers, trading houses, and OEM procurement teams continue using the CME's cash-settled USD contract, while Chinese domestic participants migrate toward GFEX. Arbitrageurs operating across both markets help maintain pricing alignment, though periodic divergences create both risk and opportunity. This is arguably the most probable near-term outcome.

Scenario Three: Limited Adoption and Fragmentation

If overseas participation in GFEX hydroxide futures remains restricted by capital controls or if domestic liquidity fails to reach the threshold required for effective price discovery, the contract may function primarily as a domestic risk management tool. This would perpetuate pricing opacity for global buyers who must navigate two partially decoupled reference prices, potentially increasing procurement planning complexity without improving overall market efficiency.

What Determines Whether the New Contract Succeeds

Several structural factors will ultimately determine whether GFEX lithium hydroxide futures achieve genuine benchmark status or remain a domestically useful but globally peripheral instrument.

Will Liquidity Thresholds Be Met?

Liquidity threshold: Sufficient open interest must develop for the contract to function as a credible hedging tool. Thinly traded contracts with wide bid-offer spreads are ineffective for risk management regardless of their official status. Building this liquidity typically requires anchor participants — whether large producers, state-linked trading entities, or major battery manufacturers — to commit meaningful volume from the outset.

Will Overseas Participation Follow?

Overseas participation: GFEX's decision to open lithium carbonate futures to overseas investors in mid-2026 signals intent to internationalise. Whether this access extends promptly to a new hydroxide contract will be critical. Without international participation, the contract cannot achieve the global price discovery function necessary for benchmark credibility beyond China's borders.

Quality standardisation: The deliverable-grade specifications must align closely with international battery manufacturer requirements. Battery-grade lithium hydroxide monohydrate requires highly consistent chemical specifications, and any misalignment between contract specifications and actual market requirements could undermine adoption considerably.

Capital controls: China's existing foreign exchange regulations and cross-border currency restrictions create structural barriers that have historically limited the internationalisation of yuan-denominated commodity contracts. Resolving these frictions will be a necessary condition for achieving genuine global benchmark status. Furthermore, the evolving battery raw materials market adds additional complexity for international participants navigating these restrictions.

Key Market Data at a Glance

| Metric | Data Point |

|---|---|

| CME Record Weekly Volume (Jan 2026) | ~8,296 tonnes |

| Fastmarkets LiOH Price Range (Jan 2026) | $15.50 to $19.00/kg CIF CJK |

| Prior Week LiOH Price Range | $12.00 to $15.50/kg CIF CJK |

| GFEX Li Carbonate May 2026 Settlement | ~156,060 yuan/tonne |

| GFEX Lithium Carbonate Launch Date | July 2023 |

| Anticipated GFEX LiOH Launch | Q4 2026 (October as possible target) |

| CME Settlement Basis | Fastmarkets CIF CJK (USD/kg) |

| GFEX Settlement Basis | Physical delivery (yuan/tonne) |

| China's Share of Global Li Processing | ~60 to 70% of battery-grade output |

| Minimum CME LiOH Purity Specification | 56.5% LiOH |

What Battery Supply Chain Participants Should Watch

For stakeholders across the lithium value chain, the implications of a functioning GFEX hydroxide futures market extend well beyond abstract questions of benchmark competition. You can track lithium spot and futures prices to monitor how these dynamics evolve in real time.

NCM and NCA cathode producers operating within China would gain access to a domestic yuan-denominated hedging instrument aligned with their functional currency and procurement cycles. This directly reduces the FX friction that has characterised their use of CME contracts. Chinese lithium refiners could furthermore use GFEX hydroxide futures to lock in processing margins in a single currency without intermediate currency conversion.

For international lithium producers supplying Chinese converters, the emergence of a credible GFEX hydroxide benchmark could introduce pressure to price offtake agreements in yuan rather than USD — shifting currency risk up the value chain toward mining entities that have historically operated with predominantly USD-denominated revenue streams.

Western automakers and battery cell buyers with procurement contracts referenced to Fastmarkets CIF CJK pricing will need to monitor whether GFEX hydroxide settlement prices and CME settlement prices begin to diverge systematically. Technologies such as direct lithium extraction could also reshape supply dynamics in ways that interact with these benchmark shifts, adding another layer of complexity for procurement teams.

The emergence of competing lithium hydroxide benchmarks is not merely a financial market development. It reflects the broader fragmentation of commodity price discovery along geopolitical lines that is becoming increasingly evident across critical minerals. Producers and buyers who understand this dynamic early will be better positioned to structure contracts, manage basis risk, and navigate the evolving landscape than those who treat it as purely a financial markets curiosity.

The launch of China lithium hydroxide futures, if successfully executed and adequately adopted, would mark the most significant structural shift in battery metal price discovery since lithium carbonate contracts first appeared in 2023. Whether it achieves genuine benchmark status will not be determined by regulatory intent or exchange infrastructure alone. It will be determined by whether real market participants — those with genuine physical exposure to lithium hydroxide prices — choose to hedge, trade, and reference the contract in sufficient volume to make it the price they trust.

Disclaimer: This article is intended for informational purposes only and does not constitute financial or investment advice. Forecasts, scenarios, and market projections discussed herein are speculative in nature and subject to change based on evolving market conditions, regulatory developments, and geopolitical factors. Readers should conduct independent due diligence before making any investment decisions.

Want to Stay Ahead of the Next Major Battery Metals Discovery?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across lithium and more than 30 other commodities — turning complex data into clear, actionable insights for both traders and long-term investors. Explore why major mineral discoveries have historically generated substantial returns and start your 14-day free trial today to position yourself ahead of the market.